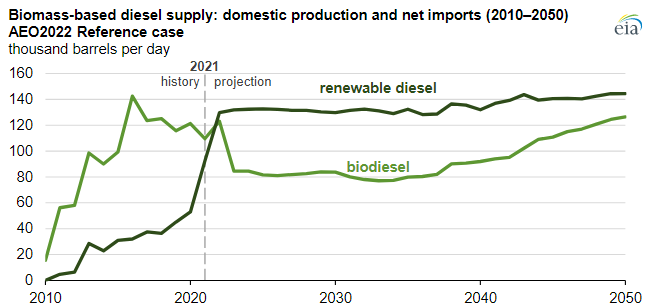

The EIA renewable diesel projections are based on a couple of things – who plans to make it and who will pay for it. All eyes are focused on the California market today as that is where the incentive lies – through the LCFS credit – and production plans plateau associated with that opportunity. As other states in the US adopt similar programs – which seems likely – we would expect to see production plans increase and the EIA will likely adapt its market view model and the chart will change. Note the dominance of renewable diesel over time, and this is where we would expect all future growth to occur. The plug-and-play nature of renewable diesel makes it a far more attractive option for refiners assuming the cost works. See more in today's daily report.

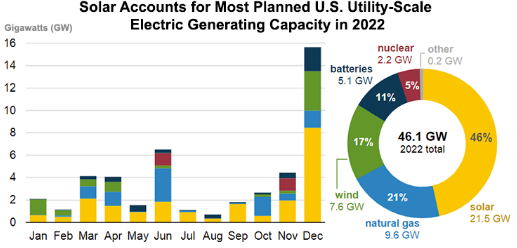

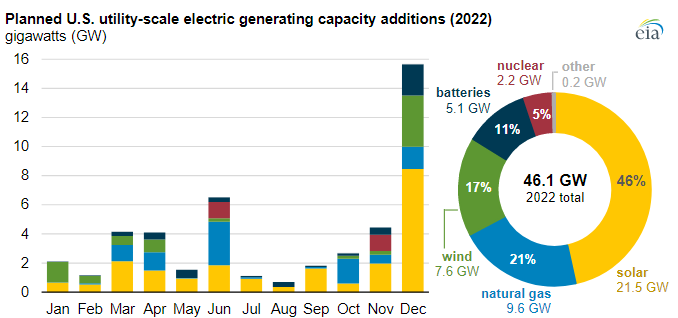

The back-end loading of the power projects for the US for 2022, as shown in the chart below leaves us somewhat skeptical concerning how much will come online this year. Supply chain problems and materials costs and availability are causing all sorts of problems with renewable power projects and installed capacity expectations for 2021 were too ambitious. We believe that companies are pushing projected start-ups later in the year to give them more of a chance of completion, but this creates the risk that they slip into 2023 or beyond. The most significant issue here is that as these plans get delayed, natural gas demand goes up, as one of the swing suppliers. This is fine as long as the US natural gas industry and shale oil industry is investing so that gas availability rises. Otherwise, we could see gas prices spike in the US next winter and another year where we use more coal than we expected. For more see this week's ESG and Climate report.

There are a handful of “renewable” headlines in today's daily report, and it is probably worthwhile discussing the differences. First; the linked Gevo RNG announcement is likely one of several RNG projects that we will see come online in 2022, as there are a number of farm-based RNG projects underway in the US and other parts of the world. The Gevo facility is based on farm manure and is expected to produce 355,000 MMBtu of RNG per year. As such it is not large, and all of the farm-based projects are small in the larger context of the natural gas markets. However, when focused on decarbonizing a specific product or process this RNG can be very important. Our take on the market is that there will likely be more demand for RNG than supply, as several companies are looking for RNG to make proposed investments make sense from a “green” perspective (Monolith would be a good example). This suggests that it will be better to be a seller than a buyer longer-term.

First, it is going to be an uphill struggle to get some common sense around the continued use of fossil fuels during any period of energy transition if the activists take away all resources from the energy industry – banking, PR, etc. While there is plenty of work to be done to minimize greenwashing, there is also plenty of work that needs to be done to explain why fossil fuels are still needed and how we can use them as cleanly as possible. If it becomes a business risk to bank or advise any company in the fossil fuel industry, while there will inevitably be workarounds, the net effect will be continued underinvestment, in production and in cleaning up the fuels and the concerns that we raised for natural gas in our Sunday Thematic will happen.

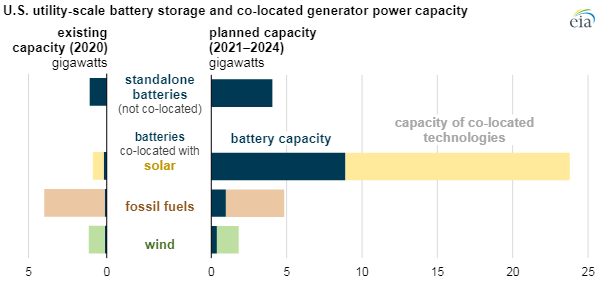

The battery storage investment chart below is interesting in that it shows significant pairing with Solar facilities and less with wind. If we are to meet the green hydrogen goals that many are optimistically predicting over the next 10 years, then the new wind and solar investments need to be paired with hydrogen and hydrogen-based swing power generation capacity. This is the only way that countries will develop effective hydrogen grids. Simply having one or two large hydrogen facilities and/or import facilities will result in very inefficient distribution models either for fuel cell vehicles or for heating and swing power generation. A distributed network for hydrogen makes much more sense and modular electrolyzers coupled with modular hydrogen power generators is a more holistic model, with much more flexibility than adding batteries. Granted, the battery technology is tested and available today, but the broader ambitions for hydrogen will not be met if we do not get out of the blocks soon.

Overnight there has been a very good IEA report on how China could get to net-zero by 2060, and further news of more industries hit by power cuts because of power shortages, some of which are apparently due to tighter emissions standards. These are both important and far-reaching topics and will require some analysis to provide the kind of insight that we believe is necessary, and accordingly, we will push these to next week’s report (all input welcome). In the meantime, we have included a couple of charts that show the way up and the IEA view of the way down. The power outages are interesting as while they may cause some manufacturing cutbacks and we have seen recent news to that effect, China has overbuilt in the last couple of years relative to domestic demand growth, and with port and shipping congestion the country has surpluses of many products sitting around at very low values. The power moves may help correct some of these imbalances and we are already seeing some chemical prices bounce off recent lows because of production cutbacks. We discussed the acetic acid chain in one of our dailies last week – linked here.

In our ESG and Climate report yesterday we focused on sustainable aviation fuel, discussing a recent report from Shell and Deloitte, which shows some of the challenges with getting the aerospace industry to net zero. The report focused on the need for sustainable aviation fuel now, and in large volumes, as this is the only thread that the industry can pull on today – synthetic fuels (from CO2 and hydrogen will be uneconomic for decades, and neither electric powered or hydrogen-powered aircraft are going to be a solution before 2050). The bp, Delta, and Boeing linked headline is one of many that we expect to see as the need for near-term progress is urgent, given the scale of investment required. See yesterday’s report for more detail.

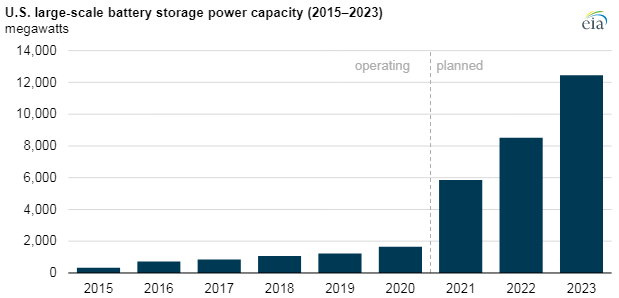

If we look at the battery storage projects highlighted in today's daily report and in the Exhibit below and then read some of the raw material inflationary concerns around batteries, we conclude that batteries will likely not end up dominating the power storage market. Both hydrogen and hydraulic-based storage are likely to be competitive if the battery costs do not come down. Note that storage batteries can afford to compromise on technology as they do not need leading-edge density – weight is not an issue for something that is not going to move. Even so, with battery demand expected to grow rapidly for EVs, it is not hard to see a scenario where other means of fixed location energy storage are more attractive.