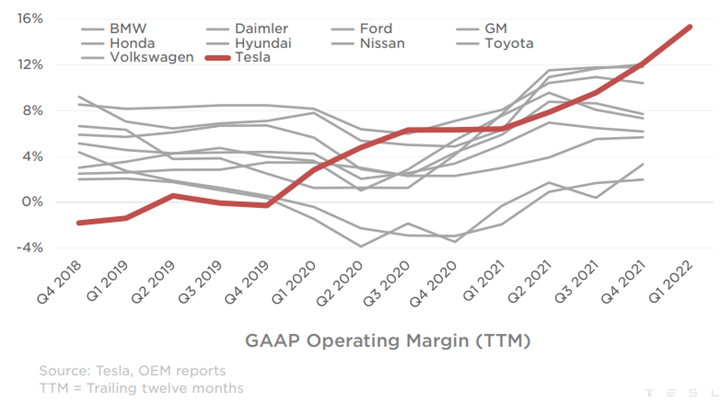

Tesla is on a roll, and showing other EV makers what is possible. The company priced its vehicles to be profitable at lower volumes and is currently seeing the benefit of scale, likely to be enhanced further as the manufacturing footprint grows. While the operating margin below looks very good, we would note that Tesla is not done scaling yet so there is considerable upside to the margin, most likely. One obvious conclusion from this analysis is that Tesla has plenty of wiggle room on pricing should macro conditions impact new car sales or should other EV makers try to steal share with pricing. Tesla has built a huge first-mover advantage in EVs and this will likely benefit the company for many years to come as long as they keep making vehicles that people want.

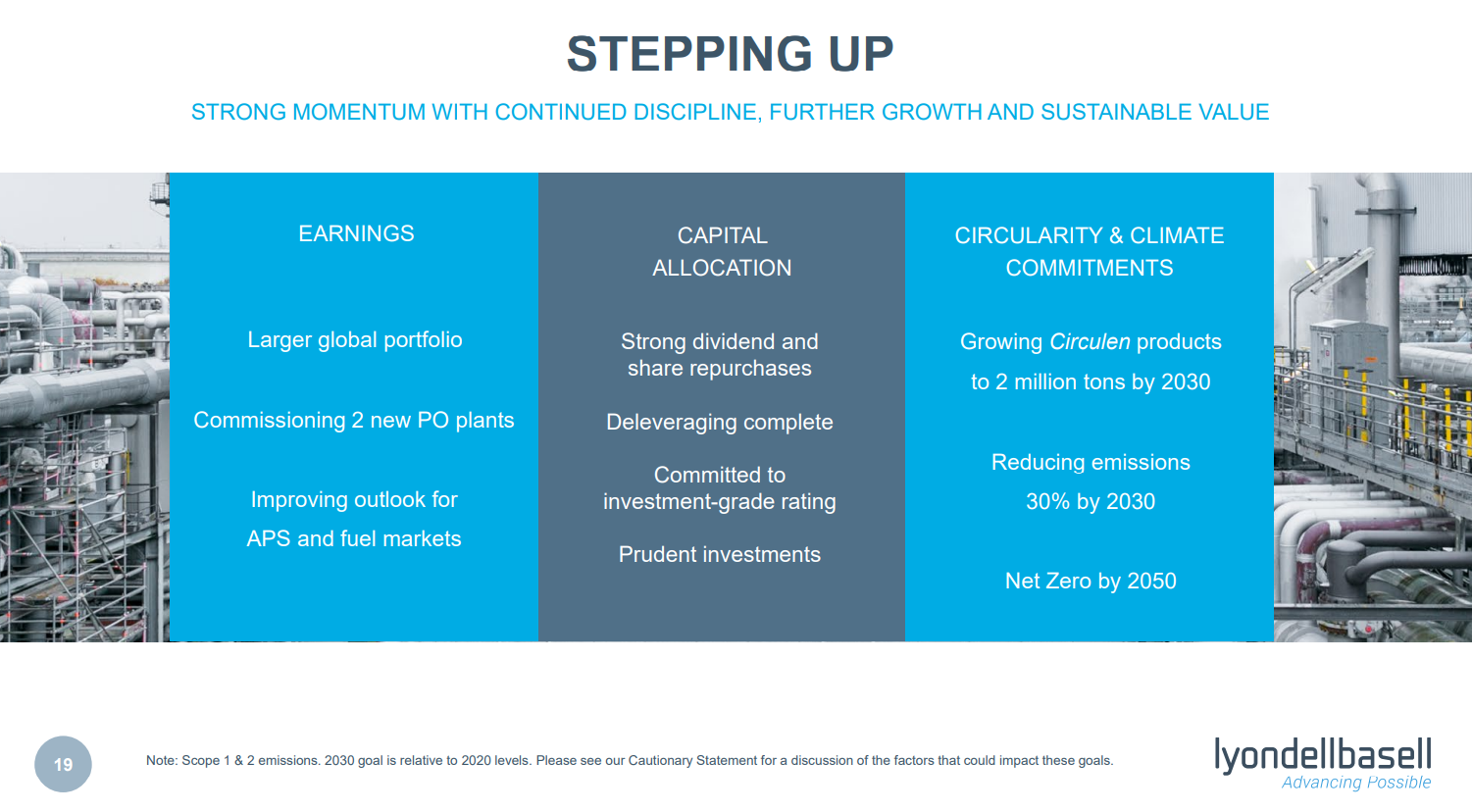

Given the lead time to get some of the emission abatement projects in place – whether it be renewable power or hydrogen with carbon capture – many of the 2030 goals that we see, like the LyondellBasell chart below – are likely to be just that – plans for 2030, with not much in the years in between. We see very little CCS coming online in the US over the next 5 years because of permitting and because of the lead time for any large hydrogen or power project that might be associated with the CCS. Not too many companies seem interested in cleaning up existing CO2 streams and are more interested in building alternative capacity that generates easier to capture CO2 – such as hydrogen from an ATR. These are expensive and long lead-time projects. LyondellBasell, ExxonMobil, Dow, and others might meet their 2030 targets but it might all happen in 2029/30.

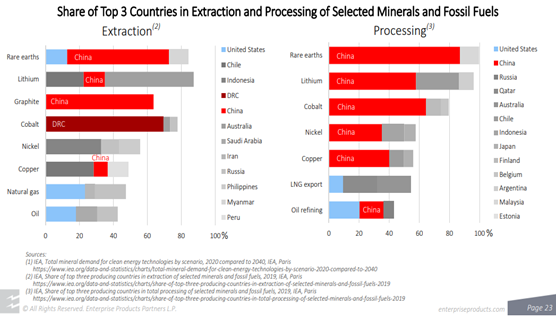

While longer-term use of oil and gas products is in Enterprise Products' best interest, it is nice to see someone else pushing the point that we have been making for more than a year – that there is not enough material out there, in the right locations, to meet the suggested clean energy goals. It is important that this becomes better understood and accepted by a broader group than just Enterprise and C-MACC, as we will not get the needed tack in strategy, priorities, and incentives if there is a broad reliance on renewable targets that will not be met – we focus on the IPCC report in tomorrow’s ESG and Climate report.

Looking at the Sempra chart below, we reflect on some research that we wrote several months ago that talked about a lost opportunity in the US because of the lack of cooperation and coordination in Washington. Energy demand is growing, the demand for materials is growing and the demand for re-shoring is growing, and if the US political and permitting system is either too hostile towards new investment or too cumbersome companies will look for workarounds. The Dow investment in Canada was partly justified by the easier regulatory environment as well as the proposed carbon price. Sempra is looking at Mexico because the ease of permitting for LNG is advantageous and we note Mattel's “near-shoring” in Mexico rather than reshoring. The opportunities for both Mexico and Canada are very significant if we remain mostly directionless in the US. For more see today's daily report.

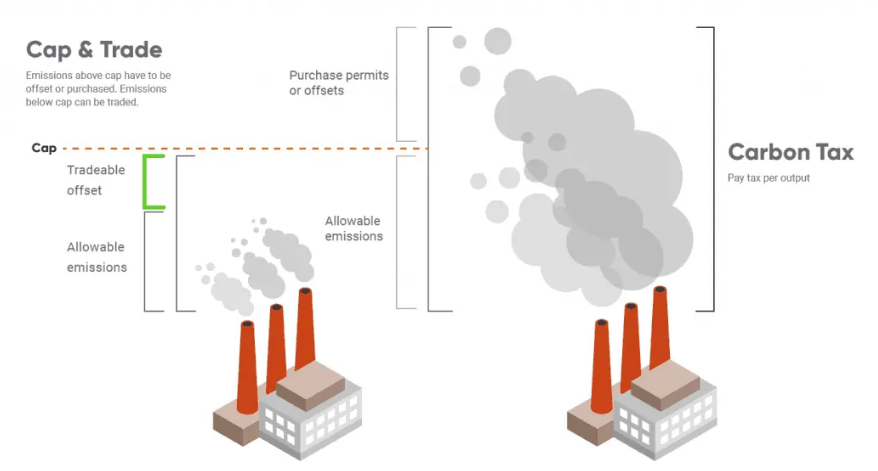

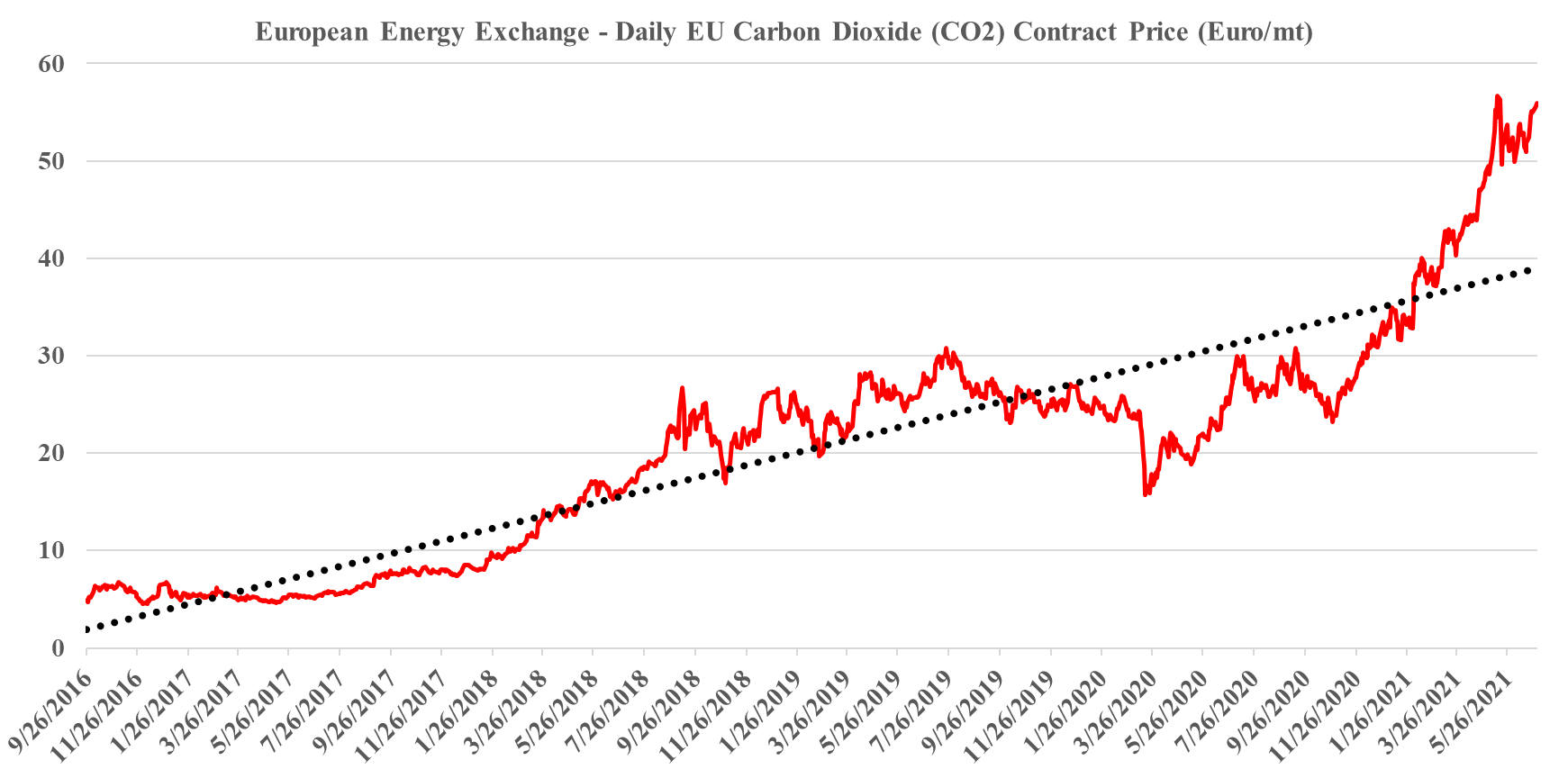

There was a very strong focus at the WPC on the need for carbon pricing in the US to facilitate investment decisions around many initiatives focused on carbon abatement. The consensus was very much that a carbon price – so a cap and trade system like they have in Europe – was the best mechanism, and far more likely to drive action and limit inflation than a carbon tax. This is something that we broadly agree with but the US is a bit late to the game and the right caps need to be set so that CO2 prices don’t languish at very low levels for years, as they did in Europe. Jim Fitterling of Dow was somewhat provocative in his comments around nuclear power, but we see this as part of a broader initiative aimed at getting a serious dialogue moving around how we make the practical steps needed to drive carbon lower. Nuclear power provides stable baseload and is carbon-free – a small modular nuclear reactor could generate enough steam and enough power to drive the decarbonization of major chemical complexes – one investment for example could transform one of the larger Dow sites. If we are going to get to net-zero targets without nuclear, we need much more progressive policies – especially around carbon pricing – which is likely the direction that Dow would like to take the discussion.

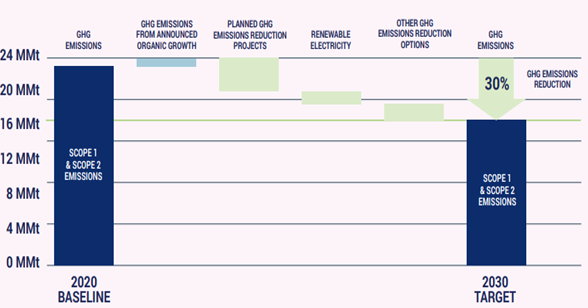

2022 is the year in which the rubber will need to meet the road for many of the chemical and other material and industrial companies who have made 2030 emission pledges. In the Dow release yesterday, the company used the call as an opportunity to remind investors about the Canada investment and tie that into the 2030 emission goals. We note LyondellBasell’s 30% emission reduction goal by 2030 and like others, LyondellBasell will not be able to get there without substantial investment. LyondellBasell and others do not necessarily have to spend in 2022 (neither does Dow), but unless there are some concrete plans by the end of the year stakeholders will likely start to question whether the emission goals are real. We suspect that most companies are trying to work out whether investments in hydrogen (likely blue hydrogen because of the volumes needed) are a better solution than trying to capture CO2 from a natural gas furnace. Any large hydrogen investment with associated CCS will take 5-6 years from concept to production. Like Dow, we would expect others to focus emission-reduction investments in countries/states that have a clear value on CO2. See today's daily report for more.

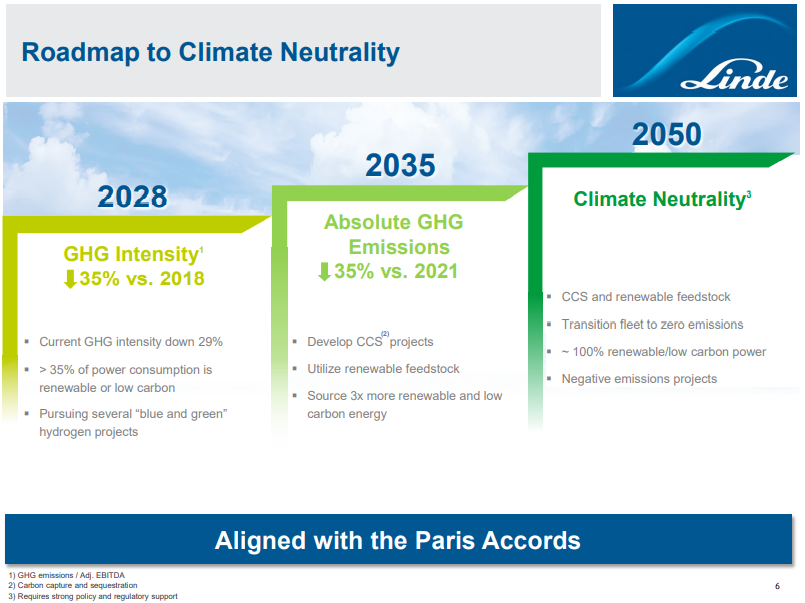

It is interesting to contrast Linde and LyondellBasell with Air Products and Dow. Air Products and Dow have transitioned away from the more generic messaging around broad objectives, and while they still have them, have started talking about concrete plans and spending aimed at lowering carbon emissions. Dow has a project on the books that will lower the emissions of existing capacity while Air Products is talking about greenfield low carbon investments at this point. Many of the commentators and climate activists are calling for concrete plans as opposed to broad objectives and we suspect that most of the narrative will move that way across energy and materials.

The Dow chart below was included in the presentation around the Canada project and repeated today in the earnings call. We have talked about the Canada project at length as well as the more recently announced Air Products blue hydrogen project in the US. The more interesting debate from here is what will happen next. Are Dow’s and Air Product’s phones ringing off the hooks with potential customers saying “we want some of that”, or is it quieter? We suspect that the phones are ringing and ringing a lot. Perhaps because people genuinely want the low carbon polyethylene or hydrogen, but also perhaps because users of polyethylene and hydrogen are likely obligated to find out more so that they can explore both the opportunities of buying from Dow or Air Products, or evaluating what their alternatives might be. We suspect that a surge in genuine customer interest is likely, good for both Dow and Air Products, but also good for others either considering decarbonizing projects or offering a carbon-free alternative already. See our ESG and Climate piece from yesterday for more on this.

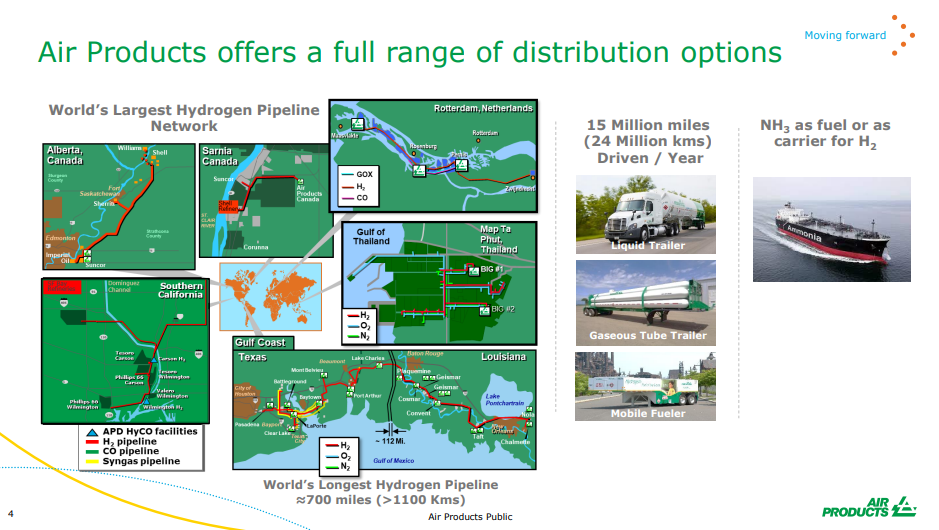

We expect to see a step up in chemical companies parading their green credentials – or plans for more green credentials, not just because COP26 is ahead but because it has now become a competitive issue. Dow’s view that it may be able to sell low carbon polyethylene in the US at a premium to regular polyethylene reflects a fairly rapidly changing narrative with customers, many of whom are also trying to accelerate their green credentials. For a couple of years, we saw packaging companies, for example, talk in broad terms about ambitions around recycled/renewable content, carbon footprints, etc. Now we are seeing the results of them trying to put their ambitions into practice and they are looking for tangible solutions from their suppliers to help them meet the pledges that they have made to consumers. For many of the packagers, the cost of the packaging is a very small component of the product cost and we would expect the packagers to look at more expensive packaging solutions if it gives them a better label. In the Air Products chart below, the company is using the La Porte start-up to remind us that it is already a huge player in hydrogen and hydrogen infrastructure. See our recent ESG and Climate Report.

The ESG investment shakeup could be one of the major events of this year, and as many of the headlines in our daily report suggest, there is a lot of work to be done, whether it is agreeing on a common set of measurement metrics – note the US and European differences discussed in one story – or the introduction of more empirical methods to judge whether what is labeled as an ESG investment fund is labeled correctly. There is also the issue of comparable disclosures, especially for companies in complex industries. It is interesting to note that in many analyses we see around carbon footprint or greenhouse gas emissions, and the potential routes to and cost of abatement, the chemical industry is omitted, except for ethanol and hydrogen. This is despite the industry accounting for 15% of the non-power emissions in the US industrial sector (similar in size to refineries). We believe that this is because the complexity of the industry makes it hard to model, and analysts choose to exclude it because they are not sure what they are doing.