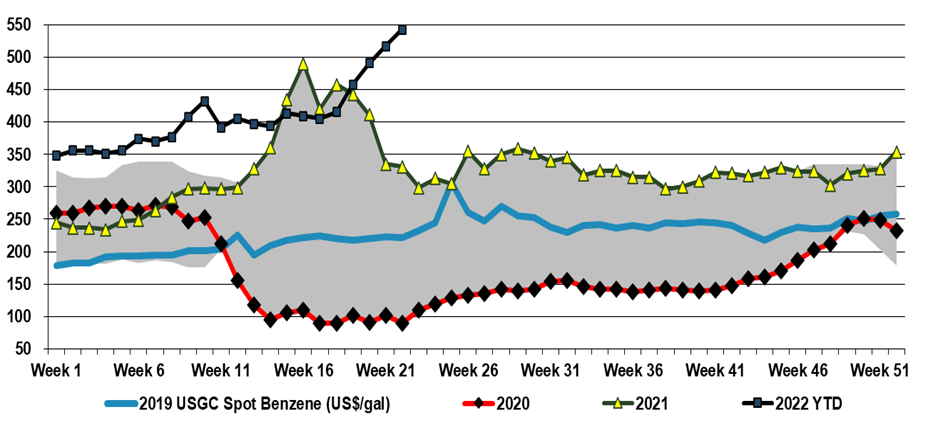

US benzene prices reflect both the net short market in the US but also the alternative value of reformate as a gasoline feed. While benzene is very limited in terms of how much can be left in fuel streams, its refinery-based feedstock, reformate, is a key component in gasoline – albeit low octane – prior to reforming and even during reforming the benzene conversion can be limited if the gasoline value is higher and volumes are constrained. In the US, as well as in many other parts of the world, we are facing gasoline shortages and today more than 13 US states have gasoline prices above $5 per gallon. While that may be shocking to Americans, the car ride from Heathrow yesterday was in a very popular make in the US that currently costs more than $200 to fill up in the UK! So benzene is getting squeezed – its feedstocks are more expensive and some of the alternatives to making benzene currently offer better netbacks. While we see all polymer costs rising in the US and elsewhere, this US benzene surge is not good for US polystyrene producers at a time when the industry is trying to justify polystyrene’s existence in a “circular” world, and it is also inflationary for the epoxy businesses, and other consumers of both styrene and phenol.

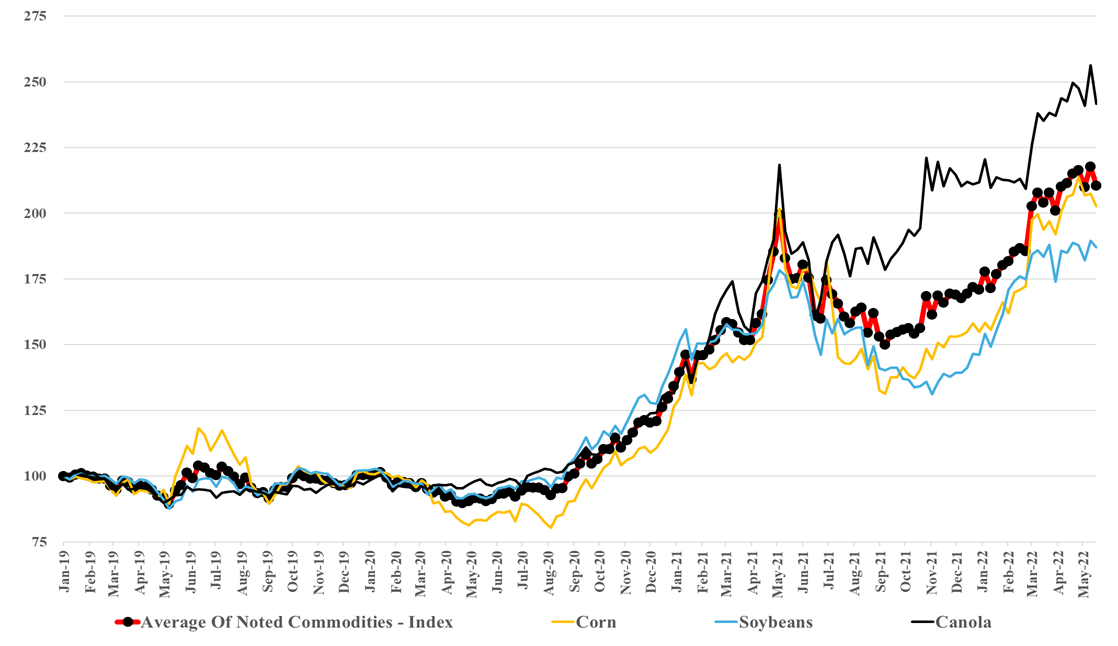

We have focused on agriculture this week with the ongoing announcements of new ammonia projects and the commodity crop prices and the overall index shown below are some of the key drivers of the activity in fertilizers but also are helping Ag equipment demand and we discuss the Deere results in today's daily report. We do not see how the trends in the chart below correct quickly and the profit through the farming, fertilizer, ag chemicals, and equipment chain should remain high in the US, at the expense of the consumer-facing high food prices (second chart below). We would need some coordinated medium-term policy to encourage moving more land in the US into agriculture, and this is especially necessary if we also intend to pursue bio-based fuels and materials. There has been much discussion around energy security over the last couple of months, but we think it is a much broader security discussion than just energy. Governments need to become much more accommodative around many aspects of production, food, energy, materials, etc. This accommodation can come with tighter emissions standards and emissions costs, but the primary objective should be to encourage more local production of many different things.

The US chemical rail volumes should be considered in the context of some of the slowing demand that has been indicated by companies downstream of chemicals, and we see this as further evidence for possible inventory build through the chain. Earlier in the year these builds would have been justified by supply chain issues that have plagued all segments of retail and manufacturing for close to two years, but today we should be at or above inventory comfort levels. We are calling for weakness in demand and some margin erosion in US chemicals and polymers in 2H 2022, before a strong rebound as early as 2024, but if buyers of polymers and chemicals and their customers look to reduce inventories more quickly, the landscape could change quickly. While this is possible, with the threat of higher energy prices very real, we would be surprised in anyone was interesting in dramatically lowering inventories today.

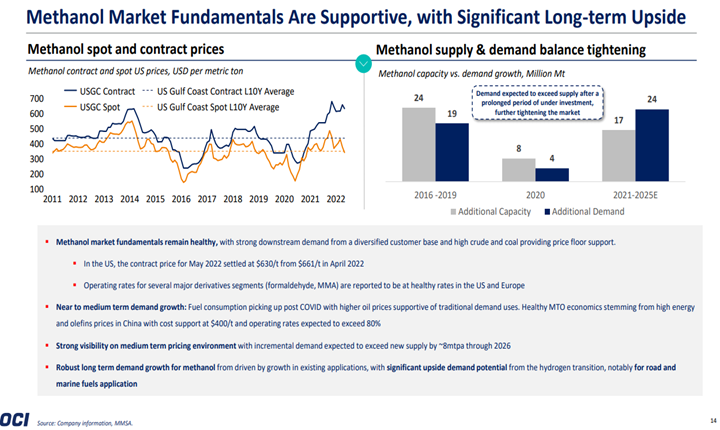

Today's apparent exceptions are in sectors very focused on energy security and transition, as we noted in our most recent Sunday Thematic, and agriculture, where crop shortages are driving up prices and demand for yield-enhancing inputs. In the OCI results below, we see a company doing well, despite having impacted assets in Europe. Still, we also see some potential upside in methanol as we head into the European winter, with the possibility that methanol is used as a fuel, essentially as a carrier for methane, and a workaround for constrained LNG infrastructure. As a fuel, it is not directly substituted for methane in any application, as it is a liquid, but some energy users might be able to adapt, and a $30 per MMBTU natural gas price in Europe can cause you to be quite creative. Of course, the methanol export opportunity for the US will depend on the US natural gas price remaining well below the price in Europe. For more see today's daily report.

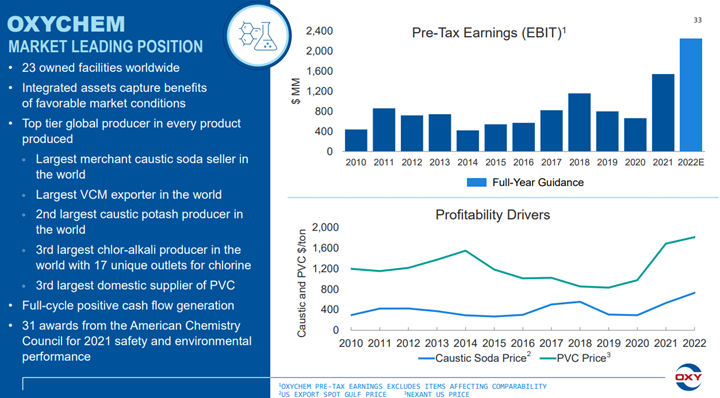

For those who are too young to remember, OxyChems’ 30-year comment is because the company owned ethylene capacity in the late 80s and early 90s and would have made more during that extreme ethylene peak. This is likely the most money that the stand-alone vinyls business has made. The strength in the PVC could see some reversal if the inflation pressure remains high and housing-related spending slows, but the strength in the caustic market could persist, regardless of economic growth because of structural shortages and the challenges with imports.

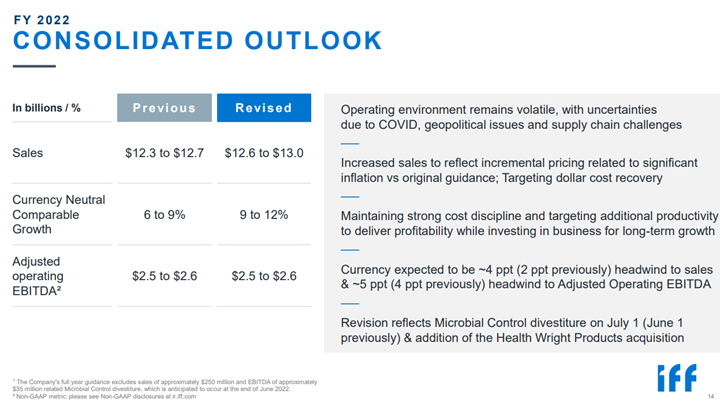

The pricing effect is very evident in the IFF results and projections, highlighted below. The company projected higher revenue expectations for the year but no increase in EBITDA with that higher revenue. We expect this trend to continue through at least the next couple of quarters, even if energy prices do not rise any further, as we believe that there is still some energy-related pass-through to come in many sectors. As the ammonia chart below shows, inputs in the agriculture/food industry keep rising.

In our Sunday Thematic to be published this weekend we are focused on business lines that will still look good in an economic turndown versus those that are more vulnerable, and ASIX may find itself spread across both buckets. The momentum in agriculture is very strong and even with a quick resolution in Ukraine, we could see high prices for crops and farm inputs for years as it will take a long time to correct recent imbalances and the Ag markets were already tightening before Russia invaded Ukraine. This and natural gas shortages (see today's daily report) should keep upward pressure on ammonia and ammonia derivatives pricing. On the other hand, any slowdown in consumer durable/discretionary spending will likely negatively impact nylon. A faster resolution in Ukraine would likely be negative for the Ag names as even if it takes a while to correct crop and fuel imbalances, the stock market will likely look through that and start focusing on eventual more normalized markets.

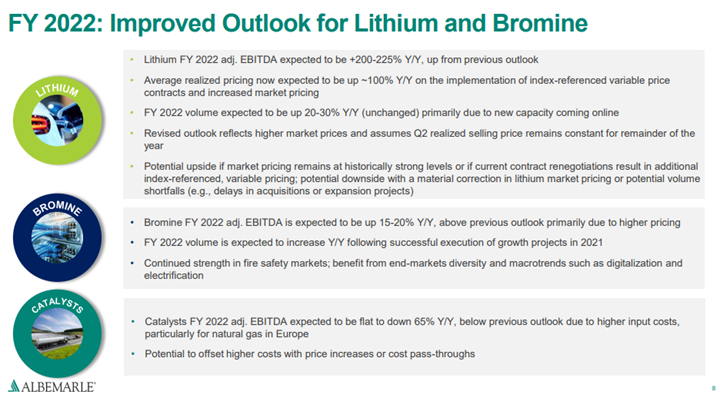

We should not be surprised by the blow-out earnings this week from Livent and Albemarle, as our “critical metals” analysis has been highlighting the runaway prices for lithium all year. This price rise has a much more profound impact on the current suppliers than the start-ups that either have minimal volumes to sell today or none at all. Both Livent and Albemarle were established players in lithium long before the current hype. The higher valuation for Albemarle is both a blessing and a curse in our view as the company is now a little hamstrung with respect to further portfolio changes, given that no one will pay as much for the catalyst and bromine businesses as is reflected in current valuation. You would need to be very convinced that the more focused lithium portfolio would see a further step up in valuation multiple to account for what would inevitably be earnings dilutive divestments.

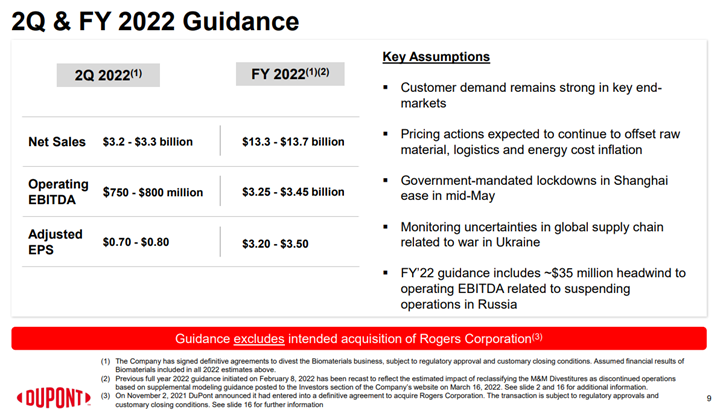

Like many of the European producers, DuPont has taken a risk in our view by holding guidance flat in the face of inflation, weakness in China, and a potential further economic slowdown in Europe and the US. We struggle with what an alternative approach should be for DuPont and others, given that it would be challenging to map out a credible downside scenario today. What we would note, however, is that when things turn negative for the materials industries they tend to fall quickly and sharply. For all of the base chemical and specialty chemical companies what might upset things for 2022 are largely outside of their control, and it is hard to second guess cutbacks in customer demand until they happen, especially in an environment where all are looking at volatile costs from energy and consumer spending uncertainty because of inflation. For more see today's daily report.

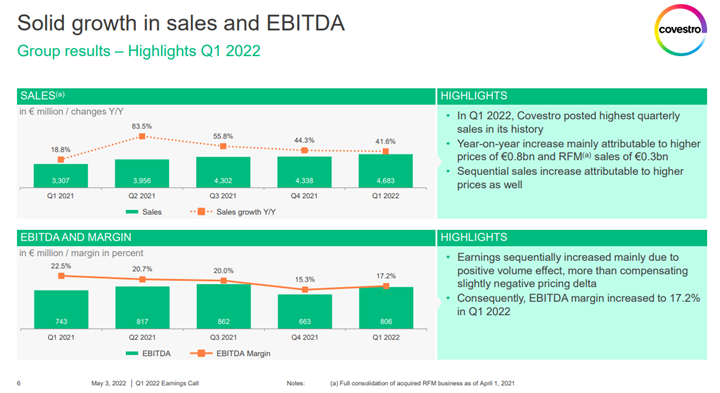

We reflect back on our BASF comments of last week and see Covestro falling into the same trap, by underestimating the potential slowdown in discretionary spending in Europe (and the US) and consequently putting too much hope into revised guidance. At the same time, we are not sure what would be gained by painting a picture of doom and gloom, but we would hedge much more overtly if we were offering guidance around the business outlook today.