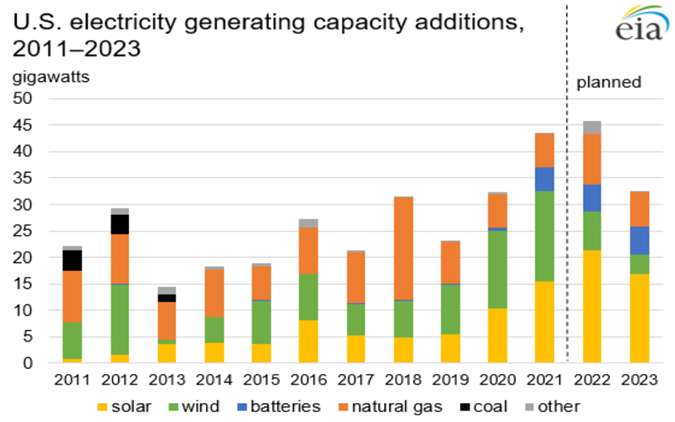

The renewable power space is heading for a very bad year in the US and Europe, as supply chain issues and raw material inflation will impact not only the amount of business that gets completed, but also the margin on that business. The trade issues between the US and China on solar panels have essentially brought the industry to a halt for the moment and suggests that all forecasts of the growth in renewable power contributions in the US in 2022 are too high, and consequently demand estimates for natural gas and coal for power generation are too low – see out comments in the energy section of today's daily report. The EIA forecast below likely fails to take into account the current woes and if governments, at the federal and the state levels act on the information in the chart they may be unprepared for some power shortages later in the year. Overestimation of the rate of renewable power installation as well as its operating rate is responsible for many of the current power shortages that we see in most regions.

We discussed the woes of the wind power industry at length in a dedicated ESG and Climate piece last week, and the Vestas results below play into the same theme. The company is cutting guidance again for 2022, which is already much lower than estimates would have suggested 6 months ago. While Siemens Gamesa has the added headache of a mismanaged platform change, all of the issues raised by Vestas are shared industry wide, delayed installations because of supply chain issues and material shortages, as well as significant cost inflation. In tomorrow’s ESG and Climate report we discuss some of the increases in European PPAs in 1Q 2022, reversing a multi-year trend of lower installed costs of power. This reversal will likely impact plans for 2022 and 2023, especially for those banking on lower power costs to justify many of the announced hydrogen ventures – particularly in Europe. Those who press ahead despite higher power costs and higher construction costs in general, may stretch both balance sheets and borrowing capacity.

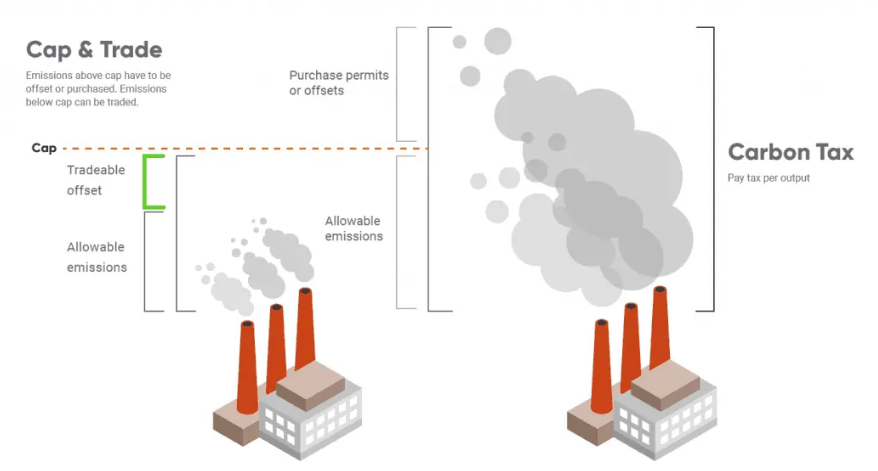

There was a very strong focus at the WPC on the need for carbon pricing in the US to facilitate investment decisions around many initiatives focused on carbon abatement. The consensus was very much that a carbon price – so a cap and trade system like they have in Europe – was the best mechanism, and far more likely to drive action and limit inflation than a carbon tax. This is something that we broadly agree with but the US is a bit late to the game and the right caps need to be set so that CO2 prices don’t languish at very low levels for years, as they did in Europe. Jim Fitterling of Dow was somewhat provocative in his comments around nuclear power, but we see this as part of a broader initiative aimed at getting a serious dialogue moving around how we make the practical steps needed to drive carbon lower. Nuclear power provides stable baseload and is carbon-free – a small modular nuclear reactor could generate enough steam and enough power to drive the decarbonization of major chemical complexes – one investment for example could transform one of the larger Dow sites. If we are going to get to net-zero targets without nuclear, we need much more progressive policies – especially around carbon pricing – which is likely the direction that Dow would like to take the discussion.

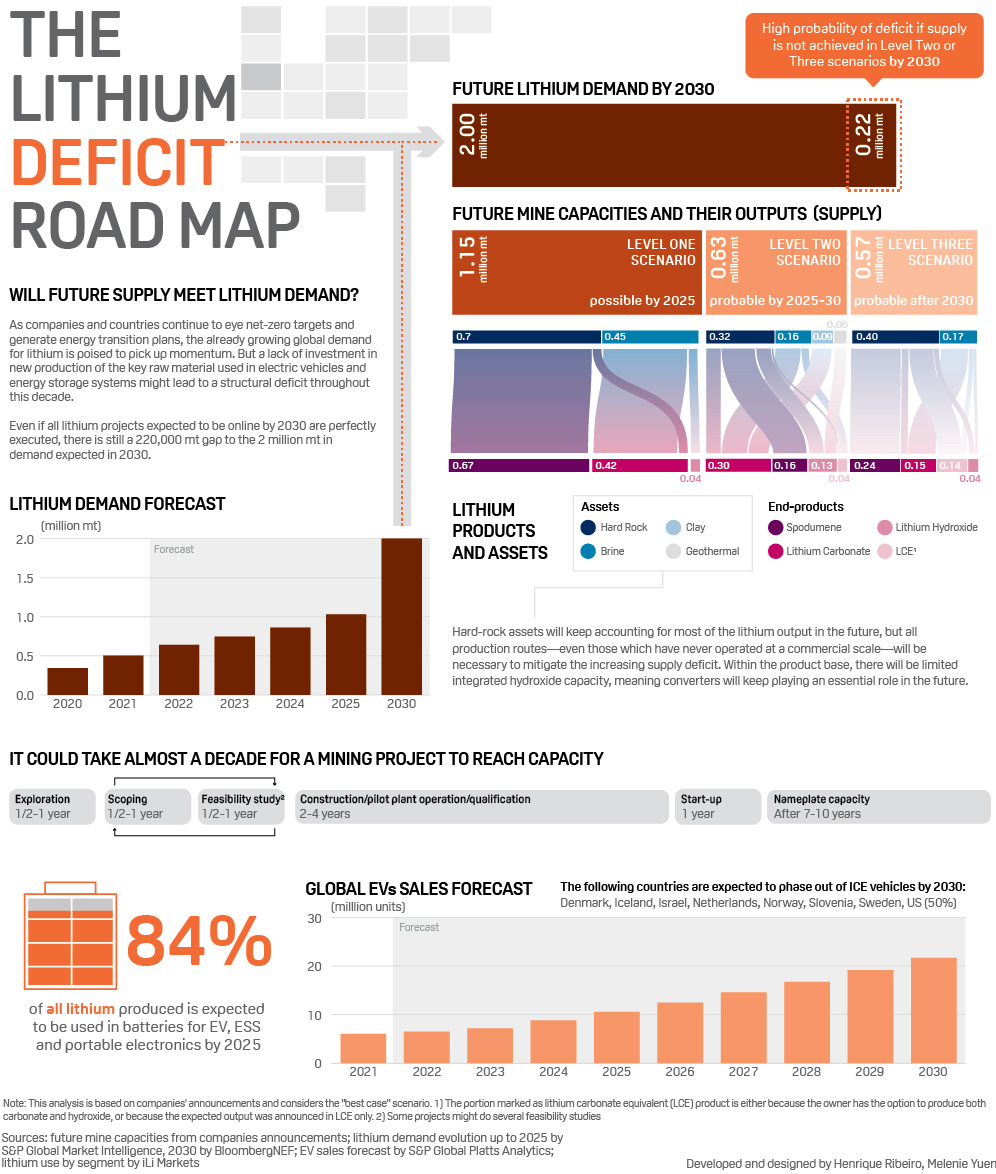

In our EGS and Climate report yesterday - Lithium – A “Special” Commodity For Now – Adding To Inflation – we talked about the current spike in lithium pricing but at the same time talked about the likelihood of lithium moving from famine to feast over the next few years and the potential for significant price volatility. This is a product for which demand growth is very high but supply growth is also very high. There are also some very divergent views of supply-demand and we highlighted a view that was bearish for lithium in yesterday's piece and show a bullish one below. The automakers and battery makers want to promote the idea that lithium will remain in short supply, as they need to encourage as much investment in lithium production as possible. While the incumbents want to keep pace with growing customer demand, they would like to see fewer new plays and are naturally conflicted in what message they want to give. We foresee supply and demand falling in and out of balance several times over the next 10+ years.

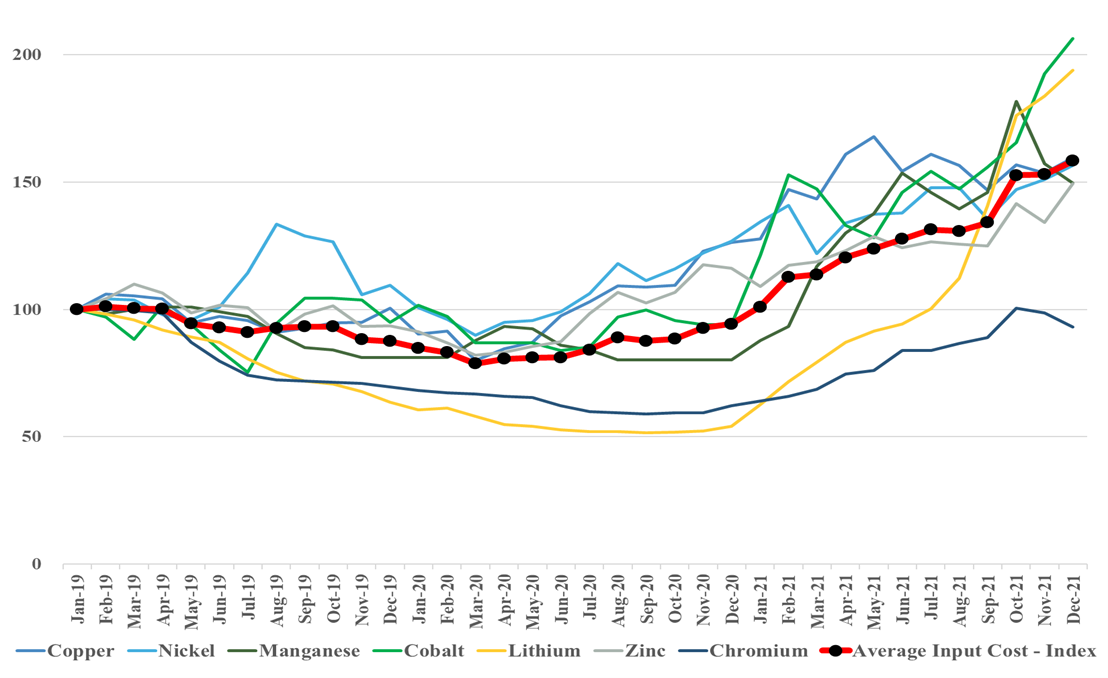

Continuing with our inflation theme this week, we show our renewables metals price index in the Exhibit below, which continues to climb and is now 50% higher than it was 2 years ago, with cobalt and lithium leading the charge at around 100% higher. These are critical components for EV and renewable power manufacture, and with 2022 forecasts for all suggesting much stronger growth, we do not see the materials supply/demand balances improving, suggesting that pricing will go higher. Energy shortages today, will only add more upward pressure to build more renewable capacity quickly and add even greater inflation risk to both components and the materials used to make them. We are concerned that, on the list below, only lithium is seeing significant capital thrown at increasing availability, suggesting that while lithium may peak in pricing, other metals could keep marching up. See our recent Daily, ESG Report, and upcoming Sunday Thematic for more.

In our ESG and Climate report yesterday we highlighted inflation as one of the most significant risks for 2022 and the estimates in the exhibits below do not leave us any less concerned. The US has struggled to meet solar installation plans for 2021, falling short of early-year estimates because of limited equipment availability and higher equipment prices. While some of this has been the result of the supply chain challenges of 2021, some shortages have also been the result of very strong global demand. The idea that we can increase solar installations in 2022 without creating more supply issues (and more inflation) should be questioned, especially in light of planned additions in China, which will consume an increasing share of Chinese solar modules.

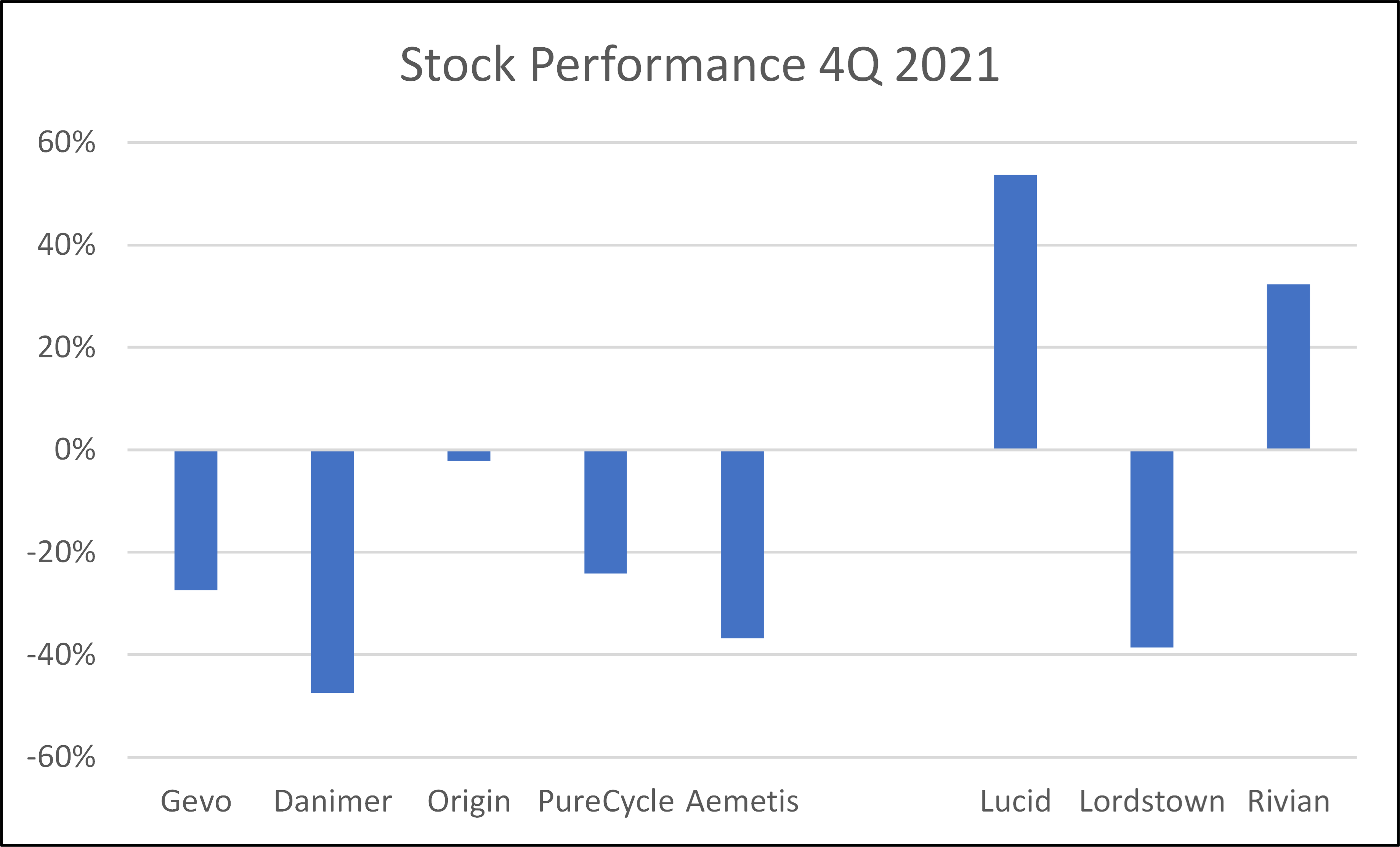

Life in 2022 is likely to be tougher for the new companies in materials and fuels, as all of them need capital to support projects that now look riskier from a cost inflation perspective and the market has moved to reflect that risk – Exhibit below. For every company below, the 2022 story was supposed to be capital spending to create commercial-scale production. The poor stock performance for many has tracked rising raw material prices – especially steel – as well as concerns around supply chain-driven delays and labor shortages. Few have the financial capacity to absorb significant cost overruns and/or construction delays. Danimer Scientific has done a recent capital raise and its impact created roughly half of the downside shown below – Danimer still likely needs more capital, but with more cash on the balance sheet may be able to get the rest through loans. Gevo, which in our view has the more impressive portfolio of potential offtake partners at this point likely plans to borrow at the facility level, and the stock weakness is likely a combination of inflation fears, the declining LCFS value, and the wait for the company to announce that it has a completed FEED study for the first plant and has reached FID. We would struggle to invest in any of these names today given the step-change in company development that each needs to make in 2022, and we would need more offtake agreements and process/construction guarantees than any company can likely get today, and if they could, they might not want to make some agreements public. See more in today's ESG and Climate report

International natural gas prices are hitting new highs this week, both on an absolute basis and relative to the US - see both charts below. At the same time, we see new contracts being signed for US LNG to move to China and Europe, but mainly China. This is happening despite significant renewable power investments globally in 2021 and it would appear that many have underestimated energy demand growth in projections and policy. The other net effect of the supply/demand imbalance this winter and possibly through 2022 will be increased coal use in Europe and the US, with local governments unable to meet near-term climate goals, especially in Europe, but also in parts of Asia and, at the same time keep the people warm and the lights on. In our ESG and Climate piece tomorrow we will focus on one highly unpopular but likely very practical opportunity for coal as part of a planned energy transition program, and it is likely that, while climate goals may not need to change, some socially unpopular decisions around the use of fossil fuels will be needed to prevent even more socially unpopular inflation or absolute shortages.

Much of the core focus of both our chemical industry and ESG and Climate research recently has been on inflation and materials shortages; we would point you to: Inaction, Caused By Inflation Fears, Is Driving More Inflation! and Coming Up Short: Materials Availability To Limit Climate Progress. This linked article suggests that, as we have predicted, cost and availability pressures are taking a toll on solar installation plans for 2022 in the US. While the inflation piece is real and the product shortages highlight some of the capacity constraints for materials and panels, the broader conclusions that can be drawn from the headline are more concerning. These shortages (and higher prices) are coming well before we see any step change in attempts to increase renewable power installations associated with all of the green hydrogen projects that have been announced over the last 6-9 months. All of these investments are relying on the deflationary trends continuing, especially for onshore wind and solar.

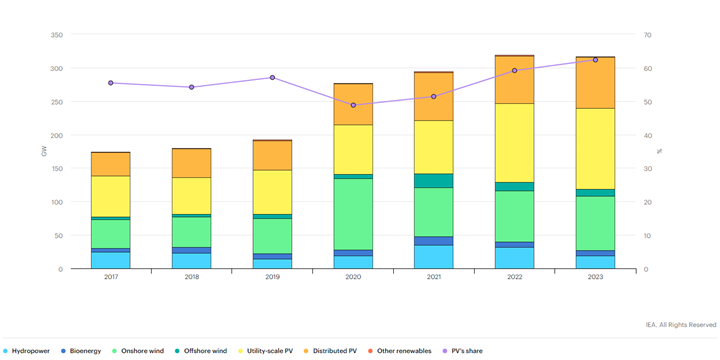

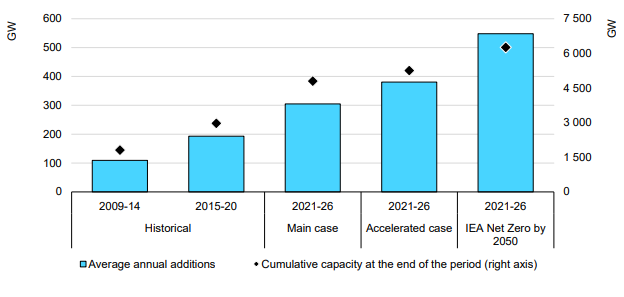

The core message of the IEA analysis published today is around how renewable power rates of investment remain far too low and need to more than double immediately to meet net-zero goals – see below. This analysis is very supportive of our renewable power inflation thesis, as none of the renewable power component manufacturers can double production either cheaply or quickly, and none of their suppliers has that much spare materials capacity. On the solar front, we may have the additional problem of regional production concentration. China has the largest share of capacity for solar module capacity and now has much more aggressive plans for solar power domestically. We could see China-based components stay in China, exaggerating shortages outside China. The IEA has an accompanying report today on the possible impact of commodity pricing on solar and wind pricing and it is also linked here – these reports were published this morning and we will cover them in more detail in next week's ESG and Climate report. More on this in today’s ESG and Climate report.