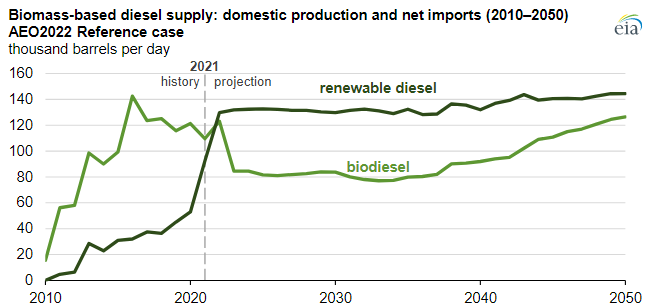

The EIA renewable diesel projections are based on a couple of things – who plans to make it and who will pay for it. All eyes are focused on the California market today as that is where the incentive lies – through the LCFS credit – and production plans plateau associated with that opportunity. As other states in the US adopt similar programs – which seems likely – we would expect to see production plans increase and the EIA will likely adapt its market view model and the chart will change. Note the dominance of renewable diesel over time, and this is where we would expect all future growth to occur. The plug-and-play nature of renewable diesel makes it a far more attractive option for refiners assuming the cost works. See more in today's daily report.

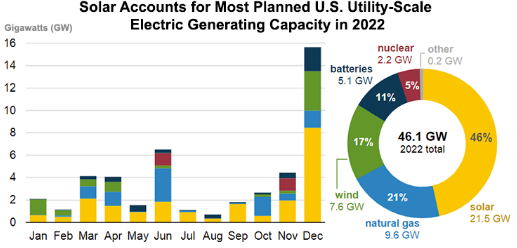

The back-end loading of the power projects for the US for 2022, as shown in the chart below leaves us somewhat skeptical concerning how much will come online this year. Supply chain problems and materials costs and availability are causing all sorts of problems with renewable power projects and installed capacity expectations for 2021 were too ambitious. We believe that companies are pushing projected start-ups later in the year to give them more of a chance of completion, but this creates the risk that they slip into 2023 or beyond. The most significant issue here is that as these plans get delayed, natural gas demand goes up, as one of the swing suppliers. This is fine as long as the US natural gas industry and shale oil industry is investing so that gas availability rises. Otherwise, we could see gas prices spike in the US next winter and another year where we use more coal than we expected. For more see this week's ESG and Climate report.

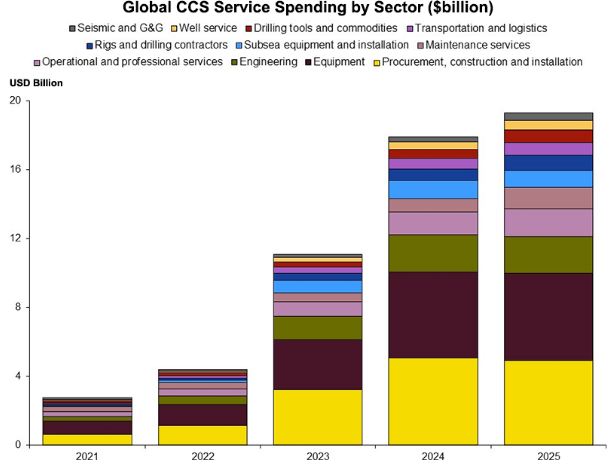

One of the subjects that we will cover at length in the ESG and Climate report tomorrow (to be found here) is the significant need for CCS globally, but especially in the US, as we see more balanced forecasts of energy supply emerging which show more use of fossil fuels for longer – especially, but not limited to natural gas. These forecasts recognize the current energy momentum as well as some of the more practical realities around the rate of construction of renewable capacity relative to energy demand growth. The CCS plans that are appearing all over the place are nothing more than plans right now and if the EPA permit activity is a true barometer – not much has moved beyond planning. This needs to change and we likely need both an increase in CCS incentives – which could take many forms – as well as some streamlining around the permitting process. Simply waiting and hoping for a renewable miracle is not going to work – nor is some sort of CCS cost breakthrough.

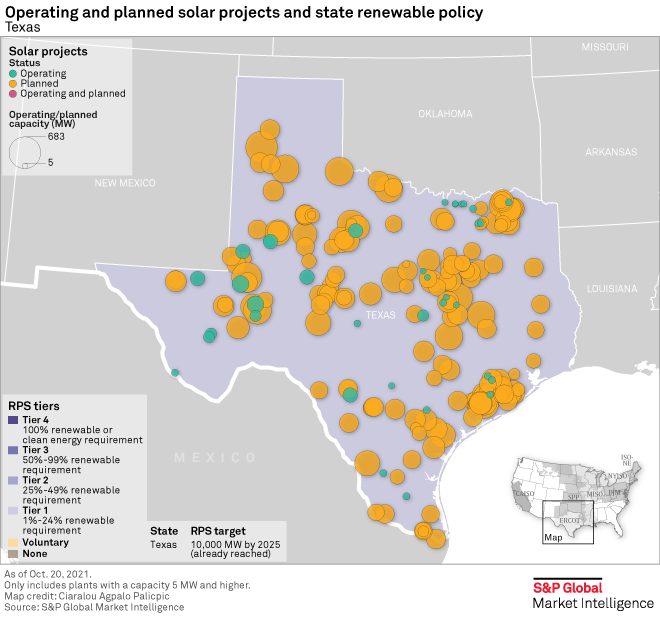

We struggle with both of the charts below, as we see the rate of potential renewable additions as far too optimistic, not because of a lack of capital, but because of a lack of materials and the knock on effect that this could have on capital if project costs increase meaningfully or if timelines extend. The solar expansions planned for Texas for example all require solar modules and there is simply not enough capacity to make these modules and in many cases not enough raw materials. All of these projects are not planned for the same year, but regardless, when you add the Texas plans to plans all over the World, you have an annual rate of addition that the equipment makers will not be able to meet. Today, many of the projects are in the planning and financing stage and the installers have yet to go looking for equipment – when they do, they may have to rethink.