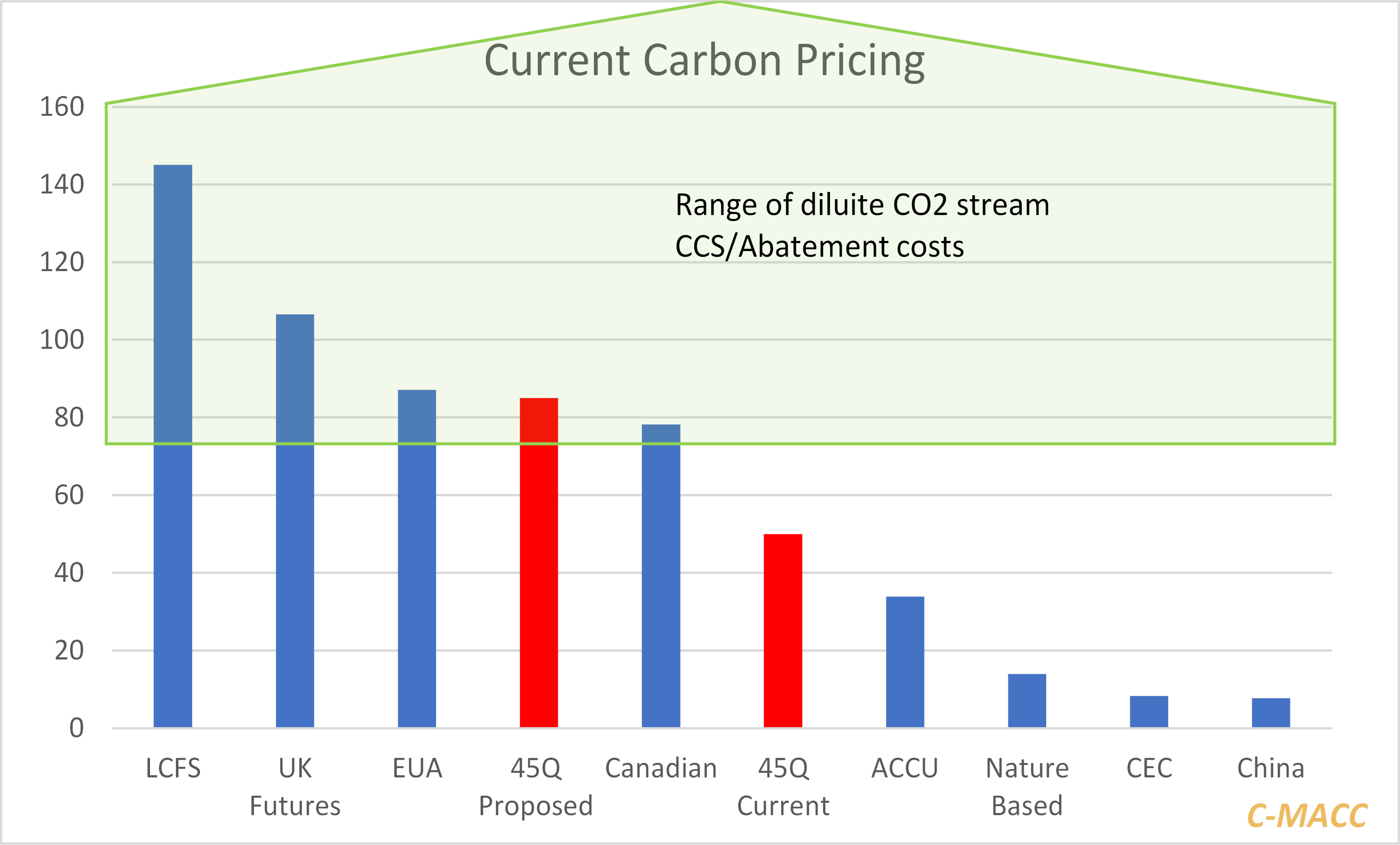

Despite the “soaring” carbon offset market in the FT article linked here, we would remind clients that this is something we have written about extensively and that while “nature-based” offset prices have jumped over the last year they remain very low compared to the physical cost of carbon abatement, whether through reforestation or physical abatement for CO2 emitting fuels and processes. The nature-based credits should at least rise to the physical cost of planting trees and maintaining forests (adjusting for the risk of fires etc). This is well above $50 per ton in our view and maybe as high as $100 per ton depending on how you define the costs. The very low price today, despite the recent rise, reflects an oversupply of credits perhaps, but it may also reflect buyers' unwillingness to pay more because of the uncertainties around accuracy and chain of custody of the credits. If the credit truly reflects the removal of 1 ton of CO2, at $14 per credit, someone is subsidizing the credit – maybe those planting the trees. The chart below shows carbon values at the end of December. See our ESG and Climate report No 57 for more.

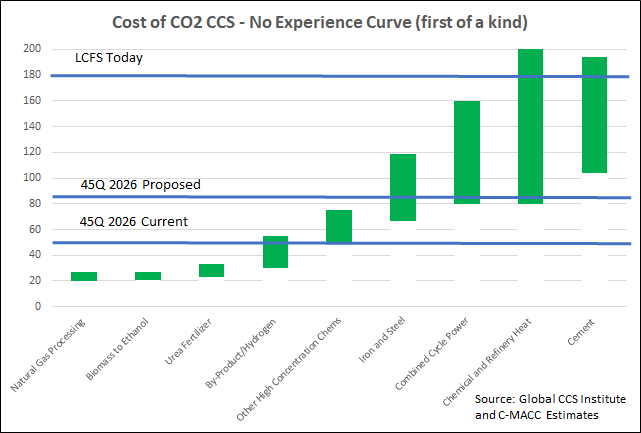

ExxonMobil is seriously upping its lower-carbon game with the CCS announcements over the last few weeks and the release this week that states the company will spend $15 billion over the next 6 years on lower carbon initiatives. In this linked headline ExxonMobil states that it will meet its 2025 emission goals this year – we are assuming that this must be correct as the company would not want to risk the accusation of greenwashing. Either way, the critics will weigh in, either claiming “greenwashing” or suggesting that the targets were not high enough, to begin with. The ExxonMobil focus is very much on CCS, which makes sense for an oil and gas-centric company whose only real play right now is to lower the carbon footprint of its fuel portfolio. In the release linked above, ExxonMobil also talks about biofuel and hydrogen initiatives, but again calls for supportive policies from governments and we suspect that the underlying push here is towards the US government. ExxonMobil and others have indicated that $100 per ton is the right incentive to drive CCS and other carbon abatement strategies and we would agree with this estimate as it backs up much of the work that we have done over the last year. See - Carbon: Trading, Offsets, and CCS as a Service – It’s All Coming! and - Carbon Games – Appetite, But Not Enough Hunger Yet. The other reason why ExxonMobil and others would like to see the US act is because other jurisdictions in which they operate will likely take a lead from the US.

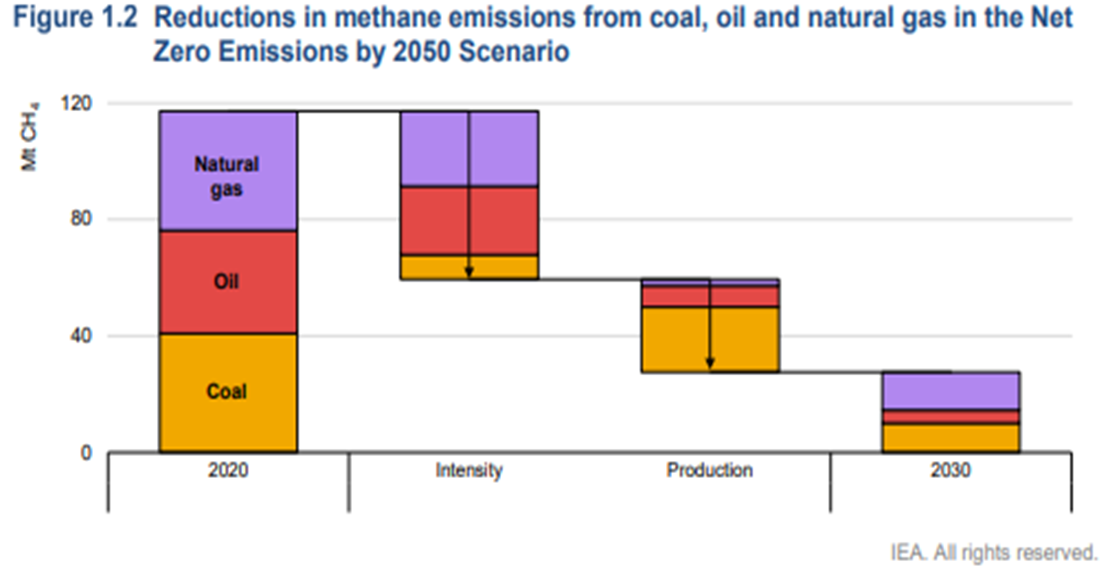

A couple of things worth highlighting in today's daily report – the first being Chevron’s move to join the net-zero club – focusing all eyes now on ExxonMobil in particular but also the rest of the US E&P crowd. Chevron will have some major challenges getting to net-zero and will likely face much of the same skepticism that bp, Shell, and TotalEnergies attracted in Europe initially and still face today. The Europeans have placed a lot of their bets on moving into renewable power – for the moment, Chevron is focused on moving to net zero in its own operations, which we read as biofuels and a lot of CCS. Given the acute shortage of international natural gas, it would make the most sense for the independent natural gas E&P companies and the LNG sellers to jump on the same boat. By promising low carbon natural gas and LNG, the industry is much more likely to gain support for the expansion that the world needs to counter some of the EIA assumptions around coal and petroleum product use from 2030 to 2050. Of course, it would be a whole lot easier for the US industry to do this if they had a value on carbon to work with! The chart below looks at one of the core clean-up issues, which is methane leakage. This is a subject we cover extensively in our ESG and Climate service linked here.

There have been some disappointing headlines out of the UN climate meeting this week, which is intended to pave the way for some of the COP26 discussions and come up with proposals that are likely to be agreed upon at the meeting. Most of the issues are around who is paying for what and whether developed nations are investing enough to help developing nations, using the guidelines put forward when the Paris Agreement was signed. In the US, the climate agenda and the Biden plan are bogged down in Congress and the plan is unlikely to pass in its current form.