Much of the core focus of both our chemical industry and ESG and Climate research recently has been on inflation and materials shortages; we would point you to: Inaction, Caused By Inflation Fears, Is Driving More Inflation! and Coming Up Short: Materials Availability To Limit Climate Progress. This linked article suggests that, as we have predicted, cost and availability pressures are taking a toll on solar installation plans for 2022 in the US. While the inflation piece is real and the product shortages highlight some of the capacity constraints for materials and panels, the broader conclusions that can be drawn from the headline are more concerning. These shortages (and higher prices) are coming well before we see any step change in attempts to increase renewable power installations associated with all of the green hydrogen projects that have been announced over the last 6-9 months. All of these investments are relying on the deflationary trends continuing, especially for onshore wind and solar.

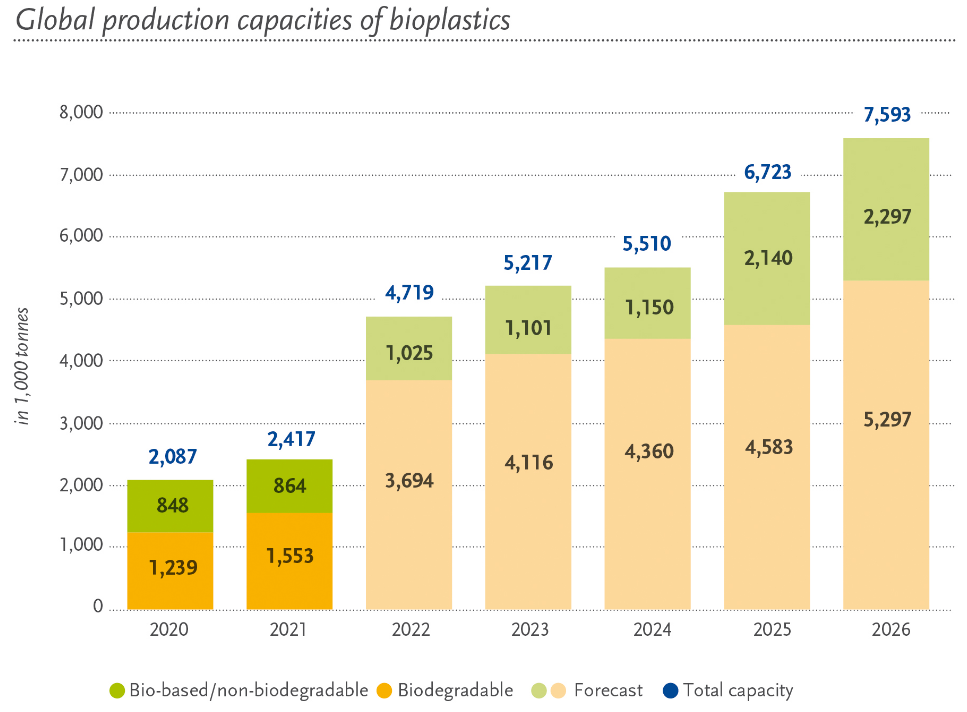

The bioplastics chart below (from today's daily report) is interesting from a couple of perspectives, the first being whether the projections are reasonable and the second being the significance of the investments. We believe that the volume targets are optimistic, given the capital requirements and that many of the companies pursuing bioplastics are relatively new and need to borrow most or all of the capital needs. The volumes would be easier to believe if the participants were large companies with strong balance sheets. The second point is just how small the volumes are in the grand scheme of plastics. Global demand for plastics exceeds 300 million tons and consequently, the 2026 projection would account for only 2.5% of global polymer demand. Note that in the article (linked here) around the uptake of biodegradable plastics – in this case in the UEA – one of the constraints to growth listed is availability. The other constraint, which likely faces producers in all markets is consumer education. Introducing a new polymer – or range of polymers – into an already confusing mix will require consumer education around what is biodegradable and what to do with the material. This topic follows on from the recycling theme in last week's ESG and Climate Report.

Our concern with the very encouraging charts below is that it is easy to join the group today, as there is no requirement to have a granular plan as to how you achieve net-zero. Many of the companies on the list may have the best intentions, but to get to their targets many need technology advances that are at best in laboratories today, and many need pricing structures – either incentives or penalties that make the right path forward more obvious. A lot of this does not exist today and the timeline to getting some of it done is being extended by political log-jams and differences of opinions. As time passes, the 100 or so companies that have signed the pledge are going to have to, at a minimum, explain what they are going to do and shortly thereafter, start committing capital.

We focused on several aspects of carbon in our ESG and Climate report yesterday and we see several headlines today that focus on carbon and storage, whether it is the blue hydrogen project in France or the Chevron interest in CCS. Chevron has some experience with CCS with the Gorgon natural gas project in Australia and while the company has been criticized recently for falling short of its capture goals for the facility – we believe that all learning experiences are valuable, and what happened in Australia likely leaves Chevron better equipped than many to pursue successful projects going forward. The likely disappointment for Chevron will be the lack of investor appreciation that it may get for the initiatives, as the focus will remain on the scale of fossil fuel exposure – see our Sunday Piece from this week. The barrage of announcements from Chevron is likely in response to the investor pressure that the company (and the industry) is under, but as we discussed on Sunday, it may not make a difference – it did not for Shell in the eyes of the Dutch court.

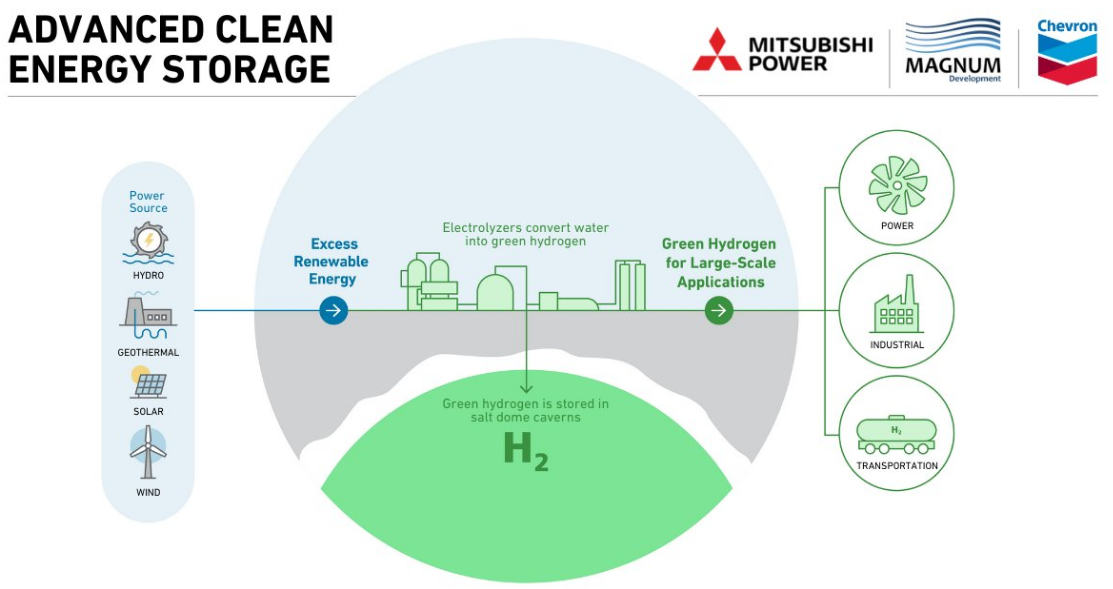

The Engine No1 headline and the Chevron headline are not necessarily the right way to think about the challenges for Chevron and whether or not the challenges are just really beginning for ExxonMobil. The Engine No 1 approach to ExxonMobil was not ESG focused and hit on a larger issue of very poor shareholder returns, with ESG/Climate only one-line item on a list. What Engine No 1 is doing now, is focusing more specifically on climate, and ExxonMobil is likely as large a target as Chevron on this basis. Last week in our Sunday report, we commented on how good the Chevron Gevo deal was for Gevo, but that it did not move the needle for Chevron. Chevron, ExxonMobil, and others are aggressively pursuing renewable fuels, mostly from waste and vegetable oils until the Gevo agreement, and there is another headline today about Chevron pursuing CCS opportunities with Enterprise and the chart below discusses a green hydrogen plan for Chevron. All of these initiatives do not sum to something that investors will take note of for any of these companies yet, and while they might be important building blocks towards a net-zero future, larger tangible investments are probably needed to get any investor buy-in. In the meantime, the activists have a lot of room to work.

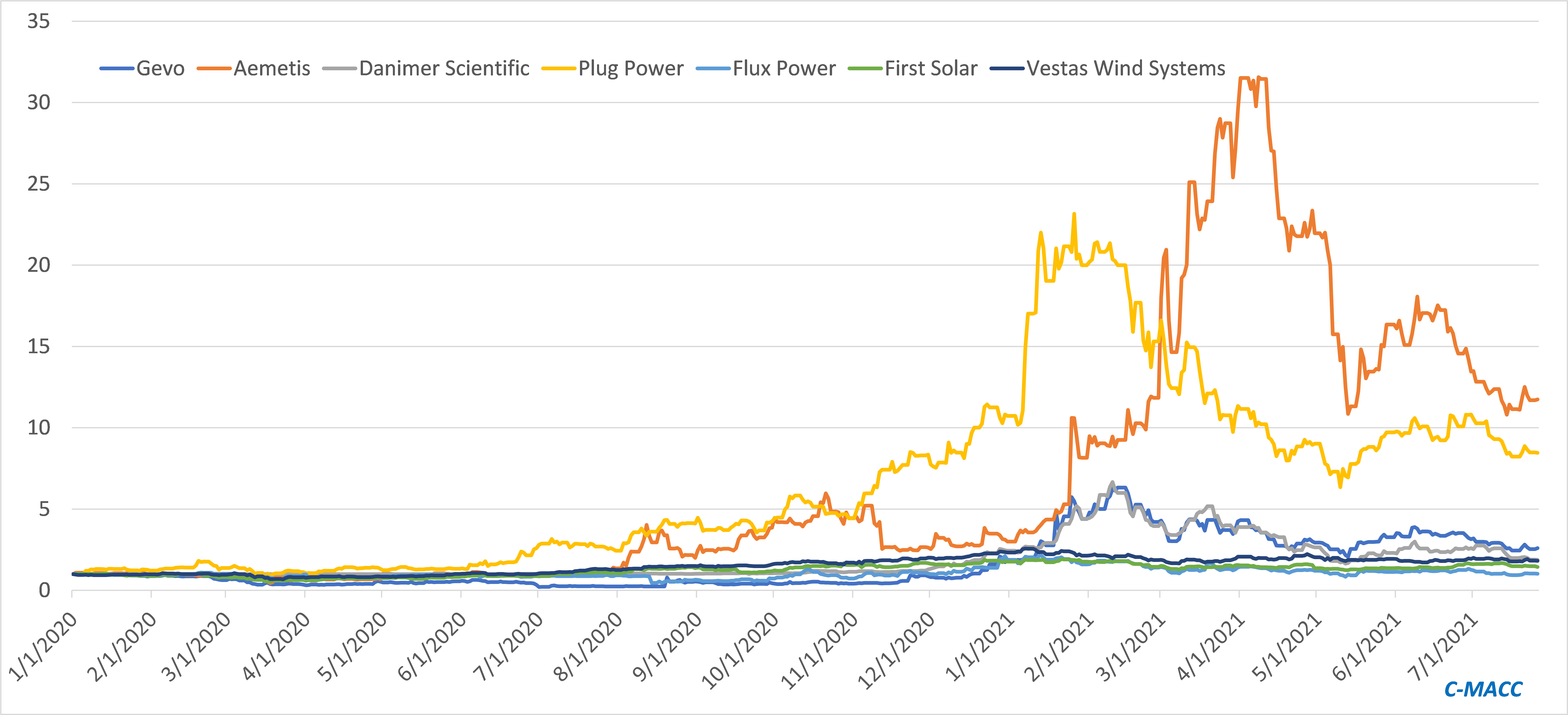

There are two elements/risks to ESG investing and both are highlighted in articles in today's daily report. The first is a reminder that returns matter and this is a reference to the very high multiples that are being applied to some of the more speculative clean energy stocks where there is credit being given today for technology and scale tomorrow. As with the tech bubble, there will inevitably be companies that fail, either because they have an offering that either will not work or will not be economic or because the market moves away from what they are doing. The fuel cell stocks would be at risk if hydrogen remains too expensive to consider as a transport fuel and if batteries or bio-based fuels become the dominant solution. Equally, bio-fuels could fall out of favor if hydrogen is abundant. On the polymer side, better collection and more chemical recycling could make switching to biodegradable polymers unnecessary or uneconomic. There will be winners and losers on this basis and the better strategy is to buy baskets of new technologies rather than bet on just one.

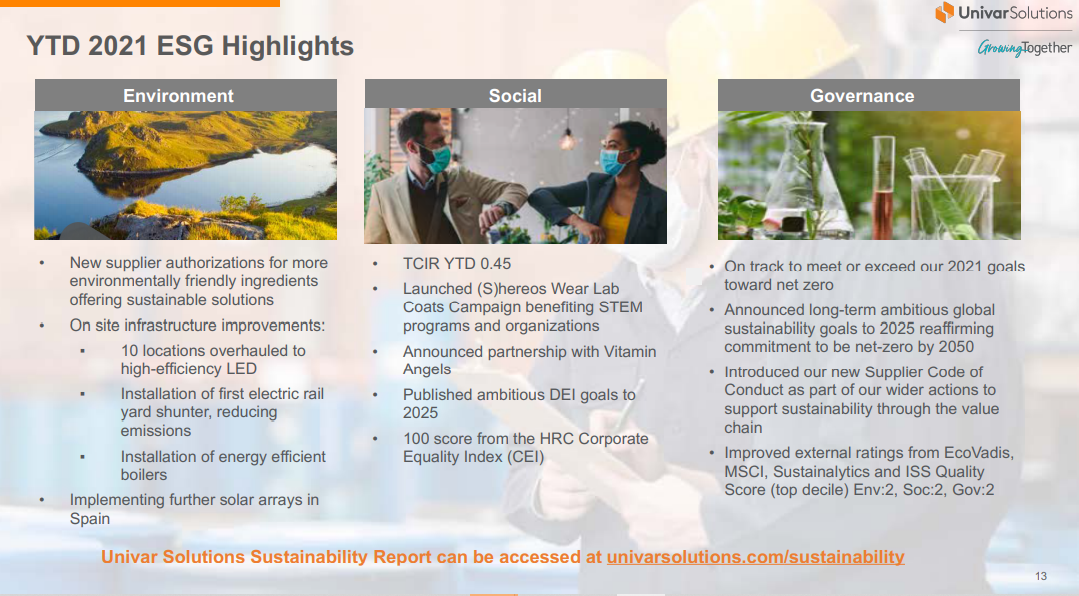

As the Univar and Eastman pictures show, it is now becoming almost mandatory to show your ESG badges in your quarterly earnings. The challenge for investors is the interpretation of the data presented. If there is no real consistency to the format, then it will be difficult to compare progress and this is one of the challenges that the SEC hopes to guide on by year-end – something we covered in last week’s ESG and Climate report.

Source: Eastman Chemical 2Q21 Earnings Release Presentation, August 2021

For example, the Univar claim that it has improved external ratings may be a function of better dialogue with the rating companies, or more consistent reporting of data and may not reflect any positive change at the company. Given the complexity of understanding environmental footprints at many of the industrial companies, including chemical manufacturing and distribution, it may not be much of a challenge to persuade any of the ESG rating agencies today that you are doing a better job than they have modeled, as they are unlikely to have the skills and experience to question you.

As we discussed in yesterday’s ESG and Climate report, the SEC has some challenges ahead, not just because there are high hopes that it will start mandating a change in terms of disclosure accuracy and consistency, as well as fund definition, but also because, as yet, it does not have the mandate to do so. All eyes are on the regional regulators, in the US, Europe, and other countries to police what is the wild west of reporting. The E piece of ESG is the major challenge and it is where corporates and fund managers alike are dealing with issues and measures that are likely very different company by company within a sector, let alone between the sectors themselves – it is far more complex and harder to analyze than, for example, board diversity.

The ESG investment shakeup could be one of the major events of this year, and as many of the headlines in our daily report suggest, there is a lot of work to be done, whether it is agreeing on a common set of measurement metrics – note the US and European differences discussed in one story – or the introduction of more empirical methods to judge whether what is labeled as an ESG investment fund is labeled correctly. There is also the issue of comparable disclosures, especially for companies in complex industries. It is interesting to note that in many analyses we see around carbon footprint or greenhouse gas emissions, and the potential routes to and cost of abatement, the chemical industry is omitted, except for ethanol and hydrogen. This is despite the industry accounting for 15% of the non-power emissions in the US industrial sector (similar in size to refineries). We believe that this is because the complexity of the industry makes it hard to model, and analysts choose to exclude it because they are not sure what they are doing.