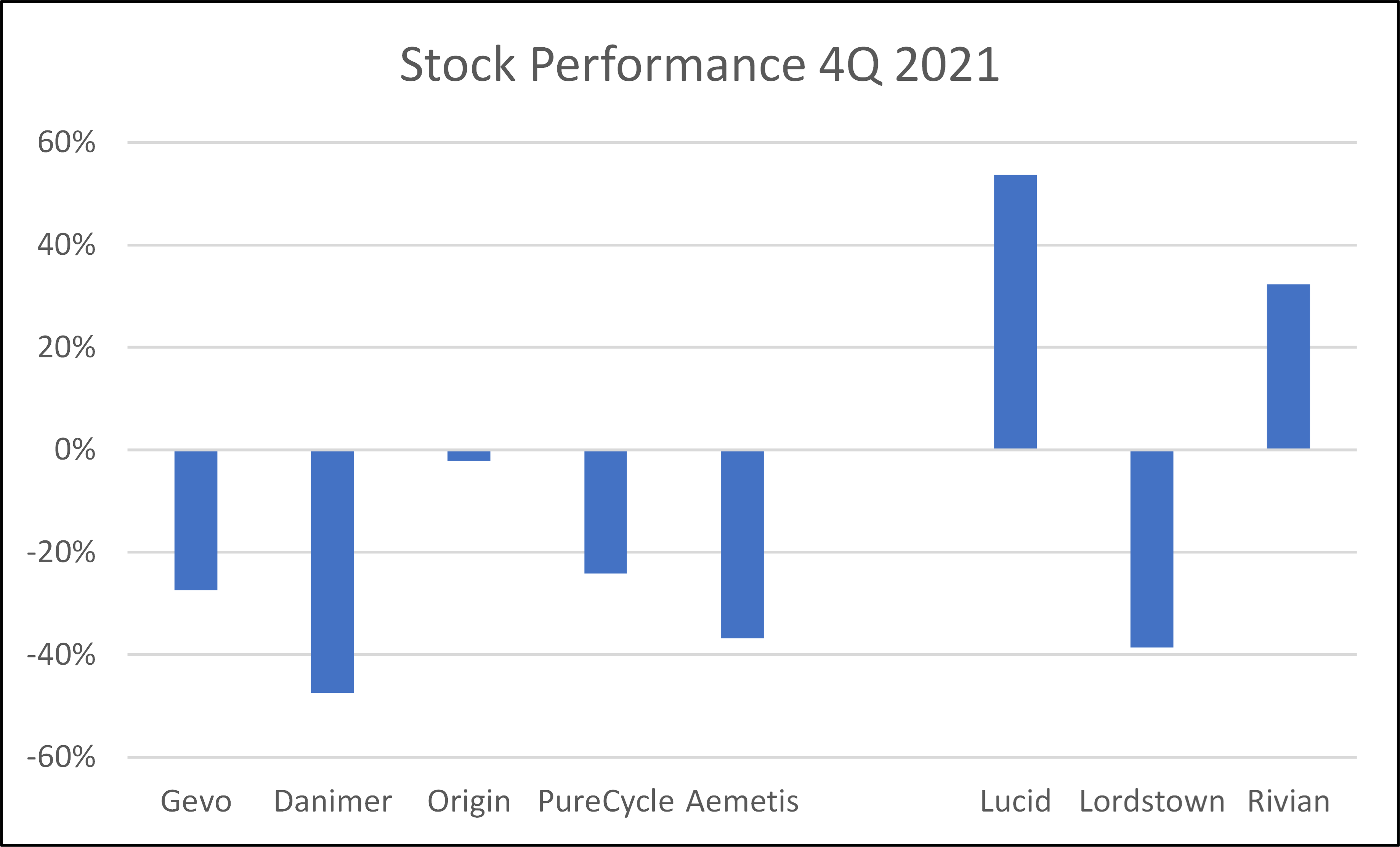

Life in 2022 is likely to be tougher for the new companies in materials and fuels, as all of them need capital to support projects that now look riskier from a cost inflation perspective and the market has moved to reflect that risk – Exhibit below. For every company below, the 2022 story was supposed to be capital spending to create commercial-scale production. The poor stock performance for many has tracked rising raw material prices – especially steel – as well as concerns around supply chain-driven delays and labor shortages. Few have the financial capacity to absorb significant cost overruns and/or construction delays. Danimer Scientific has done a recent capital raise and its impact created roughly half of the downside shown below – Danimer still likely needs more capital, but with more cash on the balance sheet may be able to get the rest through loans. Gevo, which in our view has the more impressive portfolio of potential offtake partners at this point likely plans to borrow at the facility level, and the stock weakness is likely a combination of inflation fears, the declining LCFS value, and the wait for the company to announce that it has a completed FEED study for the first plant and has reached FID. We would struggle to invest in any of these names today given the step-change in company development that each needs to make in 2022, and we would need more offtake agreements and process/construction guarantees than any company can likely get today, and if they could, they might not want to make some agreements public. See more in today's ESG and Climate report

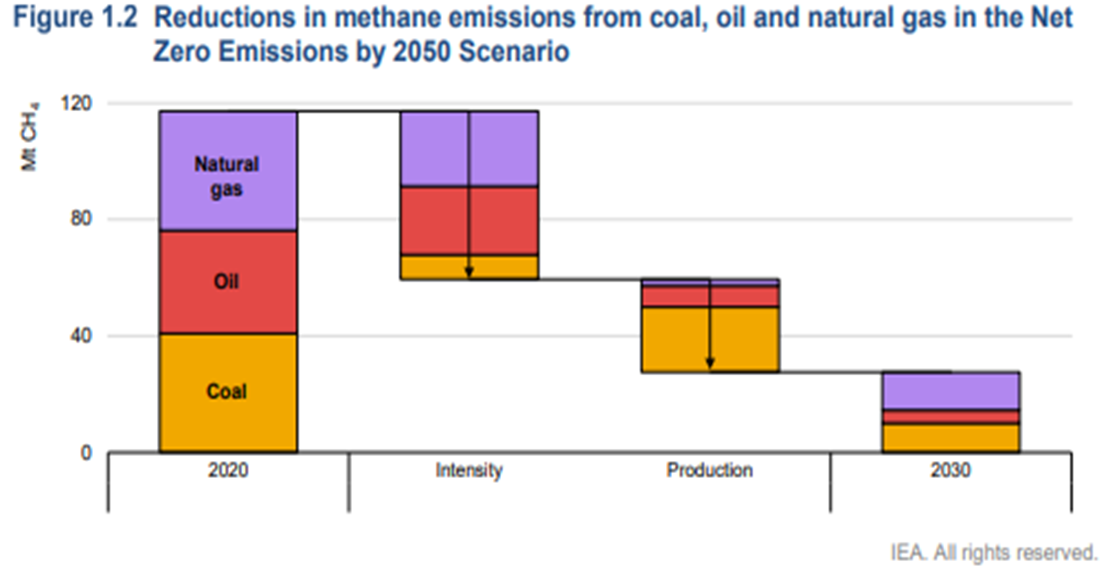

A couple of things worth highlighting in today's daily report – the first being Chevron’s move to join the net-zero club – focusing all eyes now on ExxonMobil in particular but also the rest of the US E&P crowd. Chevron will have some major challenges getting to net-zero and will likely face much of the same skepticism that bp, Shell, and TotalEnergies attracted in Europe initially and still face today. The Europeans have placed a lot of their bets on moving into renewable power – for the moment, Chevron is focused on moving to net zero in its own operations, which we read as biofuels and a lot of CCS. Given the acute shortage of international natural gas, it would make the most sense for the independent natural gas E&P companies and the LNG sellers to jump on the same boat. By promising low carbon natural gas and LNG, the industry is much more likely to gain support for the expansion that the world needs to counter some of the EIA assumptions around coal and petroleum product use from 2030 to 2050. Of course, it would be a whole lot easier for the US industry to do this if they had a value on carbon to work with! The chart below looks at one of the core clean-up issues, which is methane leakage. This is a subject we cover extensively in our ESG and Climate service linked here.

There are two elements/risks to ESG investing and both are highlighted in articles in today's daily report. The first is a reminder that returns matter and this is a reference to the very high multiples that are being applied to some of the more speculative clean energy stocks where there is credit being given today for technology and scale tomorrow. As with the tech bubble, there will inevitably be companies that fail, either because they have an offering that either will not work or will not be economic or because the market moves away from what they are doing. The fuel cell stocks would be at risk if hydrogen remains too expensive to consider as a transport fuel and if batteries or bio-based fuels become the dominant solution. Equally, bio-fuels could fall out of favor if hydrogen is abundant. On the polymer side, better collection and more chemical recycling could make switching to biodegradable polymers unnecessary or uneconomic. There will be winners and losers on this basis and the better strategy is to buy baskets of new technologies rather than bet on just one.

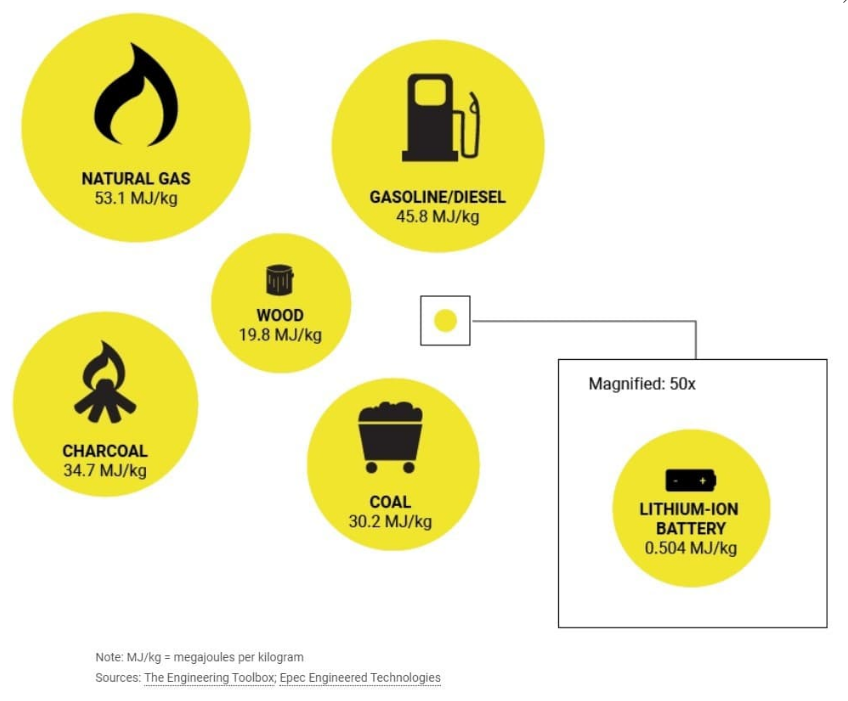

The decarbonization of the airline industry remains a hot topic. The energy density issue shown in the exhibit below is a correct assessment of why commercial aviation faces a challenge to transition to electric power. Not only is the energy density too low - which restricts weight/range - but electric power can only turn things, and propellor-based flying has speed limitations relative to jets. The announcements from the airlines to date on electric power have focused on low capacity short-haul opportunities. With this in mind and as noted in the article headlining of the exhibit below, electric power is not the only decarbonizing option for airlines. Hydrogen is the very long-term future - Airbus is saying not before 2050, but in the meantime, the push should be for low carbon or carbon-neutral biofuels. These are essentially plug-in fuels that are identical to current aviation fuel but made either from waste oils or from carbohydrates. Many of the oil majors are working on waste oil or vegetable oil-based processes, especially in California where the LCFS credit helps pay for the conversion, and companies like Gevo and Aemetis are working on carbohydrate-based routes through fermentation. If the carbohydrate, corn in the case of Gevo, is sourced from sustainable agriculture the carbon values of the fuel can be very low and potentially zero or negative through the life cycle. The airlines are going to have to pay up for the low carbon fuel if they want to bid the fuel away from the high credit markets like California diesel and gasoline, but this route could decarbonize the airlines significantly and relatively quickly with the right pricing structure and enough capital.

The ESG investment shakeup could be one of the major events of this year, and as many of the headlines in our daily report suggest, there is a lot of work to be done, whether it is agreeing on a common set of measurement metrics – note the US and European differences discussed in one story – or the introduction of more empirical methods to judge whether what is labeled as an ESG investment fund is labeled correctly. There is also the issue of comparable disclosures, especially for companies in complex industries. It is interesting to note that in many analyses we see around carbon footprint or greenhouse gas emissions, and the potential routes to and cost of abatement, the chemical industry is omitted, except for ethanol and hydrogen. This is despite the industry accounting for 15% of the non-power emissions in the US industrial sector (similar in size to refineries). We believe that this is because the complexity of the industry makes it hard to model, and analysts choose to exclude it because they are not sure what they are doing.

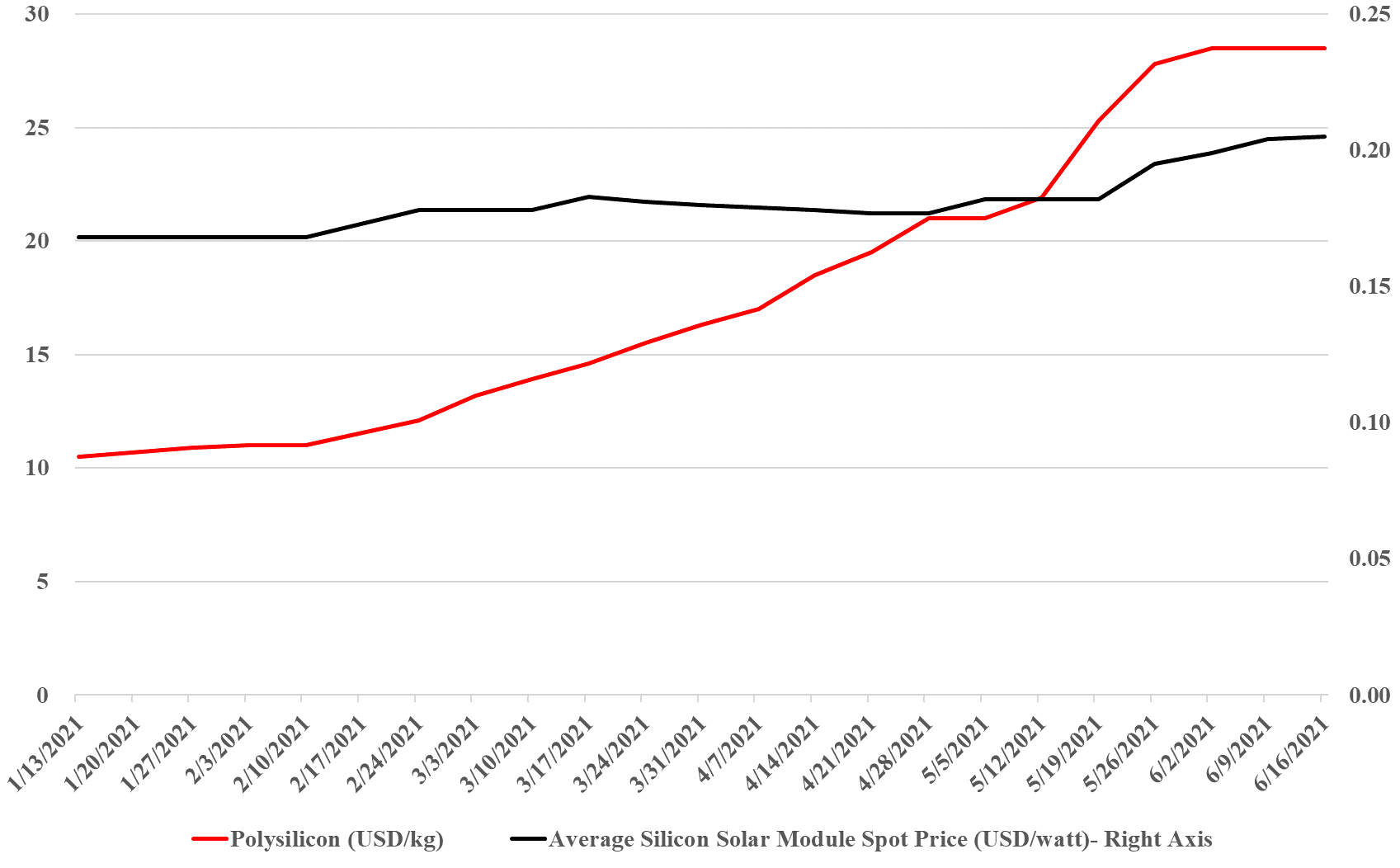

The exhibit below summarizes well one of the primary concerns that we have with some of the very ambitious goals for decarbonizing power grids, EV introduction, the further electrification of industry, and hydrogen. While the solar module price increase does not look that significant (yet), to put it in context, solar module prices have collapsed from over $1.80 per watt in 2010 to below $0.20 in 2020, and many of the expectations around cheap hydrogen require the cost to keep falling. The bigger concern is the polysilicon price, which is up 160% this year, good for the polysilicon producers like Wacker (see the headline here), but bad for the solar module producers, who are seeing major margin squeezes, especially given the rise in copper and silver as well this year. The raw material pressure should drive further increases in solar module pricing and while the higher margins for polysilicon will likely drive expansion investment, the metals are harder to call, given the ESG views on mining. We remain firmly of the view that raw material availability and price inflation, as well as module and wind turbine manufacturing capacity, will be the rate-determining constraint in terms of the growth in renewable power and this is why we question all of the near-term cheap power and cheap hydrogen goals that are being suggested by potential producers and government agencies.

The coverage of the IEA study continues with lots of opinions, which is a good sign as it means that the work is being taken seriously.

The most significant item worth discussing today is yesterday’s news that the API is likely to support a carbon pricing mechanism in the US. We will have more on this in our ESG and climate piece tomorrow. This is not a game-changer in itself, but it opens the door for one. Imposing a cost on emissions, whether a direct tax or a trading mechanism, as in Europe (but hopefully better managed in the early stages), will likely drive real change and significant investment, as it has done in Europe. The devil will be in the details and how many loopholes are attached to any regulation. For example, the chemical and energy industries are likely to lobby hard for no carbon taxes on exports for fear of losing competitiveness.

We should focus on the Gevo headline today (Gevo and HCS Group Sign Strategic Agreement to Produce Renewable Low-Carbon Chemicals and Sustainable Aviation Fuel in Europe) as it indicates further acceptance of the technology as well as the opportunities in aviation and other fuels. It is also interesting to note that HCS Group, which has signed the JV with Gevo, mentions low-carbon chemicals in the headline.