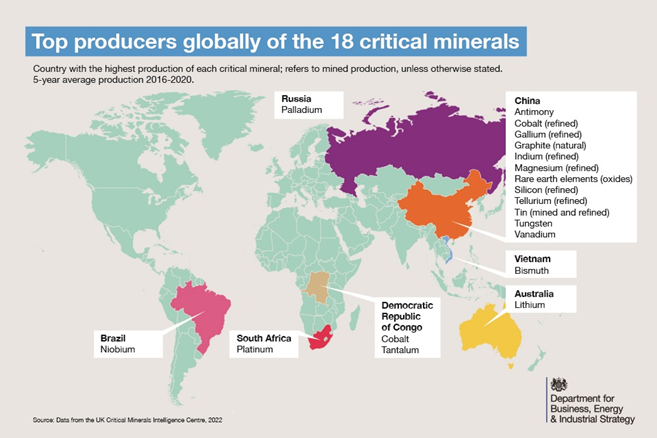

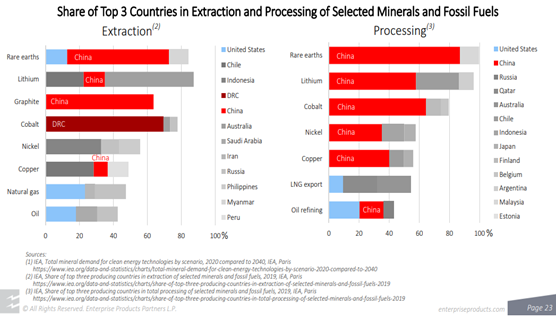

We are seeing more focus on supply chains as they relate to the energy transition. Some European countries are realizing what we have noted in prior research - EU Energy Policy: Swapping A Bad Supplier For Something Worse? - switching to an aggressive focus on renewable energy may reduce your energy exposure to Russia but it currently doubles down on your exposure to China. It is very easy to look at the scale of the problem – the share that China has in critical metals, as shown below – the share that China has of solar modules – etc., and conclude that it is too hard, especially in Europe where you will find an environmental lobby trying to stop you doing anything industrial. But the net effect is severe reliance on China. One advantage that the UK now has with its exit from the EU is more industrial freedom and the country could benefit from the right industrial policies that would attract broader energy transition investment. In our ESG and Climate report this week we talked about the U.S. desire to “friend-shore” rather than re-shore because of local investment challenges in the U.S. as a consequence of some of the political issues. The UK could benefit from becoming an industrial partner with the U.S. for some critical materials.

While longer-term use of oil and gas products is in Enterprise Products' best interest, it is nice to see someone else pushing the point that we have been making for more than a year – that there is not enough material out there, in the right locations, to meet the suggested clean energy goals. It is important that this becomes better understood and accepted by a broader group than just Enterprise and C-MACC, as we will not get the needed tack in strategy, priorities, and incentives if there is a broad reliance on renewable targets that will not be met – we focus on the IPCC report in tomorrow’s ESG and Climate report.

A couple of things worth noting today that reflects our commodity index in today's daily report but also looks at some of the results below. The linked solar headline is confirmation of one of the topics that we have probably worn out over the last few months, which is that renewable power ambitions have not taken into account real limitations in the rate of equipment supply, especially solar modules. New forecasts suggest that the US expected installations of solar capacity could come in 25% short in 2022, which has implications for energy transition ambition, but also overall power supply as the shortfall will have to be made up elsewhere. It is not just a function of solar module availability but also solar module costs, because of some of the material cost inflation illustrated in exhibit 1 (see today's daily report). These shortfalls will have implications for natural gas demand in the US if it needs to fill the gap, and we have already noted that we think US natural gas prices could spike in 2022, much higher than we saw in 2021.