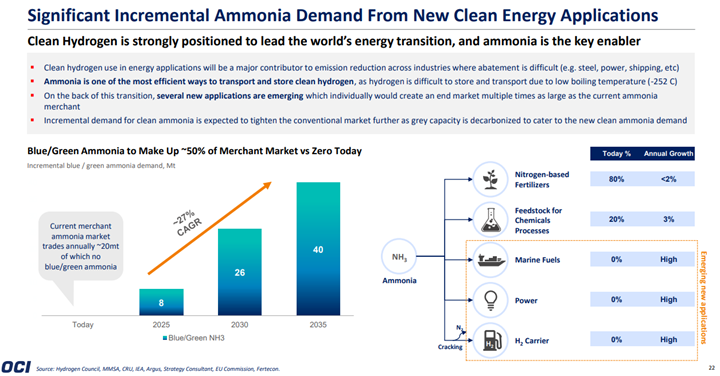

Despite all of the rhetoric about the need for green hydrogen, we see most of the large ammonia producers pursuing large blue projects – with Nutrien’s announcement yesterday coming on the heels of a CF new facility announcement and the CO2 capture project announced by LSB a couple of weeks ago. While there are some small (proof of concept) green projects in the works, they are very small, tiny when compared with the ammonia need, whether to replace lost material from Russia and Ukraine or whether to supply what could be substantial needs in Asia to co-fire coal plants, or as a shipping fuel, or as a carrier for hydrogen (see third chart below). The ammonia majors are not waiting around for “green” economics to improve as they see meaningful near-term demand that cannot wait for scale efficiencies of available power on the green side. Large-scale sources of cheap renewable power are hard to find, and where they may exist, there is competition from uses that may be able to pay more.

There is the potential for the ammonia thirst (please don’t drink it) to surpass opportunities to build cost-effective capacity for the medium term. Consequently, the shortages we see today could extend and become more severe. Co-firing coal-based power facilities in Asia is one of the more obvious ways to start decarbonizing a predominantly coal-based power region. The experiments in Japan, if successful, will drive a step-change in demand for blue or green ammonia, and this should drive much more new capacity than we have seen announced to date. The power-based demand comes on top of expected growth in fertilizer-driven demand and a possible rise as a shipping fuel. The issue for investors is that green ammonia at scale is economically challenging, especially with the recent shortfalls in renewable power generating plans and what now looks like rising power costs for a while. Blue ammonia is much easier to think about at scale, but we are still hamstrung by expensive carbon capture costs and a lack of incentives – either in terms of tax breaks or taxes or in terms of a customer willing to pay more, to get most ideas and plans past the “wouldn’t it be nice” phase. In the meantime, as indicated above, installed ammonia capacity is making abnormal returns.

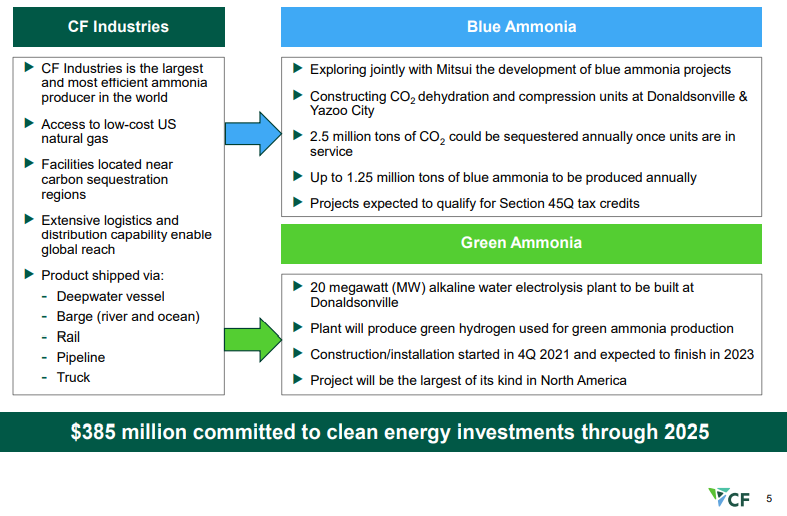

We continue to believe that the US has a cost advantage in CCS versus many of the other regions of the world and that when coupled with low natural gas prices the US should be able to take a lead in developing low carbon chemicals. CF is pushing the idea of both blue ammonia in the US as well as green ammonia, and while the company has yet to announce sequestration plans for the CO2 it is working to purify – see Exhibit - once dehydrated and compressed the incremental cost of storage should be low.

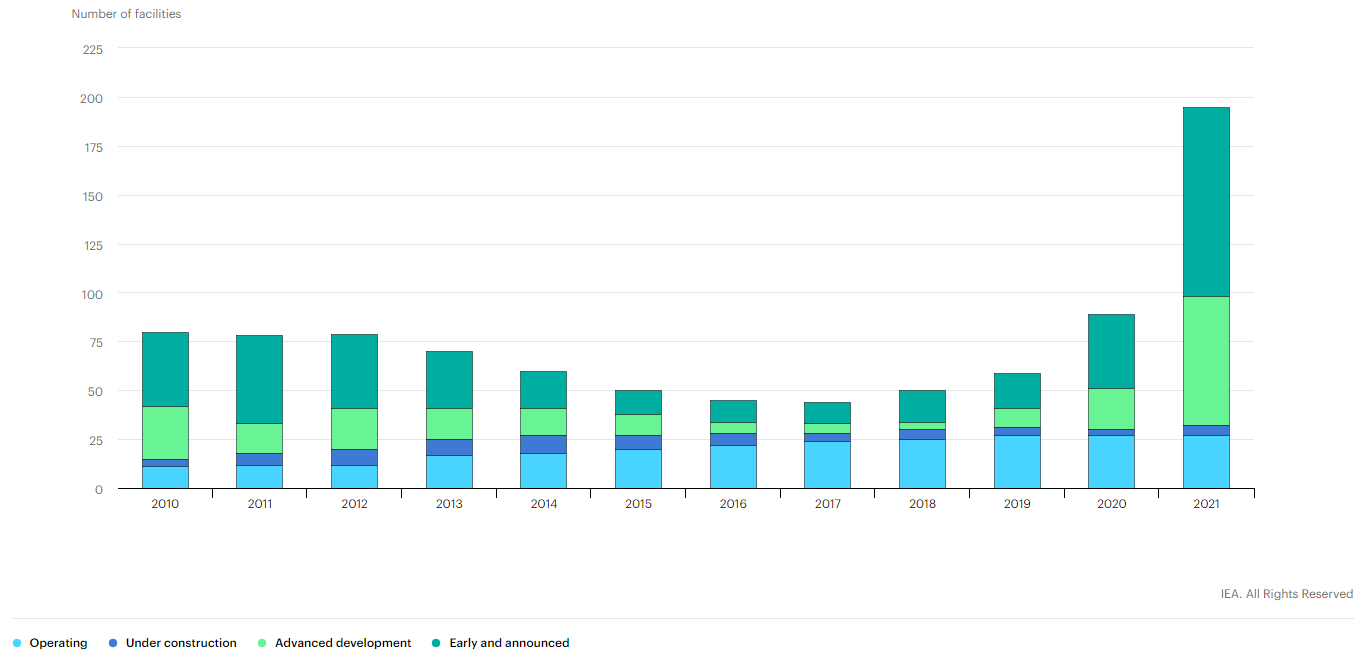

We note the IEA work on CCUS in several charts below and this is good timing relative to our ESG and climate report this week – which focused on carbon pricing, something we believe is necessary to promote more real activity in CCUS. In the Exhibit below, it is important to note how many projects are in “development” rather than operational or under construction. It is also worth noting that the number of projects under construction has not grown since 2019. One of the reasons for this is that increased activity at the planning stage is then followed by a delay associated with permitting, which depending on the region can take 2 plus years. The other constraint is uncertainty, with many of the projects under consideration waiting for something to change, either local values of CO2 or mandates or direct government support. For example, the large project planned for Houston and championed by several oil, power, and chemical companies is unlikely to move forward without a higher tax credit for CO2 sequestration or without some other incentive. The mid-West projects targeting the ethanol industry will also need permits, not just for the wells but also for the many hundreds of miles of proposed pipelines.

In our ESG piece yesterday we talked about the competitive edge that Canada now has with respect to both natural gas (because of lower prices versus the US) and CCS, both because of relatively low costs but also because of the clear value on carbon. Yet today we see an announcement in the US!

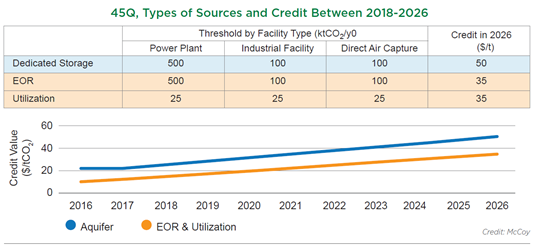

Senator Cramer’s proposed Bill to increase the value of the 45Q carbon credits for sequestration and use as well as remove the annual cap could be a game-changer in many ways. The threshold removal is necessary regardless of the credit value. In our view, the cap creates a potential competitive disadvantage for smaller companies competing with larger ones, especially in the chemical space. Should the Bill increase the tax credit enough to drive real investment in abatement but not remove the threshold we would expect to see litigation from smaller disadvantaged companies. The chart below shows the current expectations for 45Q. To date, the only real investment activity we are seeing is around sequestering CO2 from ethanol production in the US. This is because the CO2 stream is easy to separate in a fermentation process and because some of the ethanol can benefit from the much higher LCFS credit if the fuel is sold into California.