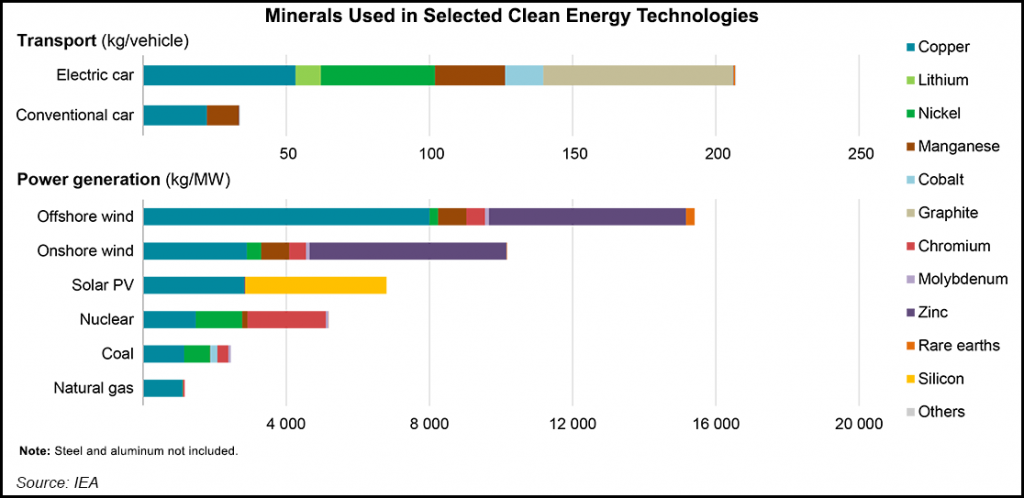

A couple of things worth noting today that reflects our commodity index in today's daily report but also looks at some of the results below. The linked solar headline is confirmation of one of the topics that we have probably worn out over the last few months, which is that renewable power ambitions have not taken into account real limitations in the rate of equipment supply, especially solar modules. New forecasts suggest that the US expected installations of solar capacity could come in 25% short in 2022, which has implications for energy transition ambition, but also overall power supply as the shortfall will have to be made up elsewhere. It is not just a function of solar module availability but also solar module costs, because of some of the material cost inflation illustrated in exhibit 1 (see today's daily report). These shortfalls will have implications for natural gas demand in the US if it needs to fill the gap, and we have already noted that we think US natural gas prices could spike in 2022, much higher than we saw in 2021.

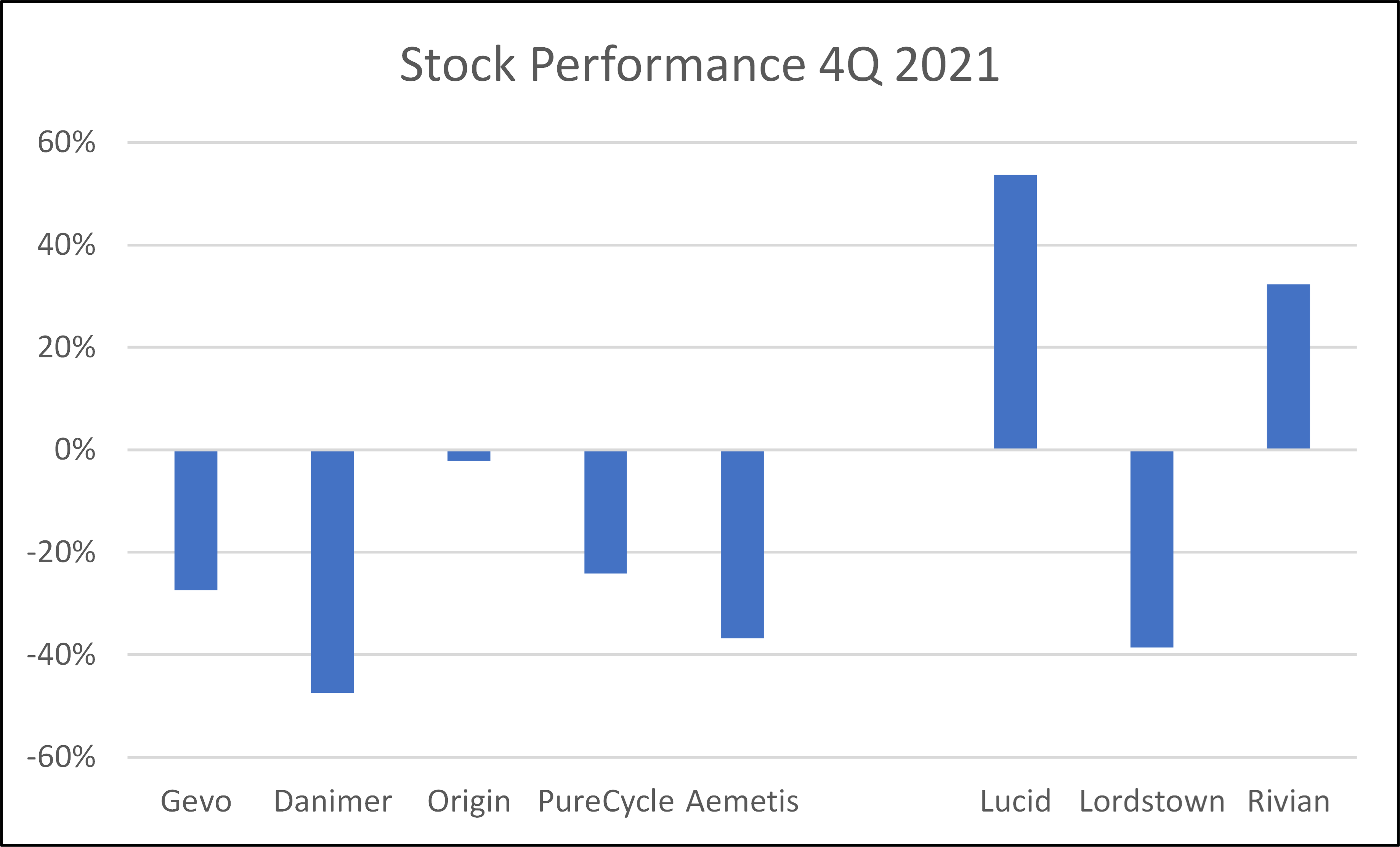

Life in 2022 is likely to be tougher for the new companies in materials and fuels, as all of them need capital to support projects that now look riskier from a cost inflation perspective and the market has moved to reflect that risk – Exhibit below. For every company below, the 2022 story was supposed to be capital spending to create commercial-scale production. The poor stock performance for many has tracked rising raw material prices – especially steel – as well as concerns around supply chain-driven delays and labor shortages. Few have the financial capacity to absorb significant cost overruns and/or construction delays. Danimer Scientific has done a recent capital raise and its impact created roughly half of the downside shown below – Danimer still likely needs more capital, but with more cash on the balance sheet may be able to get the rest through loans. Gevo, which in our view has the more impressive portfolio of potential offtake partners at this point likely plans to borrow at the facility level, and the stock weakness is likely a combination of inflation fears, the declining LCFS value, and the wait for the company to announce that it has a completed FEED study for the first plant and has reached FID. We would struggle to invest in any of these names today given the step-change in company development that each needs to make in 2022, and we would need more offtake agreements and process/construction guarantees than any company can likely get today, and if they could, they might not want to make some agreements public. See more in today's ESG and Climate report

Much of the core focus of both our chemical industry and ESG and Climate research recently has been on inflation and materials shortages; we would point you to: Inaction, Caused By Inflation Fears, Is Driving More Inflation! and Coming Up Short: Materials Availability To Limit Climate Progress. This linked article suggests that, as we have predicted, cost and availability pressures are taking a toll on solar installation plans for 2022 in the US. While the inflation piece is real and the product shortages highlight some of the capacity constraints for materials and panels, the broader conclusions that can be drawn from the headline are more concerning. These shortages (and higher prices) are coming well before we see any step change in attempts to increase renewable power installations associated with all of the green hydrogen projects that have been announced over the last 6-9 months. All of these investments are relying on the deflationary trends continuing, especially for onshore wind and solar.

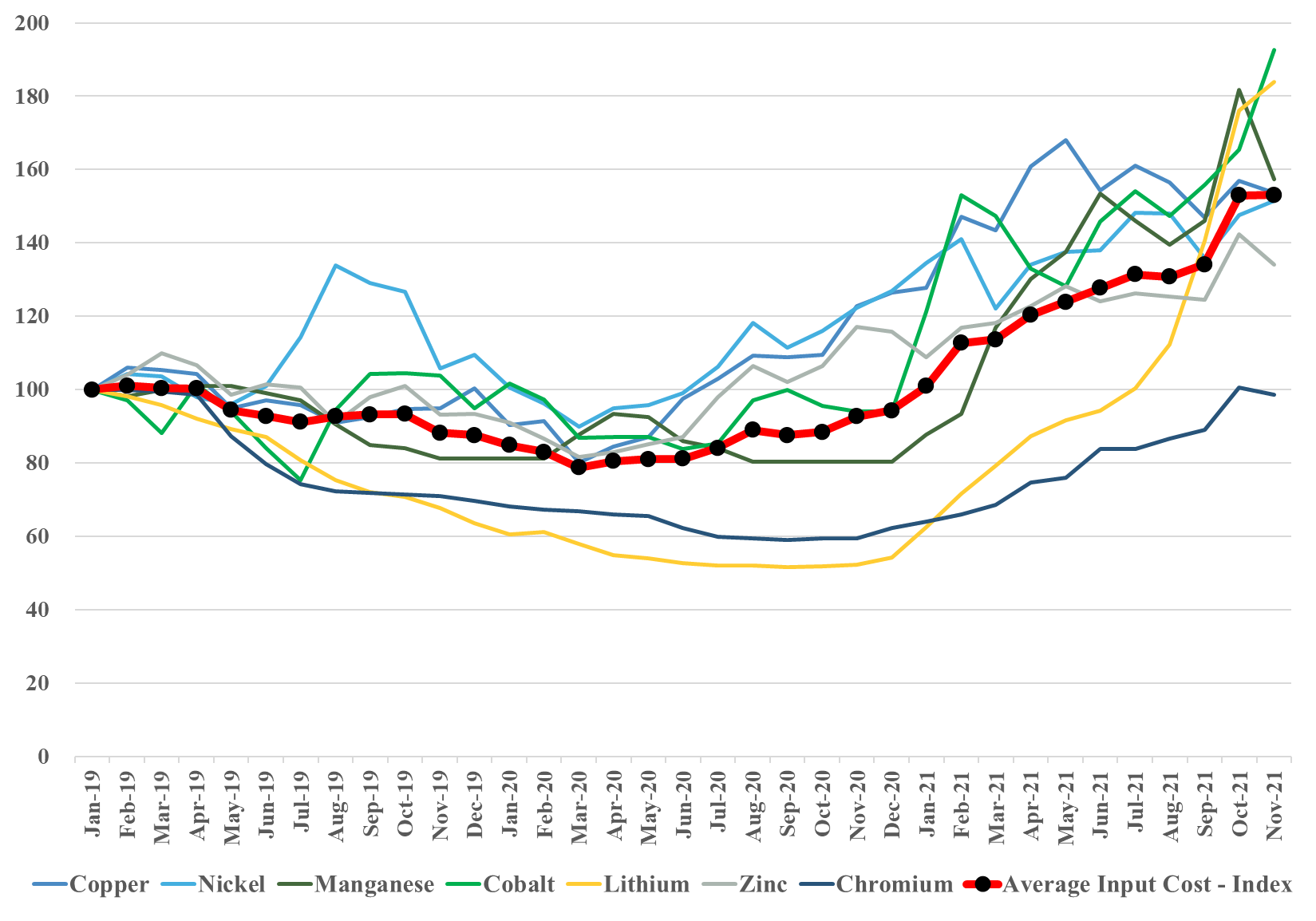

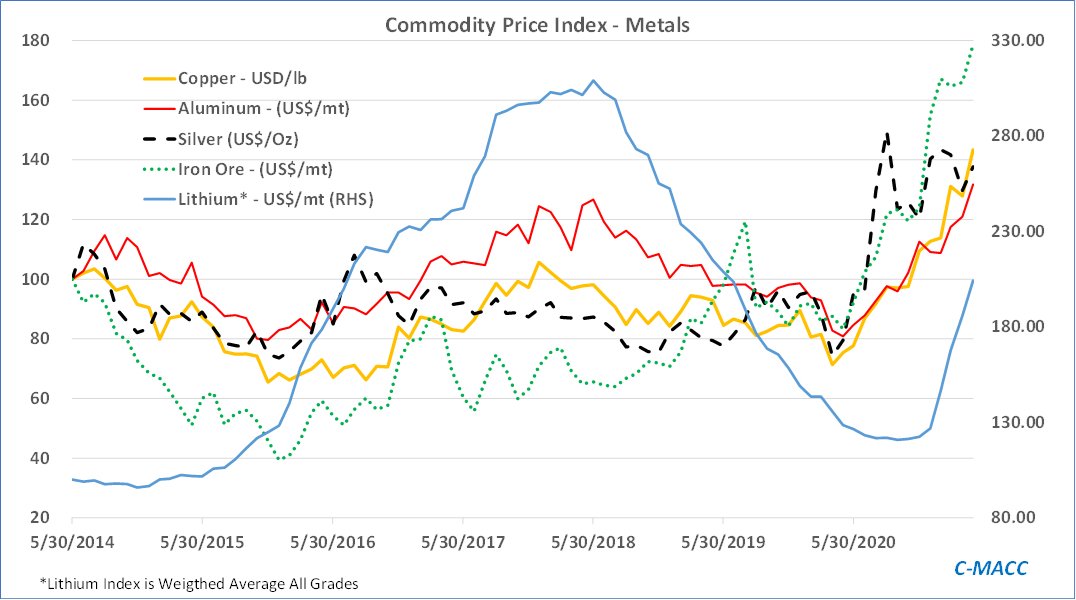

We focus today on raw material inflation and use the IEA analysis of materials demand (excluding steel and aluminum) in EVs and renewable power, creating a price index for the materials in question. This index is a straight average, but we will develop indices for specific sub-industries and include these in our next ESG and climate report. What is important is that the index below is up over 50% since the beginning of 2019 and this is before many of the EV plans and power plans move from planning to construction. We have highlighted inflation risk for more than a year now and remain very concerned that when many of the new auto plants start and many of the incremental renewable power facilities move from planning to equipment purchasing, we will see bottlenecks and faster price increases. See more in today's daily report.

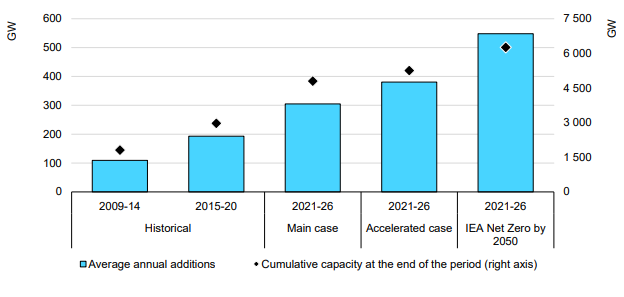

The core message of the IEA analysis published today is around how renewable power rates of investment remain far too low and need to more than double immediately to meet net-zero goals – see below. This analysis is very supportive of our renewable power inflation thesis, as none of the renewable power component manufacturers can double production either cheaply or quickly, and none of their suppliers has that much spare materials capacity. On the solar front, we may have the additional problem of regional production concentration. China has the largest share of capacity for solar module capacity and now has much more aggressive plans for solar power domestically. We could see China-based components stay in China, exaggerating shortages outside China. The IEA has an accompanying report today on the possible impact of commodity pricing on solar and wind pricing and it is also linked here – these reports were published this morning and we will cover them in more detail in next week's ESG and Climate report. More on this in today’s ESG and Climate report.

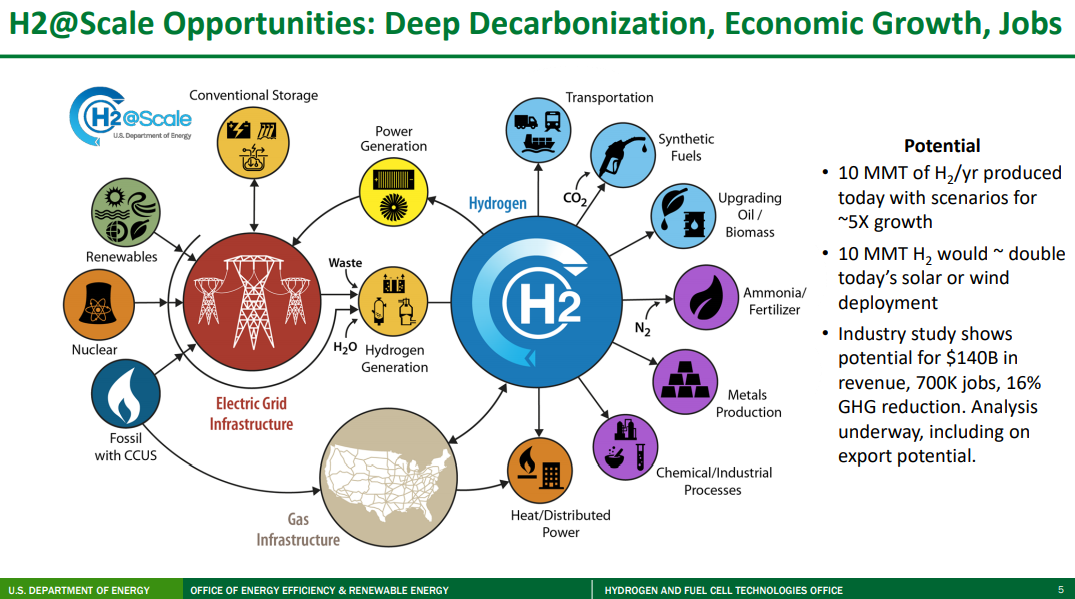

We will cover the very comprehensive DoE hydrogen work in more detail in the ESG report next week, but a couple of the charts from that work are worth mentioning today. The first picture below accurately depicts all of the potential uses of hydrogen and shows that over time it could solve a lot of “hard to solve” CO2 emission problems, especially where electricity cannot do the job efficiently. The reason why so many countries and companies are so interested in hydrogen is because of its potential versatility and because of its minimal carbon footprint (there is some carbon leakage in the full lifecycle of the production coming from construction around the plants themselves and infrastructure to use the hydrogen).

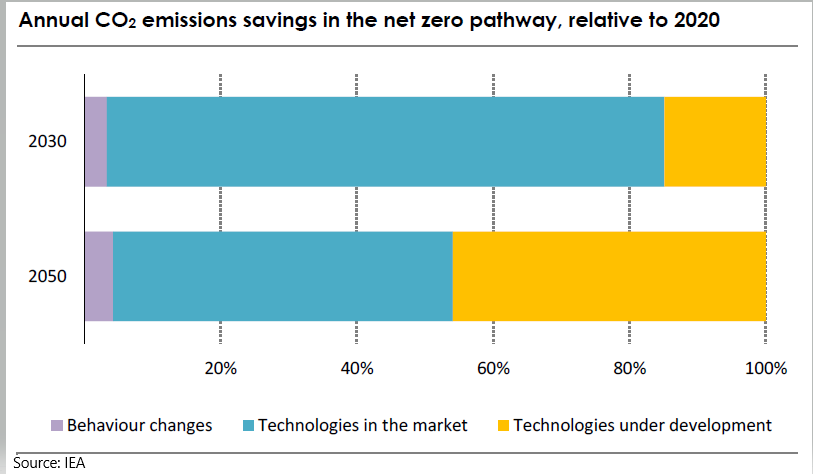

There are too many important topics to choose from today and we will cover many of these in our ESG and Climate report tomorrow. Here we focus on the IEA report published this week, which shows a path to net-zero on a global scale and looks at both the fossil fuel consuming sectors and the rate at which each must change (they are different by sector) and what fuel alternatives will be needed to replace them. Our review of the work would suggest the following:

Source: Bloomberg, C-MACC Analysis, May 2021

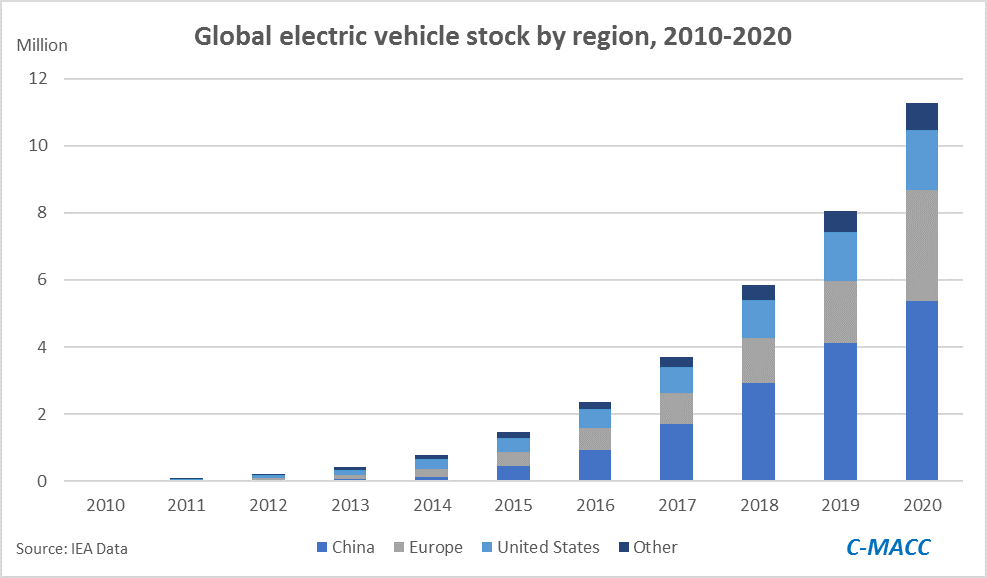

If you read our ESG and climate report which focused on the Biden agenda - The Biden Plan: Taking The Harder Path, Limiting Odds Of Success – you will understand how underwhelming the EV data is in the exhibit below. For the US to reduce its automotive transport carbon footprint to the proposed 2030 goals, the country would need to replace over 130 million ICE vehicles with EV or fuel cell-powered vehicles – 12x the total number of EVs in the world today and more than 100x the number currently in the US. This is a challenge that has almost zero chance of being met unless the benefit of switching is so high or the cost of not switching so high that consumers want to make the change – and – there are enough vehicles to buy. Both of these are remote possibilities today, but likely why we see increased focus on lithium, batteries, and faster roll-out of EVs from the majors as they attempt to do their part to move in the right direction. One unintended consequence that we have discussed at length and will cover in tomorrow's ESG and Climate report is inflation in materials, which will not be helped if the ESG lobby will not support the industries that need to provide the materials and the interlinking infrastructure investment.