There are two elements/risks to ESG investing and both are highlighted in articles in today's daily report. The first is a reminder that returns matter and this is a reference to the very high multiples that are being applied to some of the more speculative clean energy stocks where there is credit being given today for technology and scale tomorrow. As with the tech bubble, there will inevitably be companies that fail, either because they have an offering that either will not work or will not be economic or because the market moves away from what they are doing. The fuel cell stocks would be at risk if hydrogen remains too expensive to consider as a transport fuel and if batteries or bio-based fuels become the dominant solution. Equally, bio-fuels could fall out of favor if hydrogen is abundant. On the polymer side, better collection and more chemical recycling could make switching to biodegradable polymers unnecessary or uneconomic. There will be winners and losers on this basis and the better strategy is to buy baskets of new technologies rather than bet on just one.

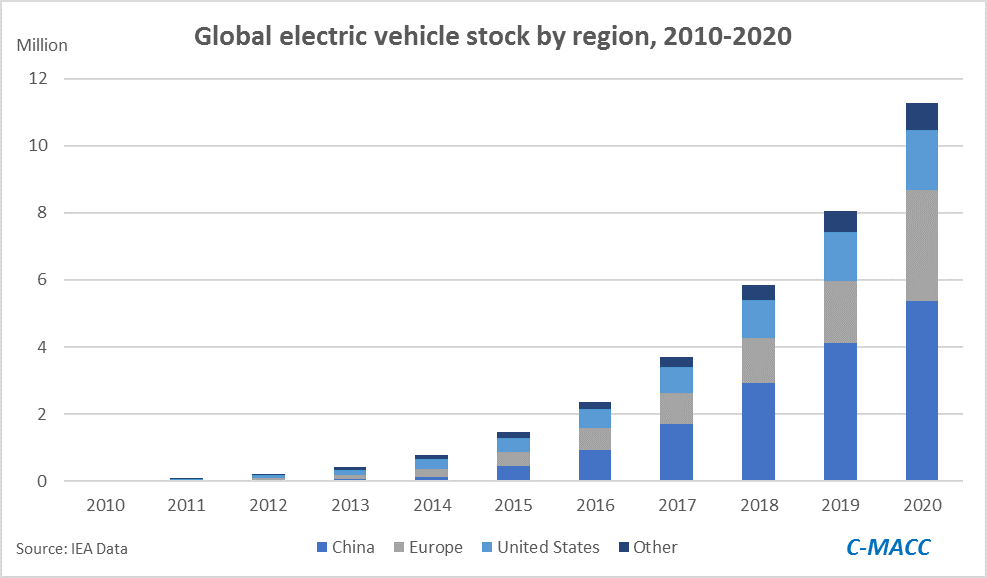

If you read our ESG and climate report which focused on the Biden agenda - The Biden Plan: Taking The Harder Path, Limiting Odds Of Success – you will understand how underwhelming the EV data is in the exhibit below. For the US to reduce its automotive transport carbon footprint to the proposed 2030 goals, the country would need to replace over 130 million ICE vehicles with EV or fuel cell-powered vehicles – 12x the total number of EVs in the world today and more than 100x the number currently in the US. This is a challenge that has almost zero chance of being met unless the benefit of switching is so high or the cost of not switching so high that consumers want to make the change – and – there are enough vehicles to buy. Both of these are remote possibilities today, but likely why we see increased focus on lithium, batteries, and faster roll-out of EVs from the majors as they attempt to do their part to move in the right direction. One unintended consequence that we have discussed at length and will cover in tomorrow's ESG and Climate report is inflation in materials, which will not be helped if the ESG lobby will not support the industries that need to provide the materials and the interlinking infrastructure investment.