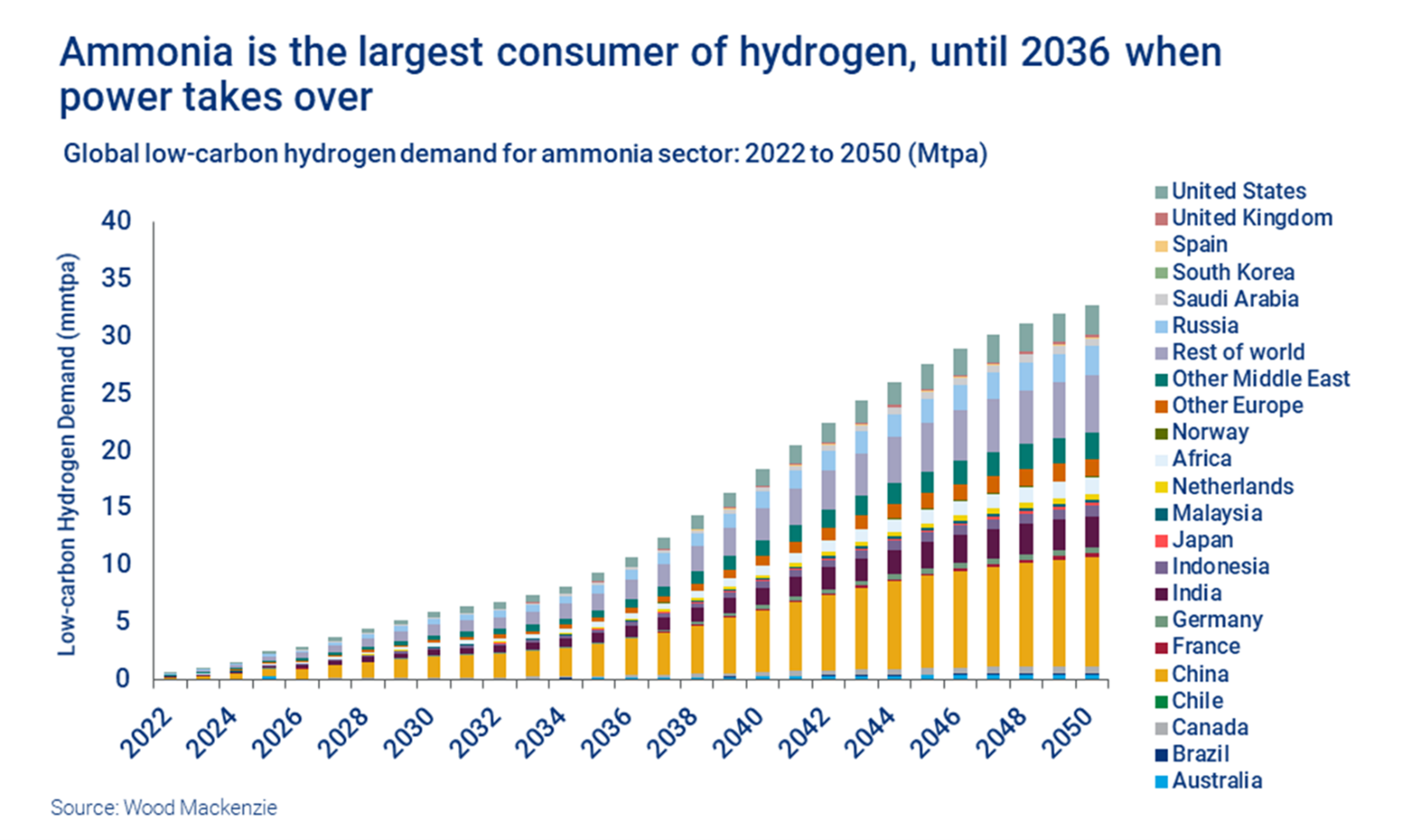

Despite all of the rhetoric about the need for green hydrogen, we see most of the large ammonia producers pursuing large blue projects – with Nutrien’s announcement yesterday coming on the heels of a CF new facility announcement and the CO2 capture project announced by LSB a couple of weeks ago. While there are some small (proof of concept) green projects in the works, they are very small, tiny when compared with the ammonia need, whether to replace lost material from Russia and Ukraine or whether to supply what could be substantial needs in Asia to co-fire coal plants, or as a shipping fuel, or as a carrier for hydrogen (see third chart below). The ammonia majors are not waiting around for “green” economics to improve as they see meaningful near-term demand that cannot wait for scale efficiencies of available power on the green side. Large-scale sources of cheap renewable power are hard to find, and where they may exist, there is competition from uses that may be able to pay more.

We discussed the woes of the wind power industry at length in a dedicated ESG and Climate piece last week, and the Vestas results below play into the same theme. The company is cutting guidance again for 2022, which is already much lower than estimates would have suggested 6 months ago. While Siemens Gamesa has the added headache of a mismanaged platform change, all of the issues raised by Vestas are shared industry wide, delayed installations because of supply chain issues and material shortages, as well as significant cost inflation. In tomorrow’s ESG and Climate report we discuss some of the increases in European PPAs in 1Q 2022, reversing a multi-year trend of lower installed costs of power. This reversal will likely impact plans for 2022 and 2023, especially for those banking on lower power costs to justify many of the announced hydrogen ventures – particularly in Europe. Those who press ahead despite higher power costs and higher construction costs in general, may stretch both balance sheets and borrowing capacity.

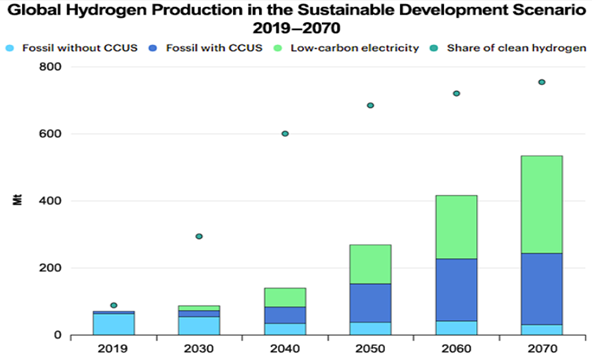

Anyone who read our ESG and Climate reports of the last two weeks will know that we do not believe in the hydrogen projections below as we see renewable power as a potentially scarce resource. Furthermore and also covered yesterday, should the API be successful with its carbon tax proposal in the US and should this be additive to the 45Q incentive for CCS, we could see an explosion of blue hydrogen investments in the US, especially on the Gulf Coast.

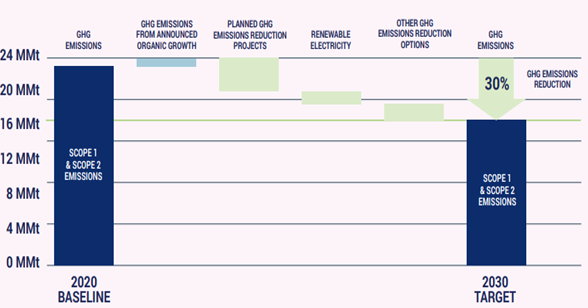

Given the lead time to get some of the emission abatement projects in place – whether it be renewable power or hydrogen with carbon capture – many of the 2030 goals that we see, like the LyondellBasell chart below – are likely to be just that – plans for 2030, with not much in the years in between. We see very little CCS coming online in the US over the next 5 years because of permitting and because of the lead time for any large hydrogen or power project that might be associated with the CCS. Not too many companies seem interested in cleaning up existing CO2 streams and are more interested in building alternative capacity that generates easier to capture CO2 – such as hydrogen from an ATR. These are expensive and long lead-time projects. LyondellBasell, ExxonMobil, Dow, and others might meet their 2030 targets but it might all happen in 2029/30.

The two charts below today are interesting bedfellows as while one talks about yet more, likely impractical, hydrogen ambitions, the other talks about a possible solution.

One of the concerns that the IPCC has in its report issued this week is that things are not happening fast enough and the Ammonia analysis in the chart below would support this view. Most of the capacity addition comes post-2030 in large part because project planners cannot see a way to enough cheap power to generate the green hydrogen needed until that time. In our view, since COP26 the transition part of the energy transition has been overwhelmed by advocates of green technology and renewable pathways without much thought about how practical they might be today. Those suggesting transition options are being given very little airtime and as a consequence, we see broad hostility towards anything that is not truly green, regardless of whether the costs or time frames make any real sense. If we do not embrace bold transitionary steps including the use of hydrocarbons with aggressive abatement targets we will not meet any of the shorter-term goals that the IPCC highlights and we are putting hope in renewable and technology development which may come up short. Related to this we see the LNG dilemma in Europe, with the current and medium-term needs very apparent, but a reluctance to sign up for longer-term supply because of an expectation that if all things renewable come to pass, the LNG might not be needed. The Europeans will need to make the longer-term commitment if they are to persuade the US and other potential exporters to build new export terminals.

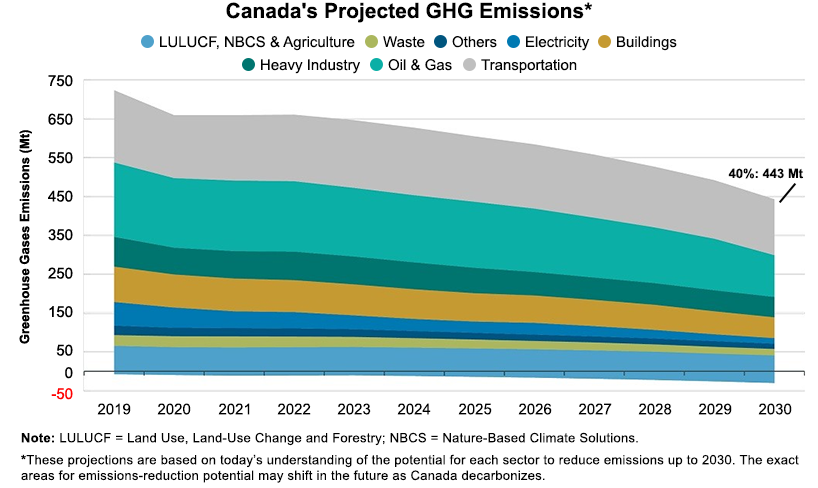

The Canadian targets highlighted below are ambitious and will likely not happen without the significant CCS projects planned for Alberta. The CCS opportunity will drive down energy and chemical (heavy industry) based emissions meaningfully and could also be the basis for new power generation capacity to allow the transport industry reductions that the country is looking for – either through EVs or hydrogen-based transport.

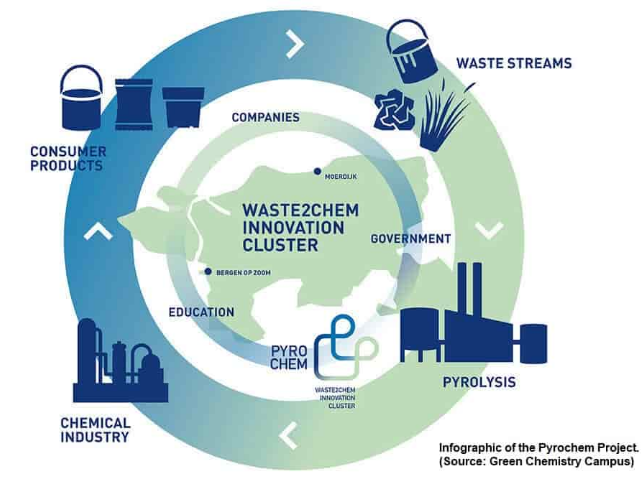

The focus of our ESG and Climate report tomorrow will be on recycling and the challenges associated with each proposed solution. The piece that most chemical recycling projects, like the one highlighted below, fail to mention is that the heat required for pyrolysis is significant, and the carbon footprint is very high unless you can heat through renewable power or you can capture the carbon associated with the heat. Given the location of the facility shown below, it could have access to offshore wind-based power and/or could tie into one of the offshore CCS projects that have been proposed. Both pyrolysis and gasification processes have very high emissions.

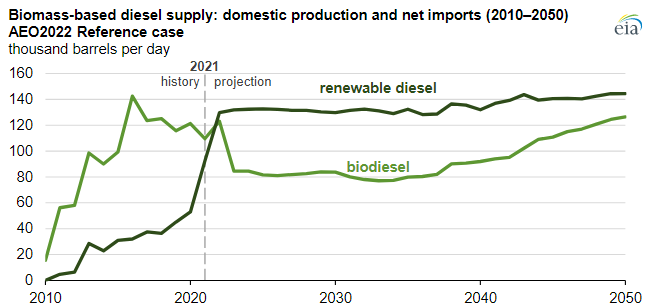

The EIA renewable diesel projections are based on a couple of things – who plans to make it and who will pay for it. All eyes are focused on the California market today as that is where the incentive lies – through the LCFS credit – and production plans plateau associated with that opportunity. As other states in the US adopt similar programs – which seems likely – we would expect to see production plans increase and the EIA will likely adapt its market view model and the chart will change. Note the dominance of renewable diesel over time, and this is where we would expect all future growth to occur. The plug-and-play nature of renewable diesel makes it a far more attractive option for refiners assuming the cost works. See more in today's daily report.

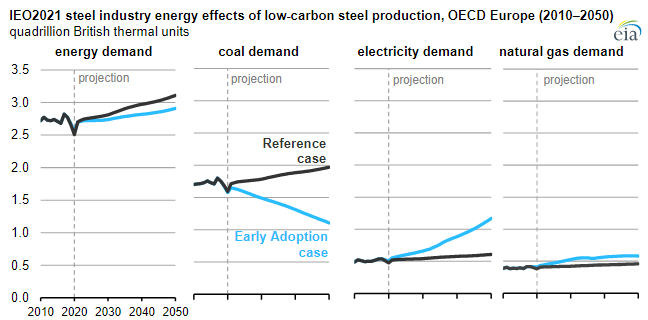

The steel analysis below is interesting because it is likely that a significant bifurcated market will develop for steel as the demand for green steel is likely to be significant, although probably not at any price, while there will also be a few opportunities to make low-cost green steel and the lucky few could make a lot of money. Anecdotally, we are helping a client look for the best use of what could be a substantial tranche of low-cost renewable power in a location that is not heavily populated, and consequently, there is a limited local demand for the power or anything you might make from it, such as hydrogen. Green steel has come up as possibly the best use of the power in a couple of conversations so far. This adds another wrinkle to the question of whether we can build renewable power fast enough – especially to meet some of the green hydrogen expectations. The challenge will be fending off potentially higher bidders for the power, and green steel is a real contender – more so if a reasonable premium can be gained in the market for the steel. See more in today's daily report.

Source: EIA – Today In Energy, March 2022