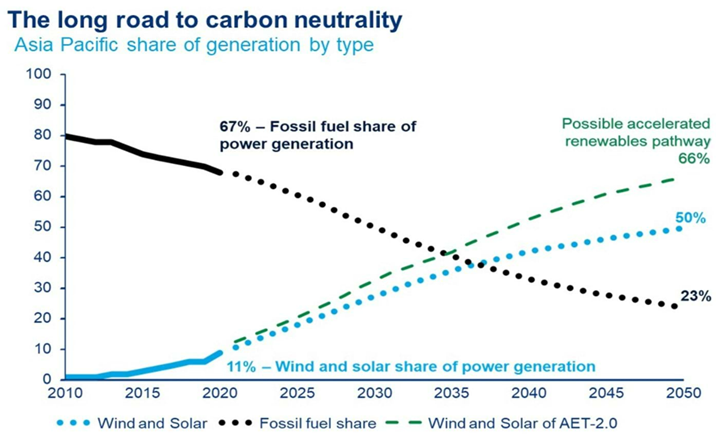

In the exhibit below, we see another chart that we find unhelpful when looking at the path to net-zero or something close. It is not an either/or game with fossil fuels and renewables. Those promoting this idea are setting impossible goals for the renewable industries, which will keep severe upward pressure on all energy costs. Wood Mackenzie may not mean what is implied in the chart below but taken at face value it suggests that more pressure will be placed on an underfunded materials market to supply an underfunded renewable power market, in which any opportunity to use decarbonized fossil fuels will be frowned upon. It would be good to see an analysis of how much global power could be generated from decarbonized natural gas and how much pressure that would take off the renewable industries.

Looking at the Bloom results and reflecting on our many recent client discussions, the low-cost providers of fuel cells and electrolyzers are going to win disproportionately in our view, but whether that is Bloom or others remains to be seen. Lower costs will come with scale, and this should allow the leaders to stay ahead, especially if they control their equipment production as Bloom does. The negative for Bloom is that its equipment production is in the US, which may add costs, but the positive is that it is on-shore and this gives the company more control over delivery in the US. Companies that can scale quickly in this space and other renewable sectors, should see the benefit of economies of scale and this should drive more wins and more economies.

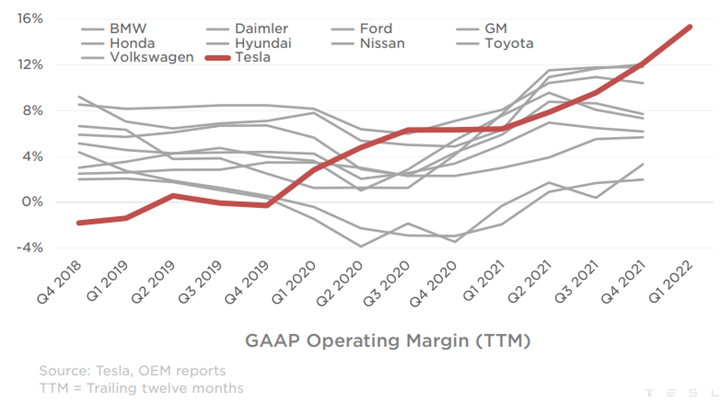

Tesla is on a roll, and showing other EV makers what is possible. The company priced its vehicles to be profitable at lower volumes and is currently seeing the benefit of scale, likely to be enhanced further as the manufacturing footprint grows. While the operating margin below looks very good, we would note that Tesla is not done scaling yet so there is considerable upside to the margin, most likely. One obvious conclusion from this analysis is that Tesla has plenty of wiggle room on pricing should macro conditions impact new car sales or should other EV makers try to steal share with pricing. Tesla has built a huge first-mover advantage in EVs and this will likely benefit the company for many years to come as long as they keep making vehicles that people want.

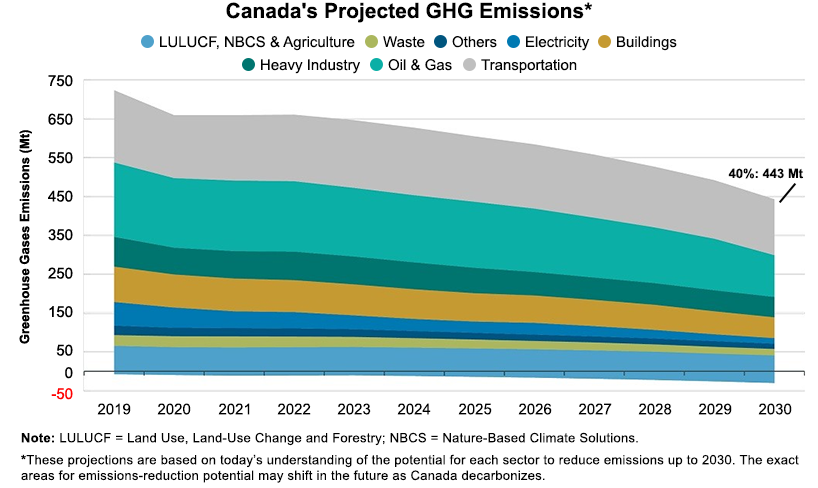

The Canadian targets highlighted below are ambitious and will likely not happen without the significant CCS projects planned for Alberta. The CCS opportunity will drive down energy and chemical (heavy industry) based emissions meaningfully and could also be the basis for new power generation capacity to allow the transport industry reductions that the country is looking for – either through EVs or hydrogen-based transport.

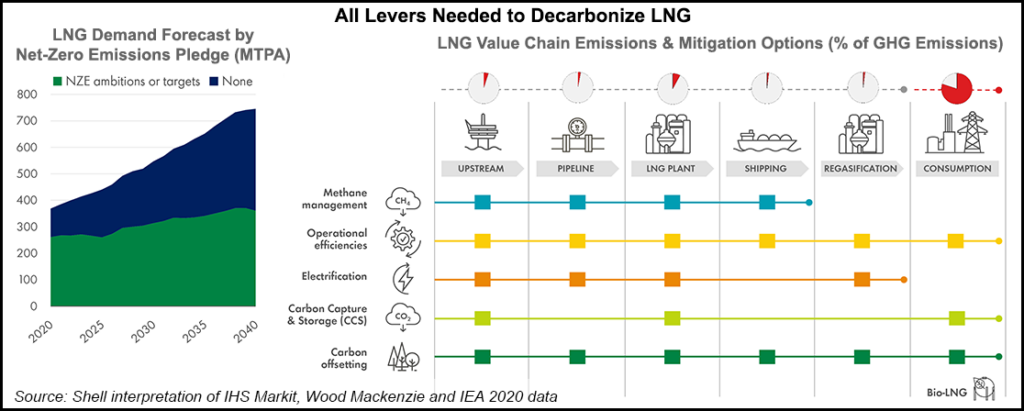

The first chart below has been included in a similar form in prior work and is a good summary of what is needed to decarbonize the LNG market to the greatest degree possible. There is a lot of resistance to the idea of endorsing natural gas as a transition fuel, but so many developed and developing countries need natural gas – often in the form of LNG – to displace or avoid (additional) coal use. If the LNG industry does not start to pursue the paths suggested in the exhibit, and reasonably quickly, it will stand very little chance of winning, or perhaps surviving, a PR battle that is very much stacked against it.

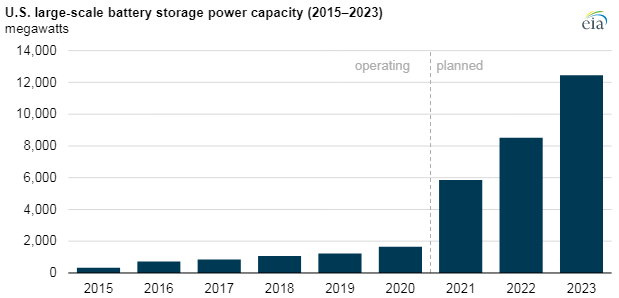

If we look at the battery storage projects highlighted in today's daily report and in the Exhibit below and then read some of the raw material inflationary concerns around batteries, we conclude that batteries will likely not end up dominating the power storage market. Both hydrogen and hydraulic-based storage are likely to be competitive if the battery costs do not come down. Note that storage batteries can afford to compromise on technology as they do not need leading-edge density – weight is not an issue for something that is not going to move. Even so, with battery demand expected to grow rapidly for EVs, it is not hard to see a scenario where other means of fixed location energy storage are more attractive.

There are several things worthy of comment today. First, the math looks wrong in the Biden EV executive order, especially when combined with tighter fuel efficiency standards that are also on the table. The US consumes around 340 million gallons (approx. 8.1 million barrels) of gasoline a day and a reduction of 340,000 would only be a 1% reduction by 2030, even assuming growth in driving over the next 10 years we would expect the fuel standards and EV introduction to have a much more meaningful impact if successful. We will write more on this is our dedicated ESG and climate work.

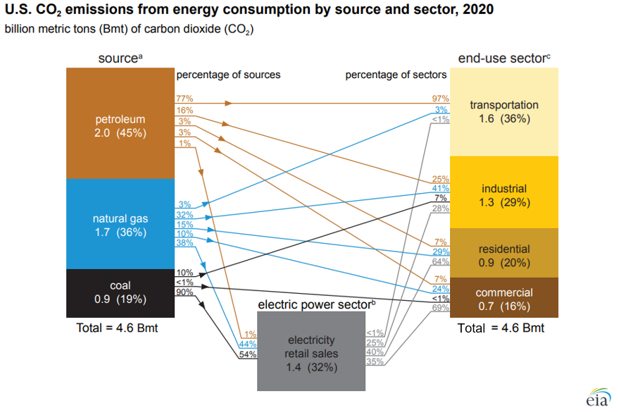

We are increasingly concerned that the US will remain a laggard concerning climate change initiatives given the major challenges of moving to the next steps and the bifurcated congressional views. The emissions reductions that the US has seen over the last 10 years have been more happenstance than planning, with the abundance of natural gas following the shale boom of the last decade creating economic reasons to replace coal-fired power with natural gas rather than environmental reasons. Lower costs for wind and solar power and focused industrial demand for that clean power have been the bigger driver of clean power investments. In the chart below, the decline in emission from the power sector is evident and it should continue. The diagram below shows sources and uses for US emissions in 2020, but the accompanying write-up talks about the step down in emissions overall in 2020. Except for the continuing electric power transition, most of the other 2020 declines are COVID-related and are expected to rebound in the near term, especially transport. The market share gains of EVs are not significant enough yet to make a difference. See more in today's daily report.

There is an unusual number of interesting topics in today's report, versus the normal mix of small pet projects or broad and unsubstantiated announcements. The EU 2030 targets are worth highlighting and they are in part connected to the central theme of the ESG and climate report that we will publish tomorrow. The European targets are not coordinated with what is happening in the rest of the World and while we admire the ambition, we suspect that the goal is not achievable, simply because the challenges of replacing the power and fossil fuel associated with the emissions to be avoided are too great, given the timeline. The level of additional renewable power generation, EV adoption, and hydrogen production needed to offset so much CO2 are extremely high, and it will be hard to get substantially more CCS offset than already announced because of land rights issues in Europe and logistics. To get the power, EV, and hydrogen, the EU will be competing with other regions that have their own targets and we see scare resources bidding up the price of power, impacting all of the elements, power itself, the cost of running EVs (see the chart below – the EV story does not work of you are using coal as a marginal source of power), and the cost of hydrogen.