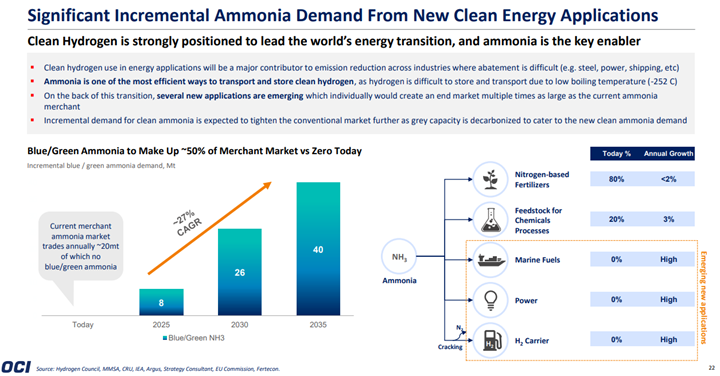

Despite all of the rhetoric about the need for green hydrogen, we see most of the large ammonia producers pursuing large blue projects – with Nutrien’s announcement yesterday coming on the heels of a CF new facility announcement and the CO2 capture project announced by LSB a couple of weeks ago. While there are some small (proof of concept) green projects in the works, they are very small, tiny when compared with the ammonia need, whether to replace lost material from Russia and Ukraine or whether to supply what could be substantial needs in Asia to co-fire coal plants, or as a shipping fuel, or as a carrier for hydrogen (see third chart below). The ammonia majors are not waiting around for “green” economics to improve as they see meaningful near-term demand that cannot wait for scale efficiencies of available power on the green side. Large-scale sources of cheap renewable power are hard to find, and where they may exist, there is competition from uses that may be able to pay more.

There is the potential for the ammonia thirst (please don’t drink it) to surpass opportunities to build cost-effective capacity for the medium term. Consequently, the shortages we see today could extend and become more severe. Co-firing coal-based power facilities in Asia is one of the more obvious ways to start decarbonizing a predominantly coal-based power region. The experiments in Japan, if successful, will drive a step-change in demand for blue or green ammonia, and this should drive much more new capacity than we have seen announced to date. The power-based demand comes on top of expected growth in fertilizer-driven demand and a possible rise as a shipping fuel. The issue for investors is that green ammonia at scale is economically challenging, especially with the recent shortfalls in renewable power generating plans and what now looks like rising power costs for a while. Blue ammonia is much easier to think about at scale, but we are still hamstrung by expensive carbon capture costs and a lack of incentives – either in terms of tax breaks or taxes or in terms of a customer willing to pay more, to get most ideas and plans past the “wouldn’t it be nice” phase. In the meantime, as indicated above, installed ammonia capacity is making abnormal returns.

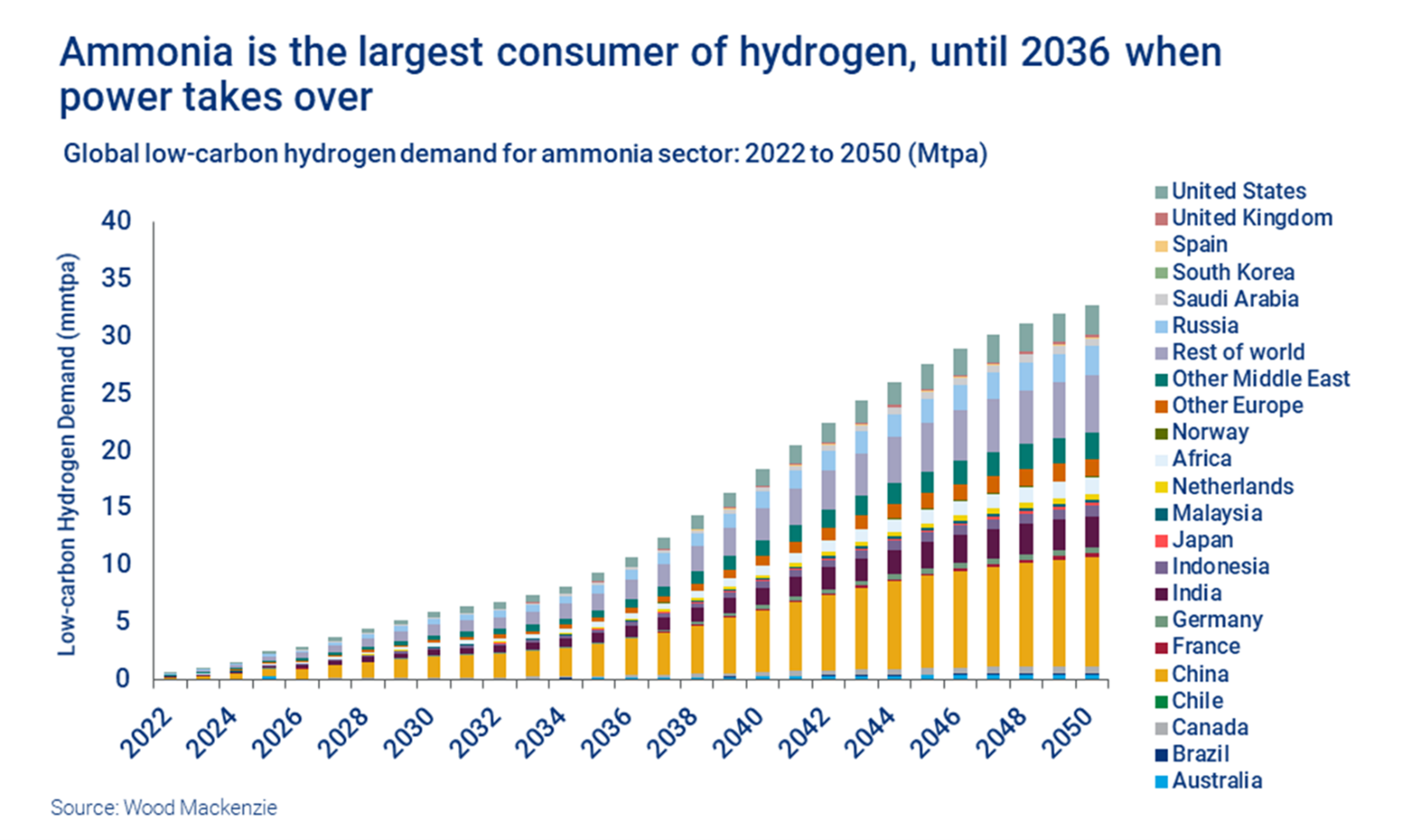

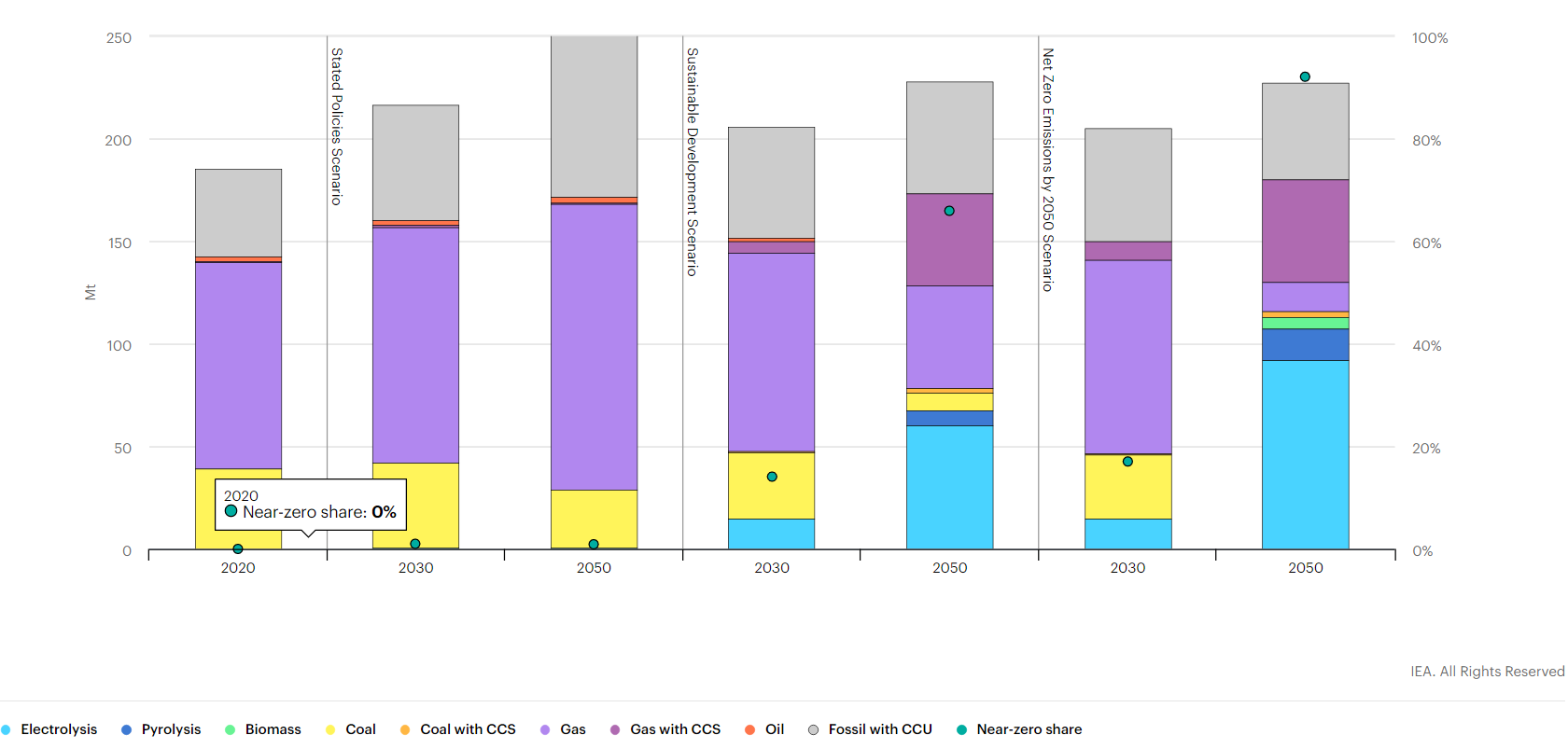

One of the concerns that the IPCC has in its report issued this week is that things are not happening fast enough and the Ammonia analysis in the chart below would support this view. Most of the capacity addition comes post-2030 in large part because project planners cannot see a way to enough cheap power to generate the green hydrogen needed until that time. In our view, since COP26 the transition part of the energy transition has been overwhelmed by advocates of green technology and renewable pathways without much thought about how practical they might be today. Those suggesting transition options are being given very little airtime and as a consequence, we see broad hostility towards anything that is not truly green, regardless of whether the costs or time frames make any real sense. If we do not embrace bold transitionary steps including the use of hydrocarbons with aggressive abatement targets we will not meet any of the shorter-term goals that the IPCC highlights and we are putting hope in renewable and technology development which may come up short. Related to this we see the LNG dilemma in Europe, with the current and medium-term needs very apparent, but a reluctance to sign up for longer-term supply because of an expectation that if all things renewable come to pass, the LNG might not be needed. The Europeans will need to make the longer-term commitment if they are to persuade the US and other potential exporters to build new export terminals.

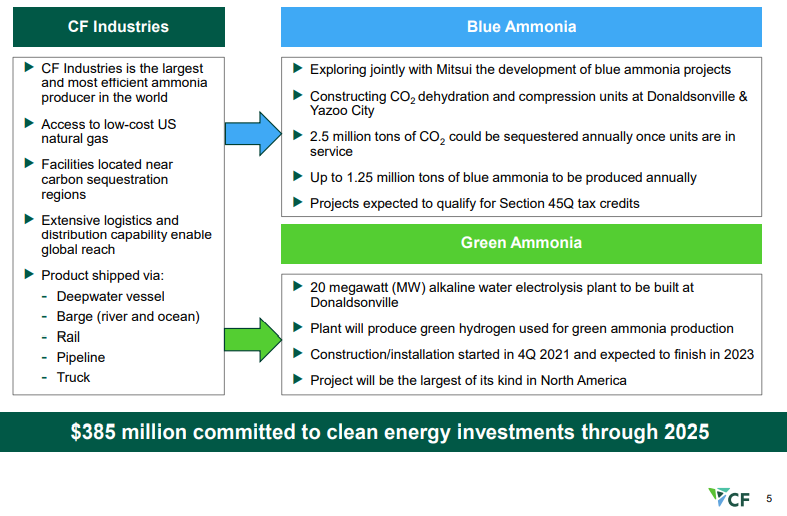

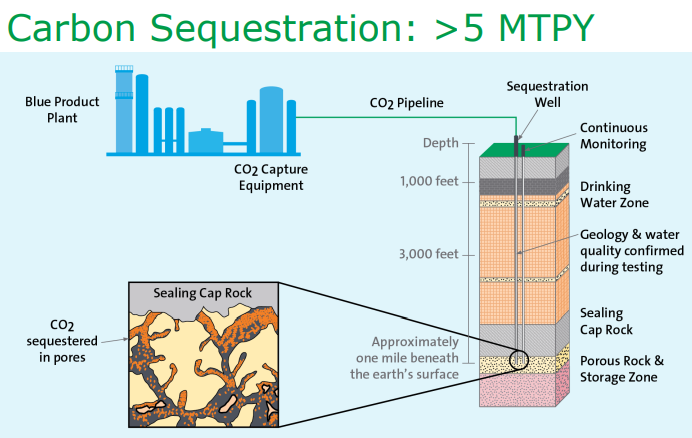

We continue to believe that the US has a cost advantage in CCS versus many of the other regions of the world and that when coupled with low natural gas prices the US should be able to take a lead in developing low carbon chemicals. CF is pushing the idea of both blue ammonia in the US as well as green ammonia, and while the company has yet to announce sequestration plans for the CO2 it is working to purify – see Exhibit - once dehydrated and compressed the incremental cost of storage should be low.

International natural gas prices are hitting new highs this week, both on an absolute basis and relative to the US - see both charts below. At the same time, we see new contracts being signed for US LNG to move to China and Europe, but mainly China. This is happening despite significant renewable power investments globally in 2021 and it would appear that many have underestimated energy demand growth in projections and policy. The other net effect of the supply/demand imbalance this winter and possibly through 2022 will be increased coal use in Europe and the US, with local governments unable to meet near-term climate goals, especially in Europe, but also in parts of Asia and, at the same time keep the people warm and the lights on. In our ESG and Climate piece tomorrow we will focus on one highly unpopular but likely very practical opportunity for coal as part of a planned energy transition program, and it is likely that, while climate goals may not need to change, some socially unpopular decisions around the use of fossil fuels will be needed to prevent even more socially unpopular inflation or absolute shortages.

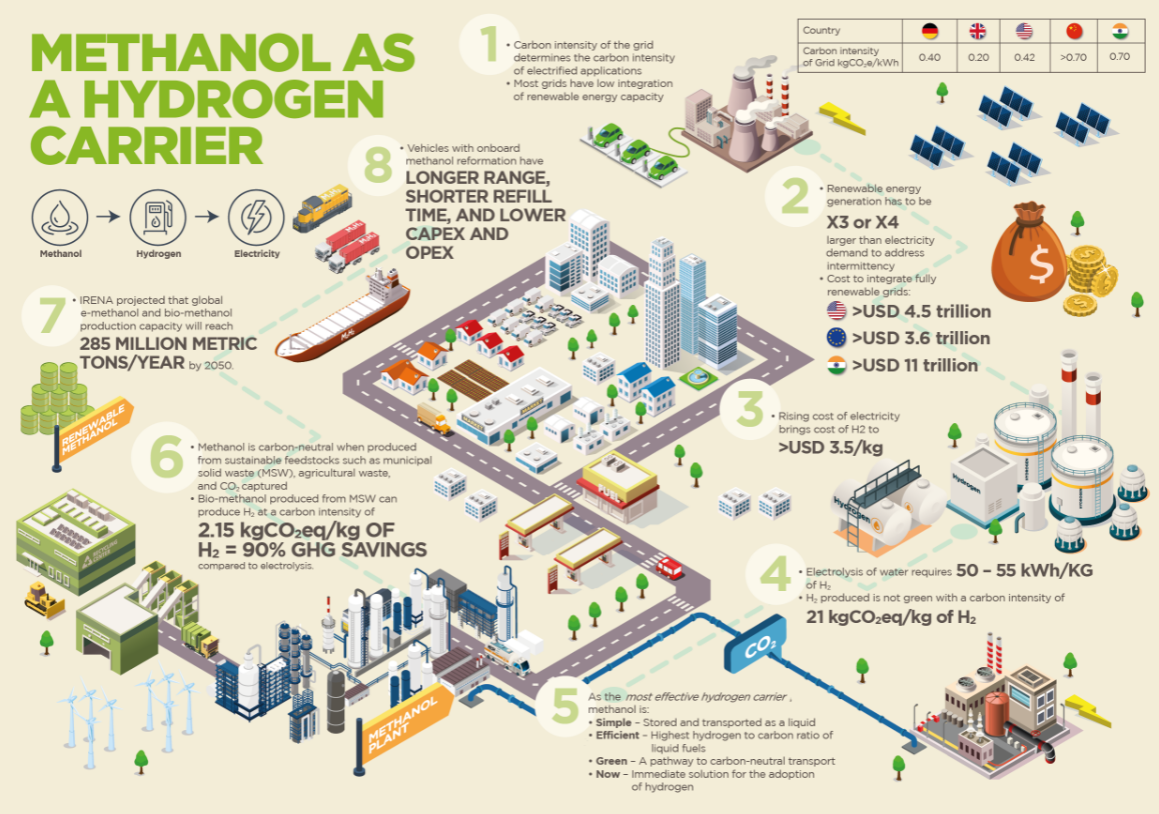

We are going to focus our Sunday Thematic this week (will be found here) on a couple of related topics: alternative technologies that only make sense when prices are high, and whether this has changed with ESG and climate pressure, and ESG solution fixation – “methanol is the only solution” – see infographic below – or it’s hydrogen or ammonia or batteries. Sticking with the theme that seems to have hit a chord with COP26 attendees and something that we discussed in a report around carbon capture several months ago – we cannot let a foolhardy quest for “perfect” get in the way of more economic “good enough” solutions. The emission issues are generally site and process specific and different solutions will be more practical and affordable for different processes and in different geographies – there is no “one size fits all” solution.

One question we would have concerning the IEA ammonia projections in the charts below is whether the absolute demand assumption for 2050 is too low. If Japan has success co-firing its coal-based facilities with ammonia over the next 6-7 years, we could see a step-change in ammonia demand. The chart likely reflects expectations in Japan, but we would expect other coal-heavy economies to follow Japan's lead. If this were the case, we would expect the share of hydrocarbon-based ammonia to rise with accompanying CCS.

In our ESG piece yesterday we talked about the competitive edge that Canada now has with respect to both natural gas (because of lower prices versus the US) and CCS, both because of relatively low costs but also because of the clear value on carbon. Yet today we see an announcement in the US!

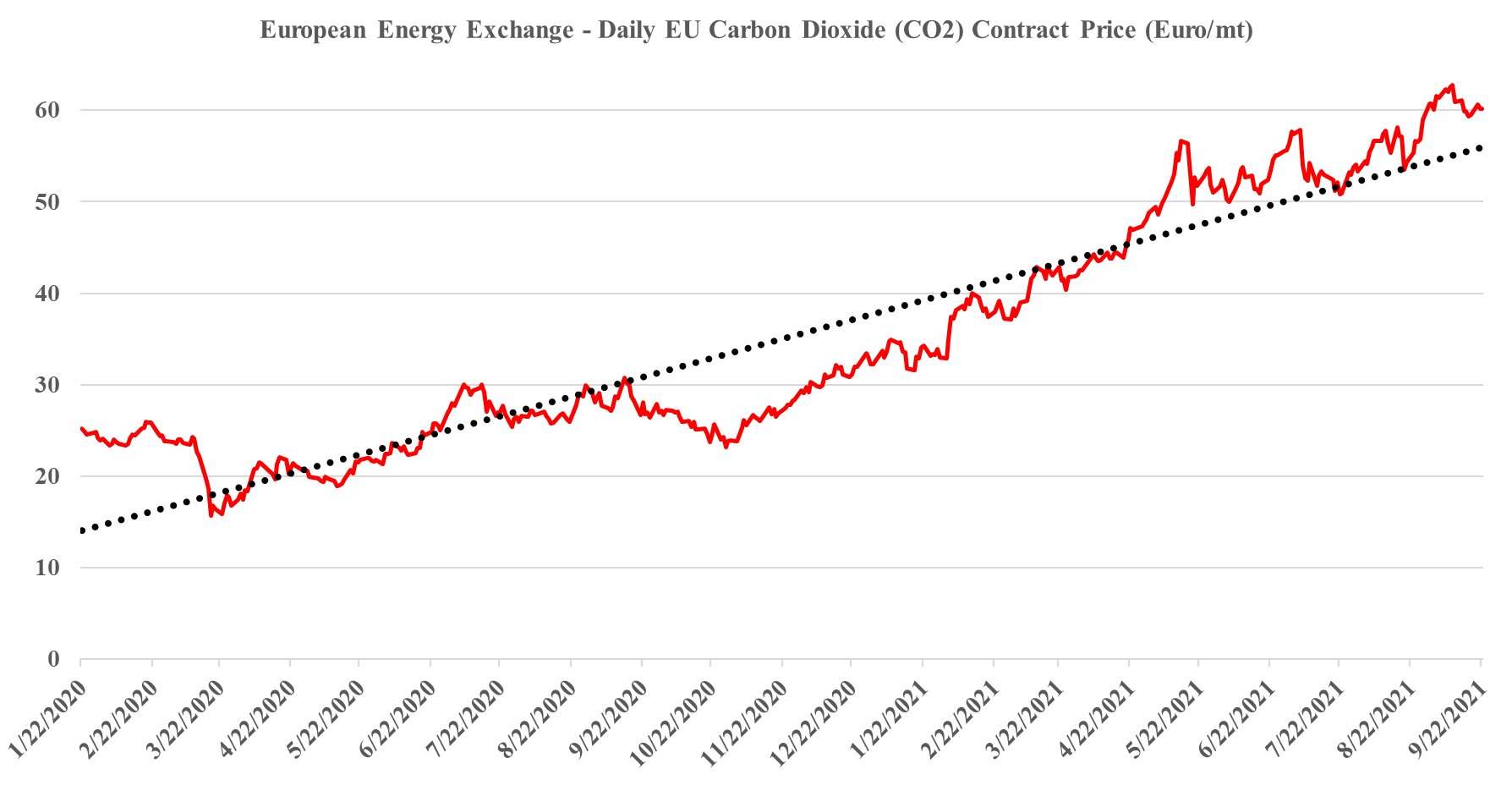

It is worth a short explanation of what is going on with European CO2, given the mixed signals of shortages in headlines today and then the slight weakness in pricing shown in the image below. These are two very different markets, with the food, beverage, medical and nuclear industries looking for pure streams of CO2 rather than the contaminated streams that make up the bulk of emissions. Historically, the food and beverage industry looked to fermentation – so alcohol production – as its source of a pure CO2 stream, but as demand grew, the next best place became ammonia production, which also has a pure CO2 stream as a by-product. Most ammonia is further converted into urea, which is a consumer of CO2 and there is not enough CO2 produced in a natural gas-based ammonia plant to convert all of the ammonia to urea. You sometimes see urea facilities also selling ammonia, but more frequently they take the carbon monoxide by-product of the syngas reaction and convert that to CO2. The result is enough CO2 to convert all of the ammonia to Urea and surplus CO2 to sell. Because of this more dominant supply of food and beverage grade CO2, and shutdowns caused in this case by runaway natural gas prices, have an immediate impact on the industries that rely on the CO2.