As we discussed in yesterday’s ESG and Climate report, the SEC has some challenges ahead, not just because there are high hopes that it will start mandating a change in terms of disclosure accuracy and consistency, as well as fund definition, but also because, as yet, it does not have the mandate to do so. All eyes are on the regional regulators, in the US, Europe, and other countries to police what is the wild west of reporting. The E piece of ESG is the major challenge and it is where corporates and fund managers alike are dealing with issues and measures that are likely very different company by company within a sector, let alone between the sectors themselves – it is far more complex and harder to analyze than, for example, board diversity.

There has been a lot of press over the last couple of months around carbon offsets – not least because of Mark Carney’s efforts to legitimize the idea. Mr. Carney’s focus is to create a robust trading platform for the buying and selling of legitimate offsets so that a carbon market can operate efficiently. He believes that without accurate and realistic carbon values, and the ability to buy and sell them, the capital markets around emission reduction will be inefficient and that less money will be attracted into the area. On this, he is probably correct, but in our view, the carbon offset markets have a long way to go.

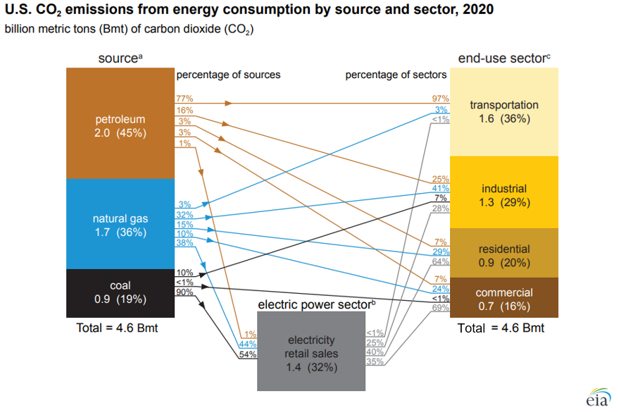

We are increasingly concerned that the US will remain a laggard concerning climate change initiatives given the major challenges of moving to the next steps and the bifurcated congressional views. The emissions reductions that the US has seen over the last 10 years have been more happenstance than planning, with the abundance of natural gas following the shale boom of the last decade creating economic reasons to replace coal-fired power with natural gas rather than environmental reasons. Lower costs for wind and solar power and focused industrial demand for that clean power have been the bigger driver of clean power investments. In the chart below, the decline in emission from the power sector is evident and it should continue. The diagram below shows sources and uses for US emissions in 2020, but the accompanying write-up talks about the step down in emissions overall in 2020. Except for the continuing electric power transition, most of the other 2020 declines are COVID-related and are expected to rebound in the near term, especially transport. The market share gains of EVs are not significant enough yet to make a difference. See more in today's daily report.

The analysis behind the projections in Exhibit 6 in today's daily report, likely makes more assumptions than just the level of reusable plastics. To get the waste reduction projected, there will still need to be a step up in collection, sorting and recycling and it will all need to work to get the results desired. We are still concerned that these “high recycle” plans ask too much of an unwilling public, a slow to move average packager, and underfunded municipalities.

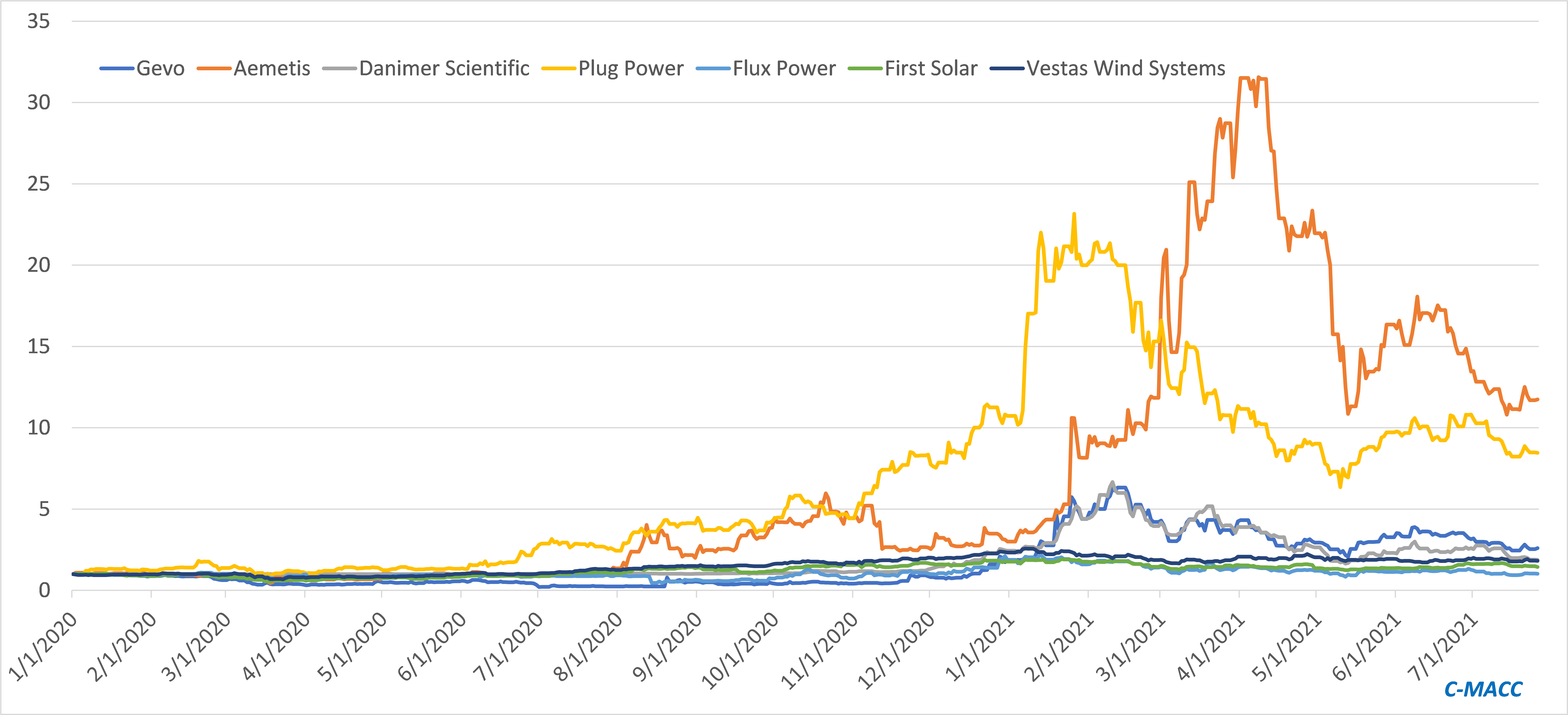

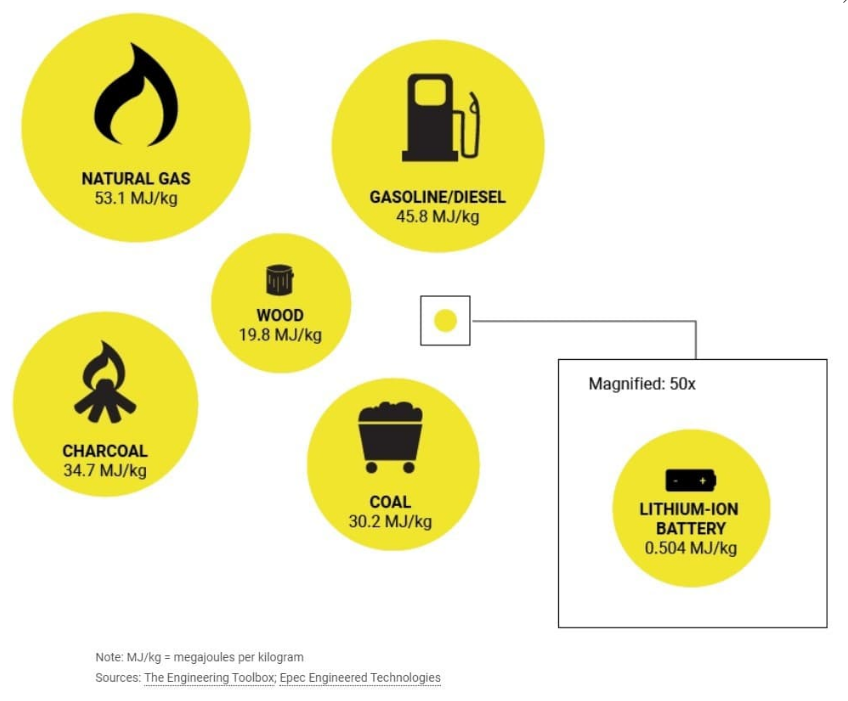

The decarbonization of the airline industry remains a hot topic. The energy density issue shown in the exhibit below is a correct assessment of why commercial aviation faces a challenge to transition to electric power. Not only is the energy density too low - which restricts weight/range - but electric power can only turn things, and propellor-based flying has speed limitations relative to jets. The announcements from the airlines to date on electric power have focused on low capacity short-haul opportunities. With this in mind and as noted in the article headlining of the exhibit below, electric power is not the only decarbonizing option for airlines. Hydrogen is the very long-term future - Airbus is saying not before 2050, but in the meantime, the push should be for low carbon or carbon-neutral biofuels. These are essentially plug-in fuels that are identical to current aviation fuel but made either from waste oils or from carbohydrates. Many of the oil majors are working on waste oil or vegetable oil-based processes, especially in California where the LCFS credit helps pay for the conversion, and companies like Gevo and Aemetis are working on carbohydrate-based routes through fermentation. If the carbohydrate, corn in the case of Gevo, is sourced from sustainable agriculture the carbon values of the fuel can be very low and potentially zero or negative through the life cycle. The airlines are going to have to pay up for the low carbon fuel if they want to bid the fuel away from the high credit markets like California diesel and gasoline, but this route could decarbonize the airlines significantly and relatively quickly with the right pricing structure and enough capital.

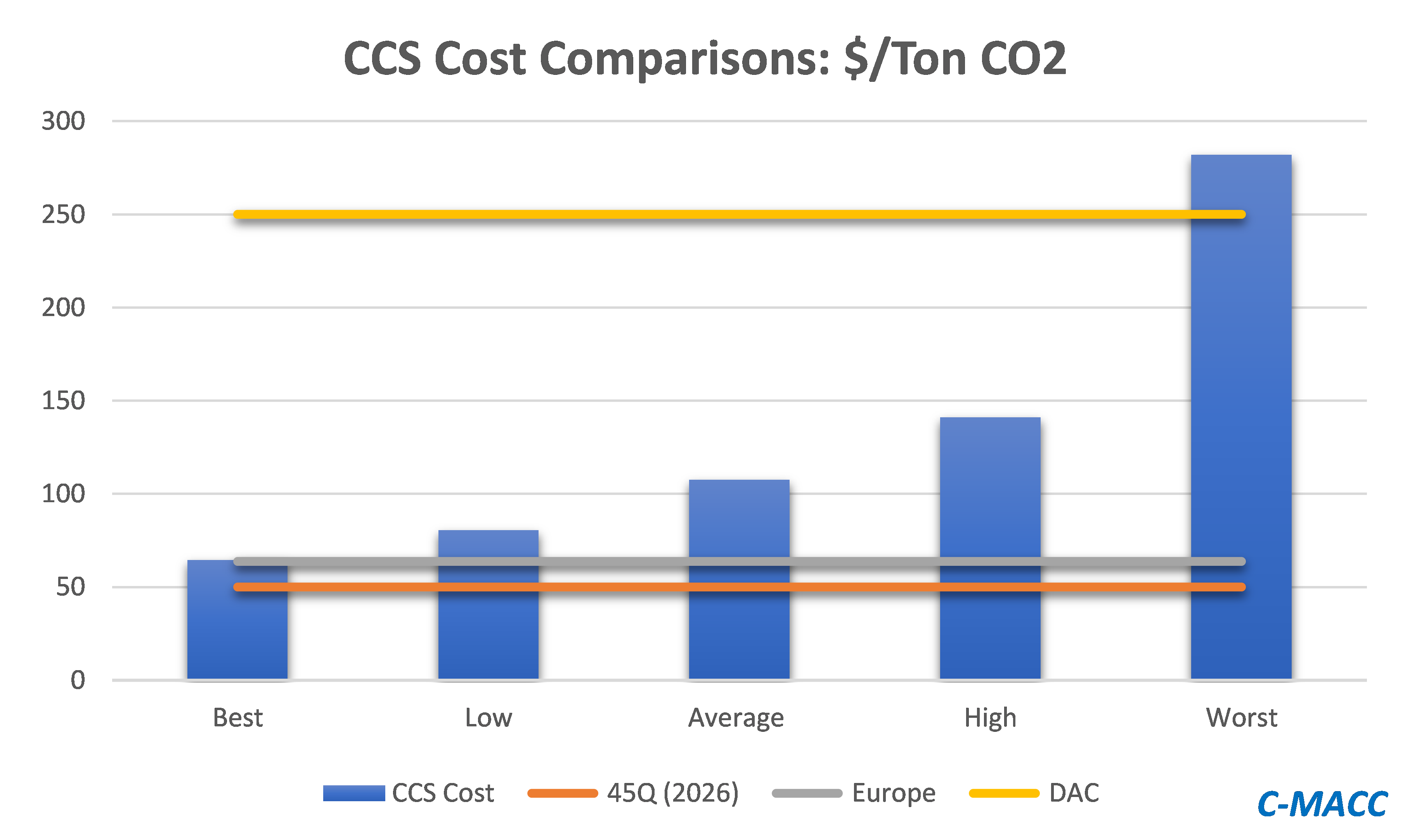

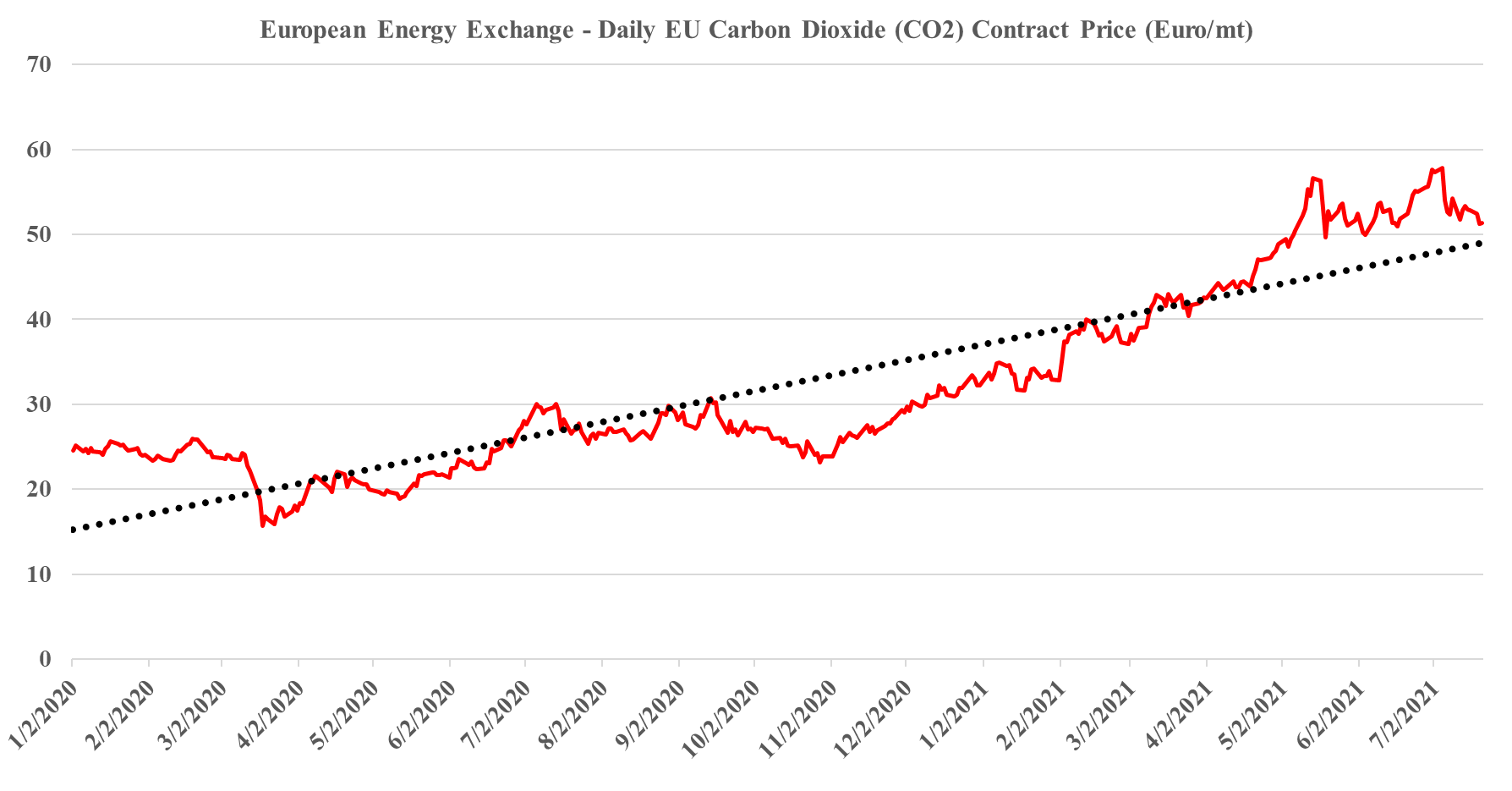

In our ESG and climate piece today we focus on Carbon Capture and Sequestration (CCS) and the likely very steep cost curve between the mega projects and those less fortunate. But as we discuss CCS, we should not forget that the World is still not convinced about CCS as part of the solution set for carbon abatement, as the headline linked discusses. The naysayers are focused on the lifeline that CCS offers to the fossil fuel industry, but always fail to offer an economic rationale for the quick elimination of fossil fuels and their replacement by renewables. Few of the proponents of CCS see it as an alternative to a long term path to alternative means of abatement, but all recognize that relying on renewable power investments will likely leave the World with a much larger CO2 footprint from 2030 to 2050 than what could be achievable with CCS – note that the 45Q incentive in the US has a finite lifespan as there is an expectation that eventually CCS will be unnecessary because of fossil fuel replacement. Chevron has not helped the CCS proponents with its missed targets in Australia as it adds fuel to the argument that CCS has not lived up to its potential. While the European carbon price trend has stalled in recent weeks – chart below – the trend remains distinct and it would be foolhardy to ignore the likelihood of prices rising to a level that makes CCS attractive – especially for the mega-projects.

The clear advantage of chemical recycling – as seen in the linked Agilyx headline – is that there are no issues with product cleanliness, etc., to get the material back into the cycle. As the polymers are essentially destroyed in the pyrolysis process and then reused as a feedstock in the traditional polymer production process, the rigors of sorting and cleaning for a mechanical recycling alternative are not needed. From a food contact perspective, chemical recycling is the easiest way to close the loop. What we are seeing in the headlines, however, is still “proof of concept” stuff and there remain plenty of challenges with logistics and/or proof of custody with the feedstocks that are flowing back to the ethylene unit, as well as how much recycling credit is appropriate, given that roughly half of the recycled feedstock does not end up as a polymer.

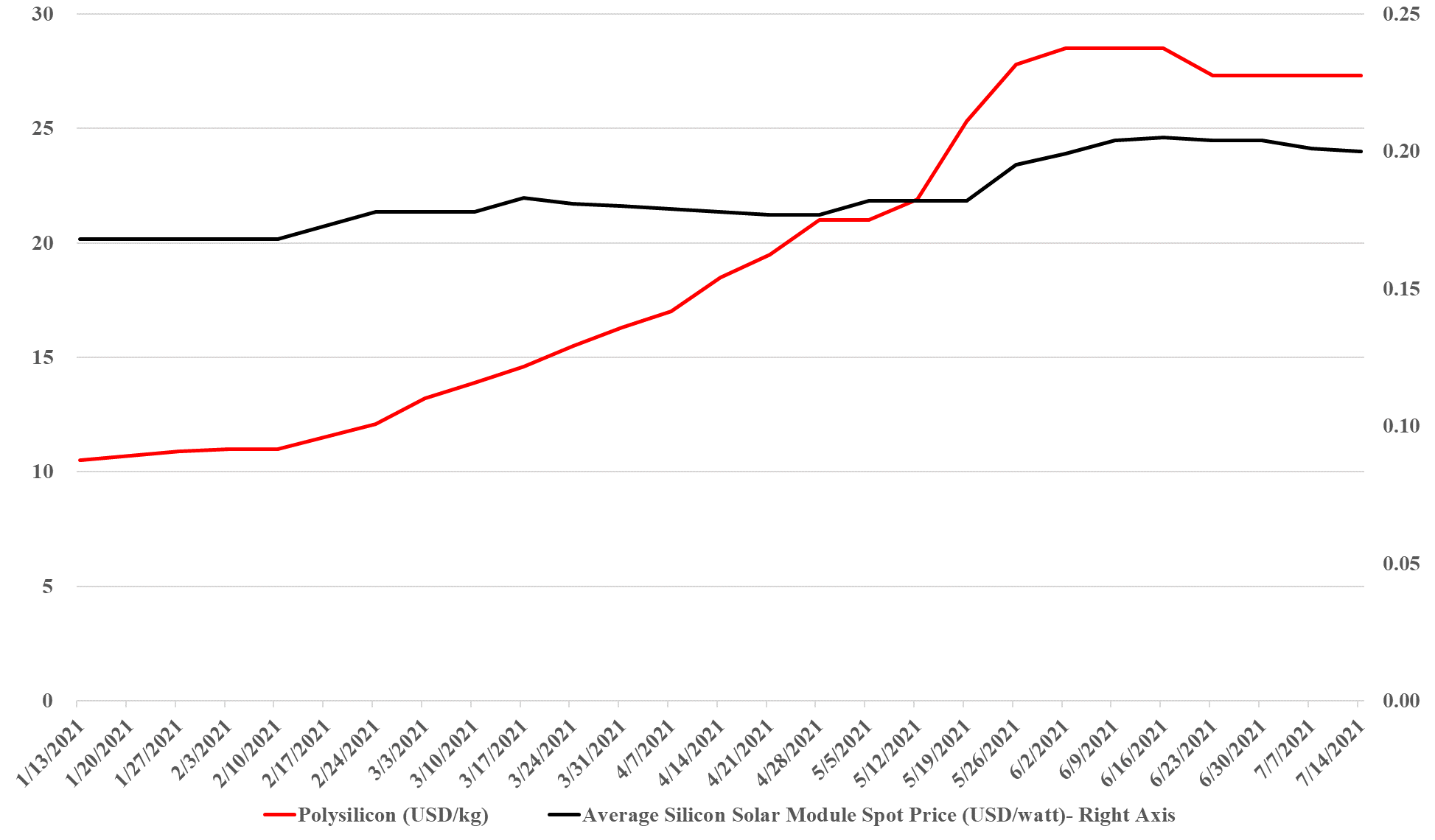

While the escalation in solar panel material costs has plateaued over the last couple of months, the increase has been enough already to reverse the decline in solar module pricing as we have noted previously (see charts below). While the increase in module pricing is not that significant there are three points to note:

The ACC call for 30% recycling of plastics by 2030 emphasizes chemical recycling, and in our ESG and Climate report yesterday we talked about an alternate path for plastics, one that focuses on reducing waste rather than increasing recycling. The product standardization and consumer and municipality waste collection and sorting rigor that would be needed to maximize mechanical recycling are significantly harder to achieve than the changes that would be needed to dramatically increase chemical recycling – i.e. it may be easier and less expensive to get to zero waste than it is to get to maximum recycling. Maybe we are thinking about this wrong, but to change tacks from here the industry would need to demonstrate that plastic waste can be removed, at scale, and then convince the plastic buyers that the path is better. We discuss the possibility in more depth in yesterday’s report.

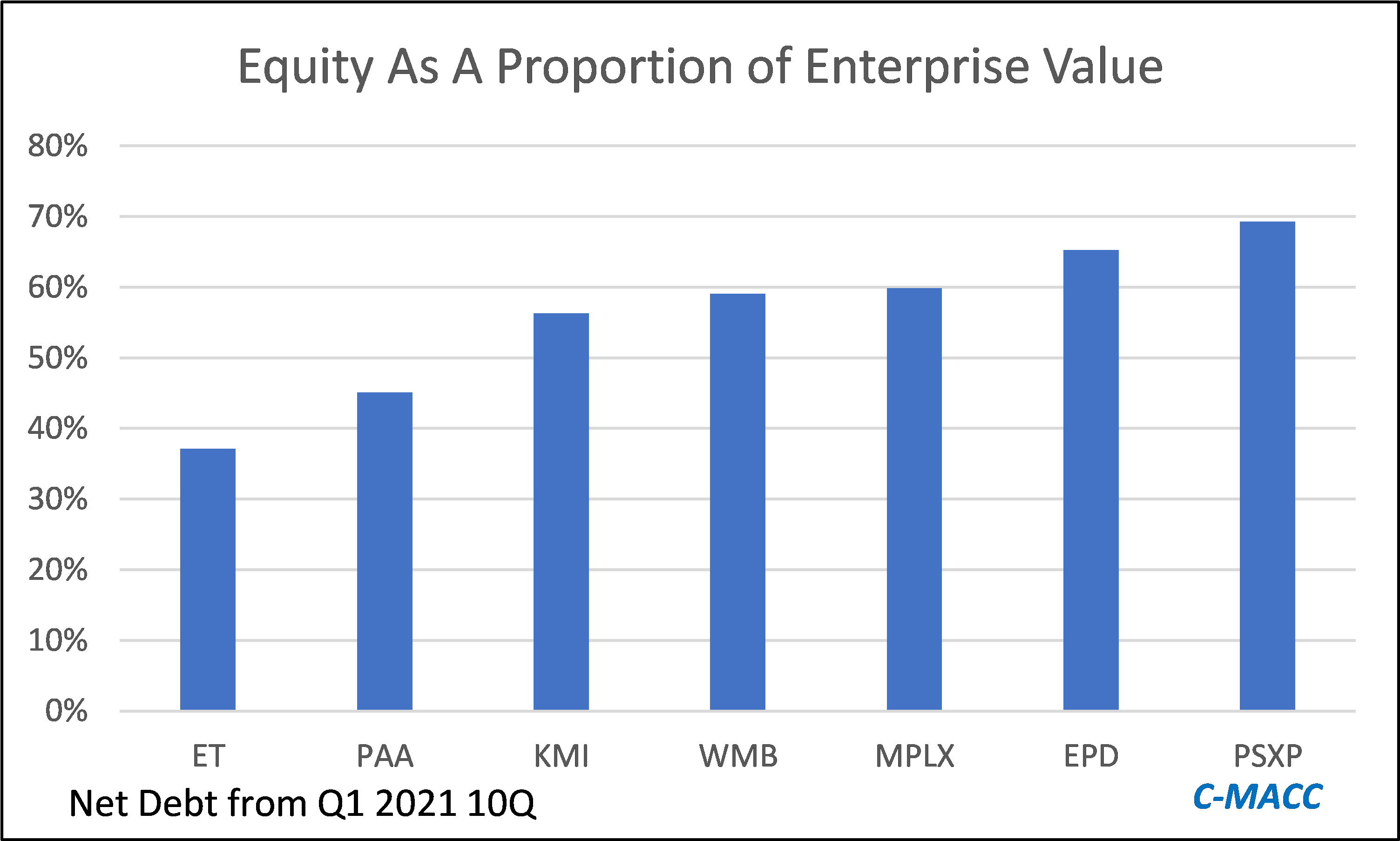

The MLP headline linked covers a subject that we have addressed in prior work as it looks at the ESG related opportunities for pipelines, not just because pipelines are the lowest cost and lowest carbon footprint means of moving large scale existing gases and liquids around the US, but because of their future potential role moving CO2 and hydrogen. Because the opportunities to grow earnings in the cleaner fuels space will likely be a function of both opportunity (whether you already have some infrastructure that can be repurposed and whether you are in the right locations) and strategy (whether you seize the opportunities as they arise and think a little outside the box), how to play the opportunity from a stock perspective is more challenging as there will be winners and losers. We suggest one of two paths – either buy a basket of the pipeline names or focus on the idea of a positive sector re-rating, in which case you want to own the company with the highest equity leverage to any EV/EBITDA re-rating, which among the large and liquid names would be Energy Transfer – Exhibit below. For more on this see today's ESG report.