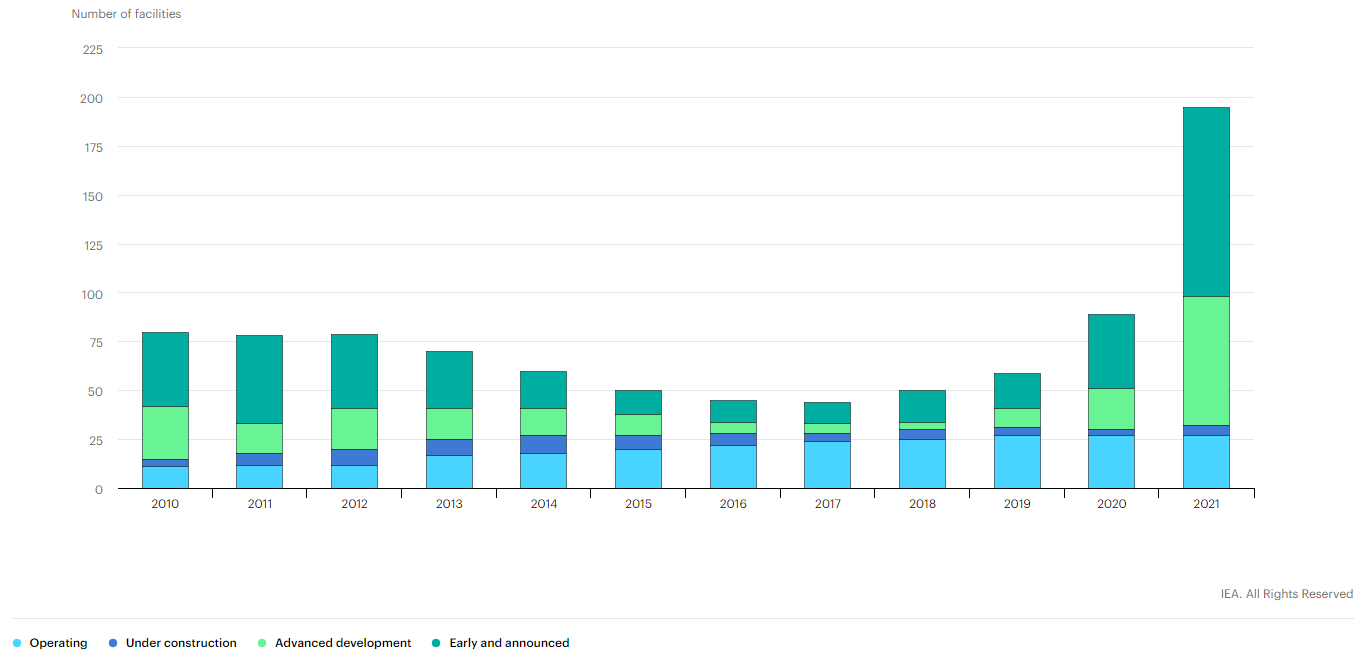

We note the IEA work on CCUS in several charts below and this is good timing relative to our ESG and climate report this week – which focused on carbon pricing, something we believe is necessary to promote more real activity in CCUS. In the Exhibit below, it is important to note how many projects are in “development” rather than operational or under construction. It is also worth noting that the number of projects under construction has not grown since 2019. One of the reasons for this is that increased activity at the planning stage is then followed by a delay associated with permitting, which depending on the region can take 2 plus years. The other constraint is uncertainty, with many of the projects under consideration waiting for something to change, either local values of CO2 or mandates or direct government support. For example, the large project planned for Houston and championed by several oil, power, and chemical companies is unlikely to move forward without a higher tax credit for CO2 sequestration or without some other incentive. The mid-West projects targeting the ethanol industry will also need permits, not just for the wells but also for the many hundreds of miles of proposed pipelines.

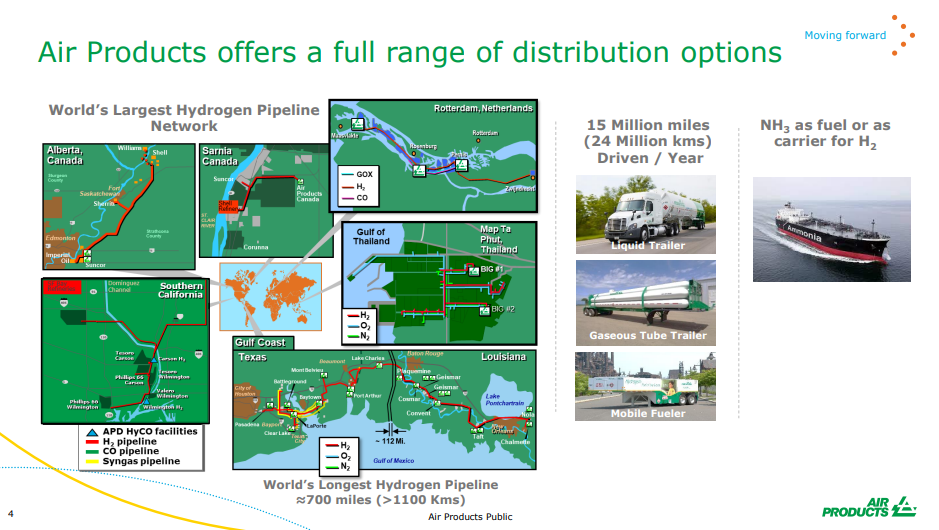

We expect to see a step up in chemical companies parading their green credentials – or plans for more green credentials, not just because COP26 is ahead but because it has now become a competitive issue. Dow’s view that it may be able to sell low carbon polyethylene in the US at a premium to regular polyethylene reflects a fairly rapidly changing narrative with customers, many of whom are also trying to accelerate their green credentials. For a couple of years, we saw packaging companies, for example, talk in broad terms about ambitions around recycled/renewable content, carbon footprints, etc. Now we are seeing the results of them trying to put their ambitions into practice and they are looking for tangible solutions from their suppliers to help them meet the pledges that they have made to consumers. For many of the packagers, the cost of the packaging is a very small component of the product cost and we would expect the packagers to look at more expensive packaging solutions if it gives them a better label. In the Air Products chart below, the company is using the La Porte start-up to remind us that it is already a huge player in hydrogen and hydrogen infrastructure. See our recent ESG and Climate Report.