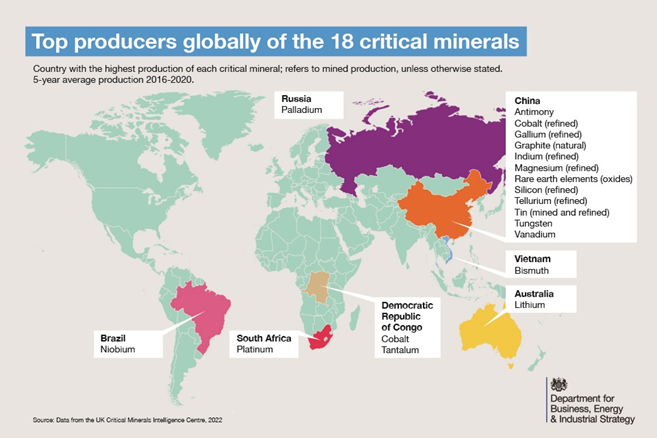

We are seeing more focus on supply chains as they relate to the energy transition. Some European countries are realizing what we have noted in prior research - EU Energy Policy: Swapping A Bad Supplier For Something Worse? - switching to an aggressive focus on renewable energy may reduce your energy exposure to Russia but it currently doubles down on your exposure to China. It is very easy to look at the scale of the problem – the share that China has in critical metals, as shown below – the share that China has of solar modules – etc., and conclude that it is too hard, especially in Europe where you will find an environmental lobby trying to stop you doing anything industrial. But the net effect is severe reliance on China. One advantage that the UK now has with its exit from the EU is more industrial freedom and the country could benefit from the right industrial policies that would attract broader energy transition investment. In our ESG and Climate report this week we talked about the U.S. desire to “friend-shore” rather than re-shore because of local investment challenges in the U.S. as a consequence of some of the political issues. The UK could benefit from becoming an industrial partner with the U.S. for some critical materials.

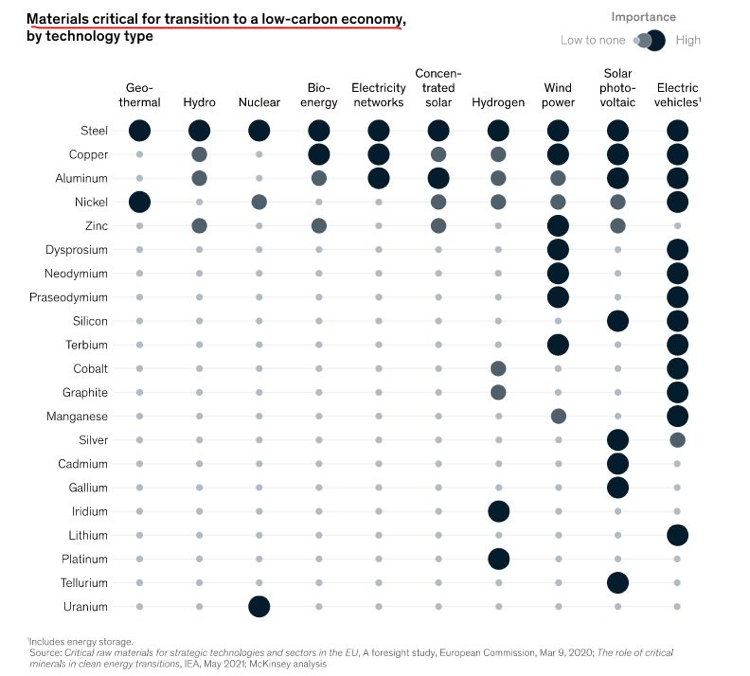

The materials chart in the exhibit below from today's daily report, is worth noting as it highlights all of the materials that are needed to advance the production of equipment required to drive renewable power production and demand. We would make one change to the chart in that lithium should also be added to the wind and solar categories to account for storage that needs to be built, although this could be done through hydrogen production or hydraulically, depending on location. One of our primary concerns concerning renewable power projections is the availability of some of these materials and we have written about the topic at length – most comprehensively in - 2022 – Policy Key, But Inflation Will Distract – Maybe Beneficially.

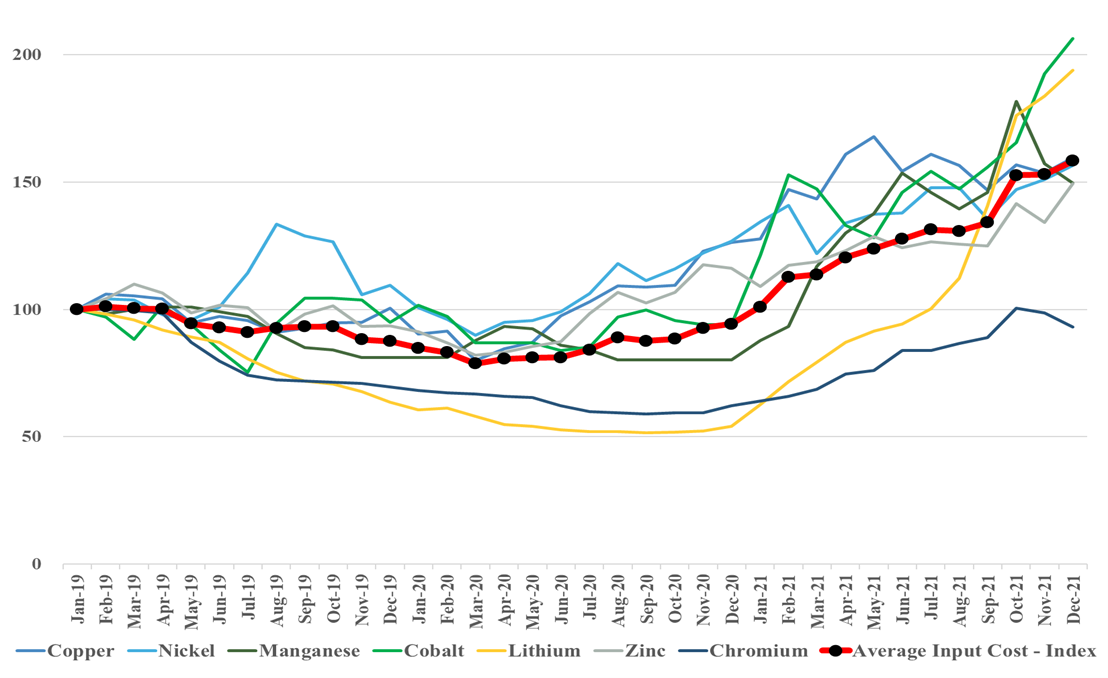

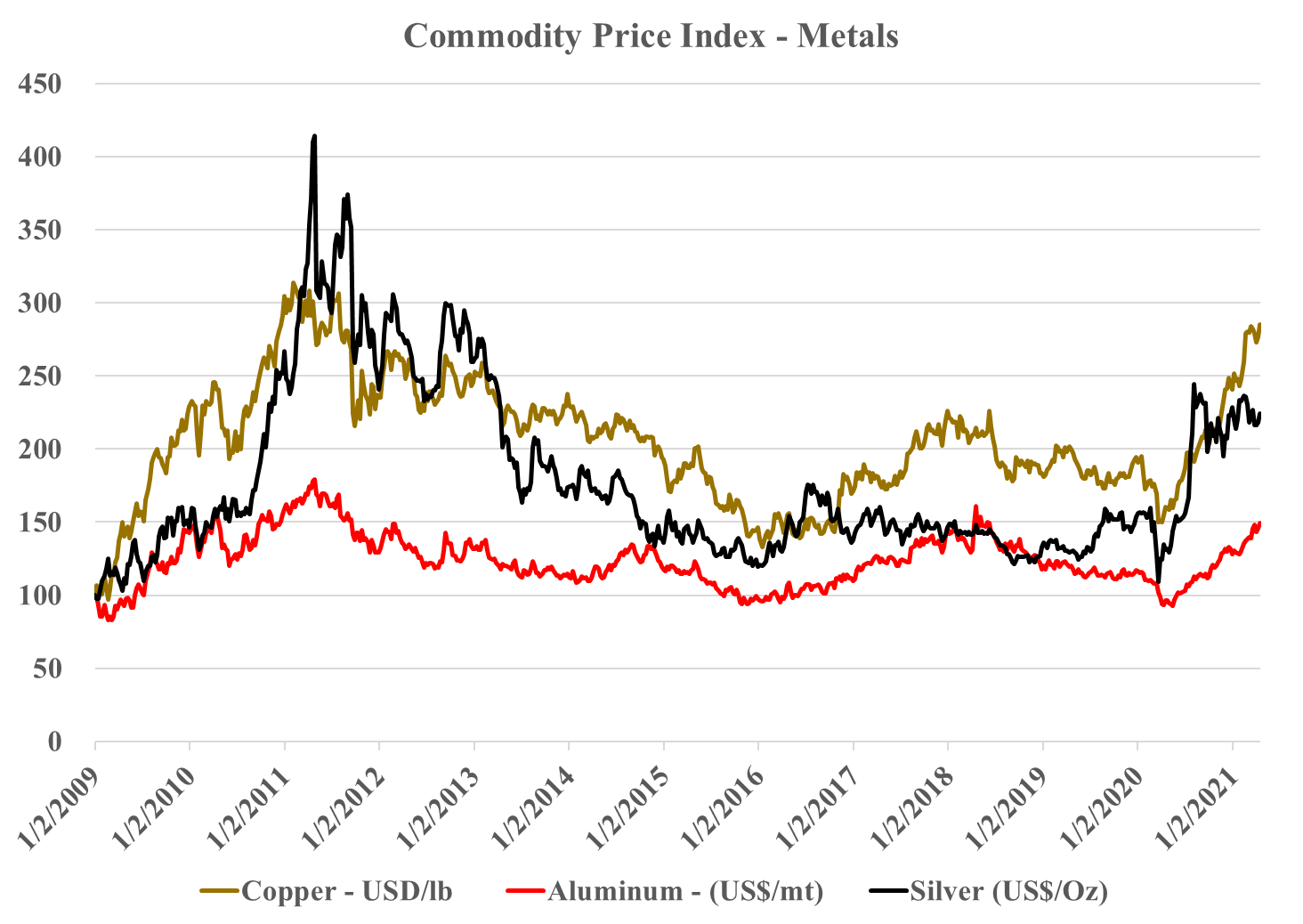

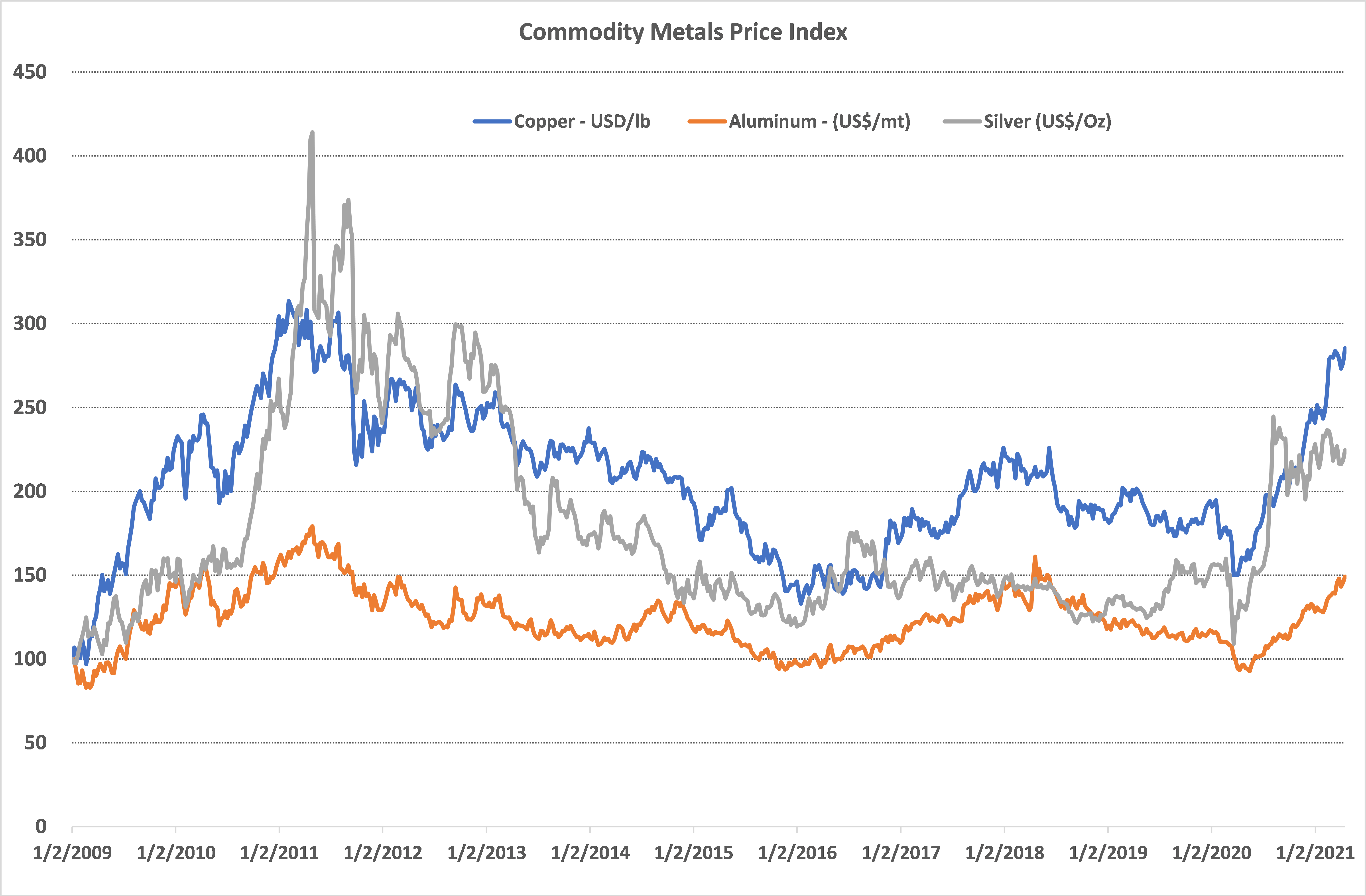

Continuing with our inflation theme this week, we show our renewables metals price index in the Exhibit below, which continues to climb and is now 50% higher than it was 2 years ago, with cobalt and lithium leading the charge at around 100% higher. These are critical components for EV and renewable power manufacture, and with 2022 forecasts for all suggesting much stronger growth, we do not see the materials supply/demand balances improving, suggesting that pricing will go higher. Energy shortages today, will only add more upward pressure to build more renewable capacity quickly and add even greater inflation risk to both components and the materials used to make them. We are concerned that, on the list below, only lithium is seeing significant capital thrown at increasing availability, suggesting that while lithium may peak in pricing, other metals could keep marching up. See our recent Daily, ESG Report, and upcoming Sunday Thematic for more.

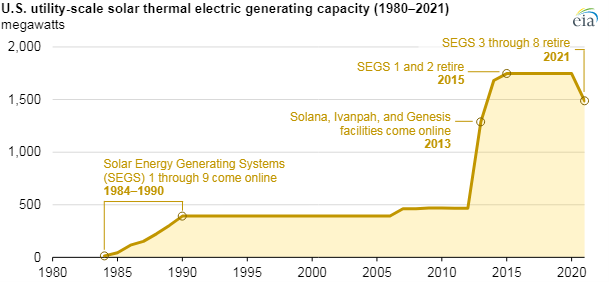

The charts below both support our view that we will see continued inflation in renewable energy costs, rather than the deflation that is baked into all of the forward models. It is easy to forget that some of the early solar installations are coming to the end of their useful lives and are retiring – these are gaps that new solar will need to fill. Wind power has the same issue, as many of the original wind farms need equipment replaced and the introduction of recyclable wind turbine blades has been in recent manufacturers' announcements. When we see analysis of who is going to use which tranche of new renewable power for which new hydrogen project we see major gaps in the power demand analysis, in part related to power demand growth at the domestic consumer – because the more rapid introduction of EVs – and in part because or retirement of facilities and the need to replace them.

Source: Bloomberg, C-MACC Analysis, May 2021

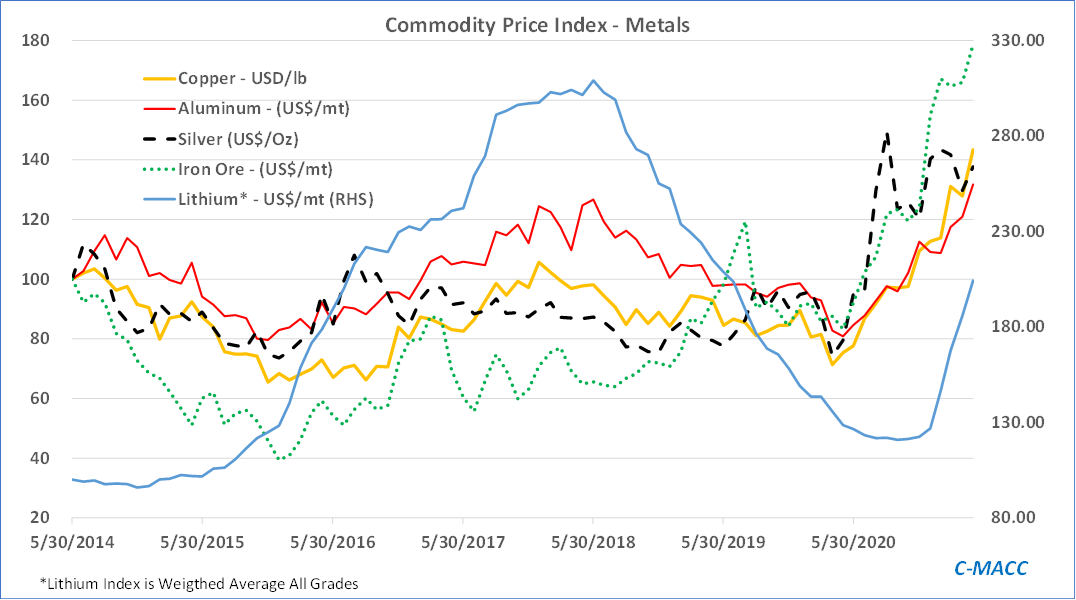

We return to a theme we have covered at length in several prior reports – the idea that the baby gets thrown out with the bathwater as politicians, regulators, and investors make decisions around what is best from a climate perspective and what is best from an ESG investing perspective. In many cases, the short-term noise and politics is masking some of the larger challenges and is likely to result in the wrong decisions, and potentially creating damaging inflation. See metals pricing chart below and today's daily report.

We have talked at length in several pieces of work published this year and last year about the risk that the ESG investor leadership in the climate debate could have unintended consequences, especially if they paint their “bad” ESG group with too broad a brush and include industries that are essential to the energy transition process. We have focused on the US mid-stream industry, which has a central role in providing logistics for more natural gas, more LNG, CO2, and hydrogen, but which will struggle to provide the infrastructure if they are thrown in the fossil fuel bucket and cannot get access to reasonably priced funding. Now we are seeing the same with the miners, many of whom are looking to expand to increase production of materials needed to aid in energy transition also – such as silver, copper, and aluminum.