We are seeing a flood of CCUS announcements in the US in 2022, but they look like “gathering” exercises at this stage rather than projects that are ready for FID. Companies are chasing potential pore space and, like Talos, leasing onshore and offshore (mainly offshore) acreage, where they believe opportunities exist to sequester CO2. These announcements sometimes include firm commitments from companies that have CO2 surpluses and sometimes are more speculative. At this stage, it seems like a “land grab” and “customer grab”. There is wide agreement that the incentive structure in the US – centered around the 45Q tax credit scheme – is not enough to drive much real investment, unless it can be stacked with other credits like the LCFS structure, which only applies to fuels in California today. We see the land grab as relatively low-cost and low-risk positioning in the hope that incentives or economics change. There are some instances where investments will go ahead, and these will focus on processes that have a reasonably low cost of carbon capture – fermentation, urea, natural gas clean-up for LNG, and a handful of other processes. The LSB Industries announcement for Arkansas, highlighted this week, is likely an example of where the economics work even if LSB cannot get much of a premium for the low-carbon urea.

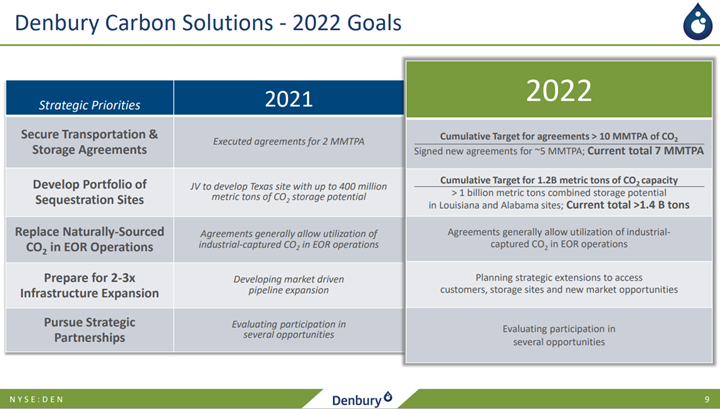

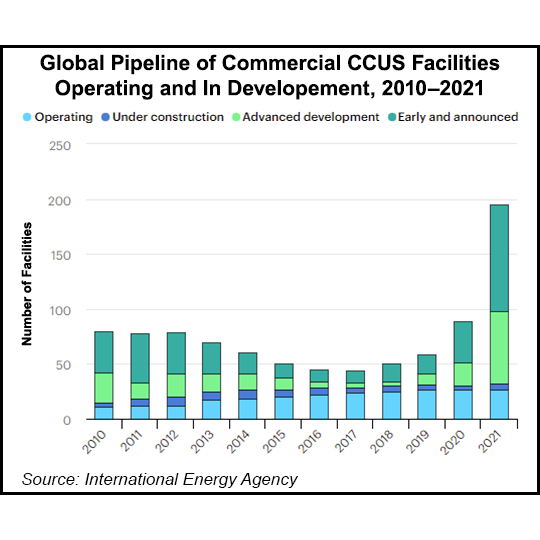

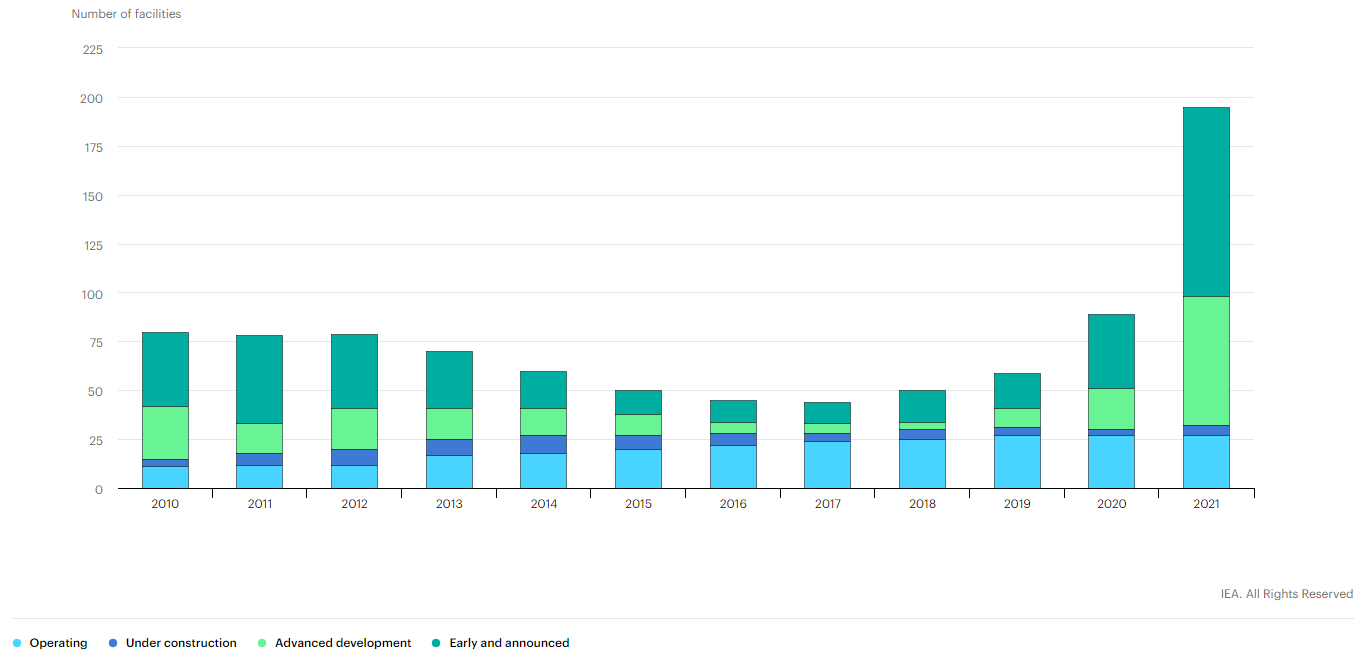

The CCS chart below is one that we have shown before and we make the same observations again as little has changed on the “action” side. The number of facilities under discussion, advanced or otherwise, continues to rise – see the Denbury announcement below, for instance - but very little is moving to the construction phase. While in the US this is in part a permitting issue, with the permit process taking several years, once you have a site plan, we get the sense that everyone is waiting for a more supportive incentive program – either a large CO2 penalty (tax) or an increased incentive – such as increasing the 45Q value. MOUs are being signed with landowners – as is the case with Denbury – and potential offtake partners, but very little cash is going out of the door for any of the US projects yet. Given the EIA analysis above, it would seem critical that something is done to move these projects from planning to action fairly quickly – if the US is going to need CCS at scale in 15-20 years, we need to start down that learning curve now. For more see the energy section of today's daily report.

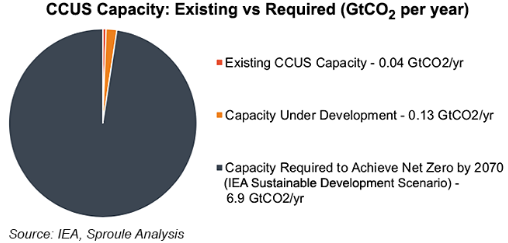

Most of the focus today is on carbon, in part because the CCS momentum is picking up, with more initiatives being announced daily all around the world, and partly because of the surge in European carbon prices as shown in Exhibit 1 from today's daily report. The IEA CCS projections in the Exhibit below, are likely low in our view, despite the significant investment needed to reach the target shown. In our ESG and climate report today we focus on many of the materials supply limitations that will likely emerge as the world tries to add wind and solar capacity at higher and higher rates. Our analysis of the IEA net-zero projections published earlier this year suggested that the IEA might be too ambitious on renewable power and that the balancing effect would likely be increased natural gas use versus its base case and more than forecast CCS. We have a long way to go to get there given the shortfall in the exhibit below, but at the same time, carbon prices are moving to make it happen. The European price has spiked again this week and is now slightly higher than $100 per ton of CO2, a level reached by the UK price late last week. At this level, we should see investments in Europe to abate carbon without additional local subsidies, or with minimal subsidies. The constraint in Europe will be finding inexpensive CCS locations. A $100 carbon price in the US would, in our opinion, drive a very significant investment in the US, not only in CCS capacity but also in new blue and green hydrogen capacity.

We note the IEA work on CCUS in several charts below and this is good timing relative to our ESG and climate report this week – which focused on carbon pricing, something we believe is necessary to promote more real activity in CCUS. In the Exhibit below, it is important to note how many projects are in “development” rather than operational or under construction. It is also worth noting that the number of projects under construction has not grown since 2019. One of the reasons for this is that increased activity at the planning stage is then followed by a delay associated with permitting, which depending on the region can take 2 plus years. The other constraint is uncertainty, with many of the projects under consideration waiting for something to change, either local values of CO2 or mandates or direct government support. For example, the large project planned for Houston and championed by several oil, power, and chemical companies is unlikely to move forward without a higher tax credit for CO2 sequestration or without some other incentive. The mid-West projects targeting the ethanol industry will also need permits, not just for the wells but also for the many hundreds of miles of proposed pipelines.

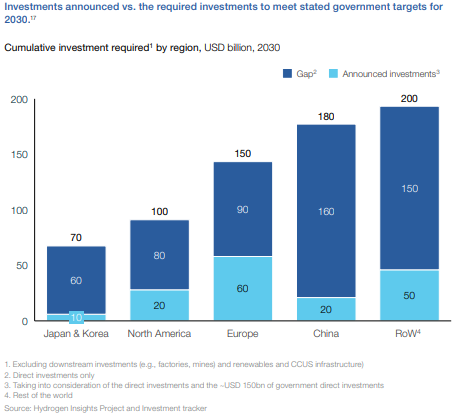

The hydrogen council chart below drags us away from 2050 and back to the more concerning near-term goals of 2030. The chart shows a significant gap in the current planned spend for hydrogen by region and the spending required to move far enough towards 2050 targets. This chart makes assumptions about the share of energy transition that will be met by hydrogen and given that it is the industry producing the chart, it is probably on the high side, but it is inclusive of both blue and green hydrogen. We have serious concerns about these totals being reached in general, but we see the target as completely unreachable without significant blue hydrogen (because of renewable power and electrolyzer capacity limits and we cannot rely on Canada to do all of the “heavy lifting” for blue hydrogen - see company section in today's daily report. The Biden administration may make more progress on emissions if the next order of business was just on CCUS rather than an omnibus bill that included CCUS but which could get held up in negotiations for months if it even gets passed.