As we see these large green hydrogen project announcements – mostly based on solar power, but some also on wind, we still wonder if anyone is totaling the accompanying demand for solar panel modules and wind turbines to check whether there will be enough capacity to manufacture during the relevant timeframe. Right now we are seeing preliminary announcements, and our concern is that as these move from the drawing board to FID, the pull on power generation components will overwhelm the capacity to manufacture and the capacity of the materials required as inputs. In the same way that we are seeing power prices and natural gas prices spike because of a supply/demand imbalance, we see a risk that projects such as the one (linked here) for Namibia end up in trouble as, by the time they are ready to build, the capital costs have risen dramatically.

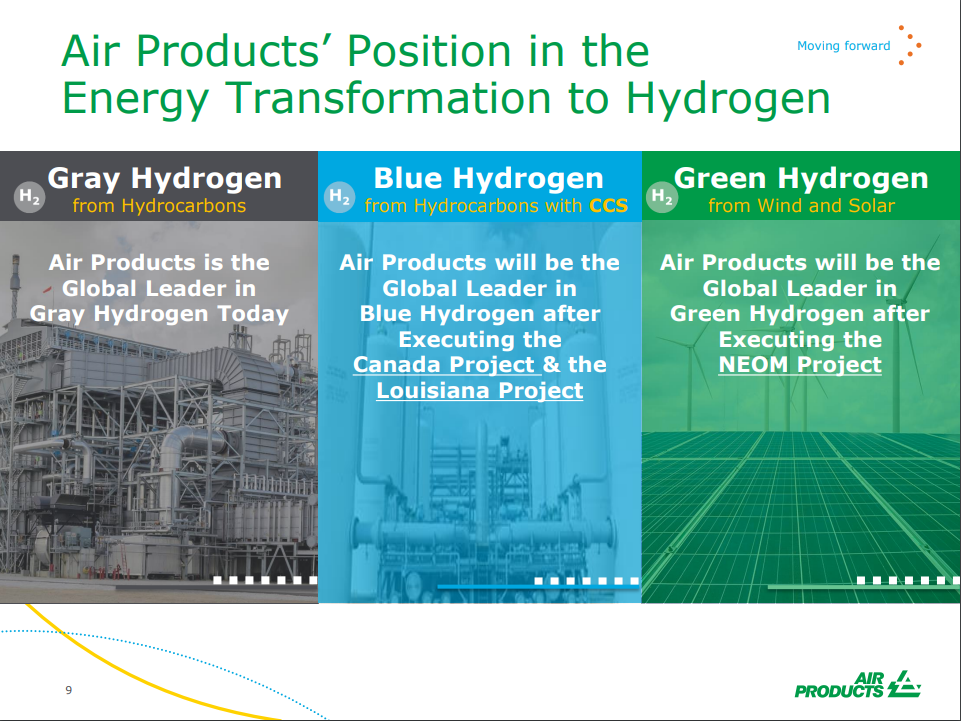

The discussion around carbon pricing and hydrogen (see link) is one we have covered in the past and we agree that there could be significant investment in CCS around existing hydrogen facilities with the right carbon price. However, a more interesting driver could be customer willingness to pay more for the blue hydrogen and not just for ammonia heading to Japan. Many hydrogen/syngas applications target products that have end-users increasingly more interested in a lower carbon footprint in what would be their Scope 2 bucket. Air Products will be an interesting test case in the US, as potential customers come out of the woodwork, especially in chemicals, with a desire to bid the hydrogen away from others. How much customers want a lower carbon input will likely drive how fast Air Products moves and whether the project is upsized. As shown in their quarterly call yesterday, Air Products plans to be a leader in blue and green hydrogen.

Source: Air Products, 2021