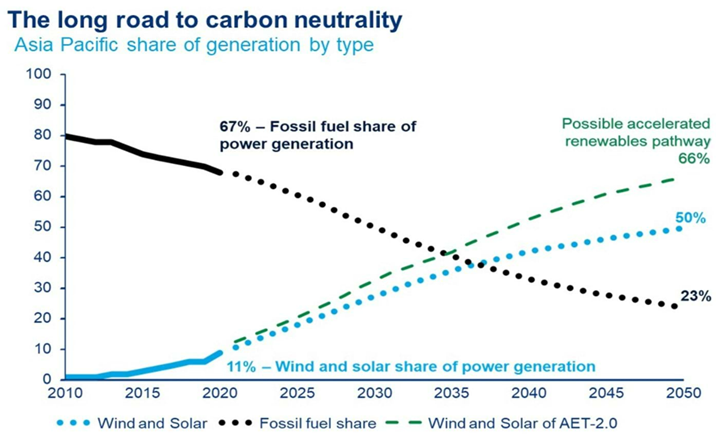

In the exhibit below, we see another chart that we find unhelpful when looking at the path to net-zero or something close. It is not an either/or game with fossil fuels and renewables. Those promoting this idea are setting impossible goals for the renewable industries, which will keep severe upward pressure on all energy costs. Wood Mackenzie may not mean what is implied in the chart below but taken at face value it suggests that more pressure will be placed on an underfunded materials market to supply an underfunded renewable power market, in which any opportunity to use decarbonized fossil fuels will be frowned upon. It would be good to see an analysis of how much global power could be generated from decarbonized natural gas and how much pressure that would take off the renewable industries.

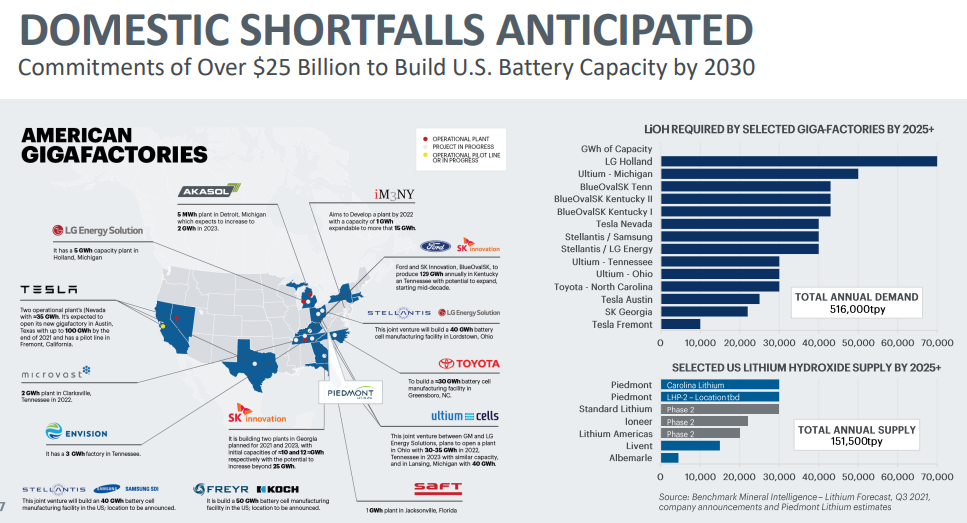

While the Piedmont Lithium analysis below makes for a compelling graphic, lithium has been a globally traded product for decades and there is an expectation that the growing lithium demand in the US will be largely met through imports. One of the significant positives of the Piedmont analysis is that it shows that US producers should have some sort of margin umbrella associated with pricing being based on import economics. That may not seem important today, given the extremely high price of lithium, but it will be important when lithium is oversupplied, which in our view is an inevitability – eventually. The barriers to entry for lithium are low and the buyer enthusiasm for new projects is very high. At some point, we will overbuild relative to demand and the net short nature of the US market may be critically important to companies like Piedmont, whose costs may not be the lowest. For more see today's ESG and Climate report.

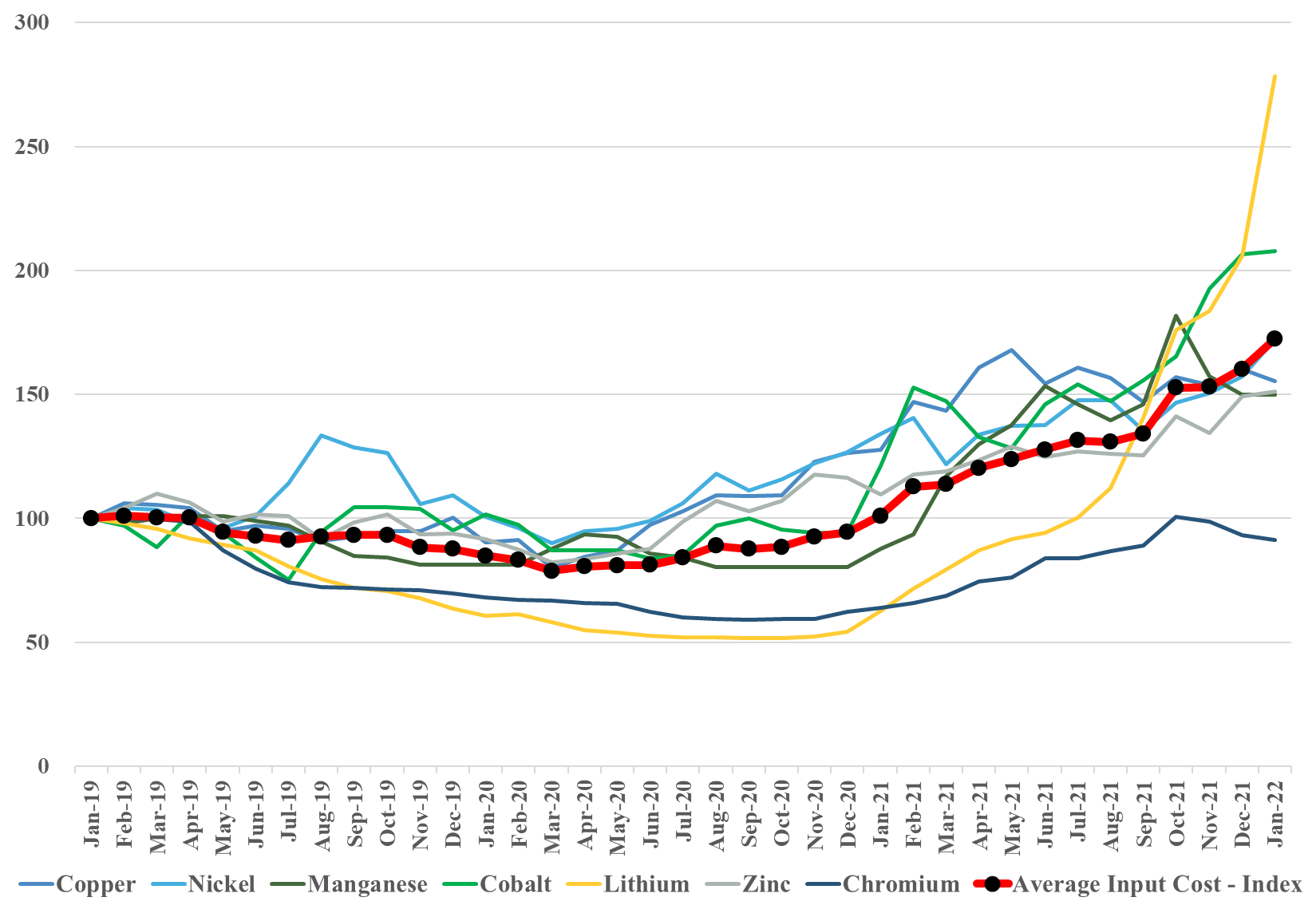

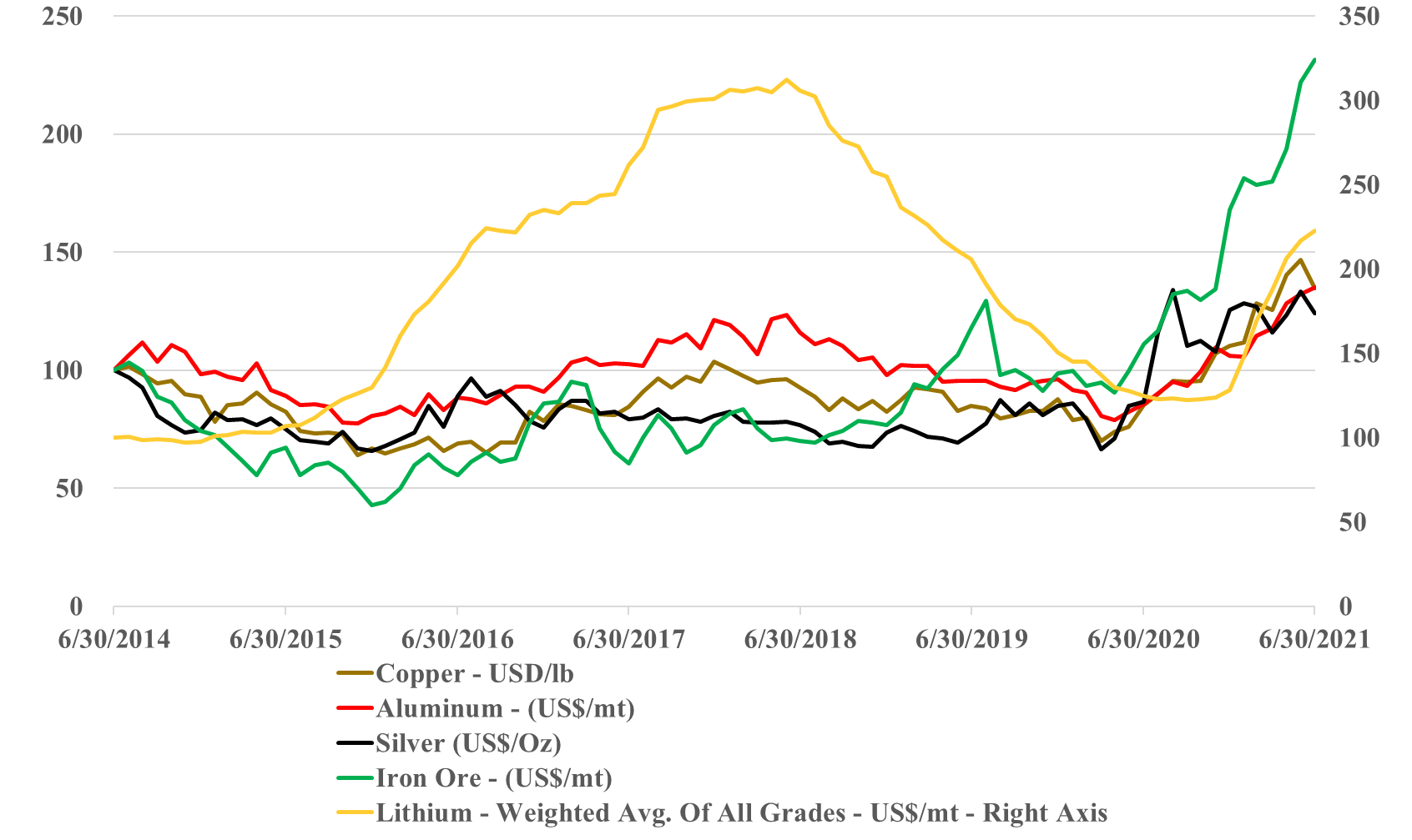

As the chart below shows, the demand, real and speculative, for lithium continues to drive prices materially higher. As new EV models prepare to launch this year and new battery facilities come online there is an inevitable supply chain impact to build inventory, whether it is the battery facilities building an inventory of lithium and other components or the automakers building an inventory of batteries. This will inflate lithium and other critical material demand relative to the vehicle output and this may be driving some of the demand panic for lithium. However, this dynamic is unlikely to be transitory in the near term, as there is a long wave of new EV capacity coming online, all of which will drive some incremental working capital build. We still believe that supply growth for lithium is very high and that the market could flip from famine to feast and back again quite quickly and frequently over the next few years although maybe not in 2022. Also see today's daily report and last week's ESG and Climate report for more on this topic.

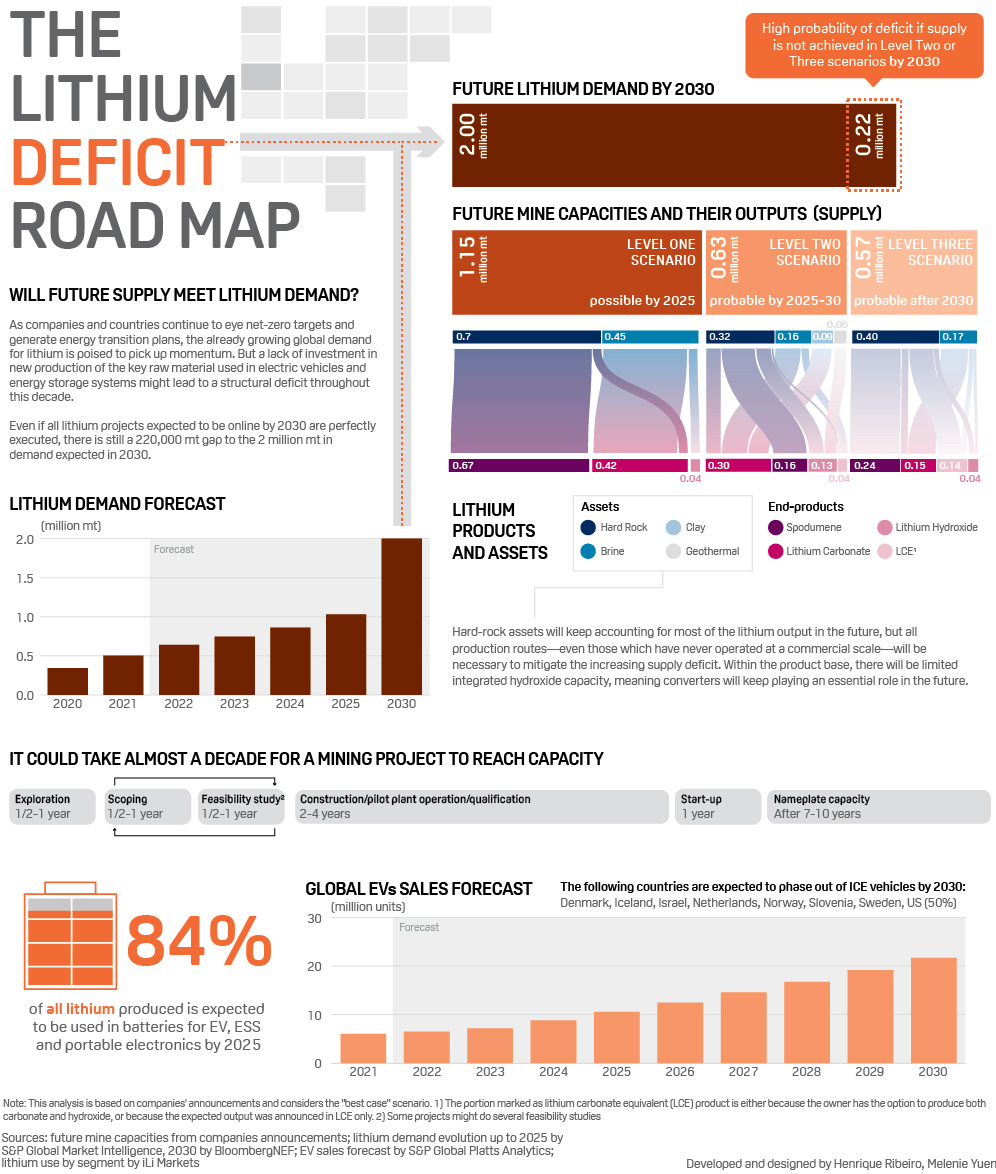

In our EGS and Climate report yesterday - Lithium – A “Special” Commodity For Now – Adding To Inflation – we talked about the current spike in lithium pricing but at the same time talked about the likelihood of lithium moving from famine to feast over the next few years and the potential for significant price volatility. This is a product for which demand growth is very high but supply growth is also very high. There are also some very divergent views of supply-demand and we highlighted a view that was bearish for lithium in yesterday's piece and show a bullish one below. The automakers and battery makers want to promote the idea that lithium will remain in short supply, as they need to encourage as much investment in lithium production as possible. While the incumbents want to keep pace with growing customer demand, they would like to see fewer new plays and are naturally conflicted in what message they want to give. We foresee supply and demand falling in and out of balance several times over the next 10+ years.

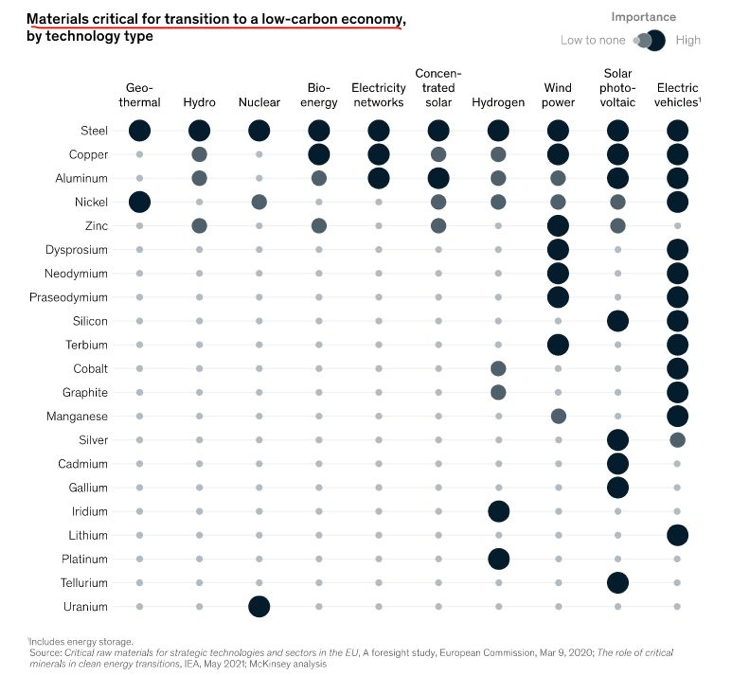

The materials chart in the exhibit below from today's daily report, is worth noting as it highlights all of the materials that are needed to advance the production of equipment required to drive renewable power production and demand. We would make one change to the chart in that lithium should also be added to the wind and solar categories to account for storage that needs to be built, although this could be done through hydrogen production or hydraulically, depending on location. One of our primary concerns concerning renewable power projections is the availability of some of these materials and we have written about the topic at length – most comprehensively in - 2022 – Policy Key, But Inflation Will Distract – Maybe Beneficially.

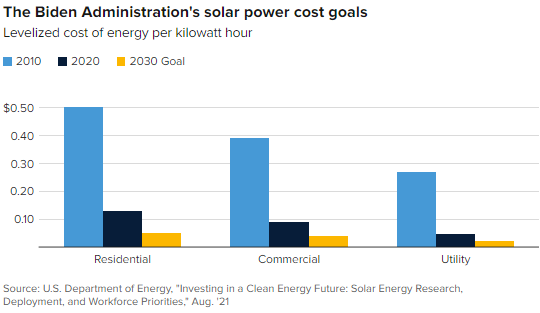

We are back on one of our pet topics today which is the reasonableness around some of the assumptions around the future cost of renewable power. We reference, work done by the US Department of Energy in the Exhibit below, and see two potential pitfalls with the assumptions around continuous improvement in solar, wind, and hydrogen costs, although there is a slight twist for hydrogen. The first is around the dynamics of learning curves. As the exhibit shows, in the early stages of any product development, there are huge leaps in cost improvements, driven by scale, better know-how, more efficient manufacturing, and in the case of solar power, both better processes for installation and some technology improvements. However, as you drive costs lower, the cost of raw materials becomes a much larger component of overall costs, and your ability to lower costs further can be overwhelmed by moves in material costs. Any inability to pass on the costs will result in economics that do not justify additional capital and you find yourselves in a commodity cycle. This is something that we have seen in basic polymers for decades, and no buyer of polyethylene today can claim that they are benefiting from a learning curve improvement. Closer to home for solar, we are seeing the same issue today in semiconductors – not enough margin to invest as everyone has been trying to push costs lower. The expectation in the DOE study and highlighted in the CNBC take on the study below is that annual solar installations in the US need to rise by 3-4X to meet some of the renewable power goals the Biden Administration is looking for by 2030, while similar growth is expected in other markets – the solar panel and other component makers have to be making good money to achieve this.

One of our concerns with the Lithium hype has been what we perceive to be very low barriers to entry – coupled with significant momentum from lithium ultimate end-users to encourage more production. If we look at the linked GM announcement, the company is making exactly the right strategic move. Providing some funding, but more importantly, high-level credibility for a new US-based project that could dwarf other US initiatives. While GM may have contracted all of the lithium volumes from this project, it is unlikely. GM’s interest, which should be aligned with all the other automakers is to ensure an ample to surplus availability of lithium long-term to keep pricing low. Investing a few million to give legitimacy to a new large project may have huge potential longer-term benefits if the capacity helps maintain a longer-term surplus market. While there may be some special sauce in the technology required to make the lithium grades for higher-end and higher density batteries, the bulk of the auto market is likely to trade range for cost in its battery decisions – and at the less expensive end, the lithium barriers are very low, with other brine-based projects under consideration and likely to find funding.