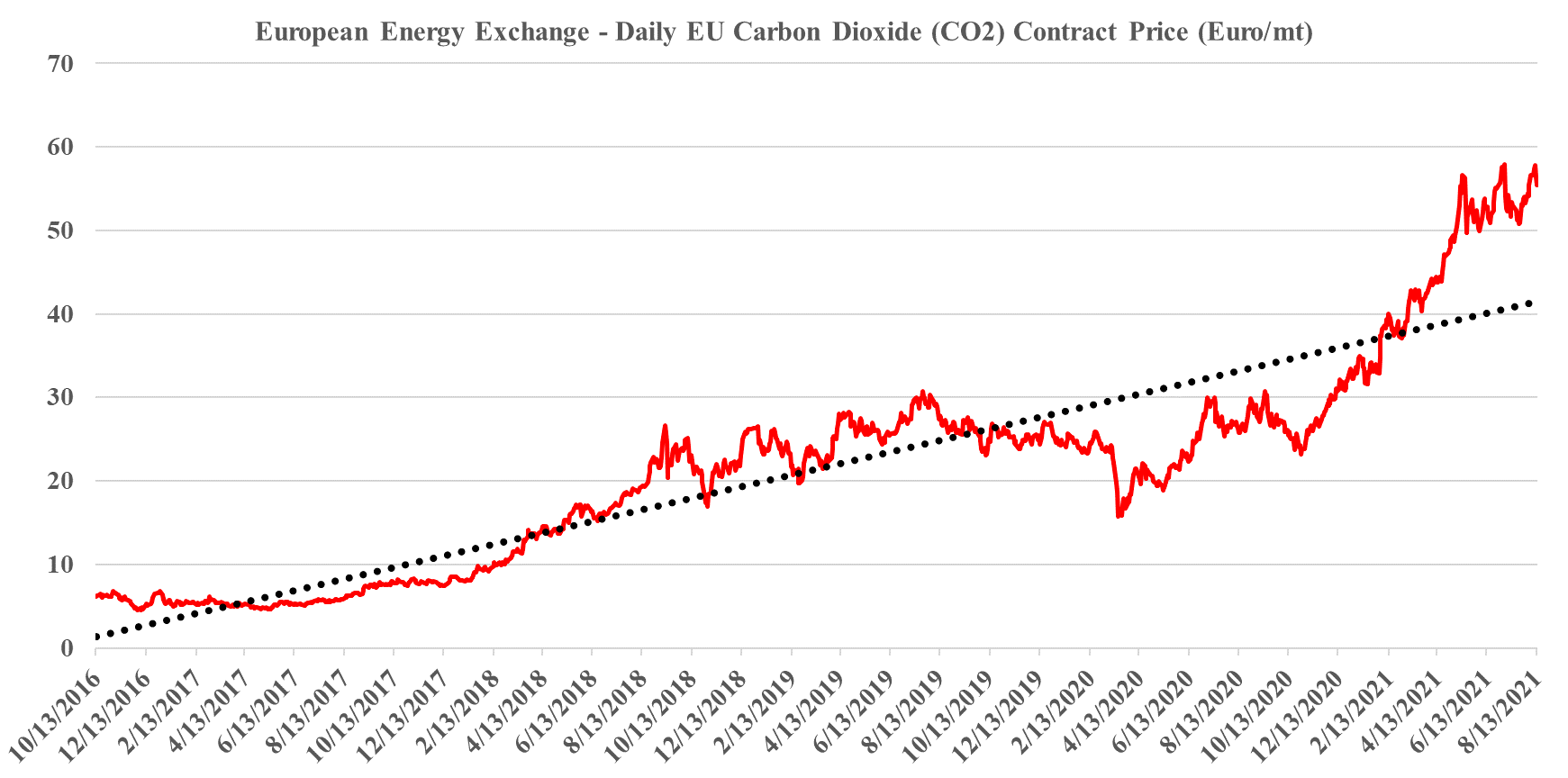

There are two elements/risks to ESG investing and both are highlighted in articles in today's daily report. The first is a reminder that returns matter and this is a reference to the very high multiples that are being applied to some of the more speculative clean energy stocks where there is credit being given today for technology and scale tomorrow. As with the tech bubble, there will inevitably be companies that fail, either because they have an offering that either will not work or will not be economic or because the market moves away from what they are doing. The fuel cell stocks would be at risk if hydrogen remains too expensive to consider as a transport fuel and if batteries or bio-based fuels become the dominant solution. Equally, bio-fuels could fall out of favor if hydrogen is abundant. On the polymer side, better collection and more chemical recycling could make switching to biodegradable polymers unnecessary or uneconomic. There will be winners and losers on this basis and the better strategy is to buy baskets of new technologies rather than bet on just one.

As we sift through the positioning for the upcoming COP26 meeting and the attention focusing report from the IPCC this week, it is a reasonable question to ask what this means for the plastic waste issue. If governments, lobbyists, and activists are likely to be more focused on climate change action over the next few years, which seems to be a reasonable conclusion, will there be the bandwidth for plastic waste? The plastic waste issue is less open to interpretation than the climate change issue and is a visible problem for all, but if governments need to prioritize where they spend their incremental dollar, and/or where they provide incentives of penalties, the climate is going to be pushed to the front of the line in our view. Plastics producers will have to deal with emissions, like any other industrial user of power and heat. The risk is that local governments, looking for revenue to support climate initiatives see taxing virgin plastic (or unrecycled plastic) as a way to both push plastic waste initiatives forward and raise revenue. Adding a plastic tax in the US to the superfund proposal in the infrastructure bill would be hitting the chemicals industry from two sides and would give bodies like the ACC far more grounds for pushback. For more on the IPCC analysis see our ESG & Climate Change report from this week.

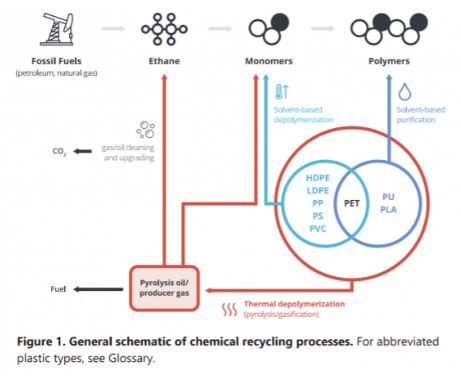

We believe that the plastics industry is right to get as much state backing for chemical recycling as it can – see Louisiana headline and diagram below. While chemical recycling is not as neat as mechanical recycling, it has far more chance of dealing with the core issue, which is the disposal of plastic waste – see report linked here. Our support for chemical recycling stems from the view that it will be very hard to get the behavioral change needed to ramp up mechanical recycling quickly and to a level that will impact waste.

Our meetings over the last couple of weeks confirm several developments within the ESG investing world, all of which have been the focuses of our prior work. The first is a very significant step up in ESG oversight among most fund managers, with dedicated ESG teams at many companies scrutinizing sustainability reports and other releases, looking for red flags either from inconsistencies in reporting or from departures from the fund managers standards. Second, there remains a lack of real empirical analysis that allows for accurate comparisons between companies and this stems from the fuzzy reporting frameworks that we have today and the lack of clear and actionable guidance from regulators. As we have discussed several times, the huge inflows into ESG funds and the proportion of overall funds market that now has a “social impact” overlay could lead to real disruptions and some rapid valuation changes if and when the regulators provide tighter guidance on both corporate reporting and fund labeling.

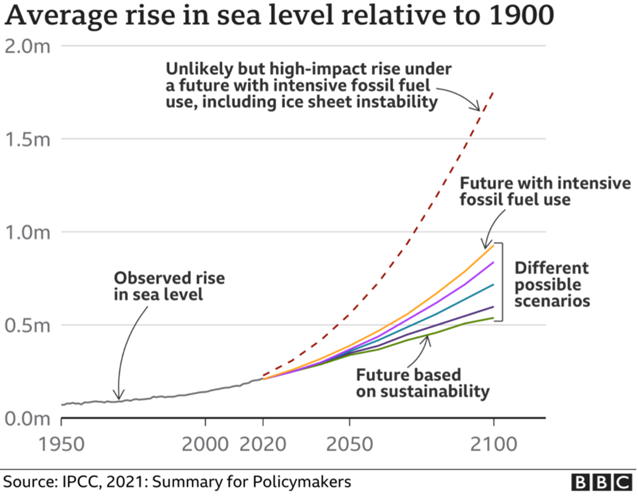

The IPCC (UN) report is all over every news outlet and its content and the ramifications of the analysis will be the core of our ESG and Climate piece tomorrow – in the Exhibit below we show a chart that was republished by the BBC which looks at projections around sea level increases. While the UN report has compelling academic and government backing and is certainly the most coordinated analysis on climate change, it is still littered with “most likely” and “more likely” comments, suggesting that the projections are still shrouded in uncertainty. There is a very good chart that shows “observed” climate change data over the last 50 years, and the ranges around the primary causality (human versus natural) conclusions are significant, suggesting that different models are telling very different stories, some less scary than others.

There are several things worthy of comment today. First, the math looks wrong in the Biden EV executive order, especially when combined with tighter fuel efficiency standards that are also on the table. The US consumes around 340 million gallons (approx. 8.1 million barrels) of gasoline a day and a reduction of 340,000 would only be a 1% reduction by 2030, even assuming growth in driving over the next 10 years we would expect the fuel standards and EV introduction to have a much more meaningful impact if successful. We will write more on this is our dedicated ESG and climate work.

The primary reason for the flurry of carbon capture related headlines in the US over the last few weeks – and our analysis shows a significant step up – is because it looks like this will be the one technology/route to lower carbon emissions that will get a real boost from the infrastructure bill. There is bipartisan support for CCS because the fossil fuel industry sees it as a way to stay in the game and the unions believe that it will create jobs. This combination should garner enough votes to push it into the bill and get it passed, although the details around how CCS would be supported remain unclear. The infrastructure bill has very few real sources of income in it to offset the very high costs – something we will discuss on Sunday – and consequently giving a bigger tax break, through the 45Q program would create an even larger funding gap than we have today. The value/cost dynamic has to rise to get the activity that everyone is looking for and maybe that could be achieved by overlaying a carbon credit onto the program. Anyone exporting to Europe and concerned about the CBAM extending to natural gas, NGLs, chemicals, and polymers would likely consider CCS if they were eligible for 45Q and could also claim an offset on their exported products to neutralize the CBAM tax/fee.

There are some serious players behind the CME offset futures trade highlighted in the linked headline. However, the press release does not provide enough information around how the offset is calculated and this will be critical if the futures product is to develop into a fully functional and fungible market. The agriculture-based offsets sound good and, in many cases, they can be robust in terms of the genuine contribution to lowering CO2 in the atmosphere – for example, where a new tree is planted and there would not have been a new tree without the direct action. But there remains a great deal of debate around whether an initiative is more positive than its alternative. Would a tree have grown naturally if the project was not there? Is the carbon footprint of any wetlands mitigation initiative taken into account when looking at the CO2 offset – same with tree planting? How do you risk adjust the CO2 value of a tree or other agriculture offset – what if the forest burns?

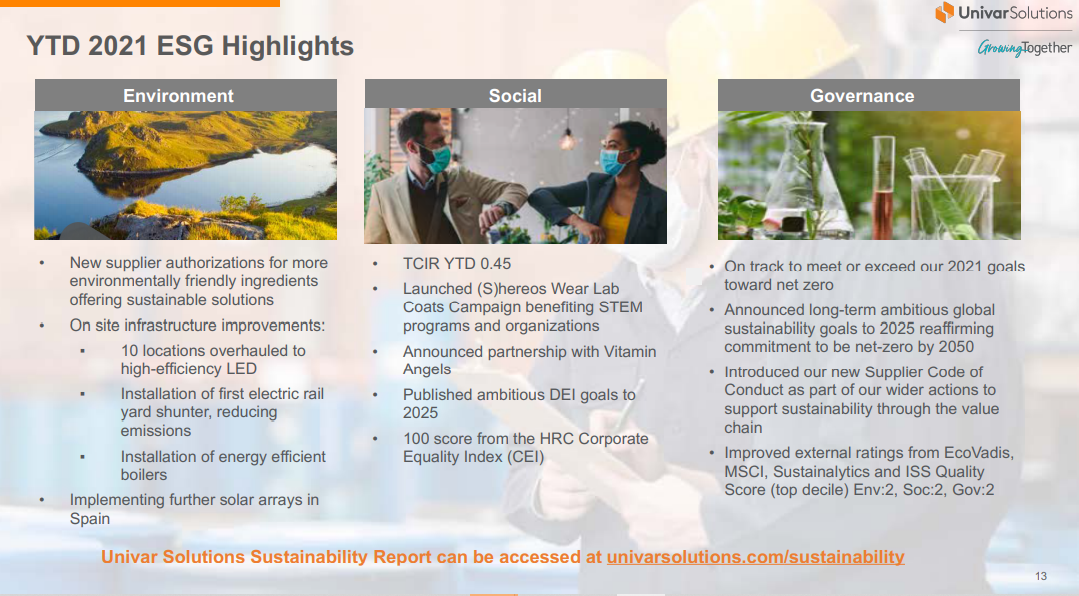

As the Univar and Eastman pictures show, it is now becoming almost mandatory to show your ESG badges in your quarterly earnings. The challenge for investors is the interpretation of the data presented. If there is no real consistency to the format, then it will be difficult to compare progress and this is one of the challenges that the SEC hopes to guide on by year-end – something we covered in last week’s ESG and Climate report.

Source: Eastman Chemical 2Q21 Earnings Release Presentation, August 2021

For example, the Univar claim that it has improved external ratings may be a function of better dialogue with the rating companies, or more consistent reporting of data and may not reflect any positive change at the company. Given the complexity of understanding environmental footprints at many of the industrial companies, including chemical manufacturing and distribution, it may not be much of a challenge to persuade any of the ESG rating agencies today that you are doing a better job than they have modeled, as they are unlikely to have the skills and experience to question you.

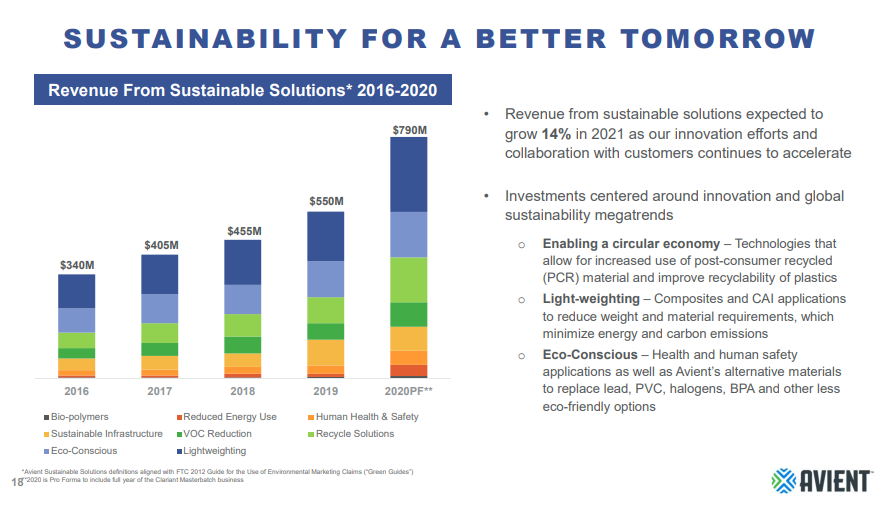

The Avient sustainability claims in the Exhibit below are in many cases in buckets where there is likely a degree of subjectivity around the assumptions and the company may be stretching the good news a bit. For example, on “lightweight” it would be interesting to know how much of their other business was cannibalized by customers choosing lightweighting options and also how much of the move was inevitable and whether the solution could have been provided by others – i.e. was it normal “course of business” competition? This is a good example of where a company is claiming something that should be questioned – it may be accurate but it may also be an overly rosy interpretation of data that can lead to different conclusions.