In our ESG and Climate report tomorrow, we will focus on SAF from a carbon intensity perspective. The Colonial pipeline initiative was inevitable given the demand for jet fuel at the East Coast airports. Still, we would not expect much volume to move in the near term for several reasons. First, there is not that much to move, and second, California can still pay more because of the LCFS credit. The Biden administration is planning to introduce a broad SAF credit which would help encourage use outside California, but this would also need to stimulate production as the volumes are still small and much smaller than the airlines would want – even the projection of volumes by bodies like the IEA fall well short of potential airline demand by 2030 and 2040. This is an investable theme, in our view, and we will discuss it in more detail tomorrow.

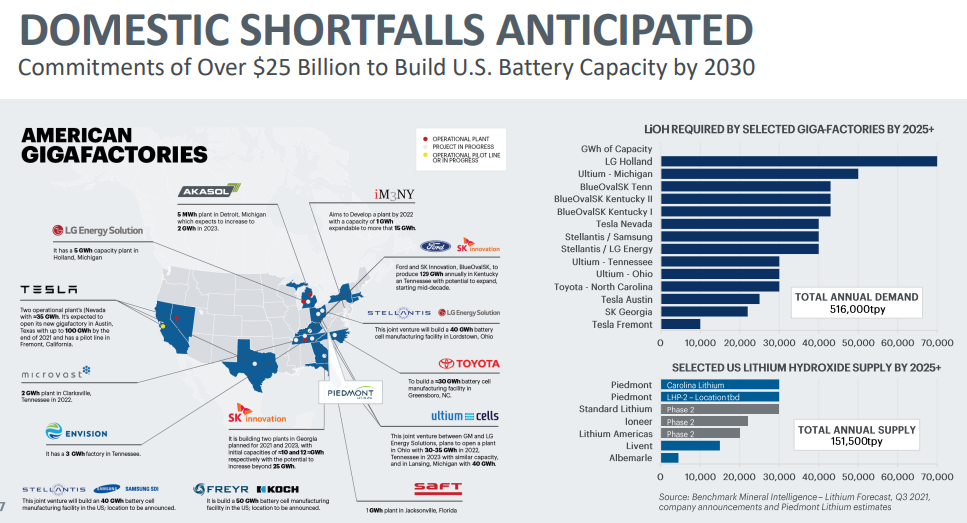

While the Piedmont Lithium analysis below makes for a compelling graphic, lithium has been a globally traded product for decades and there is an expectation that the growing lithium demand in the US will be largely met through imports. One of the significant positives of the Piedmont analysis is that it shows that US producers should have some sort of margin umbrella associated with pricing being based on import economics. That may not seem important today, given the extremely high price of lithium, but it will be important when lithium is oversupplied, which in our view is an inevitability – eventually. The barriers to entry for lithium are low and the buyer enthusiasm for new projects is very high. At some point, we will overbuild relative to demand and the net short nature of the US market may be critically important to companies like Piedmont, whose costs may not be the lowest. For more see today's ESG and Climate report.

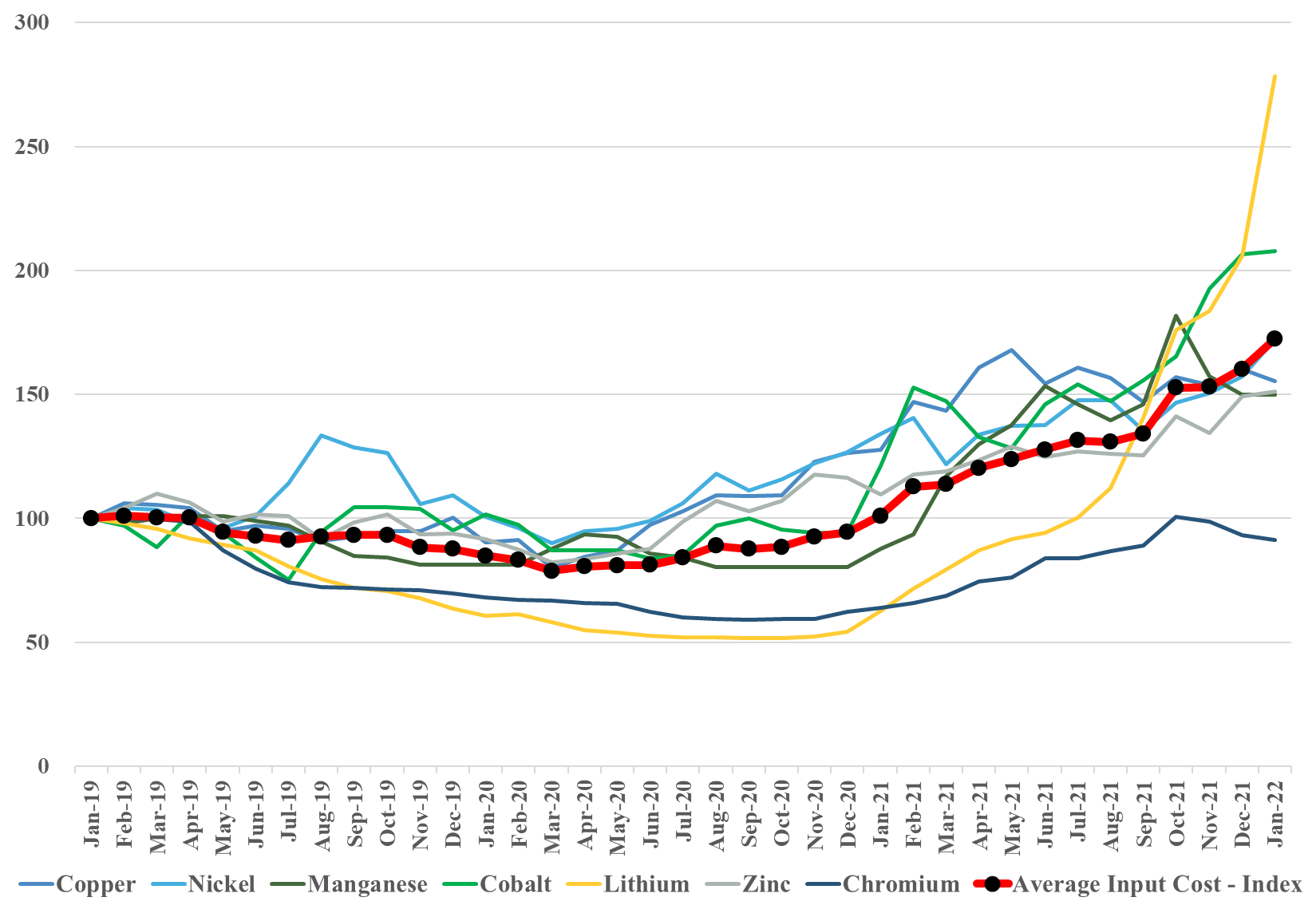

As the chart below shows, the demand, real and speculative, for lithium continues to drive prices materially higher. As new EV models prepare to launch this year and new battery facilities come online there is an inevitable supply chain impact to build inventory, whether it is the battery facilities building an inventory of lithium and other components or the automakers building an inventory of batteries. This will inflate lithium and other critical material demand relative to the vehicle output and this may be driving some of the demand panic for lithium. However, this dynamic is unlikely to be transitory in the near term, as there is a long wave of new EV capacity coming online, all of which will drive some incremental working capital build. We still believe that supply growth for lithium is very high and that the market could flip from famine to feast and back again quite quickly and frequently over the next few years although maybe not in 2022. Also see today's daily report and last week's ESG and Climate report for more on this topic.

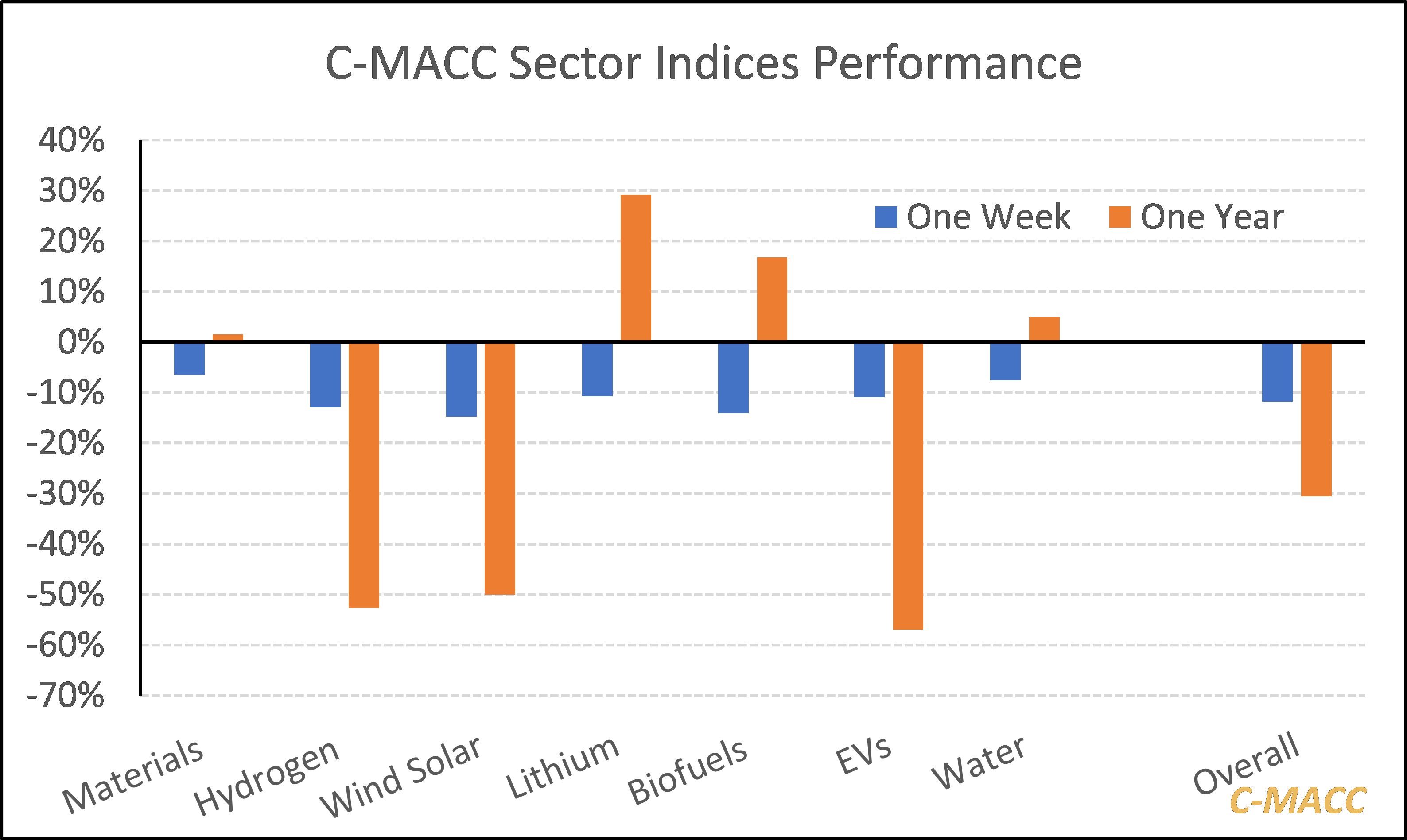

In last week's ESG & Climate report titled The Evolution Of the Plastic Industry Could Stall in 2022, we introduced our “new materials” stock index, and we have included our hydrogen index in this week's report titled, Hydrogen – Hype, Hope, and Headlines. We have created these for several sectors and each week we will add the chart below showing one-week and one-year performance for each index. Note that these are simple averages for each group and are not market cap-weighted. If we did a market cap weighting, we would have a couple of sectors where one stock dominated all - EVs for example. The steep decline in the EV index in 2021 was largely due to the negative performance of the Chinese EV companies that trade in the US and are included in the index. Note that all sectors have had a bad start to this year. We have chosen to include a water category as we have noted since we began this service that water is an area that we believe will be in greater focus going forward and will be considered an ESG topic.

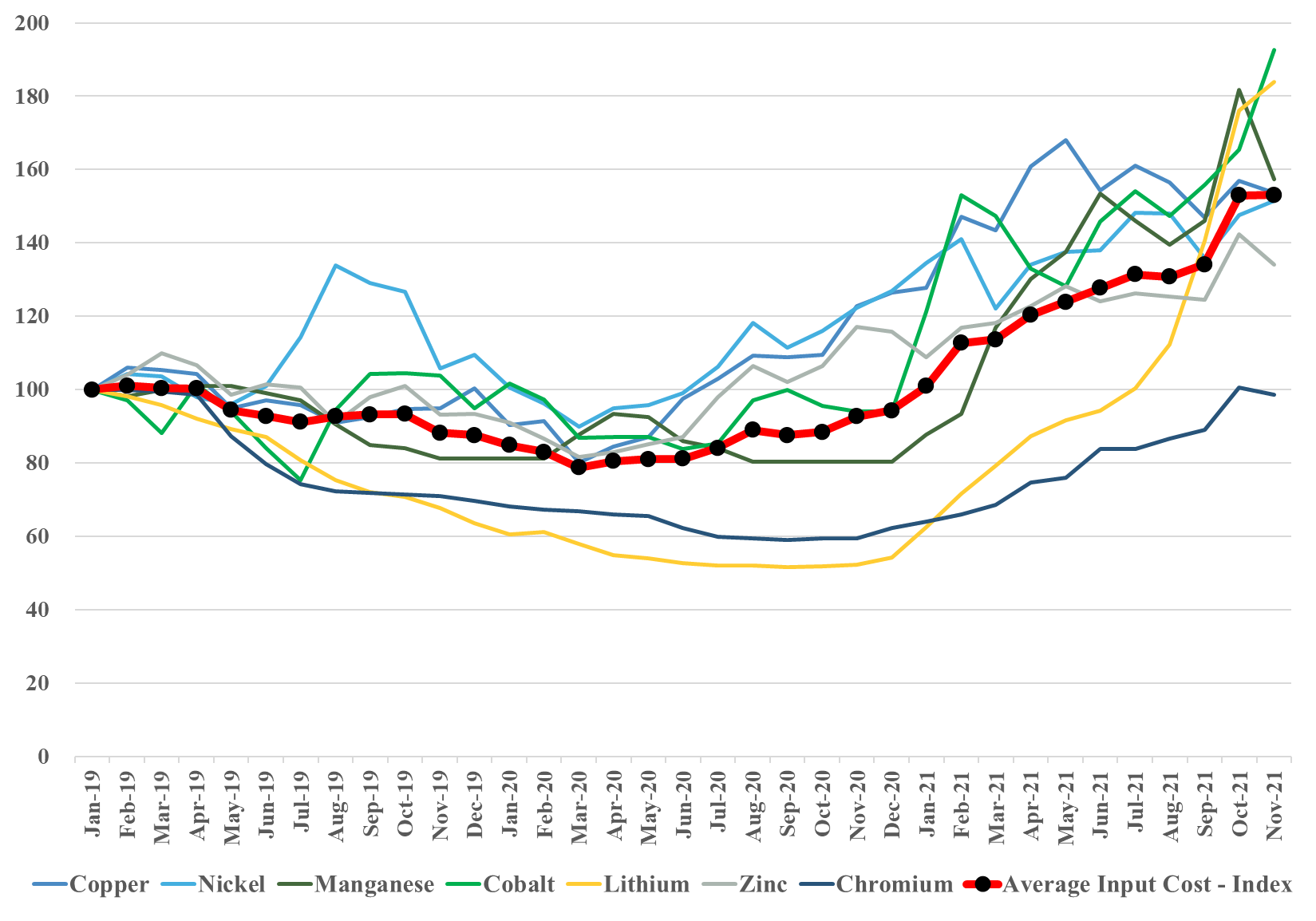

Continuing with our inflation theme this week, we show our renewables metals price index in the Exhibit below, which continues to climb and is now 50% higher than it was 2 years ago, with cobalt and lithium leading the charge at around 100% higher. These are critical components for EV and renewable power manufacture, and with 2022 forecasts for all suggesting much stronger growth, we do not see the materials supply/demand balances improving, suggesting that pricing will go higher. Energy shortages today, will only add more upward pressure to build more renewable capacity quickly and add even greater inflation risk to both components and the materials used to make them. We are concerned that, on the list below, only lithium is seeing significant capital thrown at increasing availability, suggesting that while lithium may peak in pricing, other metals could keep marching up. See our recent Daily, ESG Report, and upcoming Sunday Thematic for more.

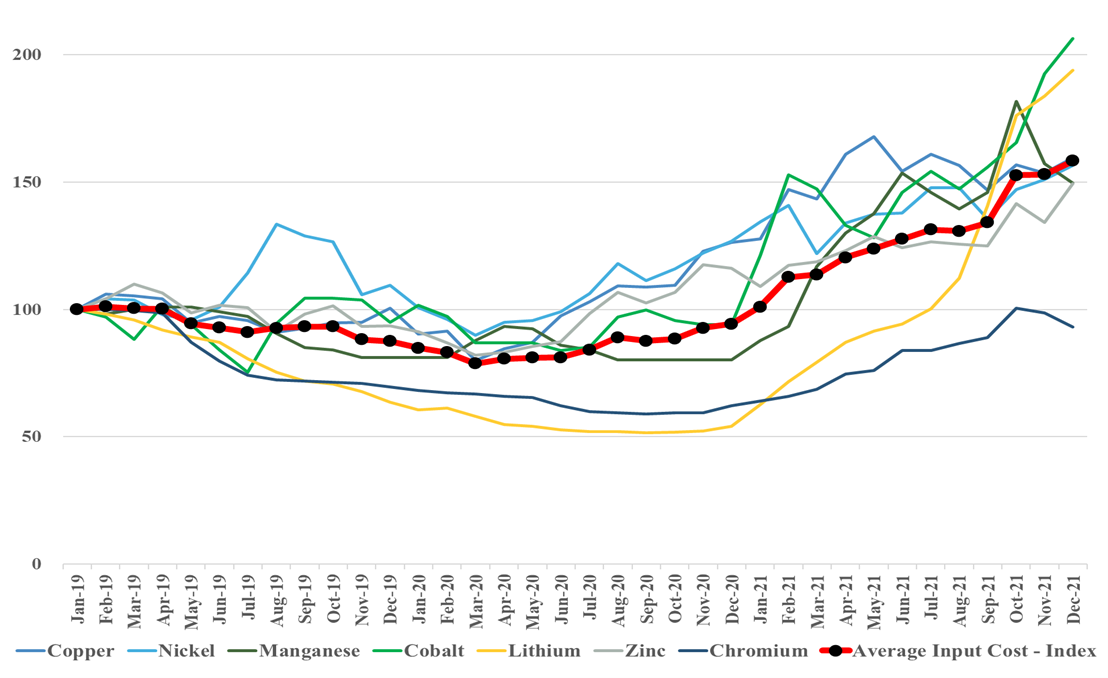

We focus today on raw material inflation and use the IEA analysis of materials demand (excluding steel and aluminum) in EVs and renewable power, creating a price index for the materials in question. This index is a straight average, but we will develop indices for specific sub-industries and include these in our next ESG and climate report. What is important is that the index below is up over 50% since the beginning of 2019 and this is before many of the EV plans and power plans move from planning to construction. We have highlighted inflation risk for more than a year now and remain very concerned that when many of the new auto plants start and many of the incremental renewable power facilities move from planning to equipment purchasing, we will see bottlenecks and faster price increases. See more in today's daily report.

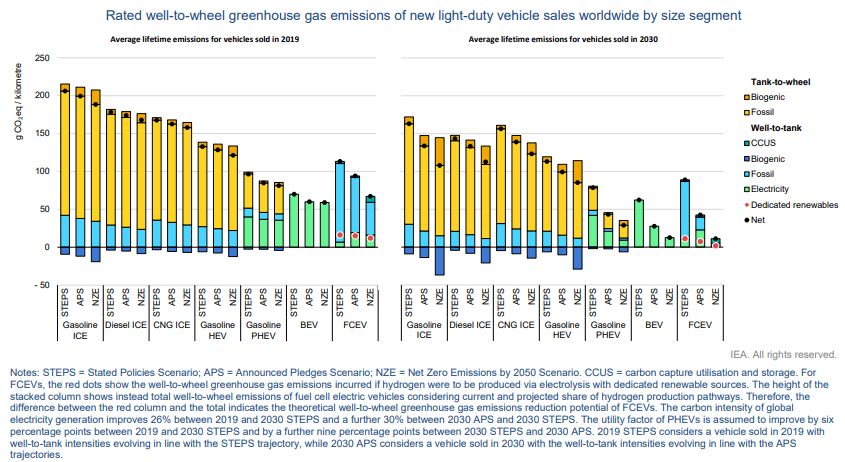

We highlight more from the IEA on the importance of EVs versus other vehicles to bring down “well to wheel” carbon footprints and the second (not unexpected) “kick in the pants” chart that shows the World woefully short in terms of its projected EV adoption rate. There are – probably expensive – hurdles to reaching the IEA net-zero goals with respect to EVs. The first is going to be the need to pay or tax consumers enough for them to give up a perfectly good ICE vehicle long before the end of its natural life.

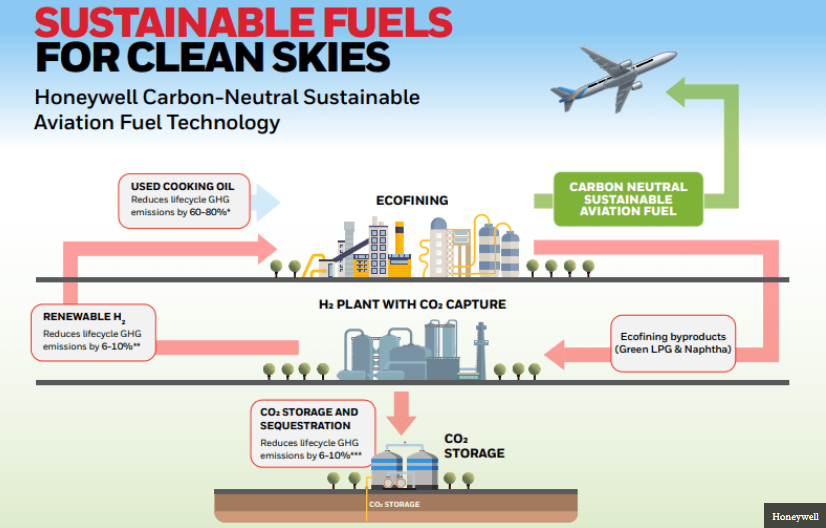

We have spent a lot of time in our ESG and Climate work talking about the huge impending challenge of producing enough sustainable aviation fuel to meet airlines desired needs for 2030 and beyond and we highlighted a Ryanair release yesterday that suggested that the company would struggle to meet its 12.5% goal by 2030. The Honeywell schematic in the exhibit below is one of many different processes that are being considered to meet both the demand for sustainable aviation fuel and renewable diesel and gasoline demand. With gasoline more likely to be replaced with increased numbers of EVs over time, we believe that the sustainable fuel focus will switch to aviation as the main priority, and we will need every technology that we can get to meet the volume needs. Waste oil and vegetable oil, with carbon capture around the refining process, is one route, fermentation-based processes are another, and waste to oil is a third, although we remain skeptical about the reliability and economics around a waste gasification-based approach.

The charts below both support our view that we will see continued inflation in renewable energy costs, rather than the deflation that is baked into all of the forward models. It is easy to forget that some of the early solar installations are coming to the end of their useful lives and are retiring – these are gaps that new solar will need to fill. Wind power has the same issue, as many of the original wind farms need equipment replaced and the introduction of recyclable wind turbine blades has been in recent manufacturers' announcements. When we see analysis of who is going to use which tranche of new renewable power for which new hydrogen project we see major gaps in the power demand analysis, in part related to power demand growth at the domestic consumer – because the more rapid introduction of EVs – and in part because or retirement of facilities and the need to replace them.