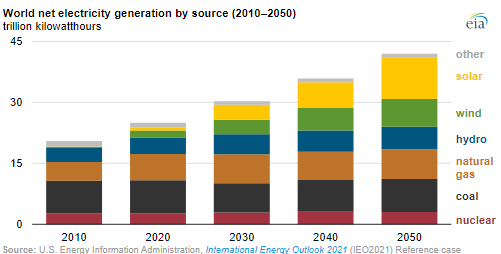

The renewable power space is heading for a very bad year in the US and Europe, as supply chain issues and raw material inflation will impact not only the amount of business that gets completed, but also the margin on that business. The trade issues between the US and China on solar panels have essentially brought the industry to a halt for the moment and suggests that all forecasts of the growth in renewable power contributions in the US in 2022 are too high, and consequently demand estimates for natural gas and coal for power generation are too low – see out comments in the energy section of today's daily report. The EIA forecast below likely fails to take into account the current woes and if governments, at the federal and the state levels act on the information in the chart they may be unprepared for some power shortages later in the year. Overestimation of the rate of renewable power installation as well as its operating rate is responsible for many of the current power shortages that we see in most regions.

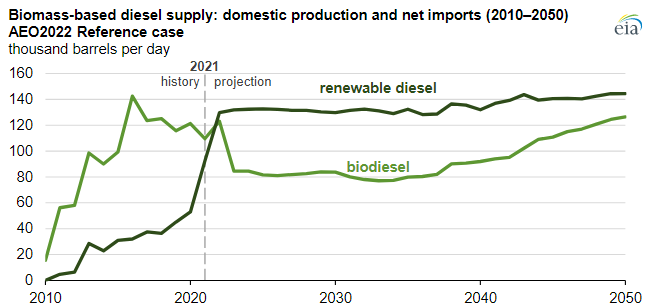

The EIA renewable diesel projections are based on a couple of things – who plans to make it and who will pay for it. All eyes are focused on the California market today as that is where the incentive lies – through the LCFS credit – and production plans plateau associated with that opportunity. As other states in the US adopt similar programs – which seems likely – we would expect to see production plans increase and the EIA will likely adapt its market view model and the chart will change. Note the dominance of renewable diesel over time, and this is where we would expect all future growth to occur. The plug-and-play nature of renewable diesel makes it a far more attractive option for refiners assuming the cost works. See more in today's daily report.

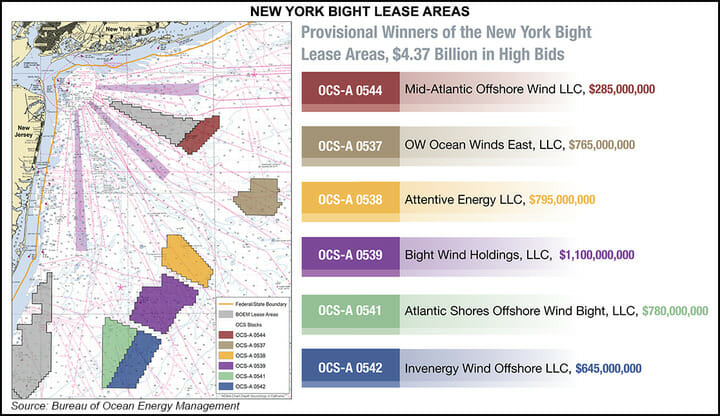

We include a couple of headlines and charts in today's daily report that step into the central theme of this week’s ESG and climate report, which will be published tomorrow (see here). The offshore wind ambitions and the EIA solar and battery projections both assume that the materials are available to build the capacity. In the case of the offshore wind leases, the winning bidders do not need to be in the market for all of the projects today and while the opportunities will lead to a step-change in demand for turbines in the US, the timing is less clear today that it will be in a few months and that timing may be adjusted to reflects equipment timing and costs, etc.

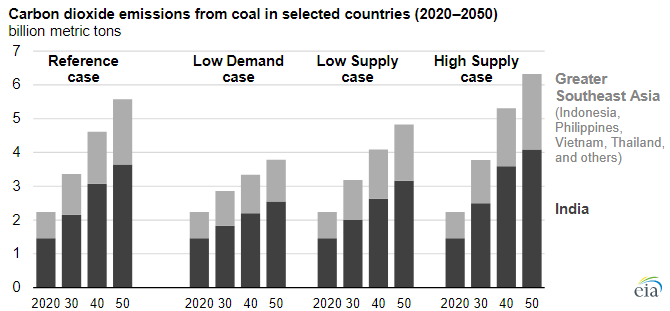

The coal data in the Exhibit below is likely not popular with the environmental lobby. However, the EIA analysis takes into account the alternatives for the countries involved and the fortunes of coal in these countries will be directly impacted by the help that other countries offer. If the region can be assured of abundant sources of alternative energy, whether renewables or more likely LNG, then the use of coal will fall. This is another example of where some of the global energy policies are coming up short in our view. The better solution is to champion (clean) LNG growth, wherever possible, to bridge the huge gap between the energy the world needs and the rate at which it can be supplied from renewables. See more in today's daily report.

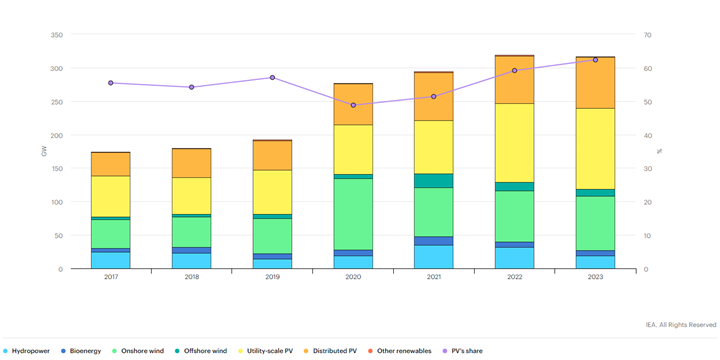

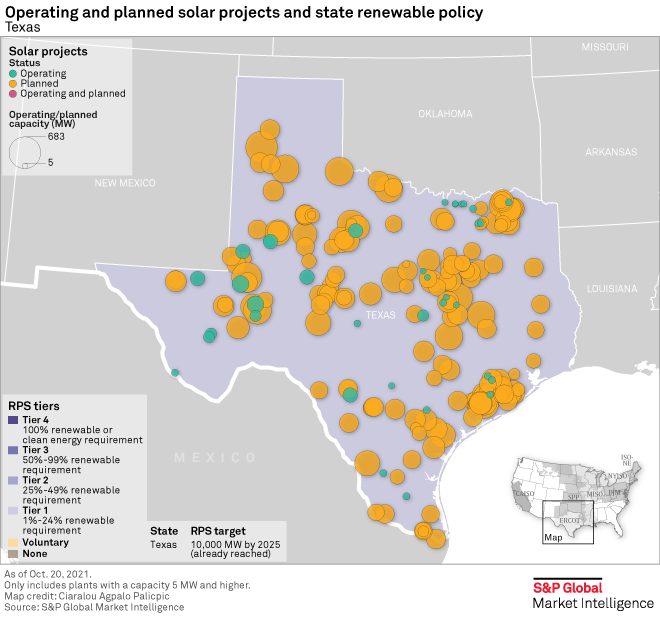

We struggle with both of the charts below, as we see the rate of potential renewable additions as far too optimistic, not because of a lack of capital, but because of a lack of materials and the knock on effect that this could have on capital if project costs increase meaningfully or if timelines extend. The solar expansions planned for Texas for example all require solar modules and there is simply not enough capacity to make these modules and in many cases not enough raw materials. All of these projects are not planned for the same year, but regardless, when you add the Texas plans to plans all over the World, you have an annual rate of addition that the equipment makers will not be able to meet. Today, many of the projects are in the planning and financing stage and the installers have yet to go looking for equipment – when they do, they may have to rethink.

If you look back at our ESG and Climate piece this week (EIA View Suggests Natural Gas & CCS Critical To Net-Zero Goals), you will note that we focused on the recent EIA global energy outlook, and another chart from this outlook is shown below. In the ESG report, we talked about the global need to support increased “clean” natural gas use to offset as much of the coal predictions in the chart as possible and to drive additional hydrogen production to offset some of the petroleum product demand that the EIA still expects to be sued as a transport fuel in 2050. We also called for the broad and warm embrace of CCS so that some of the fossil fuel that the EIA is predicting – especially all of the fuel used for power in the exhibit below. Yesterday Air Products announced not only a large blue hydrogen complex for Louisiana but also the CCS to support it and made a very compelling argument in its presentation for the need for substantial volumes of blue hydrogen – something we fully agree with. We covered the subject in detail in yesterday’s daily. “Blue Is The Color, Hydrogen Is The Game…”

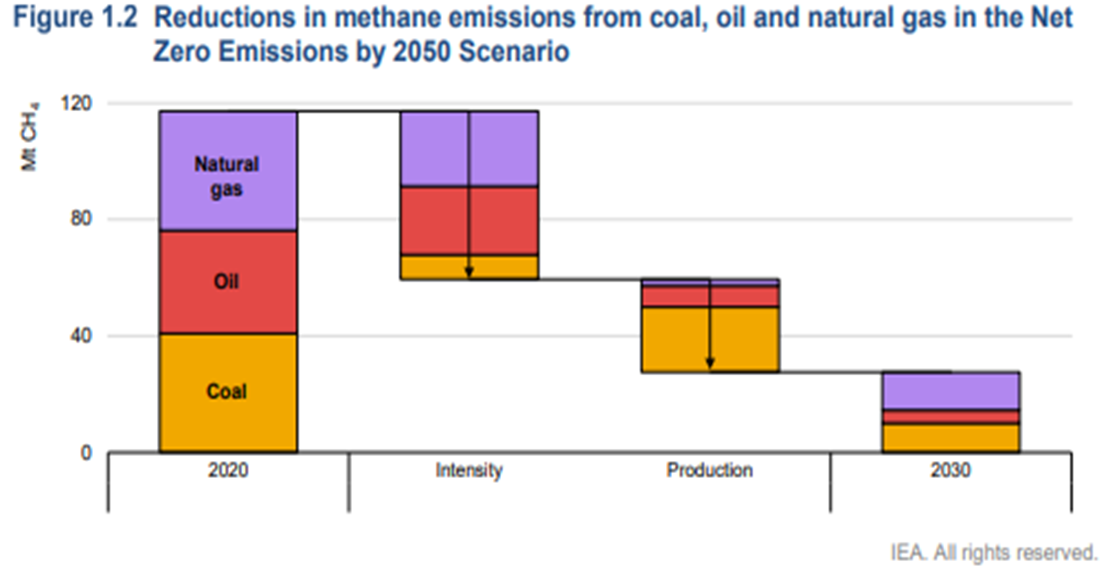

A couple of things worth highlighting in today's daily report – the first being Chevron’s move to join the net-zero club – focusing all eyes now on ExxonMobil in particular but also the rest of the US E&P crowd. Chevron will have some major challenges getting to net-zero and will likely face much of the same skepticism that bp, Shell, and TotalEnergies attracted in Europe initially and still face today. The Europeans have placed a lot of their bets on moving into renewable power – for the moment, Chevron is focused on moving to net zero in its own operations, which we read as biofuels and a lot of CCS. Given the acute shortage of international natural gas, it would make the most sense for the independent natural gas E&P companies and the LNG sellers to jump on the same boat. By promising low carbon natural gas and LNG, the industry is much more likely to gain support for the expansion that the world needs to counter some of the EIA assumptions around coal and petroleum product use from 2030 to 2050. Of course, it would be a whole lot easier for the US industry to do this if they had a value on carbon to work with! The chart below looks at one of the core clean-up issues, which is methane leakage. This is a subject we cover extensively in our ESG and Climate service linked here.

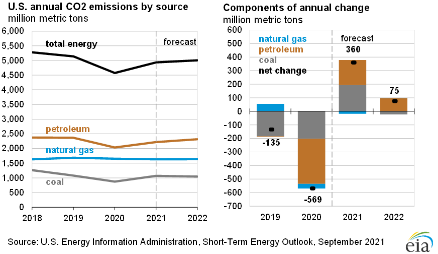

The CO2 emissions chart from the EIA should not be a surprise as the step-up in 2021 and 2022 is a recovery from the economic contraction and habit changes associated with COVID, and the projected increases in 2021 and 2022 are combined lower than the step down in 2020, suggesting that the trend is still negative. The problem is that the trend is not negative enough and as we have written about at length, it will not trend lower fast enough without all corrective opportunities at play – more renewable power, more conservation, and a lot of CCS. See our ESG and Climate work for more.

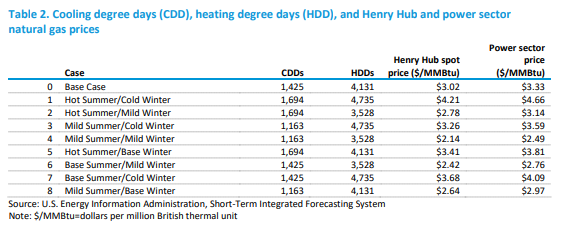

The table below is from an interesting analysis published by the EIA this week that focuses on possible power demand scenarios for the US – all weather-related – and then backs into the power sources that would be needed to meet the demand, concluding with the US carbon emissions that would correspond to each scenario. The conclusions should not be surprising, which are that carbon emissions rise disproportionately faster as power demand rises – as more coal is required to balance generation needs, and fall disproportionately more quickly as power demand falls (as less coal is needed). The analysis is effectively a study of how much less CO2 emissions are using natural gas to generate power versus coal. As renewable generation increases as a share of the total, however, the math will change, and the EIA study does not take into account the weather factor on renewable power, it looks at cooling degree days and heating degree days at a national level only. This is reasonable as there is likely not enough data to be able to put good reliability estimates yet around renewable power annual volatility and more importantly, the impact of weather on renewable power is likely to be short-term in nature. Perhaps this analysis could be improved by adding a “daily risk band” around each scenario, showing how much renewable power volatility could cause peaks in the high scenario and lows in the low, etc.