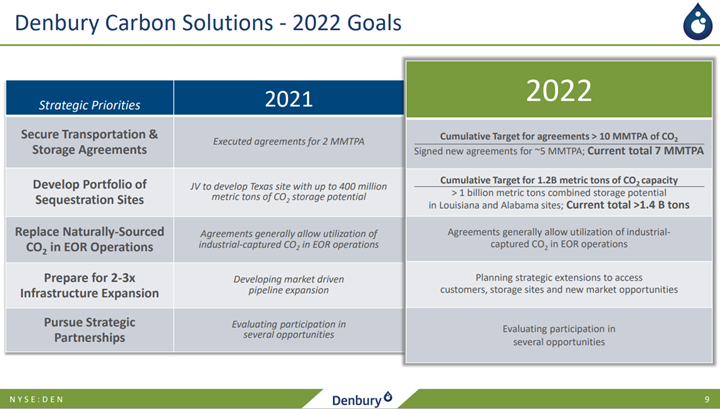

We are seeing a flood of CCUS announcements in the US in 2022, but they look like “gathering” exercises at this stage rather than projects that are ready for FID. Companies are chasing potential pore space and, like Talos, leasing onshore and offshore (mainly offshore) acreage, where they believe opportunities exist to sequester CO2. These announcements sometimes include firm commitments from companies that have CO2 surpluses and sometimes are more speculative. At this stage, it seems like a “land grab” and “customer grab”. There is wide agreement that the incentive structure in the US – centered around the 45Q tax credit scheme – is not enough to drive much real investment, unless it can be stacked with other credits like the LCFS structure, which only applies to fuels in California today. We see the land grab as relatively low-cost and low-risk positioning in the hope that incentives or economics change. There are some instances where investments will go ahead, and these will focus on processes that have a reasonably low cost of carbon capture – fermentation, urea, natural gas clean-up for LNG, and a handful of other processes. The LSB Industries announcement for Arkansas, highlighted this week, is likely an example of where the economics work even if LSB cannot get much of a premium for the low-carbon urea.

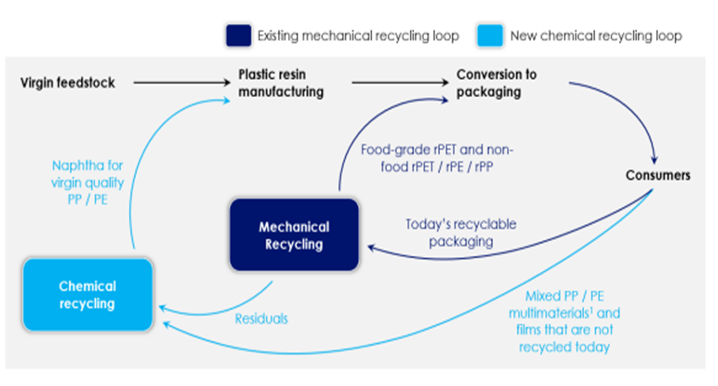

In the first picture below we see another schematic that shows how different options for polymer recycling could work together. We have suggested a more complex site than the one in the chart as there will be opportunities to recycle some polymers into non-like-for-like applications such as roadbed modification and other durable applications. In addition, there may be a better return in waste to energy versus chemical recycling and that may be an alternative or an add-on. This sort of complex site is what we believe LyondellBasell could be looking at for the Houston refinery site. An integrated waste treatment facility that optimizes that use for each tranche of the waste stream could improve the overall investment returns. In the second picture below we show our version of what a comprehensive waste recycling operation should look like. See more on recycling!

As we look at the news flow on recycling, we see many initiatives to collect, sort, and reuse polymers, whether for like-for-like applications, pyrolysis, or energy. What we do not see enough of, in our view, are initiatives to increase the pool of recycled plastics through packaging standardization or the elimination of compounds or colors that make recycling more challenging. Recycling can be improved by better collection and sorting methodologies and technologies. Still, the rate-limiting step will eventually be the pool of materials fit for recycling, and this is particularly important for like-for-like mechanical recycling. The ironic piece here is that the consumer staples and beverage companies call for higher recycled content and are primarily responsible for the amount of recyclable material in the market. If the packagers were to focus on sustainability rather than the unique look and feel of their packaging, we would see a material change in the volumes of recyclable polymers. This might come at the expense of some of the compounders, especially those with an extensive packaging component to their customer base, but it might also impact specific polymers and we would highlight polystyrene as a particularly vulnerable material as almost any application for which polystyrene is used today could be replaced with PET, polyethylene and/or polyethylene – all of which are larger volume polymers that are easier to recycle. The polystyrene industry is doing a good job of promoting recycling initiatives, but this may not be enough.

Our recent work on recycling - Recycling: Beware Of The Misleading PR – would suggest that the UK treasury will raise quite a bit of money from the plastics tax. We see very little chance of most packaging meeting a 30% recycled content goal any time soon, and possibly ever. We could see an odd dynamic where UK packagers import recycled resin from the EU to meet the minimums. This would then be at odds with EU recycled content goals and would need the EU to do something similar on the tax front to avoid the trade. The EU has a plastic tax in the works and its net effect will be similar to the one in the UK – any trade arbitrage for recycled resin would not likely last long.

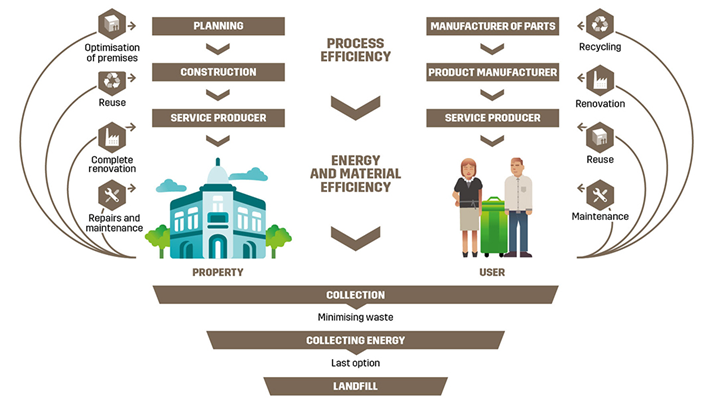

We tend to focus on recycling conventional plastic waste, but there are growing initiatives to look at the longer life cycle of durables and while this has mostly been focused on the automotive space, it is interesting to see the building industry looking at building life cycles. Many of the alternative use mechanical recycling initiatives are directed toward substituting building products such as concrete and wood and while this will help the construction sustainability story, the end of life cycle issue is less clear. The majority of commercial real-estate emissions are associated with operations (around 70%) and this is the greater focus for owners today, but the life cycle question is increasingly important for building tenants. In the UK for example there are redevelopment projects proactively advertising how much of the original building will be retained – i.e. not demolished and landfilled. Ultimately this might lead to lower demand for commercial building products where developers are looking at existing buildings, but it will not impact new greenfield builds unless you get a steep increase in recycled polymer use. The offset would likely be concrete as this is the high carbon footprint material that most are targeting. See more in today's ESG and Climate Report.

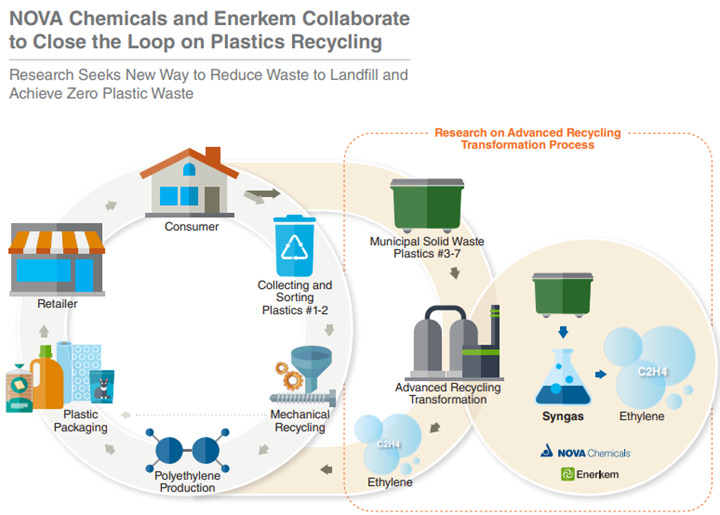

The focus of our ESG and Climate report tomorrow will be on recycling and the challenges associated with each proposed solution. The piece that most chemical recycling projects, like the one highlighted below, fail to mention is that the heat required for pyrolysis is significant, and the carbon footprint is very high unless you can heat through renewable power or you can capture the carbon associated with the heat. Given the location of the facility shown below, it could have access to offshore wind-based power and/or could tie into one of the offshore CCS projects that have been proposed. Both pyrolysis and gasification processes have very high emissions.

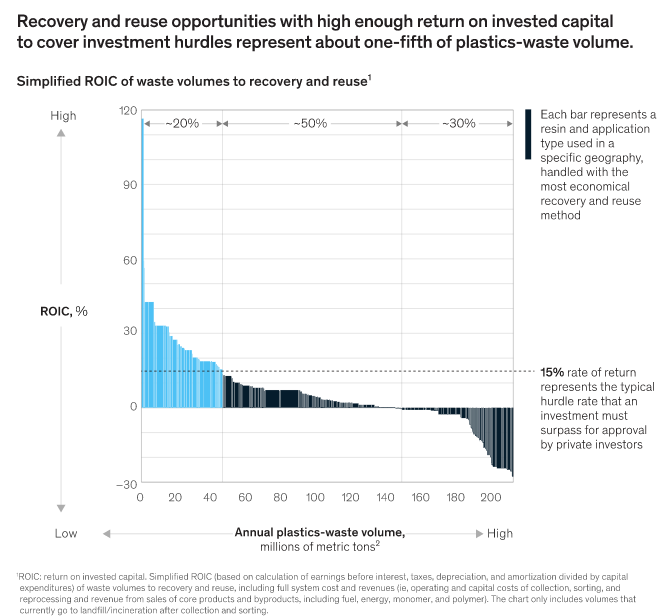

The McKinsey analysis is likely spot-on, as it is very difficult to get enough recycled polymer to produce a mechanically recycled stream that can be used in the highest value same use market. Solving for this is complicated by many factors, with too many stakeholders in many of the chains to make it work:

The linked Covestro headline from today's ESG & Climate report is a reminder that the chemicals and polymer makers are dealing with more than just recycling and product lifecycle management. Customers are equally focused on the carbon footprint of the products they buy and the green hydrogen move by Covestro (assuming that affordable green hydrogen is possible) would replace hydrogen made from fossil fuels and replace other fuels for heat in some cases. Germany has some considerable issues with decarbonizing, as the blue hydrogen route will be challenging in a country that will likely not allow onshore CCS. Covestro and others may have little choice but to buy green hydrogen and/or green power, even if supplies come up short of plan and costs are higher as a result. This is a good illustration of why we believe that the right policies in the US could drive some additional competitive edge while meeting climate objectives. Cheap hydrocarbons coupled with cheap CCS may only be matched in some parts of the Middle East.

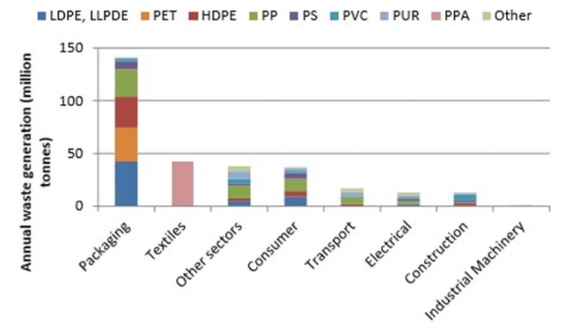

We have spent a lot of time over the last few weeks talking about polymer recycling and renewables and the chart below is another look at where plastic waste is coming from. Packaging is the big piece and it is also the area where customers, i.e. the packagers, are looking for the largest increase in the use of recycled materials quickly. As we noted in our ESG and Climate piece this week, increasing volumes of this packaging waste is moving into different use applications, such as building products and durables, and even more could potentially flow into chemical recycling – note that there are 7 headlines on chemical/advanced recycling in today's daily report. The packagers have little chance of meeting their near-term recycling content goals in our opinion, but they have zero chance if they do not accept chemical recycling as part of the mix. It will be important to accurately audit the chain of custody of chemical recycling to avoid double counting. The separate challenge with chemical recycling is the now increased focus on carbon footprints, as the pyrolysis process is energy-intensive, whether direct heat from burning fossil fuel or electric power-based heat.

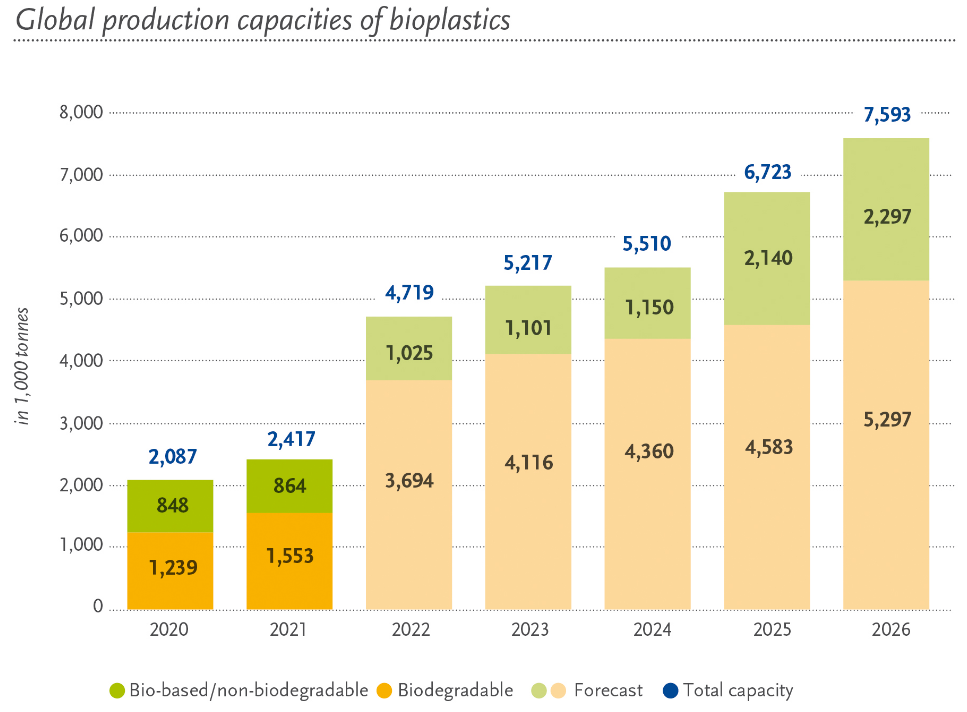

The bioplastics chart below (from today's daily report) is interesting from a couple of perspectives, the first being whether the projections are reasonable and the second being the significance of the investments. We believe that the volume targets are optimistic, given the capital requirements and that many of the companies pursuing bioplastics are relatively new and need to borrow most or all of the capital needs. The volumes would be easier to believe if the participants were large companies with strong balance sheets. The second point is just how small the volumes are in the grand scheme of plastics. Global demand for plastics exceeds 300 million tons and consequently, the 2026 projection would account for only 2.5% of global polymer demand. Note that in the article (linked here) around the uptake of biodegradable plastics – in this case in the UEA – one of the constraints to growth listed is availability. The other constraint, which likely faces producers in all markets is consumer education. Introducing a new polymer – or range of polymers – into an already confusing mix will require consumer education around what is biodegradable and what to do with the material. This topic follows on from the recycling theme in last week's ESG and Climate Report.