We share views from Christopher Sheeron - The first-ever guest author for C-MACC's most recent ESG and Climate report titled "Does DC Understand Economics – Energy Proposals Suggest No".

Main Points from this report include:

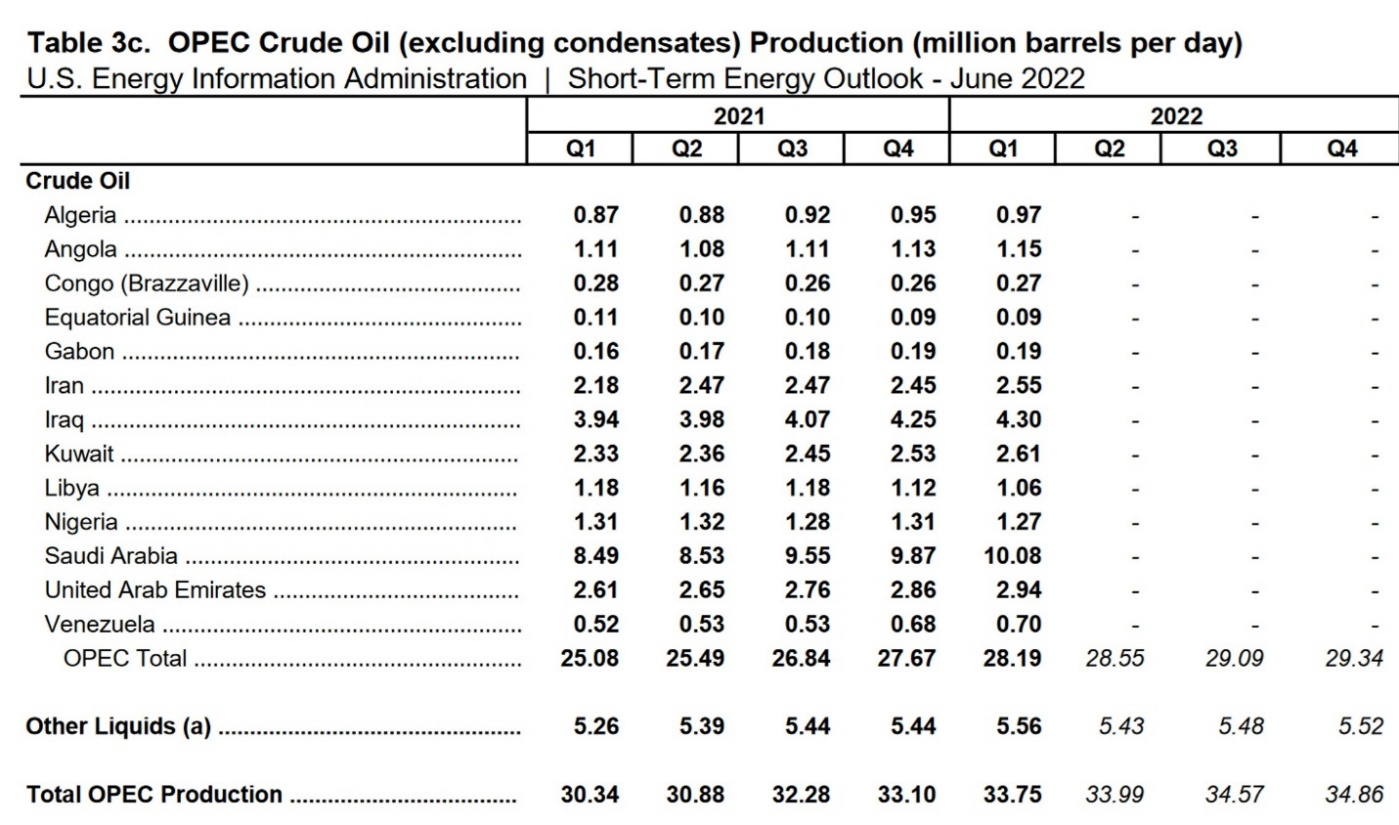

Jun 10, 2022 12:00:00 PM / by Christopher Sheeron posted in ESG, Sustainability, Renewable Power, Energy, Oil, solar, renewable energy, wind, climate, energy inflation, gasoline, water, OPEC+, NOPEC

Main Points from this report include:

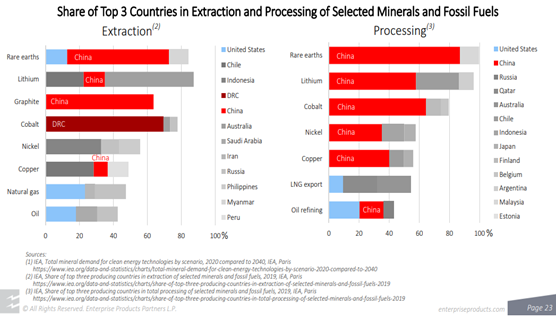

Apr 12, 2022 12:06:03 PM / by Graham Copley posted in LNG, Renewable Power, Raw Materials, Supply Chain, hydrocarbons, Dow, Oil, natural gas, clean energy, Enterprise Products, materials, fossil fuels, material cost inflation, minerals, renewable targets

While longer-term use of oil and gas products is in Enterprise Products' best interest, it is nice to see someone else pushing the point that we have been making for more than a year – that there is not enough material out there, in the right locations, to meet the suggested clean energy goals. It is important that this becomes better understood and accepted by a broader group than just Enterprise and C-MACC, as we will not get the needed tack in strategy, priorities, and incentives if there is a broad reliance on renewable targets that will not be met – we focus on the IPCC report in tomorrow’s ESG and Climate report.

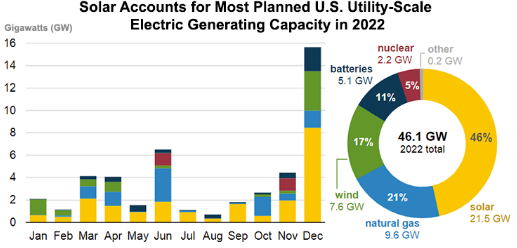

Mar 23, 2022 2:19:27 PM / by Graham Copley posted in ESG, Climate Change, Sustainability, Coal, Renewable Power, Energy, Supply Chain, Oil, natural gas, power, solar, renewable energy, solar energy, Gas prices, renewable capacity, supply chain challenges, Utility, materials costs

The back-end loading of the power projects for the US for 2022, as shown in the chart below leaves us somewhat skeptical concerning how much will come online this year. Supply chain problems and materials costs and availability are causing all sorts of problems with renewable power projects and installed capacity expectations for 2021 were too ambitious. We believe that companies are pushing projected start-ups later in the year to give them more of a chance of completion, but this creates the risk that they slip into 2023 or beyond. The most significant issue here is that as these plans get delayed, natural gas demand goes up, as one of the swing suppliers. This is fine as long as the US natural gas industry and shale oil industry is investing so that gas availability rises. Otherwise, we could see gas prices spike in the US next winter and another year where we use more coal than we expected. For more see this week's ESG and Climate report.

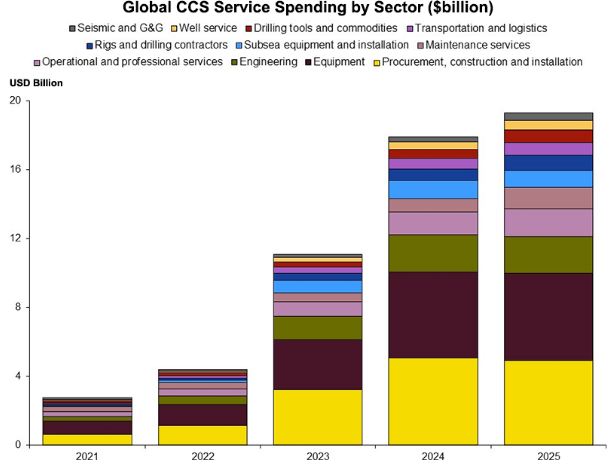

Mar 22, 2022 12:48:43 PM / by Graham Copley posted in ESG, Carbon Capture, Climate Change, Sustainability, CCS, CO2, Energy, Emissions, IEA, Oil, natural gas, clean energy, renewable, fossil fuels, renewable capacity, EPA

One of the subjects that we will cover at length in the ESG and Climate report tomorrow (to be found here) is the significant need for CCS globally, but especially in the US, as we see more balanced forecasts of energy supply emerging which show more use of fossil fuels for longer – especially, but not limited to natural gas. These forecasts recognize the current energy momentum as well as some of the more practical realities around the rate of construction of renewable capacity relative to energy demand growth. The CCS plans that are appearing all over the place are nothing more than plans right now and if the EPA permit activity is a true barometer – not much has moved beyond planning. This needs to change and we likely need both an increase in CCS incentives – which could take many forms – as well as some streamlining around the permitting process. Simply waiting and hoping for a renewable miracle is not going to work – nor is some sort of CCS cost breakthrough.

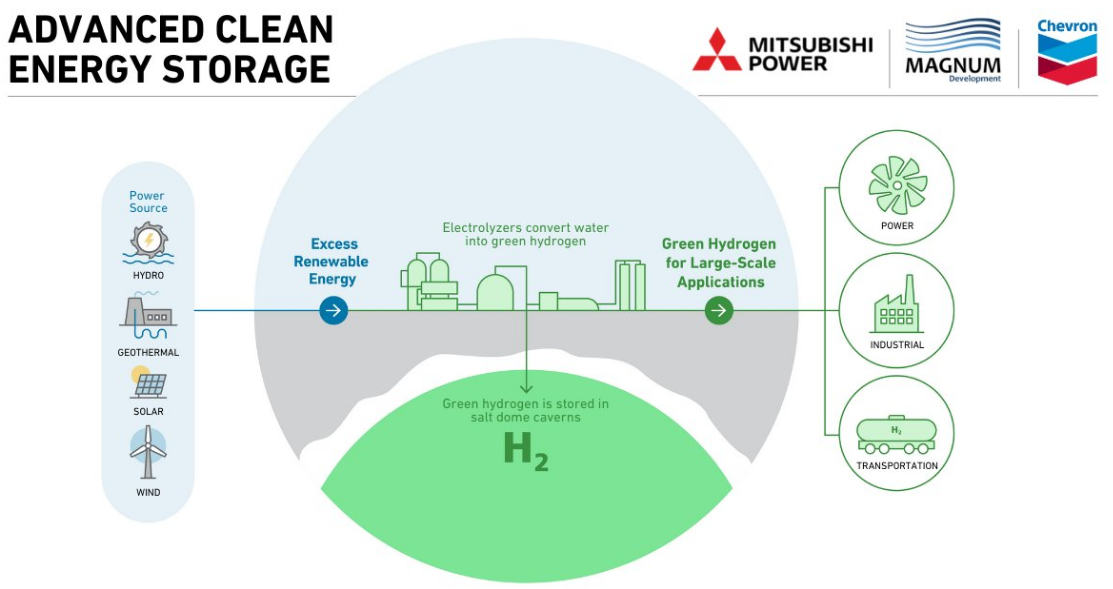

Sep 14, 2021 1:16:08 PM / by Graham Copley posted in ESG, Green Hydrogen, CCS, ESG Investing, ExxonMobil, Gevo, Oil, ESG investment, Chevron, Mitsubishi Power, Engine No1

The Engine No1 headline and the Chevron headline are not necessarily the right way to think about the challenges for Chevron and whether or not the challenges are just really beginning for ExxonMobil. The Engine No 1 approach to ExxonMobil was not ESG focused and hit on a larger issue of very poor shareholder returns, with ESG/Climate only one-line item on a list. What Engine No 1 is doing now, is focusing more specifically on climate, and ExxonMobil is likely as large a target as Chevron on this basis. Last week in our Sunday report, we commented on how good the Chevron Gevo deal was for Gevo, but that it did not move the needle for Chevron. Chevron, ExxonMobil, and others are aggressively pursuing renewable fuels, mostly from waste and vegetable oils until the Gevo agreement, and there is another headline today about Chevron pursuing CCS opportunities with Enterprise and the chart below discusses a green hydrogen plan for Chevron. All of these initiatives do not sum to something that investors will take note of for any of these companies yet, and while they might be important building blocks towards a net-zero future, larger tangible investments are probably needed to get any investor buy-in. In the meantime, the activists have a lot of room to work.

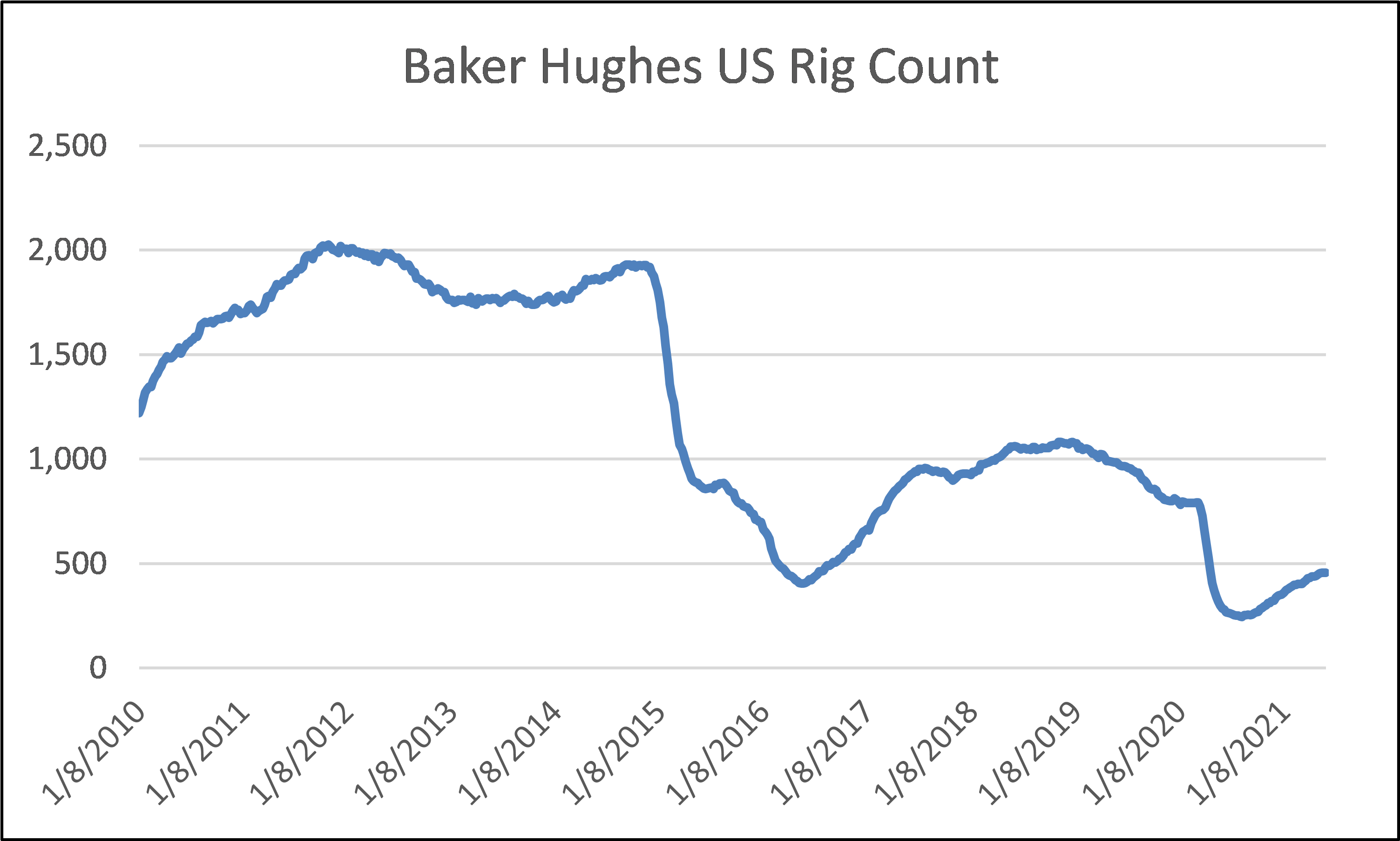

Jun 10, 2021 1:13:51 PM / by Graham Copley posted in ESG, Oil Industry, Oil, natural gas, oil producers, ethane propane

We repeat some of the commentaries from yesterday's ESG piece as we do not believe this risk can be highlighted too much.

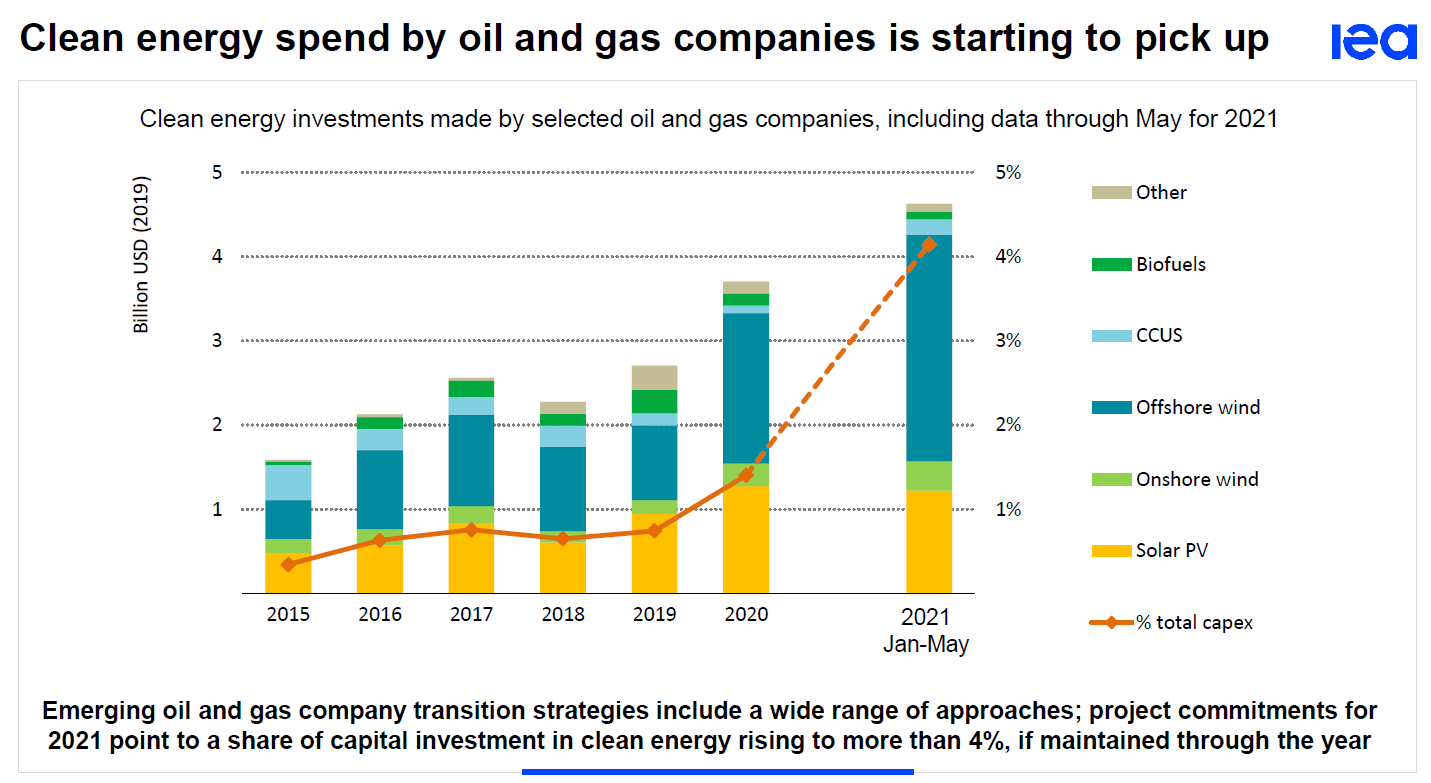

Jun 2, 2021 1:29:12 PM / by Graham Copley posted in ESG, Oil Industry, IEA, Oil

In today's ESG and Climate report we discuss the issues facing the oil industry and present several possible scenarios focused around activist behavior and government behavior – none of the outcomes are pretty and the most likely one is quite concerning. The activists seem to be laser-focused on reducing the production of fossil fuel, but they are arguing for a timeline that is impractical and very inflationary – right now they are winning and they are changing the hearts and minds of investors, both public and in some cases private, but perhaps more important, they are influencing insurers. The fossil fuel industry needs to clean up its act, no doubt, and based on the chart below it is trying harder, but a transition period is necessary to prevent hyper-inflation not just in fossil fuel prices but also in renewables, as they would not be able to keep up with an aggressive cut back in fossil fuel production today – which is what activists are pushing for.

May 28, 2021 1:50:42 PM / by Graham Copley posted in Oil Industry, Energy, Emissions, Shell, Oil

We talked about the Dutch ruling against Shell in yesterday's report and the latest refinery sale in the US is another indication of one of the risks of unilateral court-based decisions. Shell could easily get to lower emissions by divesting assets, as can anyone else with a medium-term emission target on the books. We have written previously about the possibility of an energy equivalent of the “bad bank” structure that was set up during the financial crisis, where emissions challenged assets are divested into either private entities or public holding companies that have mandates to improve excessive emission pools but also have significant cash flows and pay investors to wait.

C-MACC utilizes a proprietary process that melds decades of global chemical industry experience, detailed fundamental analysis, extensive field research and innovative analytics to provide our clients research products and services, and strategic consulting offerings. Our main objective is to enable informed decisions for our clients and to do so in a timely and cost effective manner...