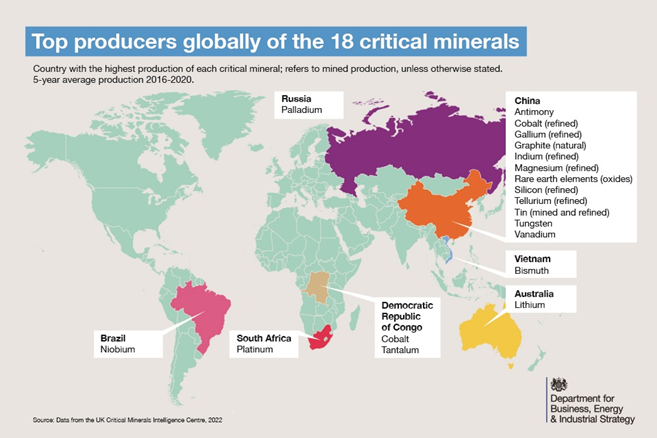

We are seeing more focus on supply chains as they relate to the energy transition. Some European countries are realizing what we have noted in prior research - EU Energy Policy: Swapping A Bad Supplier For Something Worse? - switching to an aggressive focus on renewable energy may reduce your energy exposure to Russia but it currently doubles down on your exposure to China. It is very easy to look at the scale of the problem – the share that China has in critical metals, as shown below – the share that China has of solar modules – etc., and conclude that it is too hard, especially in Europe where you will find an environmental lobby trying to stop you doing anything industrial. But the net effect is severe reliance on China. One advantage that the UK now has with its exit from the EU is more industrial freedom and the country could benefit from the right industrial policies that would attract broader energy transition investment. In our ESG and Climate report this week we talked about the U.S. desire to “friend-shore” rather than re-shore because of local investment challenges in the U.S. as a consequence of some of the political issues. The UK could benefit from becoming an industrial partner with the U.S. for some critical materials.

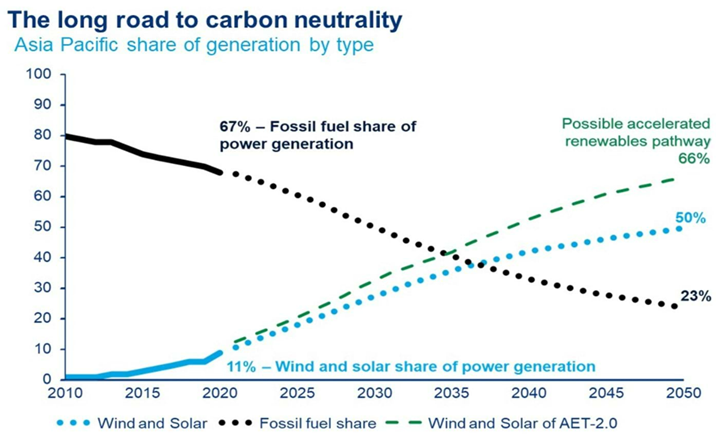

In the exhibit below, we see another chart that we find unhelpful when looking at the path to net-zero or something close. It is not an either/or game with fossil fuels and renewables. Those promoting this idea are setting impossible goals for the renewable industries, which will keep severe upward pressure on all energy costs. Wood Mackenzie may not mean what is implied in the chart below but taken at face value it suggests that more pressure will be placed on an underfunded materials market to supply an underfunded renewable power market, in which any opportunity to use decarbonized fossil fuels will be frowned upon. It would be good to see an analysis of how much global power could be generated from decarbonized natural gas and how much pressure that would take off the renewable industries.

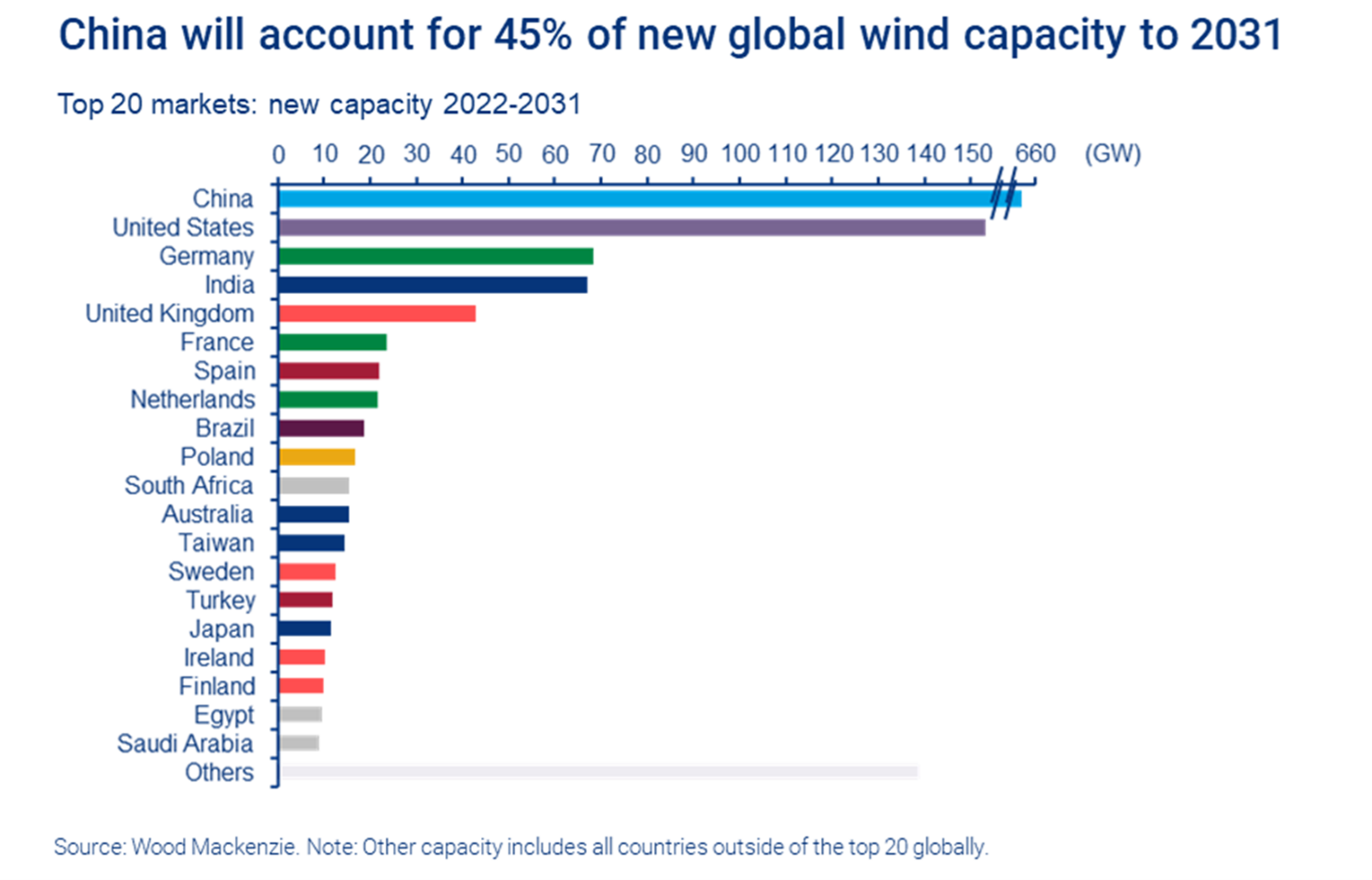

In our ESG and Climate report tomorrow we are focusing on the wind industry and specifically the problems that Siemens Gamesa is facing with execution, costs, and logistics. The estimates for China and the rest of the world in the chart below assume a significant step-up in the rate of installation, and in 2022 we are seeing an industry that is struggling with that. Siemens Gamesa is having problems with its new platform, which had been intended to deliver projects more cheaply from an installed cost basis and an operating costs basis and is perhaps an illustration of what can happen when you are trying to move too quickly – partly because your customers are demanding it. Operational problems at Siemens Gamesa have been compounded by logistic challenges and raw material price and availability, such that current expectations are for the company to break even at an EBITDA level in 2022. This is another great example of the policy and investor disconnects that we see in several aspects of energy transition – we are encouraging investment in front line capacity, but not in the materials and feedstocks needed to feed the front line – metals, natural gas, crops. See our recent body of ESG and Climate work for more on this. These subjects are at the heart of many of the private engagements that we have with several clients in this space.

In our ESG and Climate report tomorrow, we will focus on SAF from a carbon intensity perspective. The Colonial pipeline initiative was inevitable given the demand for jet fuel at the East Coast airports. Still, we would not expect much volume to move in the near term for several reasons. First, there is not that much to move, and second, California can still pay more because of the LCFS credit. The Biden administration is planning to introduce a broad SAF credit which would help encourage use outside California, but this would also need to stimulate production as the volumes are still small and much smaller than the airlines would want – even the projection of volumes by bodies like the IEA fall well short of potential airline demand by 2030 and 2040. This is an investable theme, in our view, and we will discuss it in more detail tomorrow.

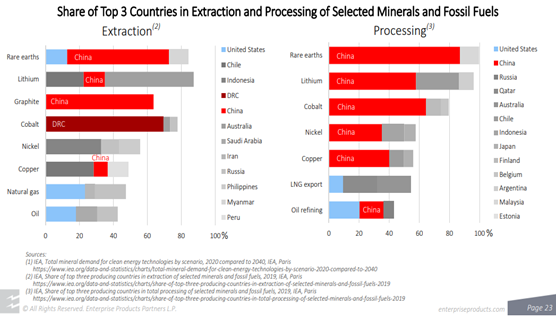

While longer-term use of oil and gas products is in Enterprise Products' best interest, it is nice to see someone else pushing the point that we have been making for more than a year – that there is not enough material out there, in the right locations, to meet the suggested clean energy goals. It is important that this becomes better understood and accepted by a broader group than just Enterprise and C-MACC, as we will not get the needed tack in strategy, priorities, and incentives if there is a broad reliance on renewable targets that will not be met – we focus on the IPCC report in tomorrow’s ESG and Climate report.

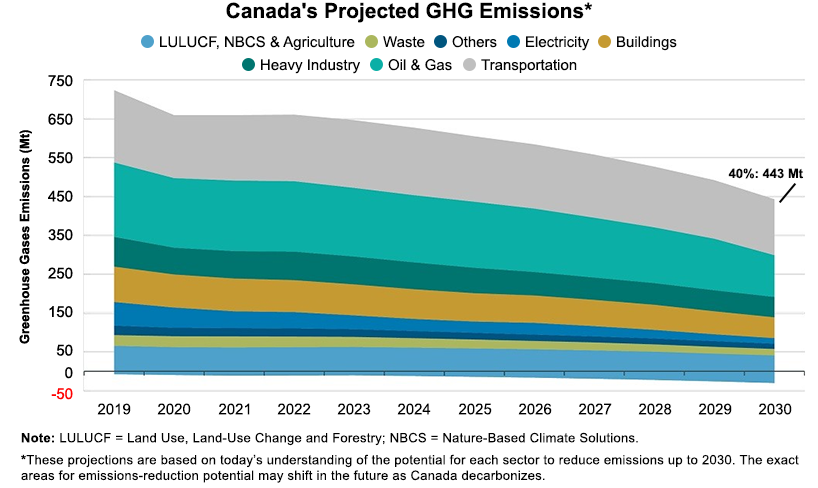

The Canadian targets highlighted below are ambitious and will likely not happen without the significant CCS projects planned for Alberta. The CCS opportunity will drive down energy and chemical (heavy industry) based emissions meaningfully and could also be the basis for new power generation capacity to allow the transport industry reductions that the country is looking for – either through EVs or hydrogen-based transport.

We tend to focus on recycling conventional plastic waste, but there are growing initiatives to look at the longer life cycle of durables and while this has mostly been focused on the automotive space, it is interesting to see the building industry looking at building life cycles. Many of the alternative use mechanical recycling initiatives are directed toward substituting building products such as concrete and wood and while this will help the construction sustainability story, the end of life cycle issue is less clear. The majority of commercial real-estate emissions are associated with operations (around 70%) and this is the greater focus for owners today, but the life cycle question is increasingly important for building tenants. In the UK for example there are redevelopment projects proactively advertising how much of the original building will be retained – i.e. not demolished and landfilled. Ultimately this might lead to lower demand for commercial building products where developers are looking at existing buildings, but it will not impact new greenfield builds unless you get a steep increase in recycled polymer use. The offset would likely be concrete as this is the high carbon footprint material that most are targeting. See more in today's ESG and Climate Report.

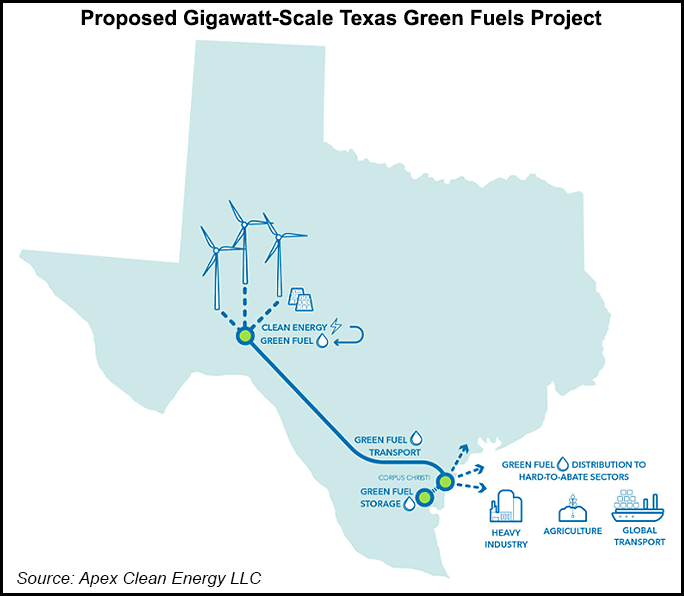

The Texas hydrogen hub is getting a lot of press and we also cover the idea in our ESG and Climate report today. We see this as not a lot more than intent today and would be surprised if any part of the project would be up and running, assuming it gets built at all, before the end of the decade. Green hydrogen economics do not (yet) make sense and some considerable efficiency learning curves need to emerge before any project could expect to make economic sense without significant subsidy. We have talked at length about the inflationary effects of material shortages and this is the core topic of our ESG report again today, where we suggest that a global recession may be the best thing for the renewable industry as it would slow other sectors' demand for critical materials. But the other wild card is renewable power demand, and how many industrial and materials companies along the Gulf Coast have their eyes on the same renewable power capacity to meet 2030 emission reduction goals. No one must buy renewable power today, because no one has 2022 emission goals. So, renewable power demand is likely understated and it is why the premium to buy renewable power in Texas today is quite low. Fast forward to 2030 – when promises have been made – and we will likely see demand spike and prices rise relative to conventionally generated power. This would materially impact the economics of the green hydrogen hub in Texas even if the electrolyzer costs could be reduced. Given the abundant pore space both onshore and offshore, blue hydrogen makes much more economic sense for Houston.

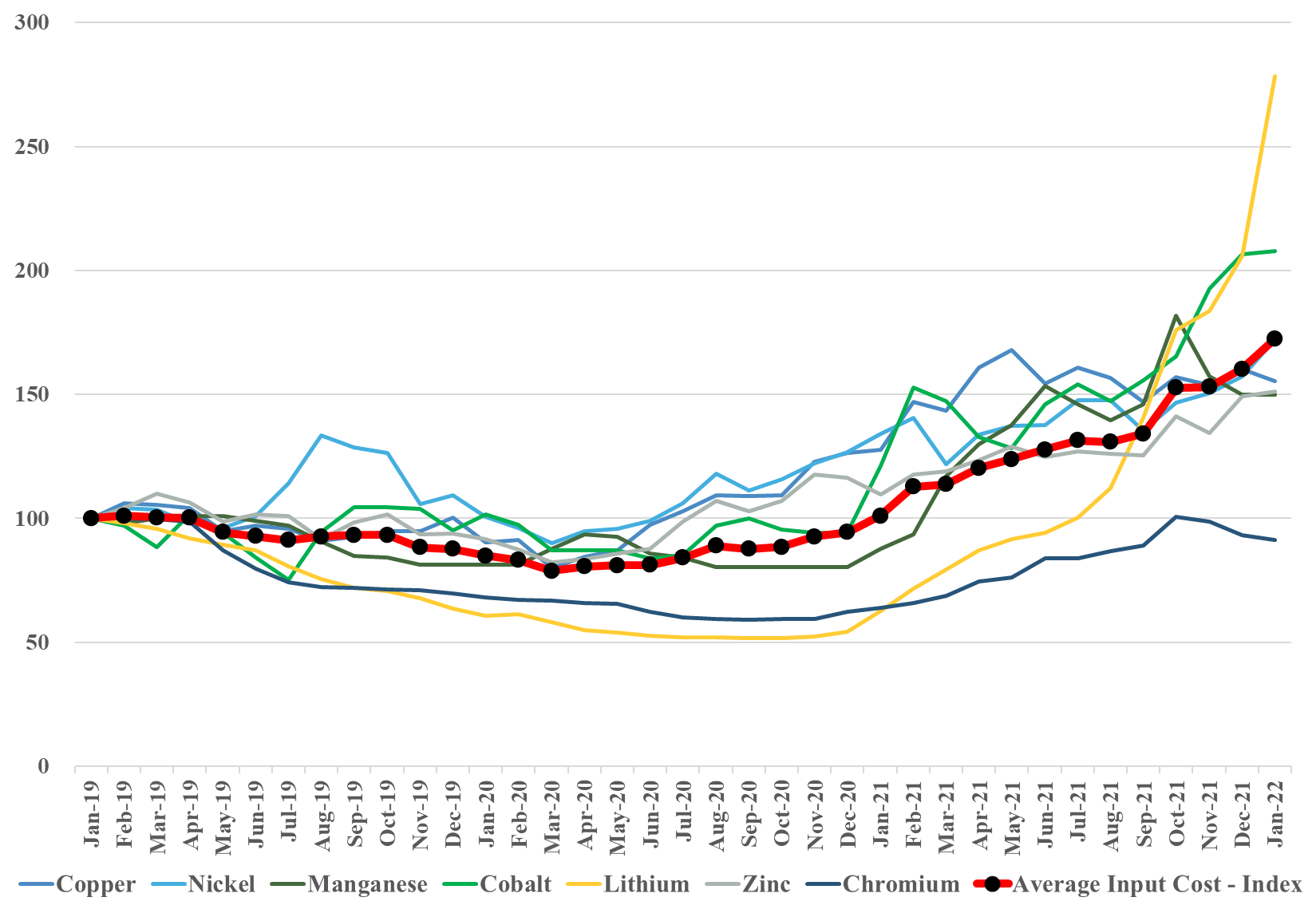

As the chart below shows, the demand, real and speculative, for lithium continues to drive prices materially higher. As new EV models prepare to launch this year and new battery facilities come online there is an inevitable supply chain impact to build inventory, whether it is the battery facilities building an inventory of lithium and other components or the automakers building an inventory of batteries. This will inflate lithium and other critical material demand relative to the vehicle output and this may be driving some of the demand panic for lithium. However, this dynamic is unlikely to be transitory in the near term, as there is a long wave of new EV capacity coming online, all of which will drive some incremental working capital build. We still believe that supply growth for lithium is very high and that the market could flip from famine to feast and back again quite quickly and frequently over the next few years although maybe not in 2022. Also see today's daily report and last week's ESG and Climate report for more on this topic.

2022 is the year in which the rubber will need to meet the road for many of the chemical and other material and industrial companies who have made 2030 emission pledges. In the Dow release yesterday, the company used the call as an opportunity to remind investors about the Canada investment and tie that into the 2030 emission goals. We note LyondellBasell’s 30% emission reduction goal by 2030 and like others, LyondellBasell will not be able to get there without substantial investment. LyondellBasell and others do not necessarily have to spend in 2022 (neither does Dow), but unless there are some concrete plans by the end of the year stakeholders will likely start to question whether the emission goals are real. We suspect that most companies are trying to work out whether investments in hydrogen (likely blue hydrogen because of the volumes needed) are a better solution than trying to capture CO2 from a natural gas furnace. Any large hydrogen investment with associated CCS will take 5-6 years from concept to production. Like Dow, we would expect others to focus emission-reduction investments in countries/states that have a clear value on CO2. See today's daily report for more.