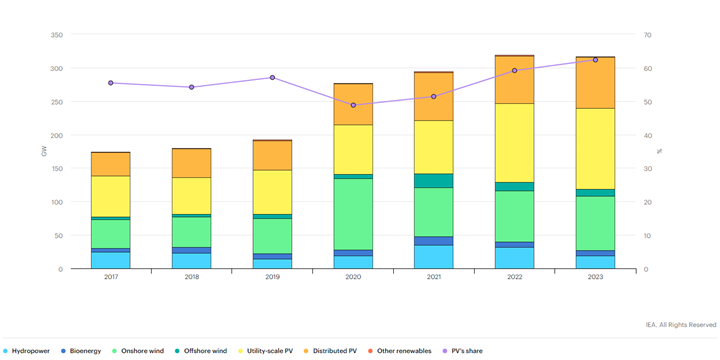

The renewable power space is heading for a very bad year in the US and Europe, as supply chain issues and raw material inflation will impact not only the amount of business that gets completed, but also the margin on that business. The trade issues between the US and China on solar panels have essentially brought the industry to a halt for the moment and suggests that all forecasts of the growth in renewable power contributions in the US in 2022 are too high, and consequently demand estimates for natural gas and coal for power generation are too low – see out comments in the energy section of today's daily report. The EIA forecast below likely fails to take into account the current woes and if governments, at the federal and the state levels act on the information in the chart they may be unprepared for some power shortages later in the year. Overestimation of the rate of renewable power installation as well as its operating rate is responsible for many of the current power shortages that we see in most regions.

We are seeing a flood of CCUS announcements in the US in 2022, but they look like “gathering” exercises at this stage rather than projects that are ready for FID. Companies are chasing potential pore space and, like Talos, leasing onshore and offshore (mainly offshore) acreage, where they believe opportunities exist to sequester CO2. These announcements sometimes include firm commitments from companies that have CO2 surpluses and sometimes are more speculative. At this stage, it seems like a “land grab” and “customer grab”. There is wide agreement that the incentive structure in the US – centered around the 45Q tax credit scheme – is not enough to drive much real investment, unless it can be stacked with other credits like the LCFS structure, which only applies to fuels in California today. We see the land grab as relatively low-cost and low-risk positioning in the hope that incentives or economics change. There are some instances where investments will go ahead, and these will focus on processes that have a reasonably low cost of carbon capture – fermentation, urea, natural gas clean-up for LNG, and a handful of other processes. The LSB Industries announcement for Arkansas, highlighted this week, is likely an example of where the economics work even if LSB cannot get much of a premium for the low-carbon urea.

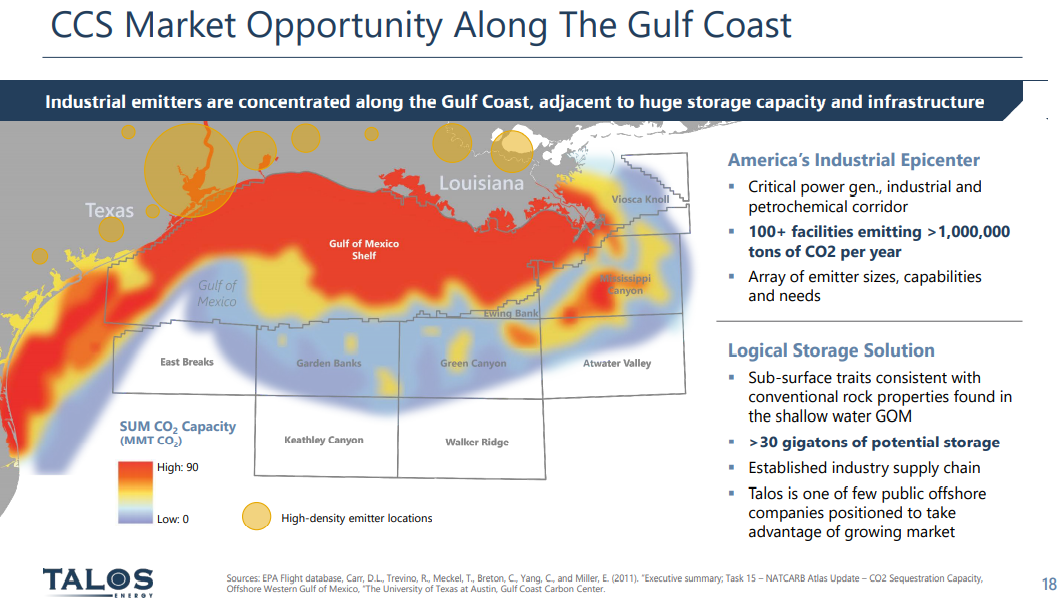

The Talos release and the map shown in the Exhibit below, highlight some of the potential for offshore CCS along the US Gulf Coast. We will likely see some of this developed over time, in our view, but the question of cost is important, not because the US Gulf is likely to be more expensive than some of the offshore locations that are proposed for Europe, but because the same offshore geology on the US Gulf exists onshore, and the onshore opportunities will likely be much lower cost. Given that one of the overriding concerns around carbon abatement is cost and how it will be paid for, who will pay for it ultimately, and what it means for the competitive landscape, finding the lowest cost solutions will be key. This is something that we have covered at length in our dedicated ESG and climate research. Building high-pressure pipelines is expensive, and high relative to the onshore cost of sequestration. Talos might find interest from CO2 suppliers but may be undercut by onshore projects – assuming these get the green light from regulators – not giving them the green light would likely be imposing further unnecessary costs on industry.