The primary reason for the flurry of carbon capture related headlines in the US over the last few weeks – and our analysis shows a significant step up – is because it looks like this will be the one technology/route to lower carbon emissions that will get a real boost from the infrastructure bill. There is bipartisan support for CCS because the fossil fuel industry sees it as a way to stay in the game and the unions believe that it will create jobs. This combination should garner enough votes to push it into the bill and get it passed, although the details around how CCS would be supported remain unclear. The infrastructure bill has very few real sources of income in it to offset the very high costs – something we will discuss on Sunday – and consequently giving a bigger tax break, through the 45Q program would create an even larger funding gap than we have today. The value/cost dynamic has to rise to get the activity that everyone is looking for and maybe that could be achieved by overlaying a carbon credit onto the program. Anyone exporting to Europe and concerned about the CBAM extending to natural gas, NGLs, chemicals, and polymers would likely consider CCS if they were eligible for 45Q and could also claim an offset on their exported products to neutralize the CBAM tax/fee.

There are some serious players behind the CME offset futures trade highlighted in the linked headline. However, the press release does not provide enough information around how the offset is calculated and this will be critical if the futures product is to develop into a fully functional and fungible market. The agriculture-based offsets sound good and, in many cases, they can be robust in terms of the genuine contribution to lowering CO2 in the atmosphere – for example, where a new tree is planted and there would not have been a new tree without the direct action. But there remains a great deal of debate around whether an initiative is more positive than its alternative. Would a tree have grown naturally if the project was not there? Is the carbon footprint of any wetlands mitigation initiative taken into account when looking at the CO2 offset – same with tree planting? How do you risk adjust the CO2 value of a tree or other agriculture offset – what if the forest burns?

There has been a lot of press over the last couple of months around carbon offsets – not least because of Mark Carney’s efforts to legitimize the idea. Mr. Carney’s focus is to create a robust trading platform for the buying and selling of legitimate offsets so that a carbon market can operate efficiently. He believes that without accurate and realistic carbon values, and the ability to buy and sell them, the capital markets around emission reduction will be inefficient and that less money will be attracted into the area. On this, he is probably correct, but in our view, the carbon offset markets have a long way to go.

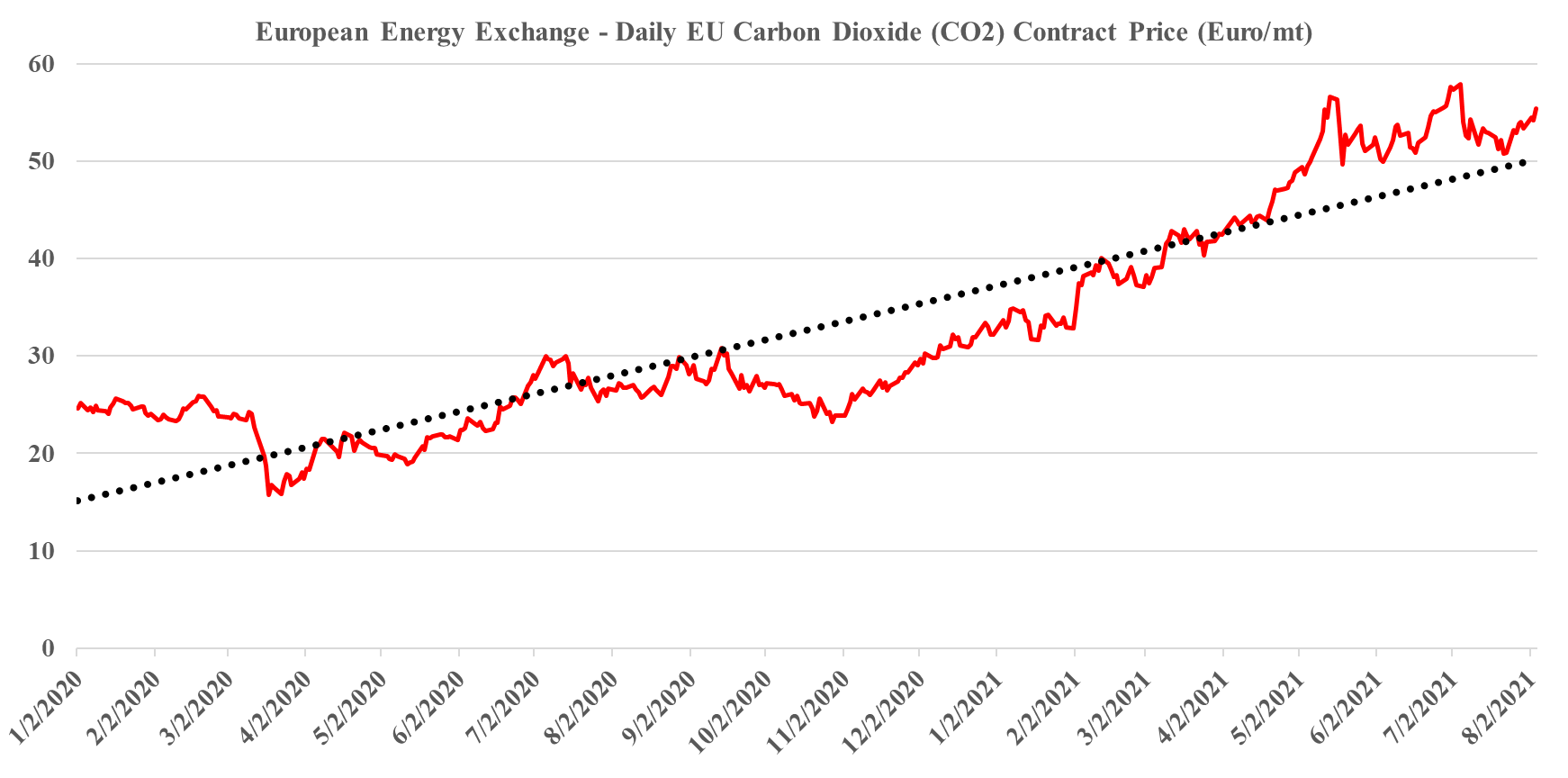

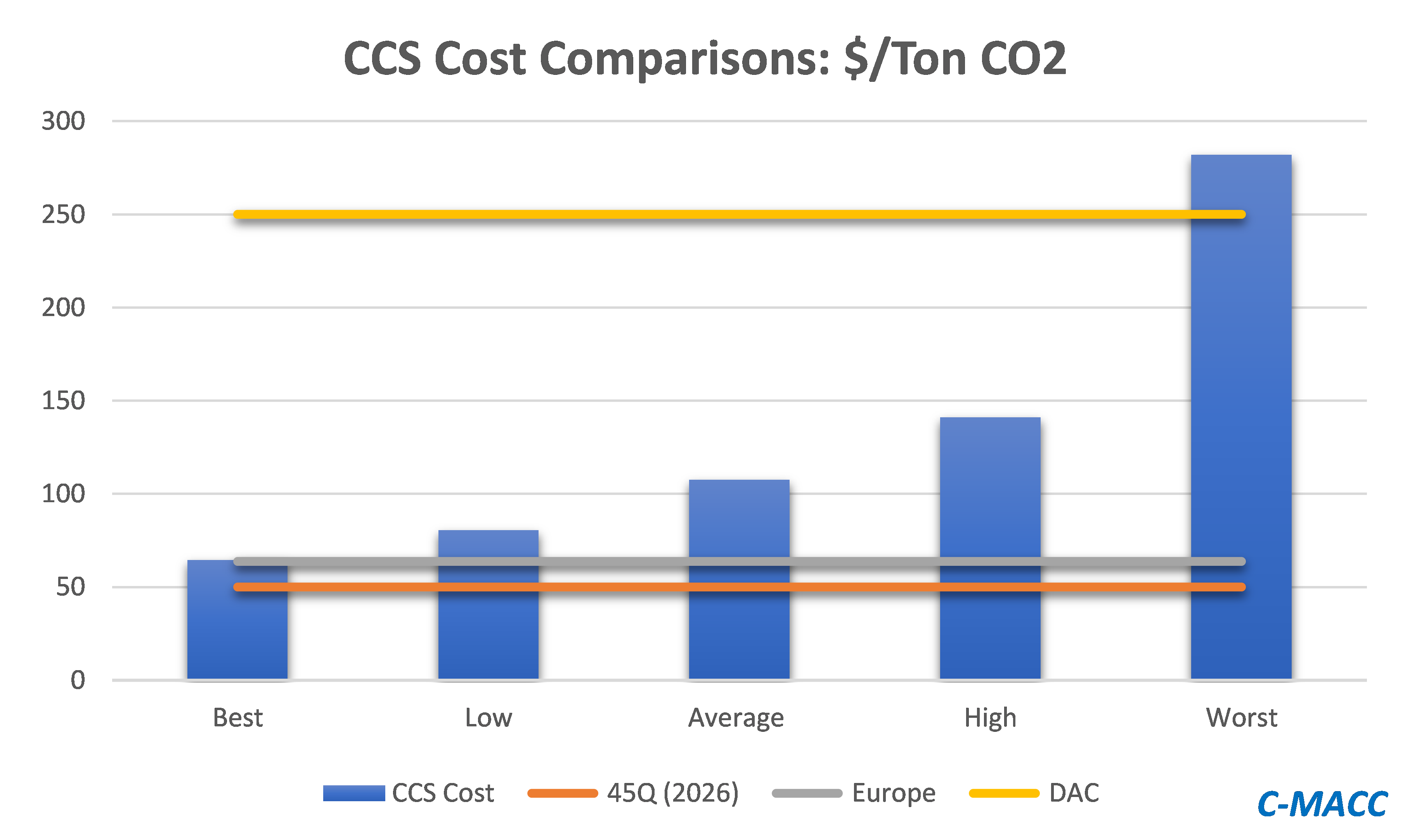

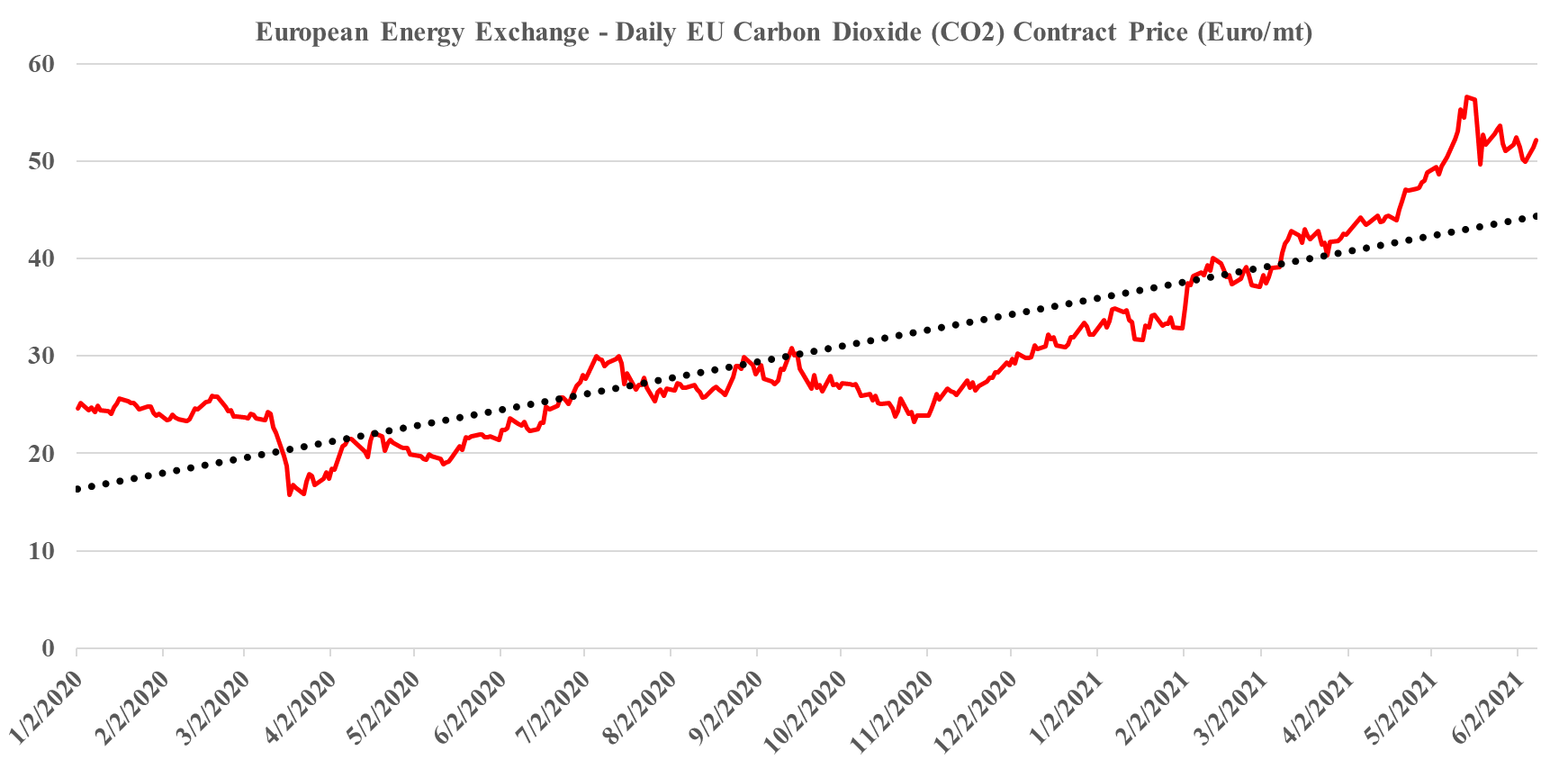

In our ESG and climate piece today we focus on Carbon Capture and Sequestration (CCS) and the likely very steep cost curve between the mega projects and those less fortunate. But as we discuss CCS, we should not forget that the World is still not convinced about CCS as part of the solution set for carbon abatement, as the headline linked discusses. The naysayers are focused on the lifeline that CCS offers to the fossil fuel industry, but always fail to offer an economic rationale for the quick elimination of fossil fuels and their replacement by renewables. Few of the proponents of CCS see it as an alternative to a long term path to alternative means of abatement, but all recognize that relying on renewable power investments will likely leave the World with a much larger CO2 footprint from 2030 to 2050 than what could be achievable with CCS – note that the 45Q incentive in the US has a finite lifespan as there is an expectation that eventually CCS will be unnecessary because of fossil fuel replacement. Chevron has not helped the CCS proponents with its missed targets in Australia as it adds fuel to the argument that CCS has not lived up to its potential. While the European carbon price trend has stalled in recent weeks – chart below – the trend remains distinct and it would be foolhardy to ignore the likelihood of prices rising to a level that makes CCS attractive – especially for the mega-projects.

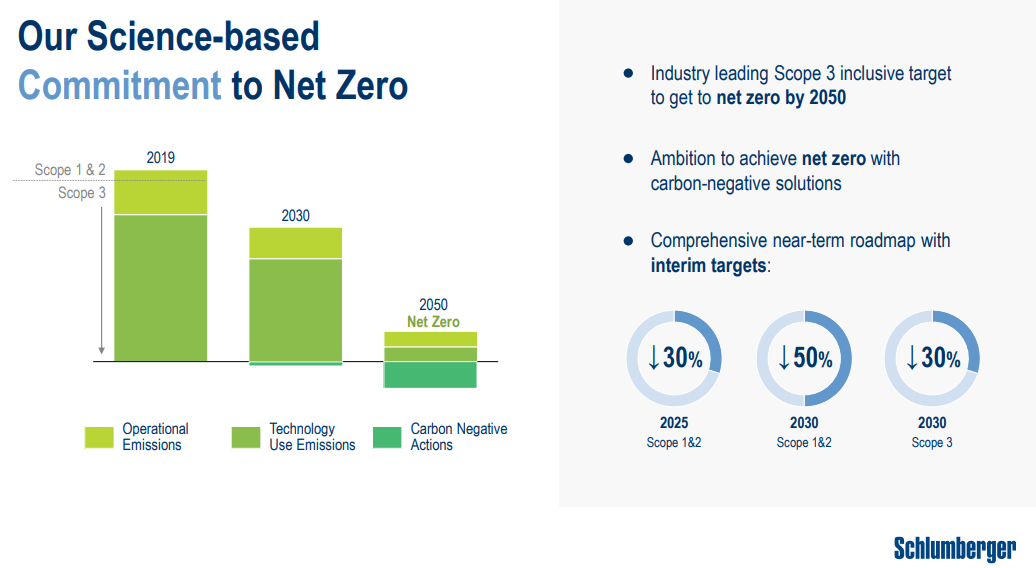

The Schlumberger net-zero goals, as discussed in a couple of articles in today's daily and the presentation linked, set some aggressive but bold ambitions, especially as they are looking to solve problems that they share with their customers, methane leakage from oil and gas wells, and minimizing flaring. Schlumberger is a little dependent on collaboration from its customers here as the technology solutions are likely to be more expensive than current options and the oil and gas producers will need to pay up.

The WSJ article linked talking about rising ESG spending and the risks associated with it is in no way inconsistent with our view that lack of US Government guidelines is constraining ESG spending. The article focuses on the power and auto industries, which, while they face regulatory and incentive uncertainty, have a much clearer path than many others. The power industry is dealing with a customer which is increasingly asking for more renewable power, an investor base that is pushing for less reliance on fossil fuels, and a Government that is pushing for a 50% emissions reduction from the sector. The auto suppliers have clear directives from some US states and some countries about the phasing out of fossil fuel-based vehicle sales, and in some geographies, they have incentive systems that they can tap into. For both industries, there is a significant risk, in that the billions of dollars that they are investing in new plants and new equipment do not come with any guarantees that those investments will pay off well or quickly, but at least the direction of travel is unlikely to change. In other words, there will be demand for their products and investors will likely be happy with the progress – while they might not get the EBITDA they would like, they may get a better multiple of that EBITDA.

Whether it is carbon capture, hydrogen investments (blue versus green or just in general), plastics waste, or any other aspect of the drive to greater sustainability and net-zero emissions, everyone is looking for a “playbook”; a set of rules that allow for more effective and less risky decision making. The headline linked that talks about the chemical industry needing governments to take more action is another such example. Companies facing increasing shareholder pressure to make change are not only looking for government guidance and possible incentives but they are also not wanting to second guess what any regulatory move might be. No one wants to make a significant capital decision if there is a risk that a government policy shift will make it the wrong move. The European carbon credit price – shown below is at least a framework that many European companies can use to value possible decisions – even if some European companies and countries are moving at different paces than others in terms of emission and hydrogen mandates. The price is tangible and its mechanism for calculation should also allow companies to forecast how it might change. Europe is also working on a plastic waste tax – this would give a stronger economic framework to push improved recycling.

Source: Bloomberg, C-MACC Analysis, June 2021

The Navigator CCS announcement is extraordinary in its boldness and potential lack of any real chance of economic success. The idea of building 1200 miles of high-pressure CO2 pipe (See exhibit below) to collect small volumes from corn-based ethanol producers and potentially have multiple sequestration sites is extremely expensive and would not begin to be covered by the 45Q tax credit, which would easily be consumed by the compression and pipeline costs alone. If some of the ethanol is making it into the LCFS markets, each ethanol producer that has some material heading that way will want a piece of the pie and if each had to jointly file with CARB, with Navigator, for what would be small portions of the overall ethanol output, the administration might be overwhelming, as would be a chain of custody process which satisfies CARB. Navigator is not an altruist fund and consequently, must see a way to make a return on the idea. This may be based on the hope that LCFS or something like it will spread to other states.

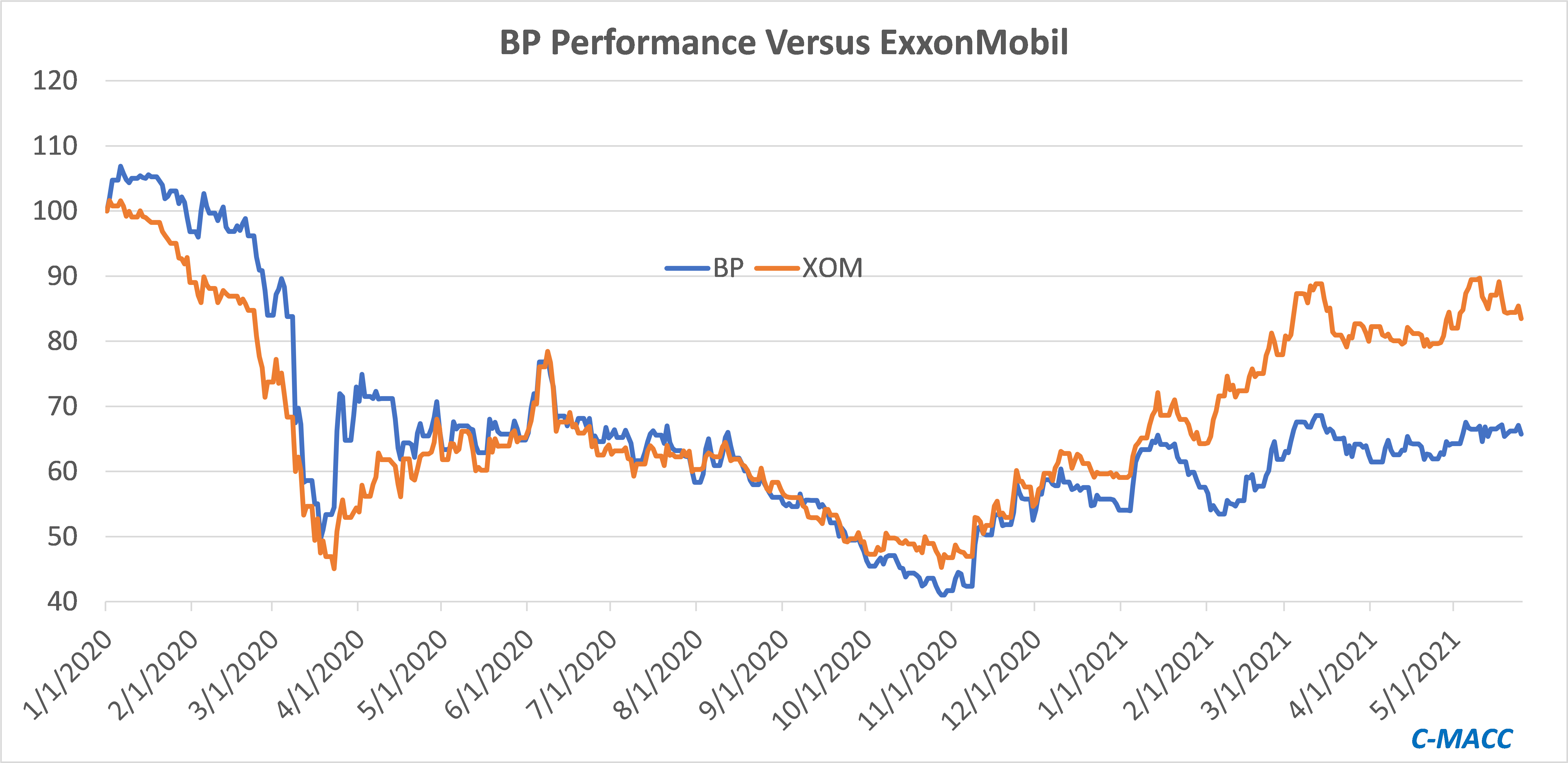

With little chemical corporate news of note, we will focus on ExxonMobil today. The shareholder activism may be high but it is unclear to us what the activists hope to achieve, even if they are successful at the annual meeting. The ESG investment group has largely given up on energy and even if ExxonMobil changes strategy and agrees to spend more on carbon abatement it is unlikely that new investors will show up, especially if the new strategy is more costly. Despite all of its directional change and rhetoric, bp has underperformed ExxonMobil since Mr. Looney took the helm in early 2020. If ExxonMobil were to follow the bp playbook, it is not clear that shareholders would benefit.