Despite all of the rhetoric about the need for green hydrogen, we see most of the large ammonia producers pursuing large blue projects – with Nutrien’s announcement yesterday coming on the heels of a CF new facility announcement and the CO2 capture project announced by LSB a couple of weeks ago. While there are some small (proof of concept) green projects in the works, they are very small, tiny when compared with the ammonia need, whether to replace lost material from Russia and Ukraine or whether to supply what could be substantial needs in Asia to co-fire coal plants, or as a shipping fuel, or as a carrier for hydrogen (see third chart below). The ammonia majors are not waiting around for “green” economics to improve as they see meaningful near-term demand that cannot wait for scale efficiencies of available power on the green side. Large-scale sources of cheap renewable power are hard to find, and where they may exist, there is competition from uses that may be able to pay more.

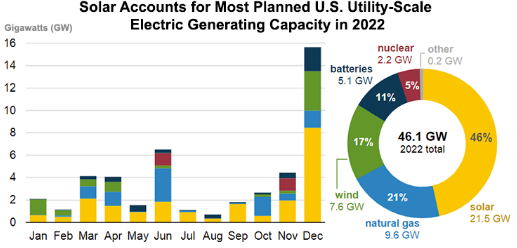

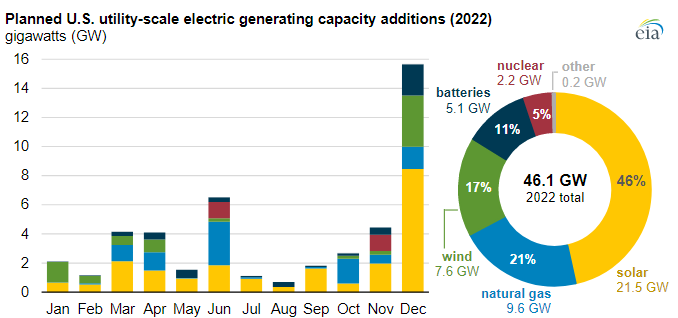

The back-end loading of the power projects for the US for 2022, as shown in the chart below leaves us somewhat skeptical concerning how much will come online this year. Supply chain problems and materials costs and availability are causing all sorts of problems with renewable power projects and installed capacity expectations for 2021 were too ambitious. We believe that companies are pushing projected start-ups later in the year to give them more of a chance of completion, but this creates the risk that they slip into 2023 or beyond. The most significant issue here is that as these plans get delayed, natural gas demand goes up, as one of the swing suppliers. This is fine as long as the US natural gas industry and shale oil industry is investing so that gas availability rises. Otherwise, we could see gas prices spike in the US next winter and another year where we use more coal than we expected. For more see this week's ESG and Climate report.

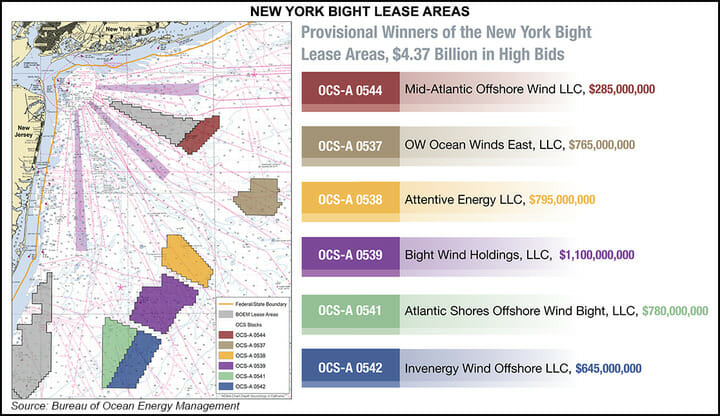

We include a couple of headlines and charts in today's daily report that step into the central theme of this week’s ESG and climate report, which will be published tomorrow (see here). The offshore wind ambitions and the EIA solar and battery projections both assume that the materials are available to build the capacity. In the case of the offshore wind leases, the winning bidders do not need to be in the market for all of the projects today and while the opportunities will lead to a step-change in demand for turbines in the US, the timing is less clear today that it will be in a few months and that timing may be adjusted to reflects equipment timing and costs, etc.

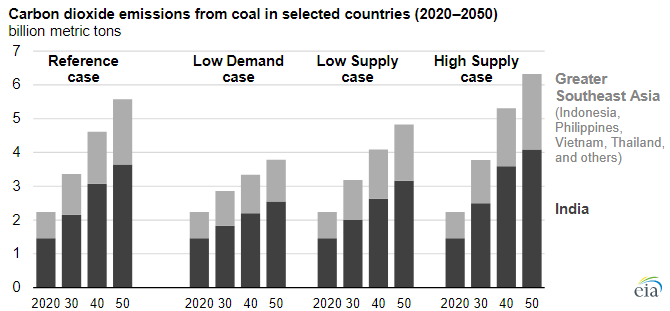

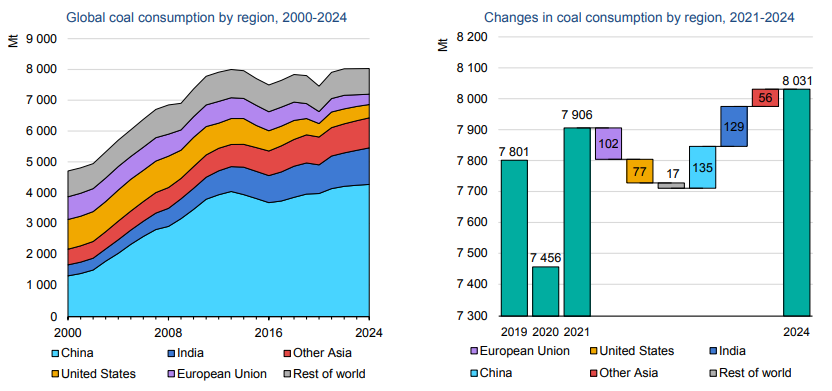

The coal data in the Exhibit below is likely not popular with the environmental lobby. However, the EIA analysis takes into account the alternatives for the countries involved and the fortunes of coal in these countries will be directly impacted by the help that other countries offer. If the region can be assured of abundant sources of alternative energy, whether renewables or more likely LNG, then the use of coal will fall. This is another example of where some of the global energy policies are coming up short in our view. The better solution is to champion (clean) LNG growth, wherever possible, to bridge the huge gap between the energy the world needs and the rate at which it can be supplied from renewables. See more in today's daily report.

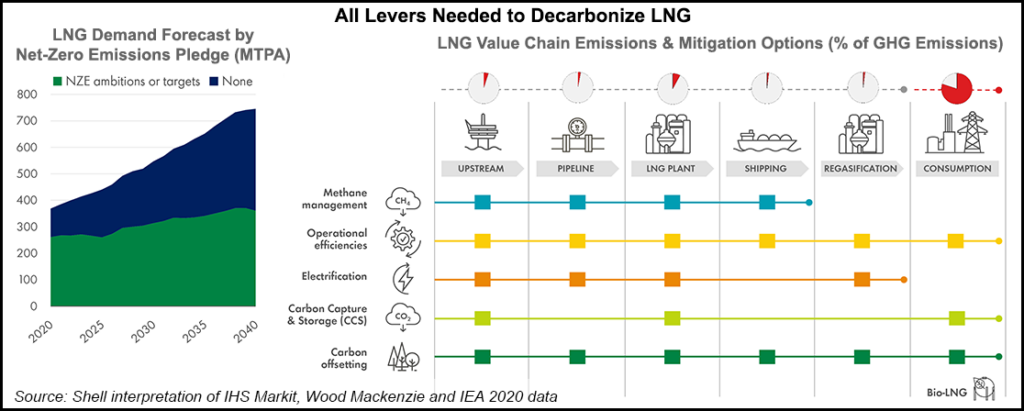

The first chart below has been included in a similar form in prior work and is a good summary of what is needed to decarbonize the LNG market to the greatest degree possible. There is a lot of resistance to the idea of endorsing natural gas as a transition fuel, but so many developed and developing countries need natural gas – often in the form of LNG – to displace or avoid (additional) coal use. If the LNG industry does not start to pursue the paths suggested in the exhibit, and reasonably quickly, it will stand very little chance of winning, or perhaps surviving, a PR battle that is very much stacked against it.

First, it is going to be an uphill struggle to get some common sense around the continued use of fossil fuels during any period of energy transition if the activists take away all resources from the energy industry – banking, PR, etc. While there is plenty of work to be done to minimize greenwashing, there is also plenty of work that needs to be done to explain why fossil fuels are still needed and how we can use them as cleanly as possible. If it becomes a business risk to bank or advise any company in the fossil fuel industry, while there will inevitably be workarounds, the net effect will be continued underinvestment, in production and in cleaning up the fuels and the concerns that we raised for natural gas in our Sunday Thematic will happen.

In yesterday's ESG and Climate report, we looked at an extreme example of how the right support for clean fossil fuel use through a long period of energy transition, could create economic growth, support job growth, and not require subsidies – coal gasification to produce low-cost hydrogen. With the opposition to the “Build Back Better” bill, there is a clear opportunity for the fossil fuel industry to step up and suggest compromises, and we are seeing increasing interest in large scale CCS, despite its cost, in part because it is a path that will allow natural gas and other fossil fuels to meet increasing demand in a way that has a much lower carbon footprint, and in part, because it will still be cheaper than some of the heavily subsidized ideas to try and accelerate investments in renewable power that will inevitably fall foul of equipment and material shortages – something we have written about at length in past research – linked here. The EIA has already noted that coal use in 2021 has risen globally and it is likely that it will rise again, given the increasing demand for electric power and the lack of supply elasticity in the renewable power and natural gas-based systems – coal is a large part of the swing capacity these days. Many of the CCS projects proposed for the US are not much more than proposals today, but we are seeing some initial investment to prove that subsurface storage opportunities are feasible.

While we would generally avoid quoting work from a company that we might consider a peripheral competitor, we are happy to do so when it backs up one of our central themes – in this case, inflation in renewable power costs. The quote is taken from the Wood Mackenzie report flagged article linked here and discusses a view on how challenges that renewable power installers have faced in 2021 will extend into 2022. The quote talks about shortages of renewable power equipment, and the obvious consequence will be higher prices for that equipment, especially as raw material prices for components remain high and possibly move higher. In our ESG and Climate report today, we talk about the need for some commonsense oversight such that impractical ESG investing targets do not limit the ability of producers of critical fuels and materials to operate.

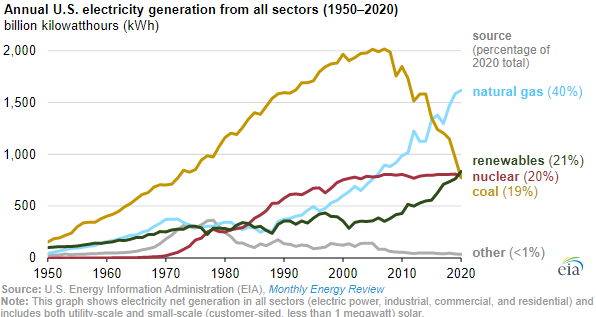

International natural gas prices are hitting new highs this week, both on an absolute basis and relative to the US - see both charts below. At the same time, we see new contracts being signed for US LNG to move to China and Europe, but mainly China. This is happening despite significant renewable power investments globally in 2021 and it would appear that many have underestimated energy demand growth in projections and policy. The other net effect of the supply/demand imbalance this winter and possibly through 2022 will be increased coal use in Europe and the US, with local governments unable to meet near-term climate goals, especially in Europe, but also in parts of Asia and, at the same time keep the people warm and the lights on. In our ESG and Climate piece tomorrow we will focus on one highly unpopular but likely very practical opportunity for coal as part of a planned energy transition program, and it is likely that, while climate goals may not need to change, some socially unpopular decisions around the use of fossil fuels will be needed to prevent even more socially unpopular inflation or absolute shortages.

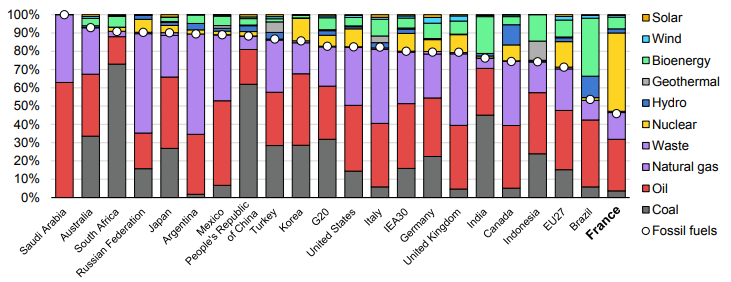

The fuel use data in the Exhibit below is very much a function of geology and the good and bad luck associated with it. The large hydrocarbon users' consumption patterns are a function of what they have – if you have a lot of coal, you use a lot of coal. The significant build-out of nuclear in France is partly because of Frances’ exceptional track record with the technology but also because the country does not have anything else to fall back on. Japan’s nuclear component was much higher before Fukashima. It is, however, worth noting the almost insignificant share of wind and solar anywhere, and then to put this into context with the collective ambitions, not just for 2050, but for the much shorter 2030 targets.