There should be little doubt that the US has a significant opportunity to decarbonize through CCS and if the US has a carbon value close to the level in Europe today we would be seeing investments announced almost weekly. While permitting would cause some significant lead time between announcement and construction/operation, the other uncertainty might be how best to capture the CO2. In its earnings release yesterday, CF talked about purifying CO2 streams at its two large Urea plants on the Gulf Coast, such that the CO2 would be ready to sequester, but the Urea process creates a relatively concentrated stream of CO2 and that makes separation much easier. For others, the better route might be hydrogen investments – driven by the relative ease of capturing the CO2, especially if it is part of the process design. If this route is more economic, the net new investment would be substantial, not just for the SMR, ATR, or fuel cell hydrogen generators, but also for the infrastructure and oxygen capacity for any ATR investment. This seems like a no-brainer bi-partisan opportunity for the US as there is broad support for CCS but incentives need to be higher. For more on this topic see our ESG and Climate research.

The linked Canada headline supports one of the themes that we have been highlighting for a while, which is that certainty around carbon pricing is likely to drive investment rather than discourage it. Canada, and specifically Alberta, has seen several new investments announced over the last few months because manufacturers can now add some certainty around carbon values to other advantages offered by the province, including cheap natural gas and what appears to be low-cost CCS opportunities. We are also seeing investments shape up in Europe – also to produce low carbon materials and fuels – and this is also driven by greater certainty around carbon value. The lack of a carbon price in the US is becoming a competitive disadvantage for the country and those opposing it in government are, in our view, very misguided. If China can develop a credible and broad carbon pricing mechanism, it will also likely gain investment dollars, possibly at the expense of the US. Not having a sound climate change and carbon value framework in the US is a major threat to many of the reshoring initiatives that US retailers and manufacturers would like to see.

The Financial Times opinion piece linked in the bullet below and from which the chart is taken has used the IEA data that we have featured in recent work. The piece comprehensively walks through how the world is likely to come up short, and while it gives the measures that are needed and the money that likely needs to be spent, it is not an optimistic review of what will most likely occur. We remain firmly of the belief that much more progress could be made if there was a global agreement to make carbon very expensive – accompanied by an agreement on how to share the spoils of that expensive carbon such that the inflationary pressures are offset where they are most needed and that environmental injustices are minimized – this is idealistic are we recognize that.

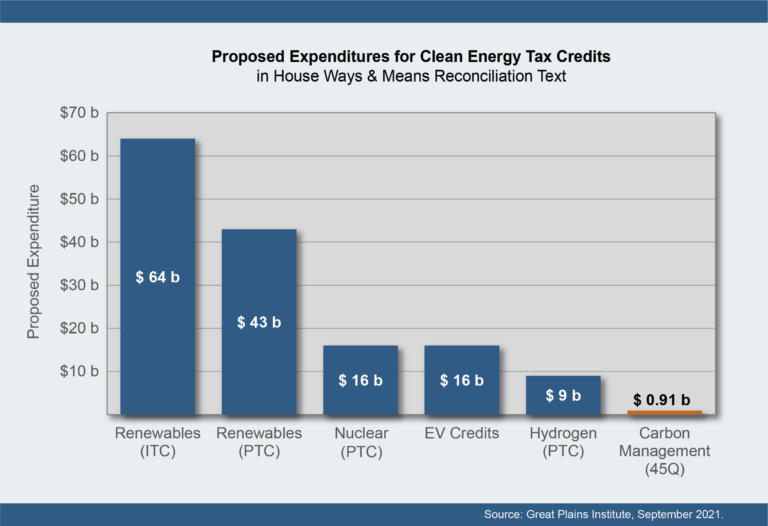

The tax credits suggested for 45Q in the budget reconciliation plan – see Exhibit below – would pay for roughly 18 million tons of CO2 sequestered or used in EOR over the life of the budget, assuming a credit value of $50 per ton of carbon. While this may seem huge in the context of the current levels of CCS in the US, the country had around 2.5 billion tons of emissions in 2019 that could be addressed with CCS (power and industrials), and if we assume 10% of that needs to be dealt with through CCS, the 45Q provisions in the budget reconciliation would cover less than 8% of the volume for one year and the percentage will be even lower if the “CATCH” act is successful in driving the 45Q value to $85 per ton of CO2. So the numbers are either inadequate, or the government is assuming that the levels of CCS in the US will be much lower than the potential – note that the ExxonMobil proposal for a hub in and around Texas talked about the maximum size for the one project being as much as 100 million tons per annum which should equate to $5 billion of tax credits – per annum. See our ESG & Climate report for much more on carbon markets today.

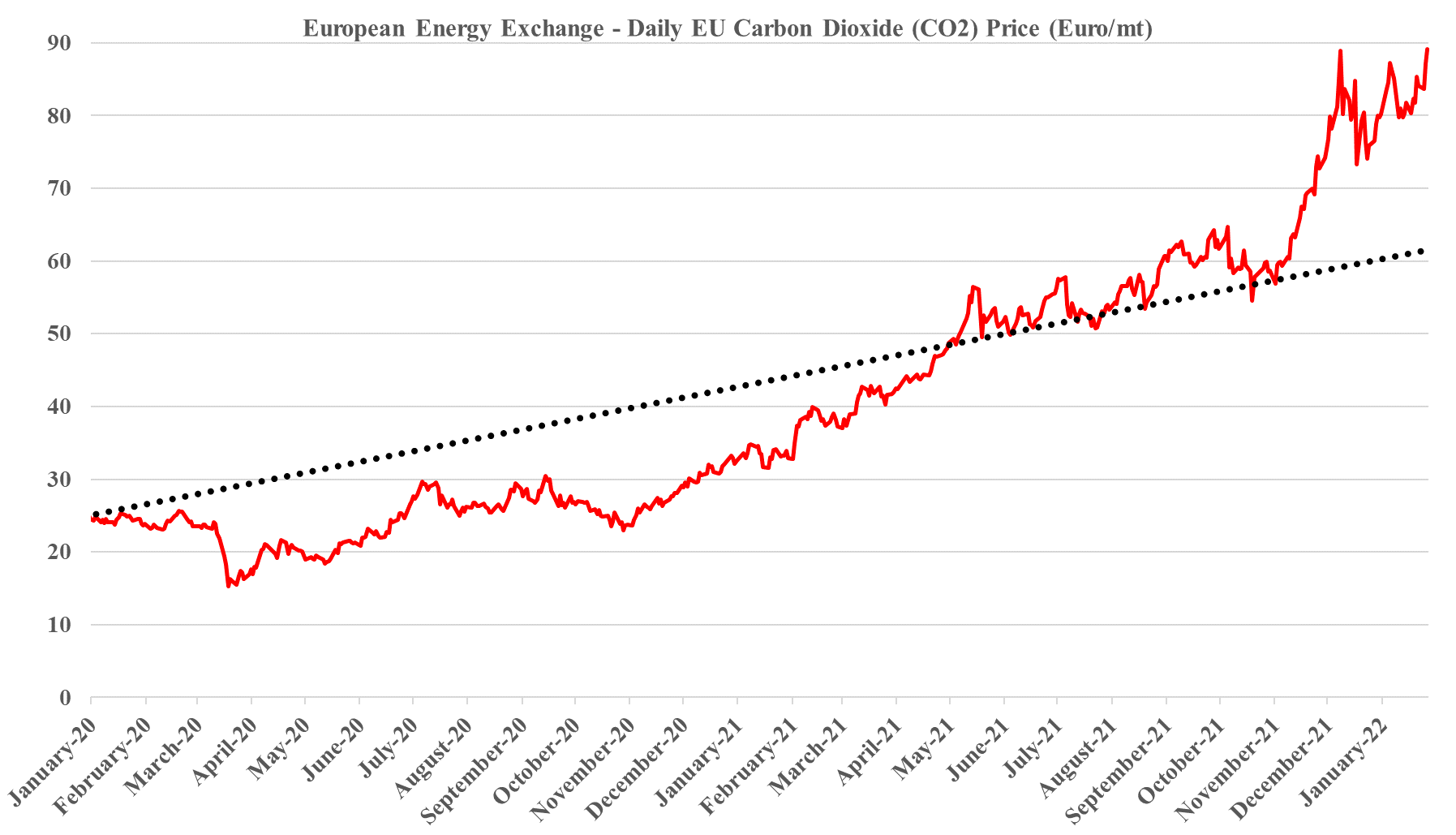

We have maintained all year that the strength in the European carbon price is sustainable and that it should go even higher and consequently, we are not surprised by this week’s move, even if much of the impetus is speculation. The European price is still not high enough to justify unsubsidized CCS or widespread renewable power investments to replace carbon-heavy energy sources, especially as renewable power costs rise. We estimate that a price in the €85-100 per metric ton range would be needed to stimulate investment, but because of the structure of the European market prices could overshoot this level meaningfully and be quite volatile until the level of abatement spending accelerates. When we start seeing investments in Europe to lower carbon that are not highly subsidized by local governments (in addition to the incentive of the carbon price) we will have a better guide around where 45Q needs to go in the US (or other mechanisms) to get investments rolling. Our analysis suggests that the US has some lower-cost abatement opportunities than Europe, especially on the CCS front, but not by much. For more on carbon costs and prices see today's ESG & Climate report.

Finally, Larry Fink has recognized the flaw in his aggressive ESG rhetoric. Maybe he knew this all along, but it is good to see him step into the debate in favor of not crippling the fossil fuel industry by denying it access to capital and investors too quickly. However, that boat may have sailed, with investors like Engine No. 1 feeling empowered by their win over ExxonMobil and raising more money as a consequence. We have covered this subject at length in our ESG and climate weekly this week: Big Oil’s Big Problem – Hard To Find A Favorable Scenario – maybe Larry read it!