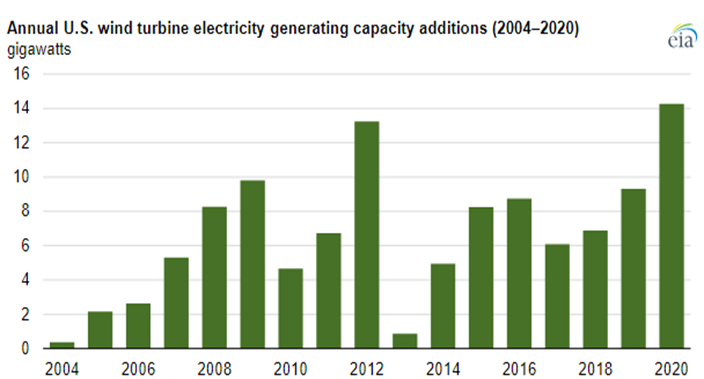

It should not be surprising that 2021 has seen a rebound in emissions as nothing has changed fast enough over the last 24 months in terms of renewable power additions and carbon abatement to offset more than the underlying growth in power demand, and based on what we are seeing in European and Asia LNG markets, we have fallen short of demand growth. The wind capacity chart below has one main conclusion – not enough. One of our main inflationary fears for 2022 is that both wind and solar installation rates need to step up meaningfully from current levels to make a difference – the IEA suggests that installation rates need to double (at a minimum). It has already proven difficult to meet installation targets in 2021, in part because of supply chain issues but also in part because of material shortages, all of which have led to rising installation costs, against the longer-term run of falling costs because of learning curve gains. We believe that costs will rise again in 2022 and 2023 as installers/projects compete for limited solar module and wind turbine components

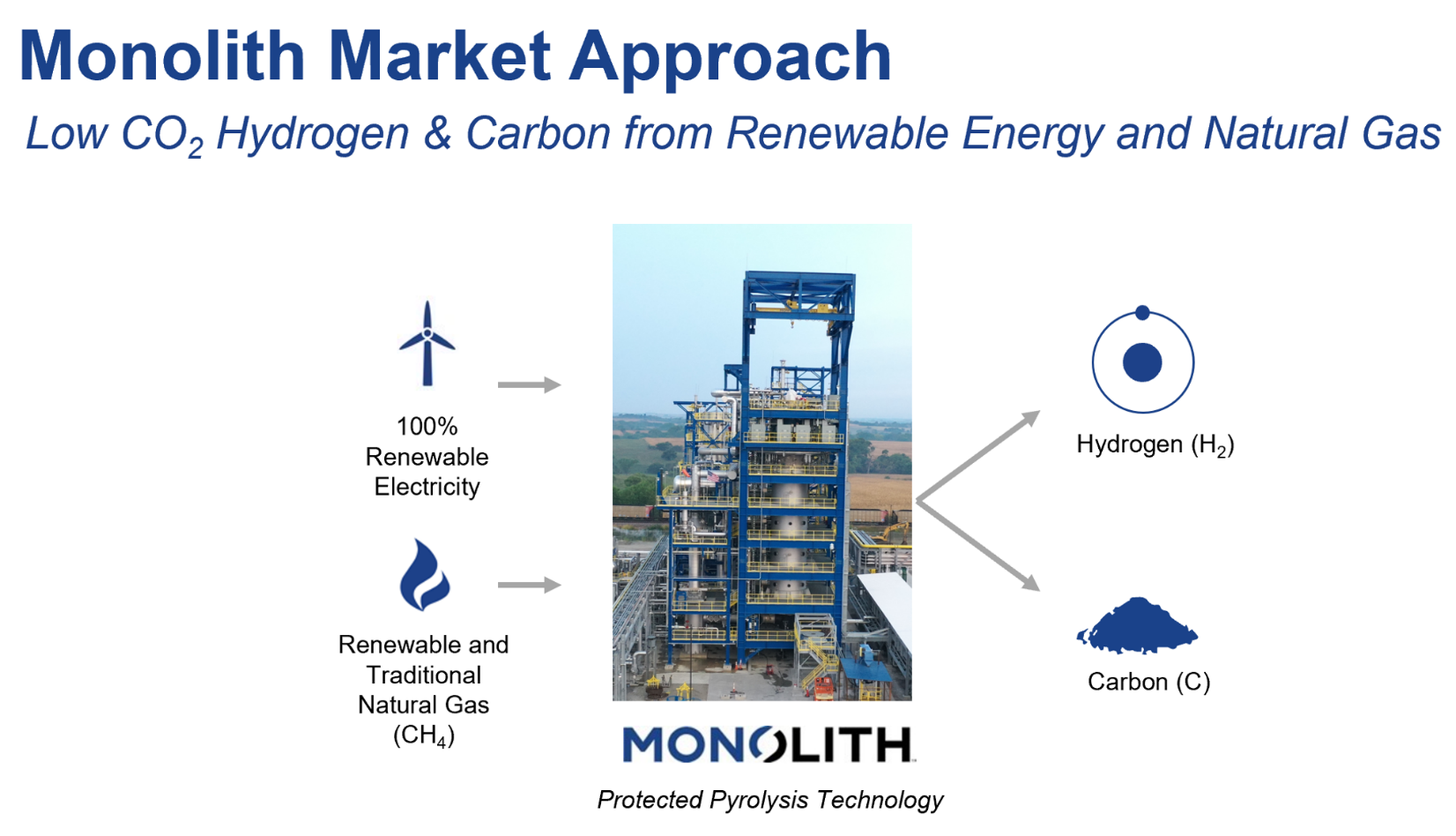

The Monolith announcement is not that surprising, as the auto industry is very focused on its carbon footprint and its suppliers, like Goodyear, are under pressure to look for more sustainable solutions. While Monolith uses natural gas as a feed, it’s carbon black is produced with very limited Scope 1 emissions, unlike the traditional route, used by the incumbents. It is not clear what the production economics are for Monolith because the co-product value of hydrogen could vary greatly depending on local needs, but the emergence of a competitor who sees carbon black potentially as a by-product is not likely to be good news for the traditional makers. A by-product that is more environmentally friendly is even more of a threat. Complicating the picture further could be the arrival of larger volume production from Origin Materials, which has a renewable based carbon black like material, which may also be seen as a by-product.

The coverage of the IEA study continues with lots of opinions, which is a good sign as it means that the work is being taken seriously.