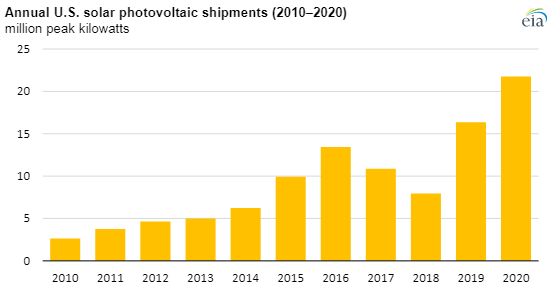

In our ESG and climate piece yesterday we discussed rising costs of climate-related actions, with a focus on some of the likely inflation in renewable power costs. The optimists are looking at the Exhibit below, and what were falling module costs through 2020, and concluding that solar installations can grow and that costs can still fall. While the module shipment growth in 2020 was impressive at 33%, some of the forecasts of what will be needed call for a much more dramatic rate of module growth than we saw in 2020.

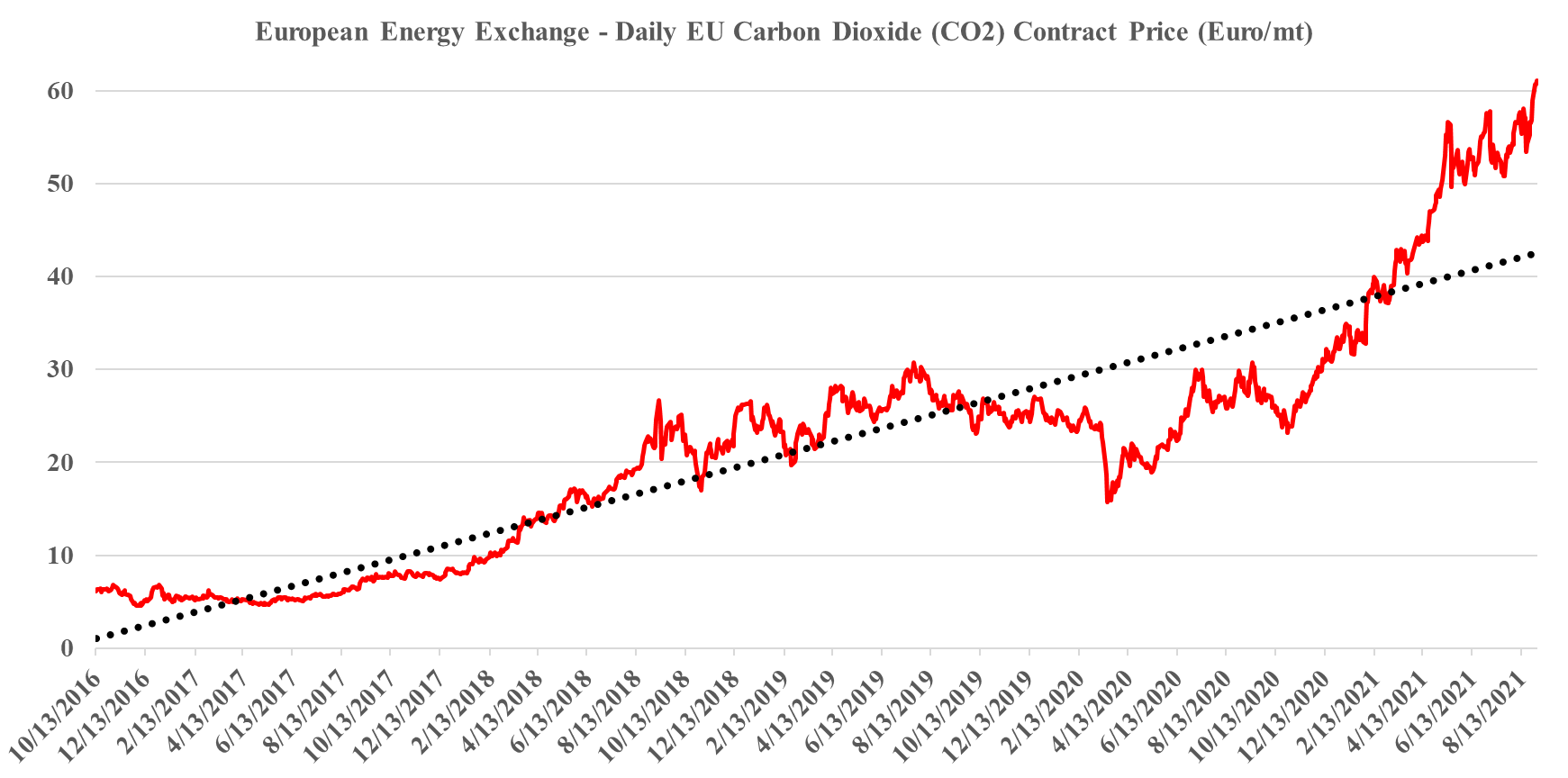

We have maintained all year that the strength in the European carbon price is sustainable and that it should go even higher and consequently, we are not surprised by this week’s move, even if much of the impetus is speculation. The European price is still not high enough to justify unsubsidized CCS or widespread renewable power investments to replace carbon-heavy energy sources, especially as renewable power costs rise. We estimate that a price in the €85-100 per metric ton range would be needed to stimulate investment, but because of the structure of the European market prices could overshoot this level meaningfully and be quite volatile until the level of abatement spending accelerates. When we start seeing investments in Europe to lower carbon that are not highly subsidized by local governments (in addition to the incentive of the carbon price) we will have a better guide around where 45Q needs to go in the US (or other mechanisms) to get investments rolling. Our analysis suggests that the US has some lower-cost abatement opportunities than Europe, especially on the CCS front, but not by much. For more on carbon costs and prices see today's ESG & Climate report.

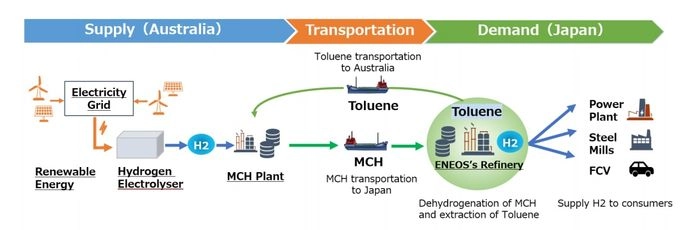

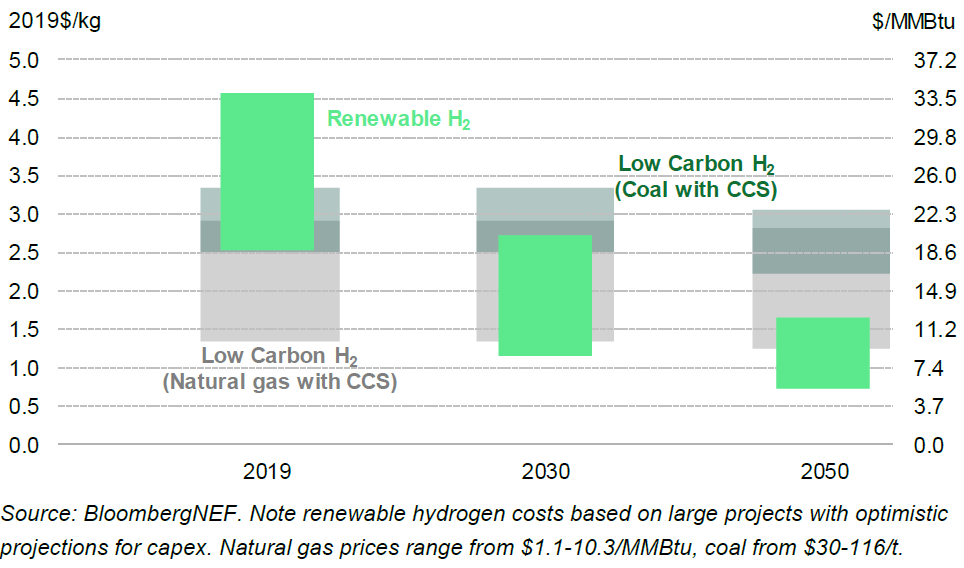

The exhibit below highlights one of the more significant constraints for green hydrogen, which is that the abundant low-cost power opportunities (strong wind and lots of sunshine) are often not where demand for hydrogen exists and the challenge is how to transport it. The problem with reacting it to make something else and then recovering it at the point of use or a distribution hub is that hydrogen is very light and you end up moving a lot of something else to get a little hydrogen. Air Products is looking at making ammonia in Saudi Arabia and shipping the liquid ammonia and the project below is looking at using toluene as a carrier in what appears to be a closed-loop with toluene moving one way and methylcyclohexane moving the other way. The liquid shipping would be cheap, but with the MCH route, only 5% of what you would be moving to Japan would be the green hydrogen. Using ammonia the green hydrogen content is slightly less than 18%, but you have to make the nitrogen on-site. The cost of making the nitrogen would be a function of the local cost of power and these remote locations should have very low-cost renewable power. In the example below, the opportunity is likely unique to the refinery structure and shipping opportunity and we doubt that it is easily replicated in a way that would be more economic than shipping ammonia or shipping compressed hydrogen itself.

Source: H2 Bulletin, August 2021

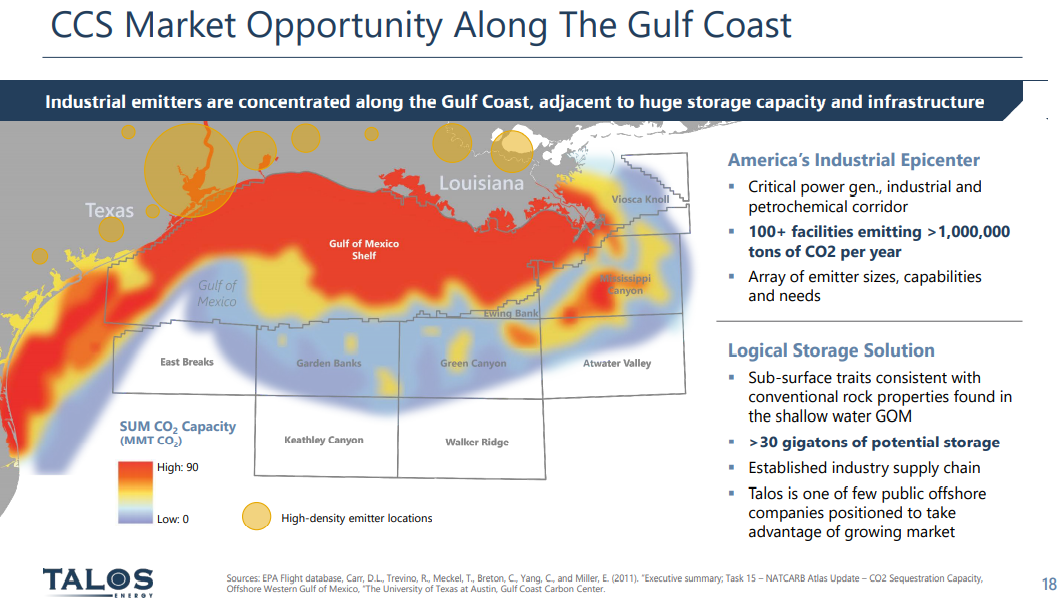

The Talos release and the map shown in the Exhibit below, highlight some of the potential for offshore CCS along the US Gulf Coast. We will likely see some of this developed over time, in our view, but the question of cost is important, not because the US Gulf is likely to be more expensive than some of the offshore locations that are proposed for Europe, but because the same offshore geology on the US Gulf exists onshore, and the onshore opportunities will likely be much lower cost. Given that one of the overriding concerns around carbon abatement is cost and how it will be paid for, who will pay for it ultimately, and what it means for the competitive landscape, finding the lowest cost solutions will be key. This is something that we have covered at length in our dedicated ESG and climate research. Building high-pressure pipelines is expensive, and high relative to the onshore cost of sequestration. Talos might find interest from CO2 suppliers but may be undercut by onshore projects – assuming these get the green light from regulators – not giving them the green light would likely be imposing further unnecessary costs on industry.

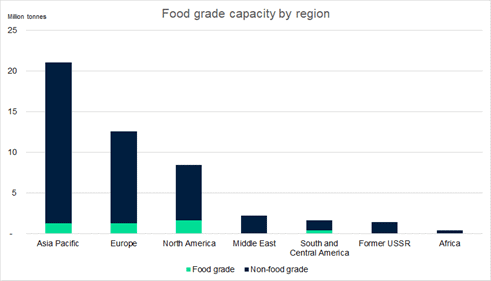

The exhibit below will come to many as a surprise, and it underlines one of the most significant challenges facing the recycling world. It is the food packagers who want the recycled content, but most food-grade polymer is not easily recycled (mechanically) once it has been in contact with food. Shrink-wrap for example is hard to collect and even harder to clean to a standard that is deemed safe and then hard to regrind because it is thin-film. This is where the polymer industry can really push the benefits of “advanced” chemical recycling as the process can take a mixed and not thoroughly cleaned stream of waste polymers with the recycling process itself (pyrolysis) destroying the contaminants and for the output that gets redirected back to ethylene units an additional shot at 1600-1700 Fahrenheit should remove any fears of contamination. You will not get the pound for pound recycle, but 35% is much better than the numbers suggested in the chart. Plus, in the process, you can destroy and reuse a great deal of plastic waste. See our ACC initiative write-up in yesterday’s ESG and Climate report.

The ACC goal of recovering 100% of packaging polymers is bold but likely necessary to show that its members are focused on a full solution, rather than some sort of halfway step. The goal is broken down as follows:

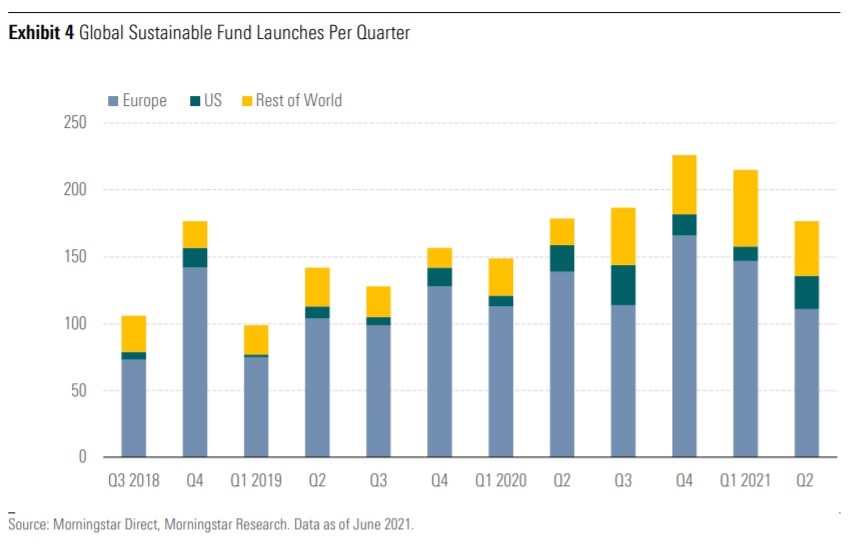

There is a significant increase in the number of commentators taking a swing at ESG investing and suggesting that it is neither effective nor in the best interest of investors as it likely puts them at risk of underperformance. The performance piece has largely been a moot point until now as the funds flowing into the ESG space have been high enough to ensure outperformance from a simple supply/demand perspective, see chart below. However, should the flow of funds slow and investments be judged on their own merits many fund managers are going to find that they own some egregiously expensive stocks with fundamentals that do not support the valuation. If this then leads to a rotation out of a sub-set of names, the future outperformance of the class is far from guaranteed.

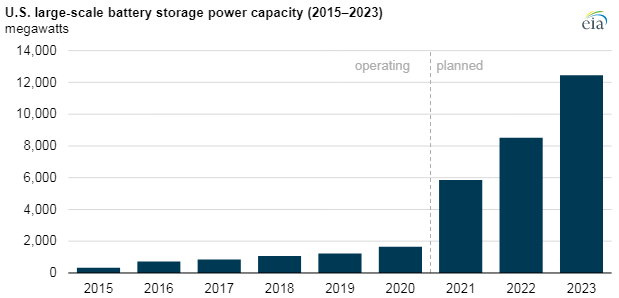

If we look at the battery storage projects highlighted in today's daily report and in the Exhibit below and then read some of the raw material inflationary concerns around batteries, we conclude that batteries will likely not end up dominating the power storage market. Both hydrogen and hydraulic-based storage are likely to be competitive if the battery costs do not come down. Note that storage batteries can afford to compromise on technology as they do not need leading-edge density – weight is not an issue for something that is not going to move. Even so, with battery demand expected to grow rapidly for EVs, it is not hard to see a scenario where other means of fixed location energy storage are more attractive.

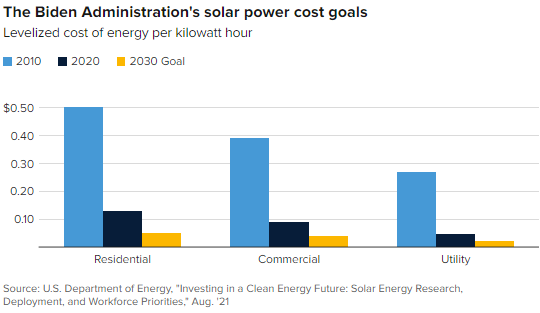

We are back on one of our pet topics today which is the reasonableness around some of the assumptions around the future cost of renewable power. We reference, work done by the US Department of Energy in the Exhibit below, and see two potential pitfalls with the assumptions around continuous improvement in solar, wind, and hydrogen costs, although there is a slight twist for hydrogen. The first is around the dynamics of learning curves. As the exhibit shows, in the early stages of any product development, there are huge leaps in cost improvements, driven by scale, better know-how, more efficient manufacturing, and in the case of solar power, both better processes for installation and some technology improvements. However, as you drive costs lower, the cost of raw materials becomes a much larger component of overall costs, and your ability to lower costs further can be overwhelmed by moves in material costs. Any inability to pass on the costs will result in economics that do not justify additional capital and you find yourselves in a commodity cycle. This is something that we have seen in basic polymers for decades, and no buyer of polyethylene today can claim that they are benefiting from a learning curve improvement. Closer to home for solar, we are seeing the same issue today in semiconductors – not enough margin to invest as everyone has been trying to push costs lower. The expectation in the DOE study and highlighted in the CNBC take on the study below is that annual solar installations in the US need to rise by 3-4X to meet some of the renewable power goals the Biden Administration is looking for by 2030, while similar growth is expected in other markets – the solar panel and other component makers have to be making good money to achieve this.

It is hard to ignore the number of headlines on hydrogen initiatives, today, highlighted in our ESG and climate report, as well as the acceleration in project announcements over the last several months. In the 80s in the UK, it was trendy to drive a VW Golf GTI – everyone had to have one – hydrogen has the same feel today – everyone has to have a project. The projects vary and fall into a handful of categories: