We share views from Christopher Sheeron - The first-ever guest author for C-MACC's most recent ESG and Climate report titled "Does DC Understand Economics – Energy Proposals Suggest No".

Main Points from this report include:

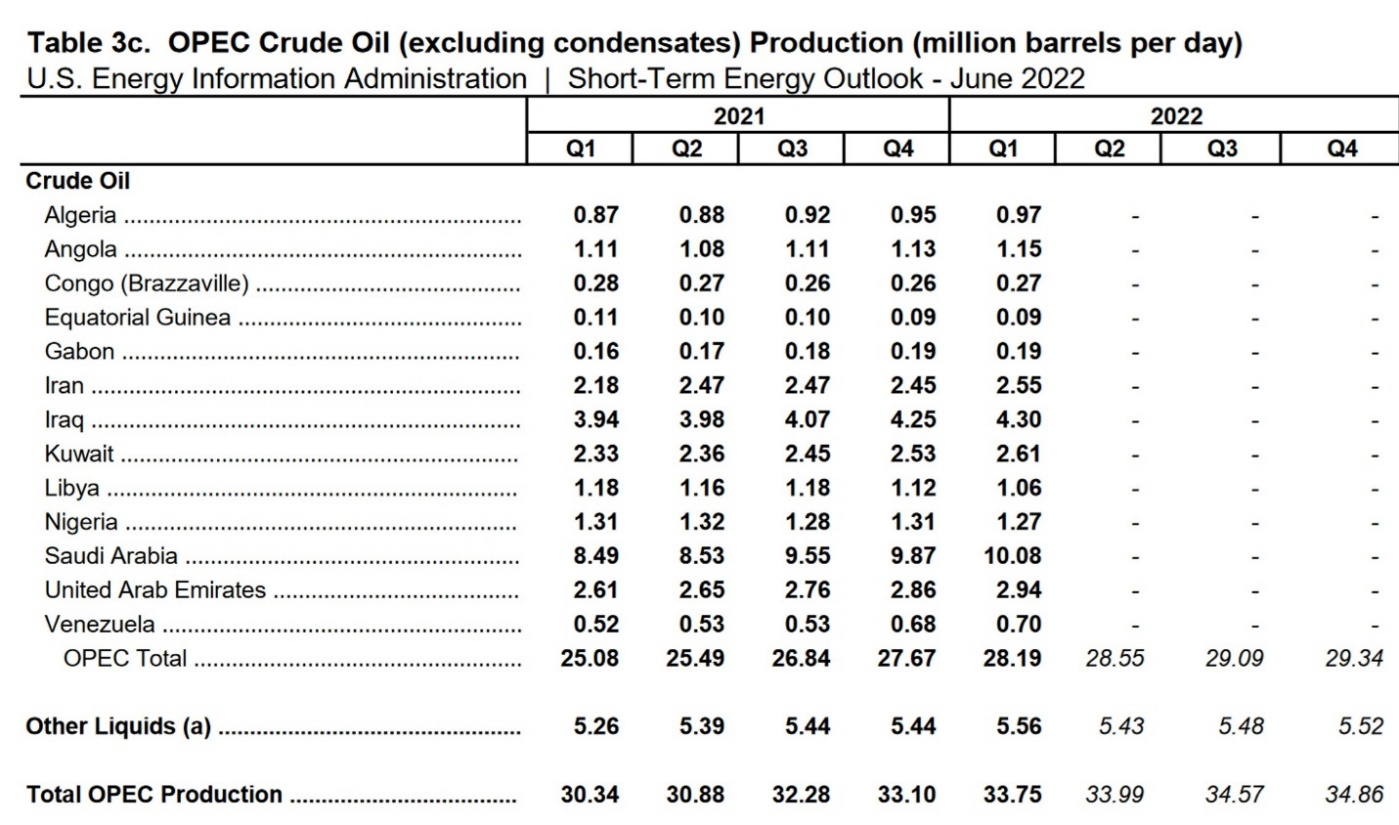

Jun 10, 2022 12:00:00 PM / by Christopher Sheeron posted in ESG, Sustainability, Renewable Power, Energy, Oil, solar, renewable energy, wind, climate, energy inflation, gasoline, water, OPEC+, NOPEC

Main Points from this report include:

Apr 6, 2022 12:36:34 PM / by Graham Copley posted in ESG, Hydrogen, Climate Change, Sustainability, LNG, Green Hydrogen, Renewable Power, Ammonia, hydrocarbons, solar, renewable energy, renewables, wind, energy transition, waste, hydro, geothermal

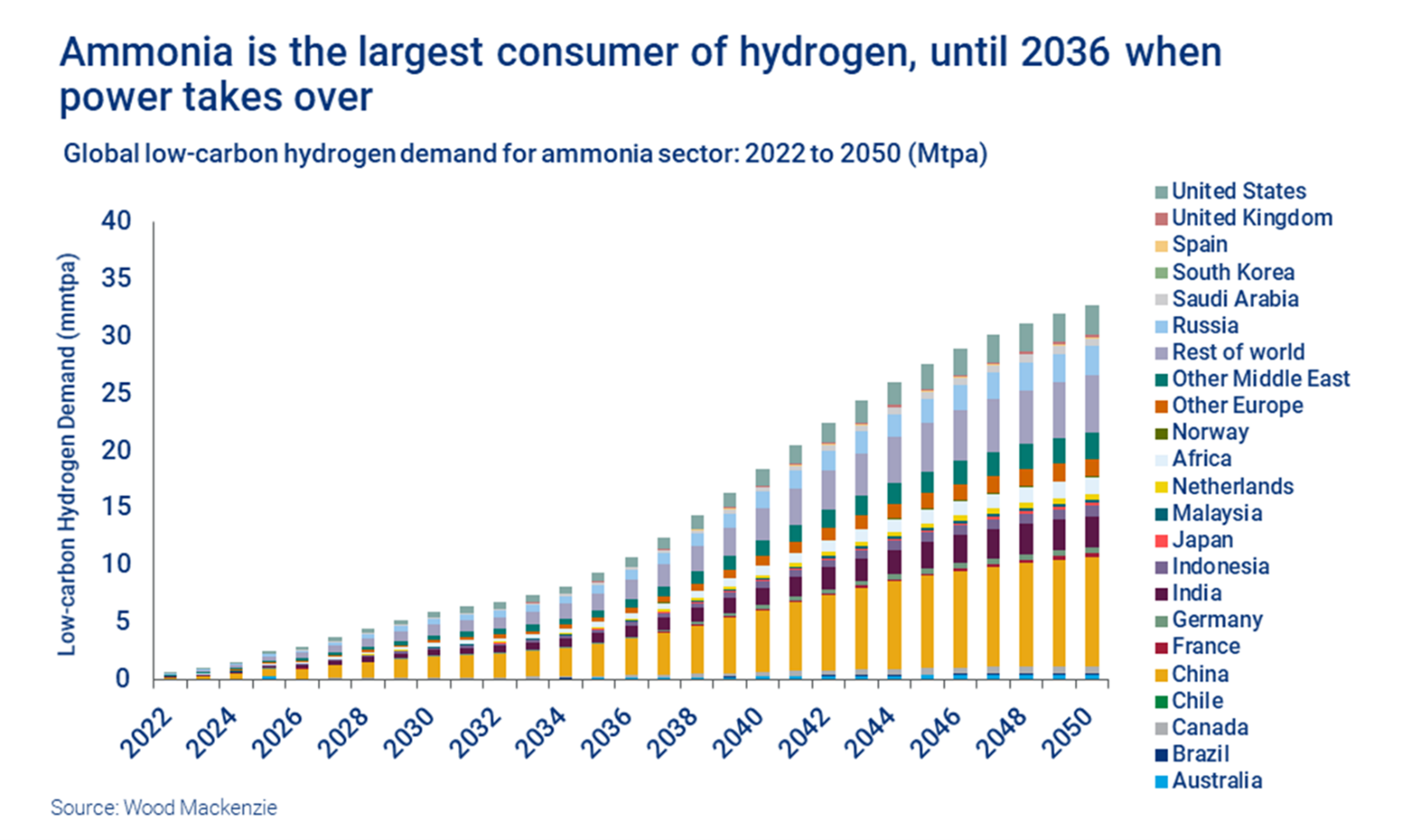

One of the concerns that the IPCC has in its report issued this week is that things are not happening fast enough and the Ammonia analysis in the chart below would support this view. Most of the capacity addition comes post-2030 in large part because project planners cannot see a way to enough cheap power to generate the green hydrogen needed until that time. In our view, since COP26 the transition part of the energy transition has been overwhelmed by advocates of green technology and renewable pathways without much thought about how practical they might be today. Those suggesting transition options are being given very little airtime and as a consequence, we see broad hostility towards anything that is not truly green, regardless of whether the costs or time frames make any real sense. If we do not embrace bold transitionary steps including the use of hydrocarbons with aggressive abatement targets we will not meet any of the shorter-term goals that the IPCC highlights and we are putting hope in renewable and technology development which may come up short. Related to this we see the LNG dilemma in Europe, with the current and medium-term needs very apparent, but a reluctance to sign up for longer-term supply because of an expectation that if all things renewable come to pass, the LNG might not be needed. The Europeans will need to make the longer-term commitment if they are to persuade the US and other potential exporters to build new export terminals.

Apr 5, 2022 12:32:08 PM / by Graham Copley posted in ESG, Climate Change, CO2, Energy, Net-Zero, carbon abatement, solar, renewable energy, wind, carbon prices

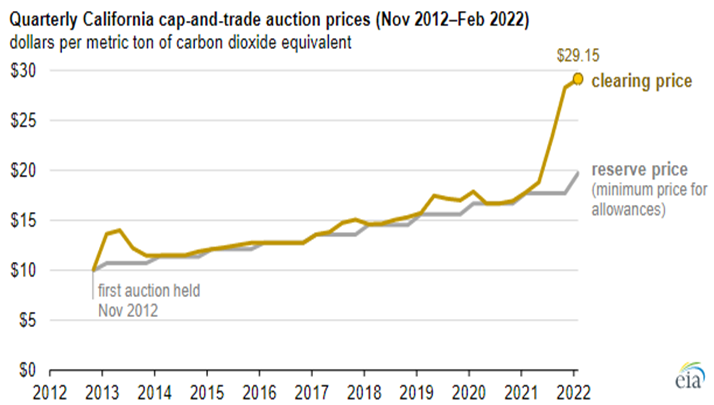

We have written extensively about carbon prices over the last two years and followers of our dedicated ESG and Climate service will know that our expectation is for all CO2 markets to see prices rise to levels that justify large investments to avoid CO2 production or sequester it. We see that price closer to $100 per ton than the $50 per ton that 45Q will rise to by 2026. The California price shown below has much more upside as credits demand rises. Many of the net-zero pledges made by manufacturers and energy producers today cannot be achieved without buying some sort of credit and we expect demand to rise relative to supply through the balance of the decade and possibly quite quickly.

Mar 23, 2022 2:19:27 PM / by Graham Copley posted in ESG, Climate Change, Sustainability, Coal, Renewable Power, Energy, Supply Chain, Oil, natural gas, power, solar, renewable energy, solar energy, Gas prices, renewable capacity, supply chain challenges, Utility, materials costs

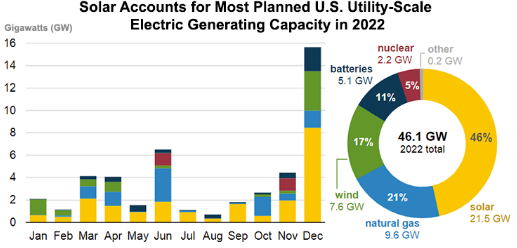

The back-end loading of the power projects for the US for 2022, as shown in the chart below leaves us somewhat skeptical concerning how much will come online this year. Supply chain problems and materials costs and availability are causing all sorts of problems with renewable power projects and installed capacity expectations for 2021 were too ambitious. We believe that companies are pushing projected start-ups later in the year to give them more of a chance of completion, but this creates the risk that they slip into 2023 or beyond. The most significant issue here is that as these plans get delayed, natural gas demand goes up, as one of the swing suppliers. This is fine as long as the US natural gas industry and shale oil industry is investing so that gas availability rises. Otherwise, we could see gas prices spike in the US next winter and another year where we use more coal than we expected. For more see this week's ESG and Climate report.

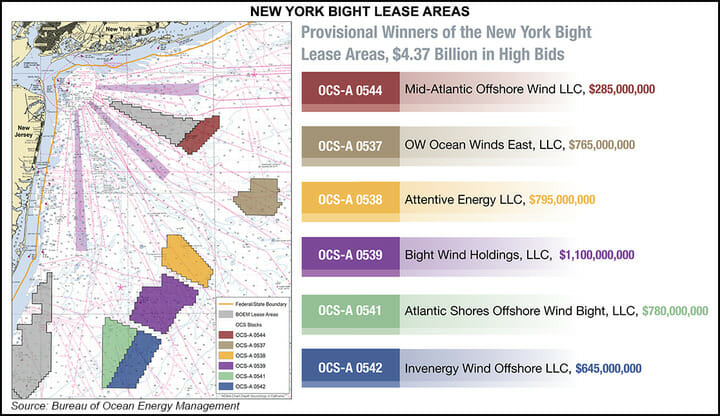

Mar 8, 2022 1:49:00 PM / by Graham Copley posted in ESG, Climate Change, Sustainability, Coal, Energy, natural gas, solar, renewable energy, power demand, manufacturing, wind, EIA, reshoring, offshore wind, raw material, battery

We include a couple of headlines and charts in today's daily report that step into the central theme of this week’s ESG and climate report, which will be published tomorrow (see here). The offshore wind ambitions and the EIA solar and battery projections both assume that the materials are available to build the capacity. In the case of the offshore wind leases, the winning bidders do not need to be in the market for all of the projects today and while the opportunities will lead to a step-change in demand for turbines in the US, the timing is less clear today that it will be in a few months and that timing may be adjusted to reflects equipment timing and costs, etc.

Feb 4, 2022 1:17:36 PM / by Graham Copley posted in Hydrogen, Carbon Capture, Wind Power, CCS, Renewable Power, natural gas, solar, renewable energy, wind, energy transition, material shortages, wind capacity, onshore wind, price inflation, Siemens Gamesa, logistic issues, offshore wind, solar industry, wind industry

The linked Siemens Gamesa news could not have been a more clear example of one of our key research themes of the last year – backlog up, suggesting strong demand for new wind power capacity – deliveries and profits down because of material shortages – price inflation and logistic issues. While the company is getting squeezed because of higher costs on contracts that have limited opportunity to pass through the cost, at the same time slide 8 of the earnings release deck shows that selling prices rose in fiscal 1Q 2022. This breaks a declining trend in pricing and one of the core assumptions behind many energy transition plans – that renewable power prices can keep falling. Onshore wind orders are falling, but offshore orders are rising – and these come with higher costs and the need for more materials as we showed in a chart in yesterday’s daily. The added costs burden of more offshore wind projects may only serve to tighten markets for materials further, leading to further increases in installed costs.

Jan 25, 2022 1:39:27 PM / by Graham Copley posted in Commodities, Renewable Power, Materials Inflation, natural gas, solar, clean energy, energy transition, commodity prices, US natural gas, supply shortages, solar capacity, natural gas demand, solar installations, commodity index, solar modules, power supply, material cost inflation, US natural gas prices, minerals

A couple of things worth noting today that reflects our commodity index in today's daily report but also looks at some of the results below. The linked solar headline is confirmation of one of the topics that we have probably worn out over the last few months, which is that renewable power ambitions have not taken into account real limitations in the rate of equipment supply, especially solar modules. New forecasts suggest that the US expected installations of solar capacity could come in 25% short in 2022, which has implications for energy transition ambition, but also overall power supply as the shortfall will have to be made up elsewhere. It is not just a function of solar module availability but also solar module costs, because of some of the material cost inflation illustrated in exhibit 1 (see today's daily report). These shortfalls will have implications for natural gas demand in the US if it needs to fill the gap, and we have already noted that we think US natural gas prices could spike in 2022, much higher than we saw in 2021.

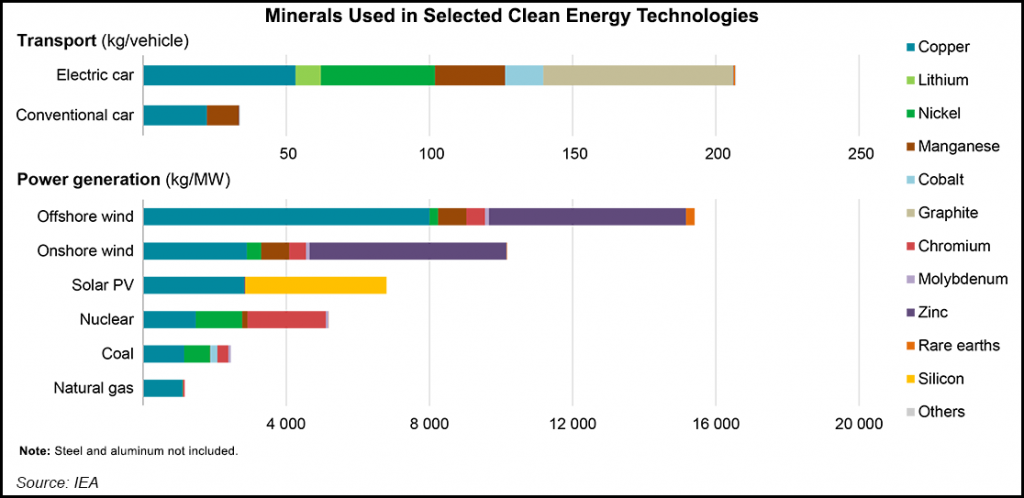

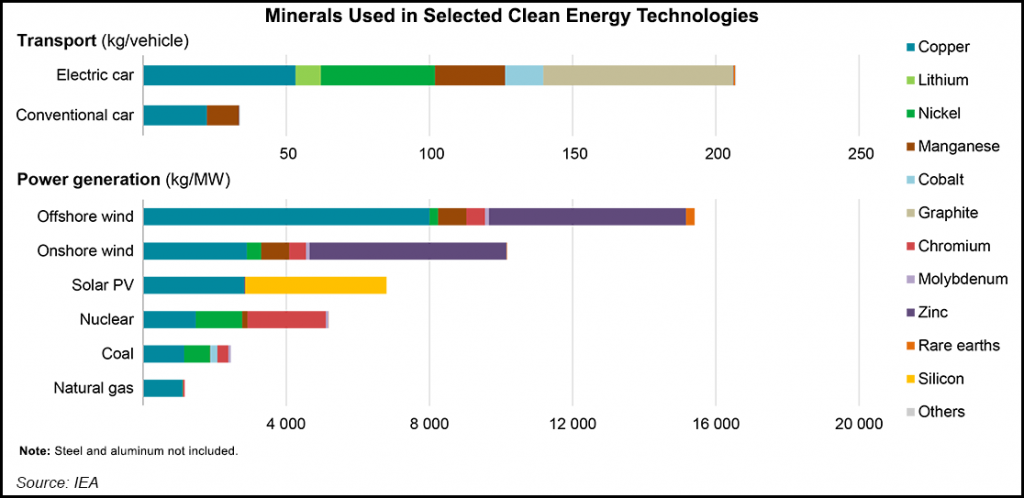

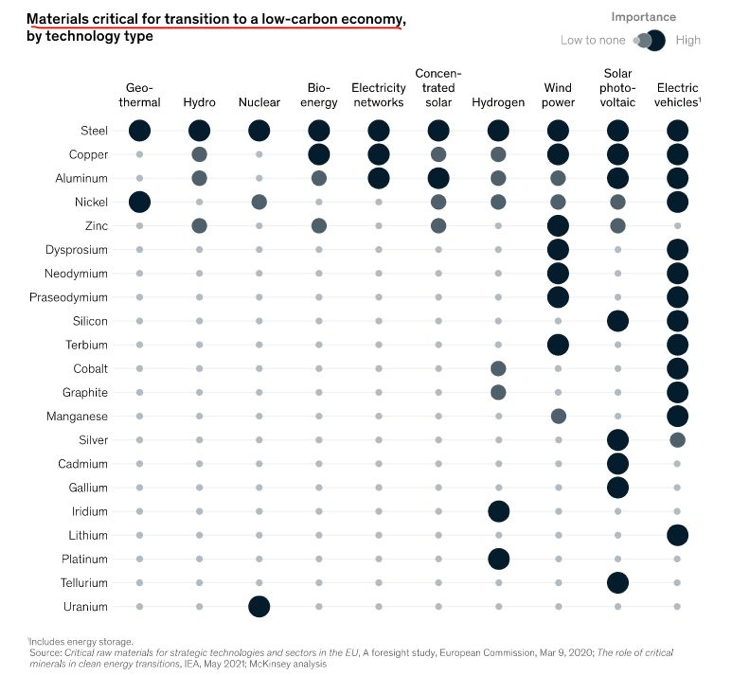

Jan 21, 2022 1:07:16 PM / by Graham Copley posted in ESG, Hydrogen, Sustainability, Renewable Power, Metals, Raw Materials, solar, renewable energy, wind, energy transition, Lithium, climate, advanced recycling, materials, low carbon, material shortages, low carbon economy, renewable power production

The materials chart in the exhibit below from today's daily report, is worth noting as it highlights all of the materials that are needed to advance the production of equipment required to drive renewable power production and demand. We would make one change to the chart in that lithium should also be added to the wind and solar categories to account for storage that needs to be built, although this could be done through hydrogen production or hydraulically, depending on location. One of our primary concerns concerning renewable power projections is the availability of some of these materials and we have written about the topic at length – most comprehensively in - 2022 – Policy Key, But Inflation Will Distract – Maybe Beneficially.

Jan 20, 2022 11:58:06 AM / by Graham Copley posted in ESG, Sustainability, Renewable Power, solar, renewable energy, climate, EIA, US natural gas, materials, energy inflation, material shortages, solar capacity, US natural gas demand, renewable capacity

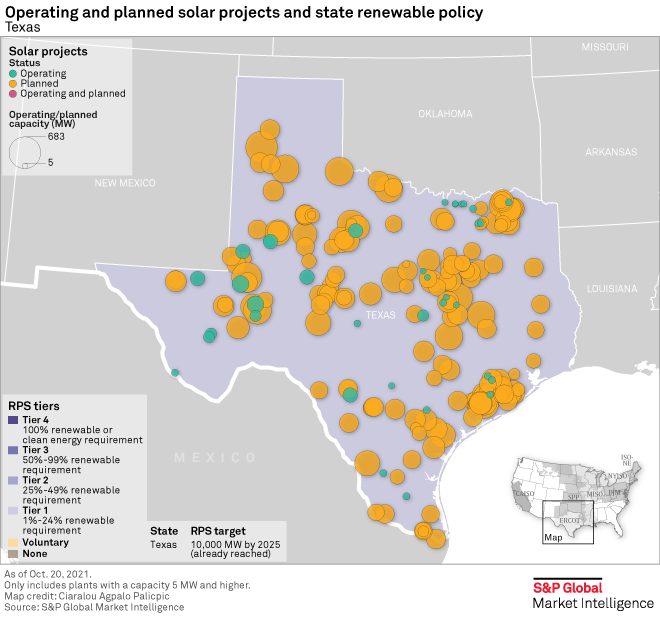

We struggle with both of the charts below, as we see the rate of potential renewable additions as far too optimistic, not because of a lack of capital, but because of a lack of materials and the knock on effect that this could have on capital if project costs increase meaningfully or if timelines extend. The solar expansions planned for Texas for example all require solar modules and there is simply not enough capacity to make these modules and in many cases not enough raw materials. All of these projects are not planned for the same year, but regardless, when you add the Texas plans to plans all over the World, you have an annual rate of addition that the equipment makers will not be able to meet. Today, many of the projects are in the planning and financing stage and the installers have yet to go looking for equipment – when they do, they may have to rethink.

Dec 31, 2021 12:26:02 PM / by Graham Copley posted in Wind Power, Renewable Power, Metals, raw materials inflation, Inflation, solar, EVs

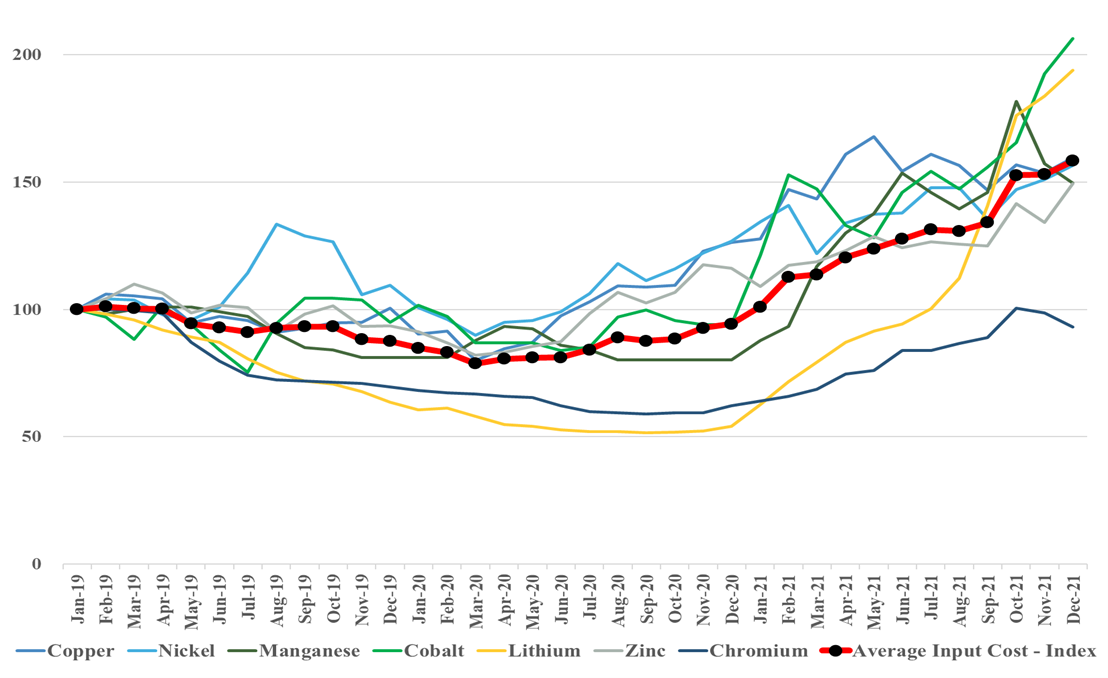

Continuing with our inflation theme this week, we show our renewables metals price index in the Exhibit below, which continues to climb and is now 50% higher than it was 2 years ago, with cobalt and lithium leading the charge at around 100% higher. These are critical components for EV and renewable power manufacture, and with 2022 forecasts for all suggesting much stronger growth, we do not see the materials supply/demand balances improving, suggesting that pricing will go higher. Energy shortages today, will only add more upward pressure to build more renewable capacity quickly and add even greater inflation risk to both components and the materials used to make them. We are concerned that, on the list below, only lithium is seeing significant capital thrown at increasing availability, suggesting that while lithium may peak in pricing, other metals could keep marching up. See our recent Daily, ESG Report, and upcoming Sunday Thematic for more.

C-MACC utilizes a proprietary process that melds decades of global chemical industry experience, detailed fundamental analysis, extensive field research and innovative analytics to provide our clients research products and services, and strategic consulting offerings. Our main objective is to enable informed decisions for our clients and to do so in a timely and cost effective manner...