Methane emissions are one of the more challenging carbon equivalent problems in part because it is lots of small emitters, associated with many thousands of wells and many thousands of miles of pipelines, rather than a large source of CO2 that can be eliminated with a specific investment. The API carbon tax, proposed last week, has a condition in the proposal that would prevent any other emission-based legislation for many years to evaluate the effect of the tax. This will not drive lower methane emissions unless it is a broad carbon “equivalent tax”, which could potentially drive a very punitive tax on methane and would get an almost instant response from those that own the wells and the pipes. Some of the abatement solutions are easier than they first appear and all pipeline operators should look at the technology offered by Pipeotech, for example. Wellhead emissions are more problematic but not beyond the engineering skills that exist within the major E&P companies. The harder problem is what to do with emissions from abandoned wells – here the tax idea would not work as there is no one to pay the tax and a fairly complex financial structure would be needed to encourage someone to take on the role of cleaning up these properties. That said, all these pathways will need to be explored to get to the targets outlined below.

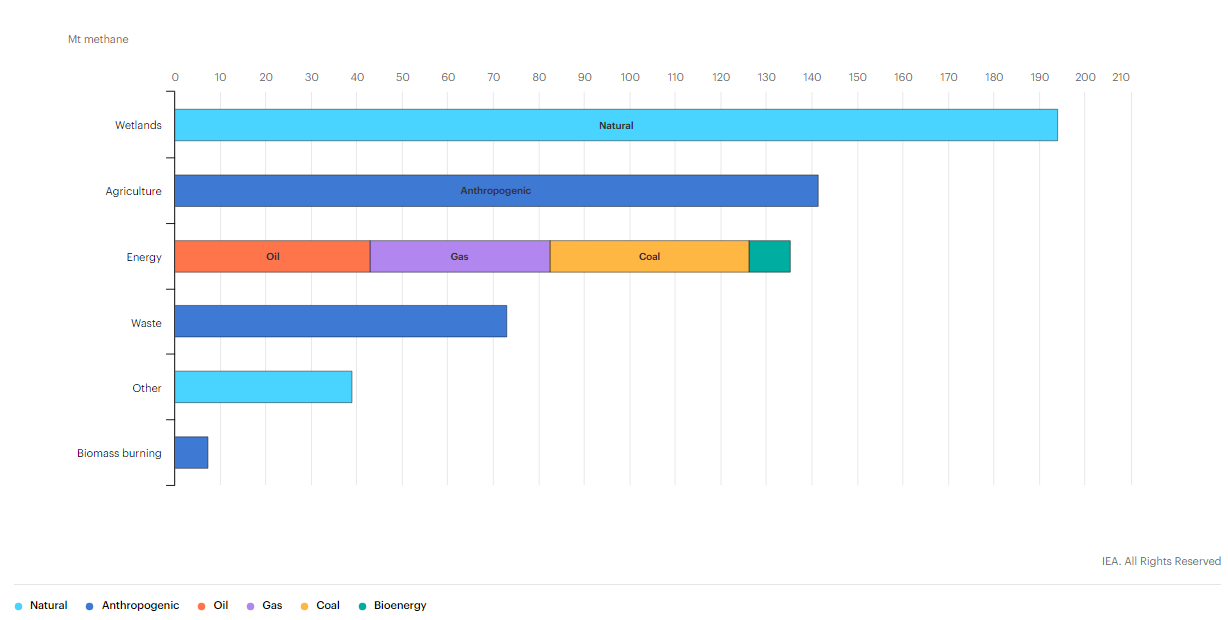

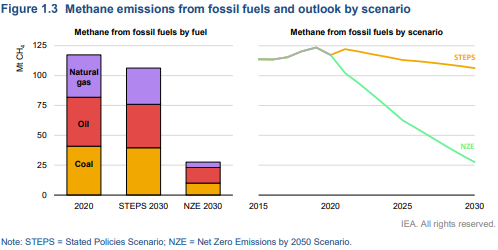

We have noted several renewable natural gas initiatives in the US and the data in the chart below shows how much methane is emitted by agriculture – the largest source after natural leakage. The agriculture-based RNG projects only make economic sense today where you have access to very large farms, where customers are willing to pay a premium, or where you qualify for incentives. That said we expect more projects, with growth stories at companies like Archaea Energy dependent on building new projects. The chart also shows how much emissions flow from the energy industry and this has been a more acute focus for remediation since COP26. See more in today's ESG and Climate report.

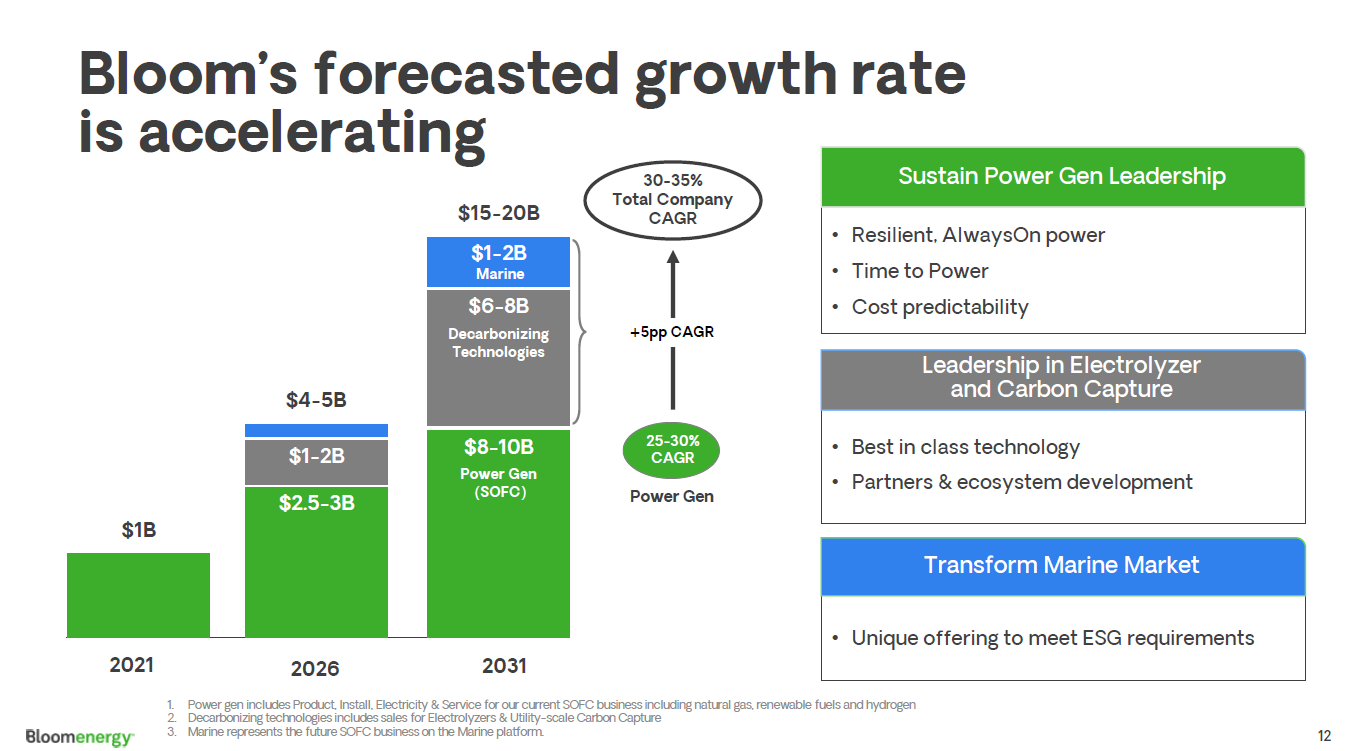

There is a lot in the ESG section of today's daily report and we will elaborate more in our ESG and Climate report next week (to be found here). The Bloom Energy results were strong and the modular nature of what Bloom is offering, in our view, should only increase the level of interest going forward. SMR and ATR base blue hydrogen projects are very large, requiring billions of dollars of capital and taking years to construct. The projects are further complicated by the likely need to build dedicated CCS with each unit. The methane fuel cells that Bloom offers are modular and can be much smaller and more incremental from an investment perspective. For blue hydrogen, they will still need CCS, but they offer a lower capital-based route to hydrogen and power today. We can see an opportunity to deploy these units, or something similar, everywhere there is CCS, as either an incremental source of hydrogen and power or a large source. Bloom still has work to do on lowering costs, but much less work than green hydrogen appears to have today, in our view.

The linked Canada headline supports one of the themes that we have been highlighting for a while, which is that certainty around carbon pricing is likely to drive investment rather than discourage it. Canada, and specifically Alberta, has seen several new investments announced over the last few months because manufacturers can now add some certainty around carbon values to other advantages offered by the province, including cheap natural gas and what appears to be low-cost CCS opportunities. We are also seeing investments shape up in Europe – also to produce low carbon materials and fuels – and this is also driven by greater certainty around carbon value. The lack of a carbon price in the US is becoming a competitive disadvantage for the country and those opposing it in government are, in our view, very misguided. If China can develop a credible and broad carbon pricing mechanism, it will also likely gain investment dollars, possibly at the expense of the US. Not having a sound climate change and carbon value framework in the US is a major threat to many of the reshoring initiatives that US retailers and manufacturers would like to see.

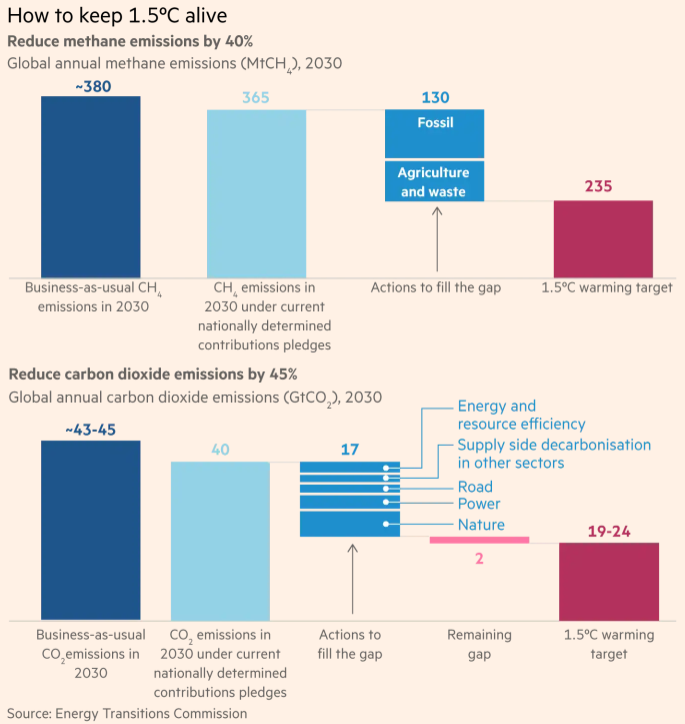

Our ESG and Climate Piece today focuses heavily on COP26, which begins this weekend, and has been the subject of many of this week's stories, as attending countries make their concerns and preferences known and as companies and lobbying groups try to be heard. The linked FT article talks about the minimum needs from COP26. We highlight this because we have been talking about the same things for months – the significant gap between what is pledged for 2030 and what is needed, and the need to attack emissions of methane and CO2 aggressively. The methane issue can likely best be achieved through legislation – especially as some of the leaks around the world may not belong to anyone, who could benefit from an incentive or be penalized for the leak. The CO2 emission issue will always be bet addressed through a pricing mechanism on carbon.

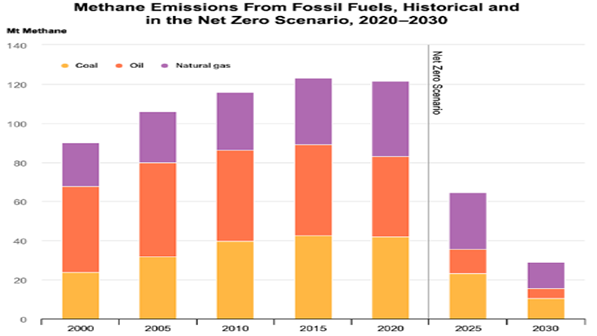

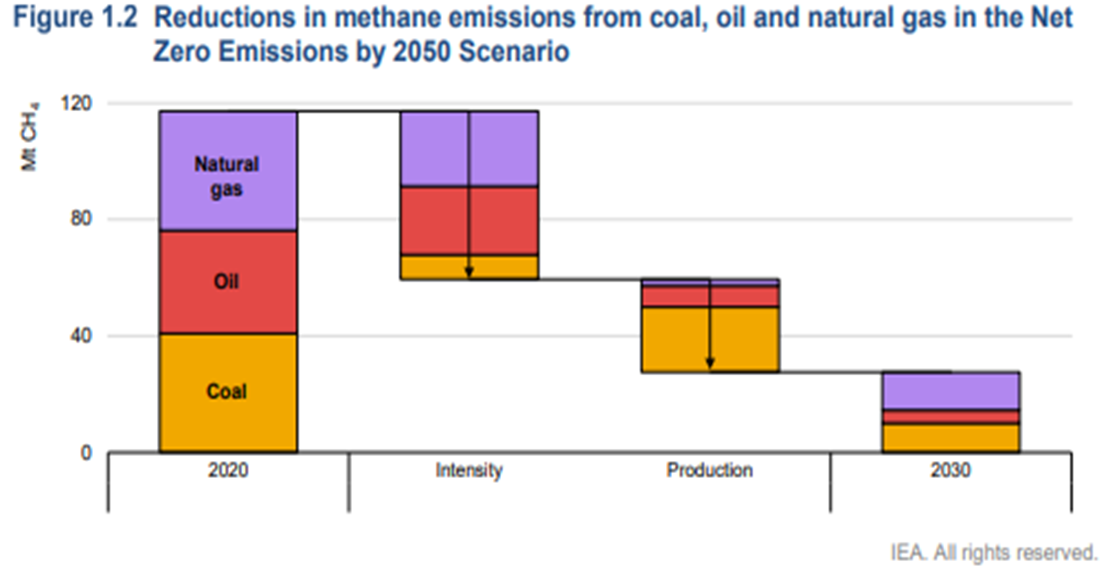

A couple of things worth highlighting in today's daily report – the first being Chevron’s move to join the net-zero club – focusing all eyes now on ExxonMobil in particular but also the rest of the US E&P crowd. Chevron will have some major challenges getting to net-zero and will likely face much of the same skepticism that bp, Shell, and TotalEnergies attracted in Europe initially and still face today. The Europeans have placed a lot of their bets on moving into renewable power – for the moment, Chevron is focused on moving to net zero in its own operations, which we read as biofuels and a lot of CCS. Given the acute shortage of international natural gas, it would make the most sense for the independent natural gas E&P companies and the LNG sellers to jump on the same boat. By promising low carbon natural gas and LNG, the industry is much more likely to gain support for the expansion that the world needs to counter some of the EIA assumptions around coal and petroleum product use from 2030 to 2050. Of course, it would be a whole lot easier for the US industry to do this if they had a value on carbon to work with! The chart below looks at one of the core clean-up issues, which is methane leakage. This is a subject we cover extensively in our ESG and Climate service linked here.

The methane chart below is another reminder of how important it is for governments to increase their demands on methane emitters to find solutions to cut leakage. The current stated policies are grossly inadequate, and while we are seeing some of the majors taking proactive steps to reduce emissions, the problems are more acute among the independents in the West as well as abandoned wells that might have no current ownership and operators outside the US and Europe. We keep talking about the need for COP26 to focus on natural gas, and this would be one of the key issues on which a global agreement would help. See several of our ESG reports for more on this subject.

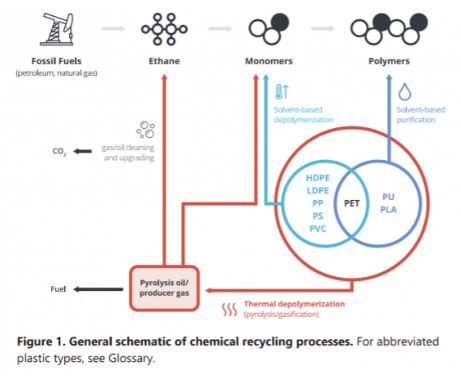

We believe that the plastics industry is right to get as much state backing for chemical recycling as it can – see Louisiana headline and diagram below. While chemical recycling is not as neat as mechanical recycling, it has far more chance of dealing with the core issue, which is the disposal of plastic waste – see report linked here. Our support for chemical recycling stems from the view that it will be very hard to get the behavioral change needed to ramp up mechanical recycling quickly and to a level that will impact waste.

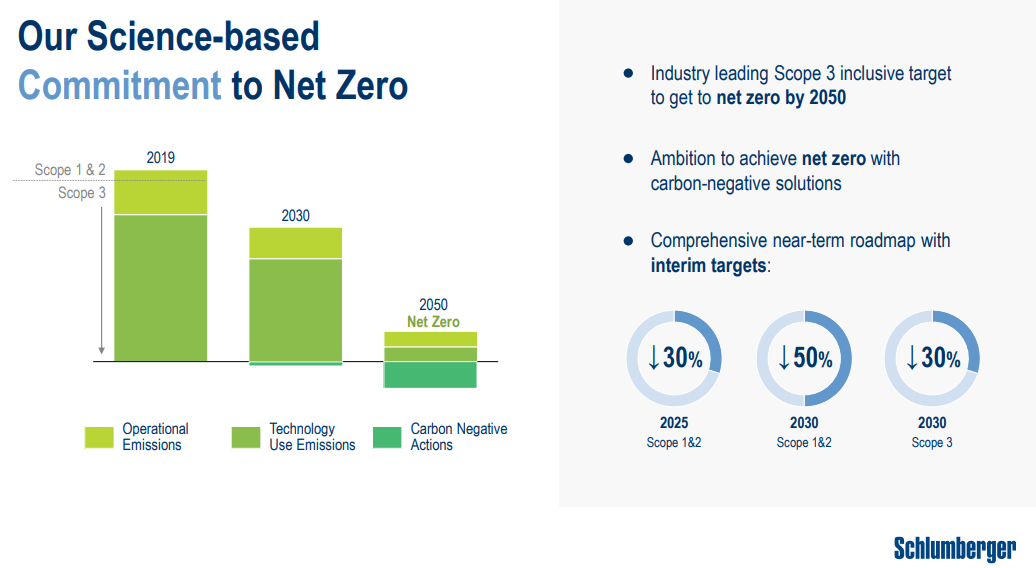

The Schlumberger net-zero goals, as discussed in a couple of articles in today's daily and the presentation linked, set some aggressive but bold ambitions, especially as they are looking to solve problems that they share with their customers, methane leakage from oil and gas wells, and minimizing flaring. Schlumberger is a little dependent on collaboration from its customers here as the technology solutions are likely to be more expensive than current options and the oil and gas producers will need to pay up.

The “adapt or die” headline targeting the US oil industry which was featured in our Daily report yesterday is a bit extreme, especially for an administration that does not believe it can enforce a carbon tax or cap and trade system. If the investment community were to make that statement frankly today it would have more credibility. There is talk about a Senate-sponsored bill to ban methane emissions or at least aggressively penalize them – which would be a better approach. Putting a high price on methane could encourage the use of some interesting small-scale technologies to turn local methane supplies into LNG, or methanol, or ammonia/urea. We have discussed all of these technologies in prior work and are happy to discuss them with anyone interested.

The other more interesting take on “adapt or die” might be “adapt and thrive”, which is likely a more palatable message to give to the energy industry. While the US seems to have limited teeth from a regulatory perspective, the rest of the world does not, and the ability for the US to produce lower carbon fuels may give US producers a competitive edge globally – see our ESG and Climate piece from Wednesday