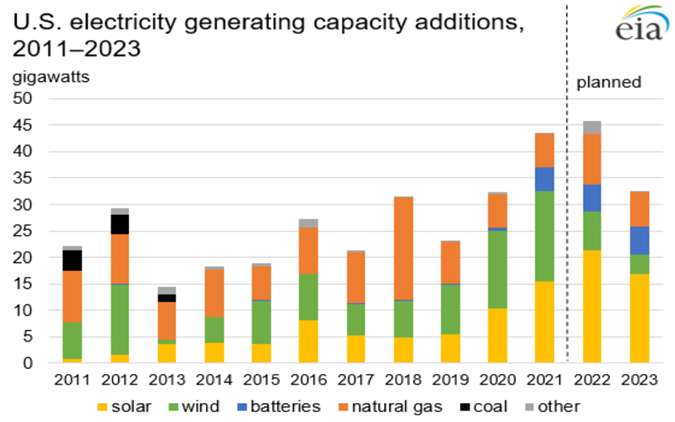

In our ESG and Climate report yesterday we highlighted inflation as one of the most significant risks for 2022 and the estimates in the exhibits below do not leave us any less concerned. The US has struggled to meet solar installation plans for 2021, falling short of early-year estimates because of limited equipment availability and higher equipment prices. While some of this has been the result of the supply chain challenges of 2021, some shortages have also been the result of very strong global demand. The idea that we can increase solar installations in 2022 without creating more supply issues (and more inflation) should be questioned, especially in light of planned additions in China, which will consume an increasing share of Chinese solar modules.

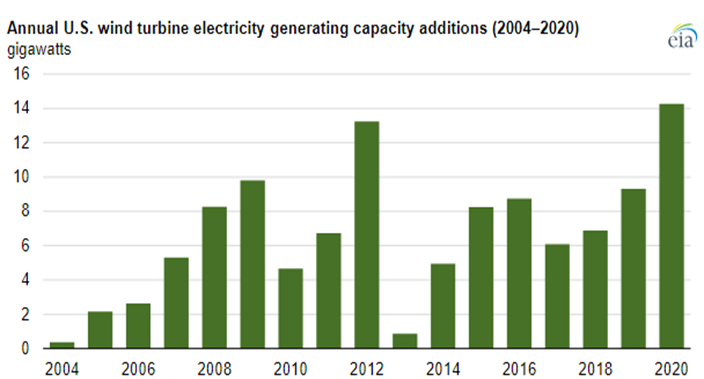

It should not be surprising that 2021 has seen a rebound in emissions as nothing has changed fast enough over the last 24 months in terms of renewable power additions and carbon abatement to offset more than the underlying growth in power demand, and based on what we are seeing in European and Asia LNG markets, we have fallen short of demand growth. The wind capacity chart below has one main conclusion – not enough. One of our main inflationary fears for 2022 is that both wind and solar installation rates need to step up meaningfully from current levels to make a difference – the IEA suggests that installation rates need to double (at a minimum). It has already proven difficult to meet installation targets in 2021, in part because of supply chain issues but also in part because of material shortages, all of which have led to rising installation costs, against the longer-term run of falling costs because of learning curve gains. We believe that costs will rise again in 2022 and 2023 as installers/projects compete for limited solar module and wind turbine components