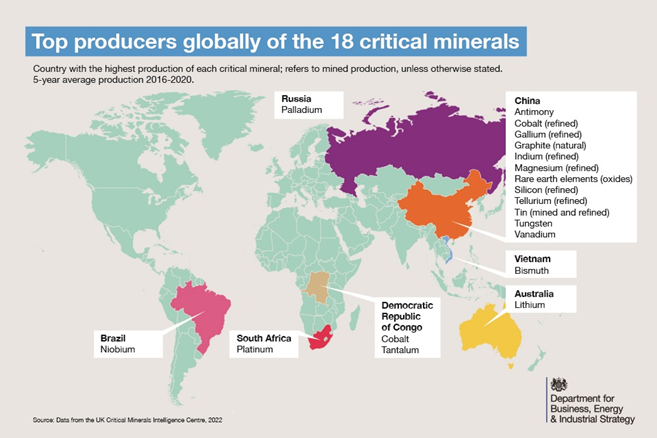

We are seeing more focus on supply chains as they relate to the energy transition. Some European countries are realizing what we have noted in prior research - EU Energy Policy: Swapping A Bad Supplier For Something Worse? - switching to an aggressive focus on renewable energy may reduce your energy exposure to Russia but it currently doubles down on your exposure to China. It is very easy to look at the scale of the problem – the share that China has in critical metals, as shown below – the share that China has of solar modules – etc., and conclude that it is too hard, especially in Europe where you will find an environmental lobby trying to stop you doing anything industrial. But the net effect is severe reliance on China. One advantage that the UK now has with its exit from the EU is more industrial freedom and the country could benefit from the right industrial policies that would attract broader energy transition investment. In our ESG and Climate report this week we talked about the U.S. desire to “friend-shore” rather than re-shore because of local investment challenges in the U.S. as a consequence of some of the political issues. The UK could benefit from becoming an industrial partner with the U.S. for some critical materials.

We share views from Christopher Sheeron - The first-ever guest author for C-MACC's most recent ESG and Climate report titled "Does DC Understand Economics – Energy Proposals Suggest No".

Main Points from this report include:

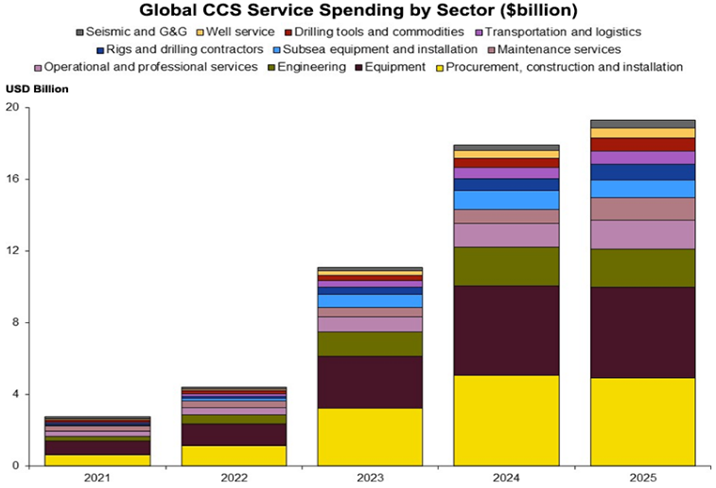

The CCS spending chart below is quite detailed, but shows the limited amount of spending in 2021 and 2022 and may underestimate the amount of seismic spending needed, especially in the US, as companies prepare permit applications. We do not expect to see much spending in the US before mid-decade beyond permit applications. However, as we discuss in today’s ESG and Climate report, should the API proposed carbon tax, or something similar, be additive to the 45Q tax credit, we could see a step-change in CCS when/if the tax is approved. The tax on its own is likely not enough to drive decarbonizing investment, but when added to 45Q it could be a specific trigger for CCS investment, and we could see a step-change in the second half of the decade. This might involve large-scale blue hydrogen production, especially on the Gulf Coast to decarbonize the refining and chemical industries.

In our ESG and Climate report tomorrow, we will focus on SAF from a carbon intensity perspective. The Colonial pipeline initiative was inevitable given the demand for jet fuel at the East Coast airports. Still, we would not expect much volume to move in the near term for several reasons. First, there is not that much to move, and second, California can still pay more because of the LCFS credit. The Biden administration is planning to introduce a broad SAF credit which would help encourage use outside California, but this would also need to stimulate production as the volumes are still small and much smaller than the airlines would want – even the projection of volumes by bodies like the IEA fall well short of potential airline demand by 2030 and 2040. This is an investable theme, in our view, and we will discuss it in more detail tomorrow.

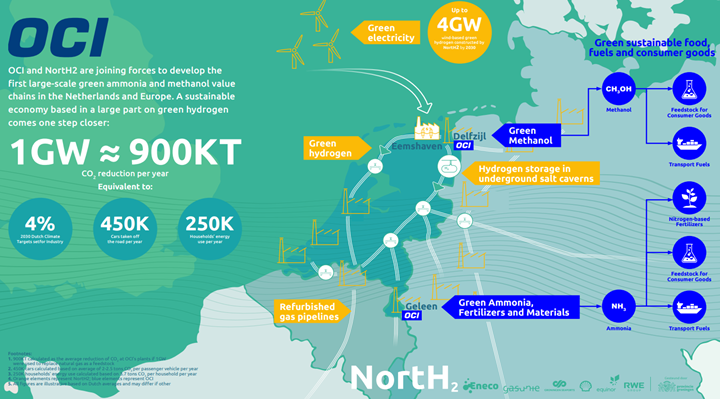

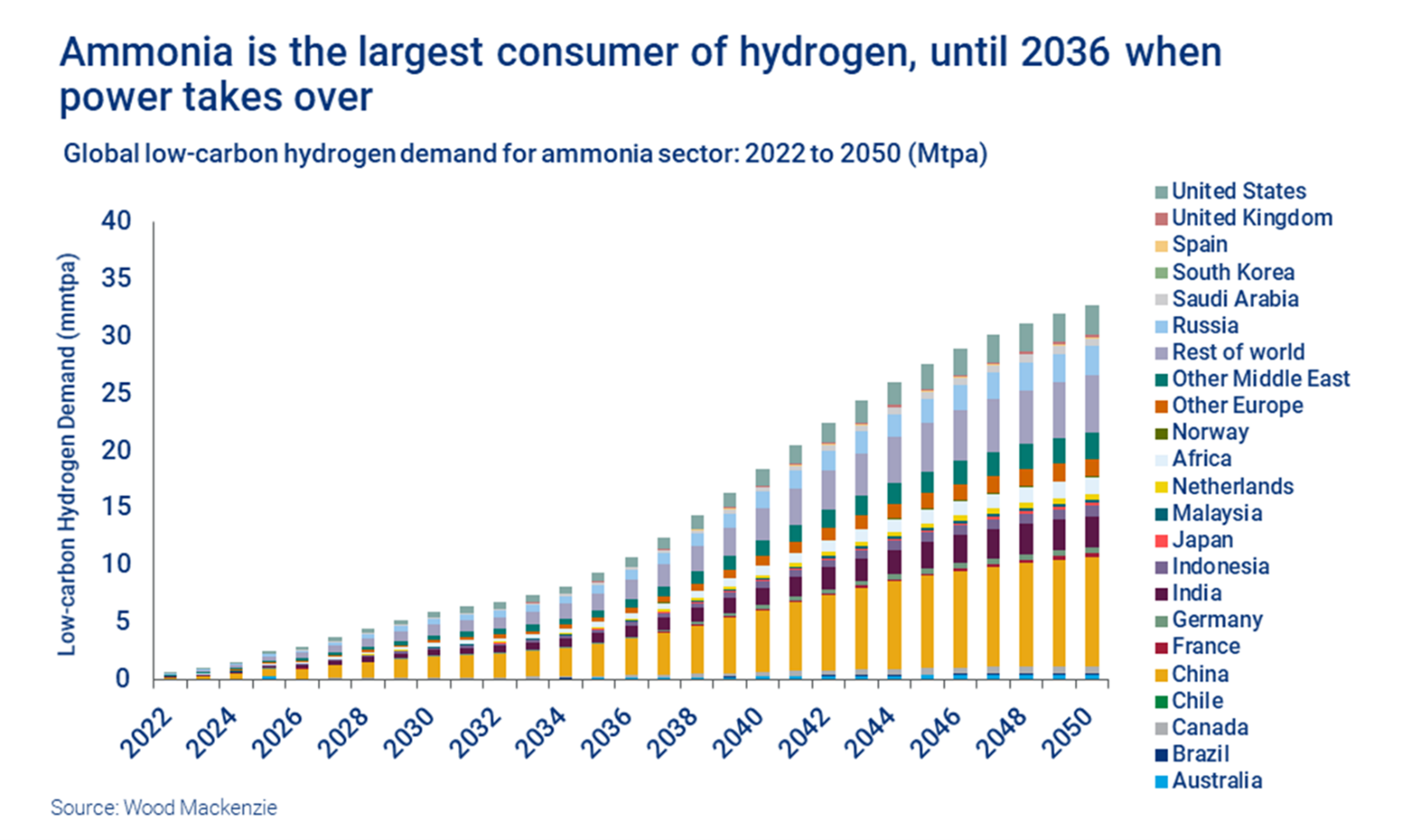

The two charts below today are interesting bedfellows as while one talks about yet more, likely impractical, hydrogen ambitions, the other talks about a possible solution.

One of the concerns that the IPCC has in its report issued this week is that things are not happening fast enough and the Ammonia analysis in the chart below would support this view. Most of the capacity addition comes post-2030 in large part because project planners cannot see a way to enough cheap power to generate the green hydrogen needed until that time. In our view, since COP26 the transition part of the energy transition has been overwhelmed by advocates of green technology and renewable pathways without much thought about how practical they might be today. Those suggesting transition options are being given very little airtime and as a consequence, we see broad hostility towards anything that is not truly green, regardless of whether the costs or time frames make any real sense. If we do not embrace bold transitionary steps including the use of hydrocarbons with aggressive abatement targets we will not meet any of the shorter-term goals that the IPCC highlights and we are putting hope in renewable and technology development which may come up short. Related to this we see the LNG dilemma in Europe, with the current and medium-term needs very apparent, but a reluctance to sign up for longer-term supply because of an expectation that if all things renewable come to pass, the LNG might not be needed. The Europeans will need to make the longer-term commitment if they are to persuade the US and other potential exporters to build new export terminals.

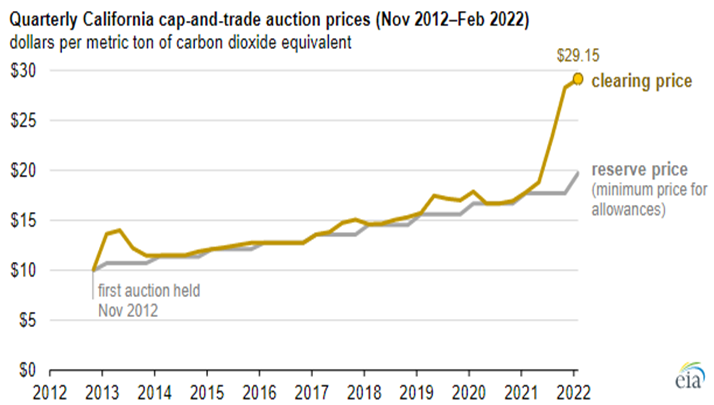

We have written extensively about carbon prices over the last two years and followers of our dedicated ESG and Climate service will know that our expectation is for all CO2 markets to see prices rise to levels that justify large investments to avoid CO2 production or sequester it. We see that price closer to $100 per ton than the $50 per ton that 45Q will rise to by 2026. The California price shown below has much more upside as credits demand rises. Many of the net-zero pledges made by manufacturers and energy producers today cannot be achieved without buying some sort of credit and we expect demand to rise relative to supply through the balance of the decade and possibly quite quickly.

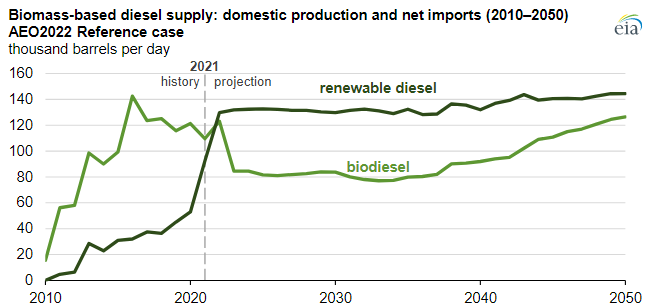

The EIA renewable diesel projections are based on a couple of things – who plans to make it and who will pay for it. All eyes are focused on the California market today as that is where the incentive lies – through the LCFS credit – and production plans plateau associated with that opportunity. As other states in the US adopt similar programs – which seems likely – we would expect to see production plans increase and the EIA will likely adapt its market view model and the chart will change. Note the dominance of renewable diesel over time, and this is where we would expect all future growth to occur. The plug-and-play nature of renewable diesel makes it a far more attractive option for refiners assuming the cost works. See more in today's daily report.

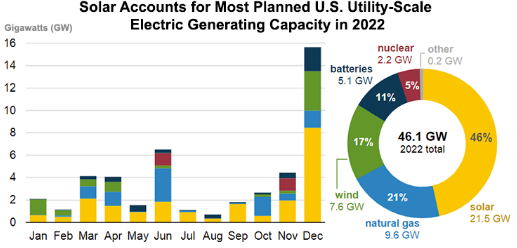

The back-end loading of the power projects for the US for 2022, as shown in the chart below leaves us somewhat skeptical concerning how much will come online this year. Supply chain problems and materials costs and availability are causing all sorts of problems with renewable power projects and installed capacity expectations for 2021 were too ambitious. We believe that companies are pushing projected start-ups later in the year to give them more of a chance of completion, but this creates the risk that they slip into 2023 or beyond. The most significant issue here is that as these plans get delayed, natural gas demand goes up, as one of the swing suppliers. This is fine as long as the US natural gas industry and shale oil industry is investing so that gas availability rises. Otherwise, we could see gas prices spike in the US next winter and another year where we use more coal than we expected. For more see this week's ESG and Climate report.

The annual review of World energy from bp shows a stark reversal of the company’s position only a short while ago. When the pandemic hit, bp went on record suggesting that we may have seen peak oil demand in 2019. It was an interesting theory and one that we discussed at the time, but it underestimated the impact that aggressive COVID-related stimulus would have on consumers globally and we suspect that bp, like many others, overestimated the rate at which renewables could be added. Now the company is exploring a very different scenario, one in which the current momentum in the energy market continues and the rate of renewable additions slows, either because of more limited capital or because of material constraints – or a combination of both.