There is an unusual number of interesting topics in today's report, versus the normal mix of small pet projects or broad and unsubstantiated announcements. The EU 2030 targets are worth highlighting and they are in part connected to the central theme of the ESG and climate report that we will publish tomorrow. The European targets are not coordinated with what is happening in the rest of the World and while we admire the ambition, we suspect that the goal is not achievable, simply because the challenges of replacing the power and fossil fuel associated with the emissions to be avoided are too great, given the timeline. The level of additional renewable power generation, EV adoption, and hydrogen production needed to offset so much CO2 are extremely high, and it will be hard to get substantially more CCS offset than already announced because of land rights issues in Europe and logistics. To get the power, EV, and hydrogen, the EU will be competing with other regions that have their own targets and we see scare resources bidding up the price of power, impacting all of the elements, power itself, the cost of running EVs (see the chart below – the EV story does not work of you are using coal as a marginal source of power), and the cost of hydrogen.

There are several headlines today that speak to one of the most pressing issues that we have with the pace of energy transition – the competition for renewable power and the likely inability of the industry to keep up with the competing needs, let alone do so without significant power cost inflation.

The WSJ article linked talking about rising ESG spending and the risks associated with it is in no way inconsistent with our view that lack of US Government guidelines is constraining ESG spending. The article focuses on the power and auto industries, which, while they face regulatory and incentive uncertainty, have a much clearer path than many others. The power industry is dealing with a customer which is increasingly asking for more renewable power, an investor base that is pushing for less reliance on fossil fuels, and a Government that is pushing for a 50% emissions reduction from the sector. The auto suppliers have clear directives from some US states and some countries about the phasing out of fossil fuel-based vehicle sales, and in some geographies, they have incentive systems that they can tap into. For both industries, there is a significant risk, in that the billions of dollars that they are investing in new plants and new equipment do not come with any guarantees that those investments will pay off well or quickly, but at least the direction of travel is unlikely to change. In other words, there will be demand for their products and investors will likely be happy with the progress – while they might not get the EBITDA they would like, they may get a better multiple of that EBITDA.

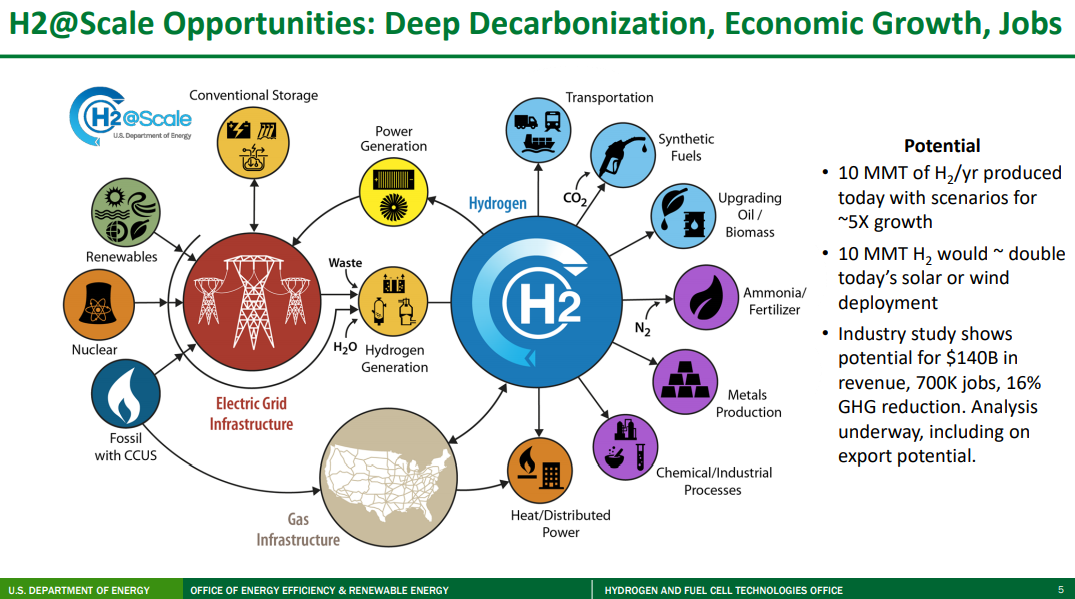

We will cover the very comprehensive DoE hydrogen work in more detail in the ESG report next week, but a couple of the charts from that work are worth mentioning today. The first picture below accurately depicts all of the potential uses of hydrogen and shows that over time it could solve a lot of “hard to solve” CO2 emission problems, especially where electricity cannot do the job efficiently. The reason why so many countries and companies are so interested in hydrogen is because of its potential versatility and because of its minimal carbon footprint (there is some carbon leakage in the full lifecycle of the production coming from construction around the plants themselves and infrastructure to use the hydrogen).

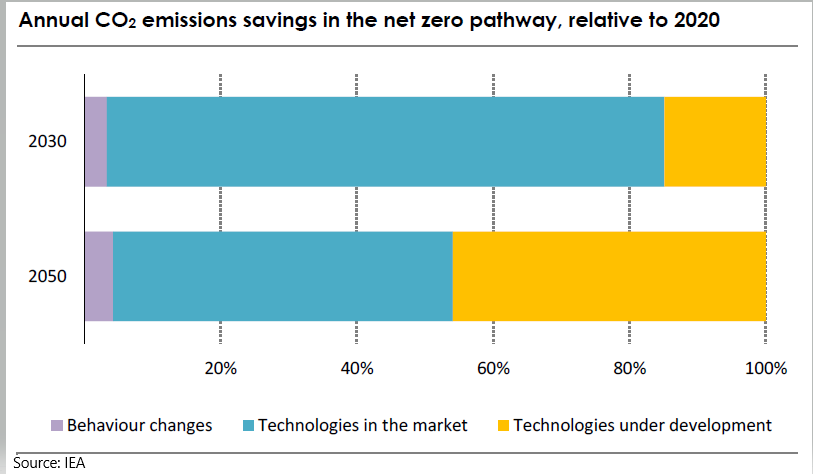

There are too many important topics to choose from today and we will cover many of these in our ESG and Climate report tomorrow. Here we focus on the IEA report published this week, which shows a path to net-zero on a global scale and looks at both the fossil fuel consuming sectors and the rate at which each must change (they are different by sector) and what fuel alternatives will be needed to replace them. Our review of the work would suggest the following:

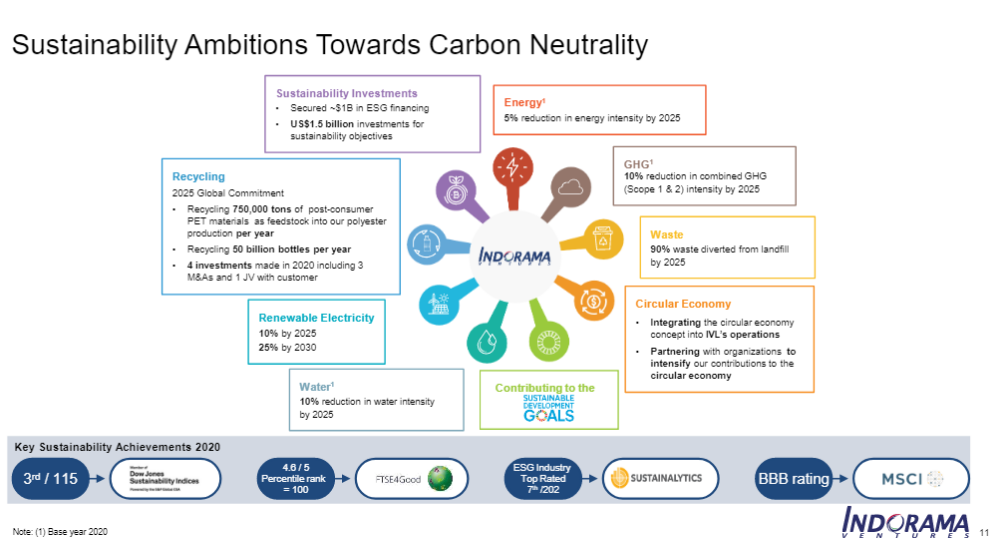

The headlines in today's daily report are interesting as they discuss a large number of different initiatives in recycling, carbon use, and capture, routes to hydrogen, etc. Each initiative is small, but the collective news is encouraging as it suggests that the mood might be changing from one which focuses on only a handful of tools to meet emission goals – which in turn are already helping to driven materials inflation - to a much broader approach that recognizes, or at least beings to recognize, that we need to try everything. We need to experiment with new approaches to recycling; we need more use for CO2 than simply pushing it all underground (but we must still push a lot underground), and we need to try multiple routes to hydrogen, not just those that need to consume vast amounts of renewable power. We need more partnerships – several listed this week - and we need government support where it can be most effective. The headlines today are far more heterogeneous, which is a good sign. One company's view of the solution is show in the chart below.

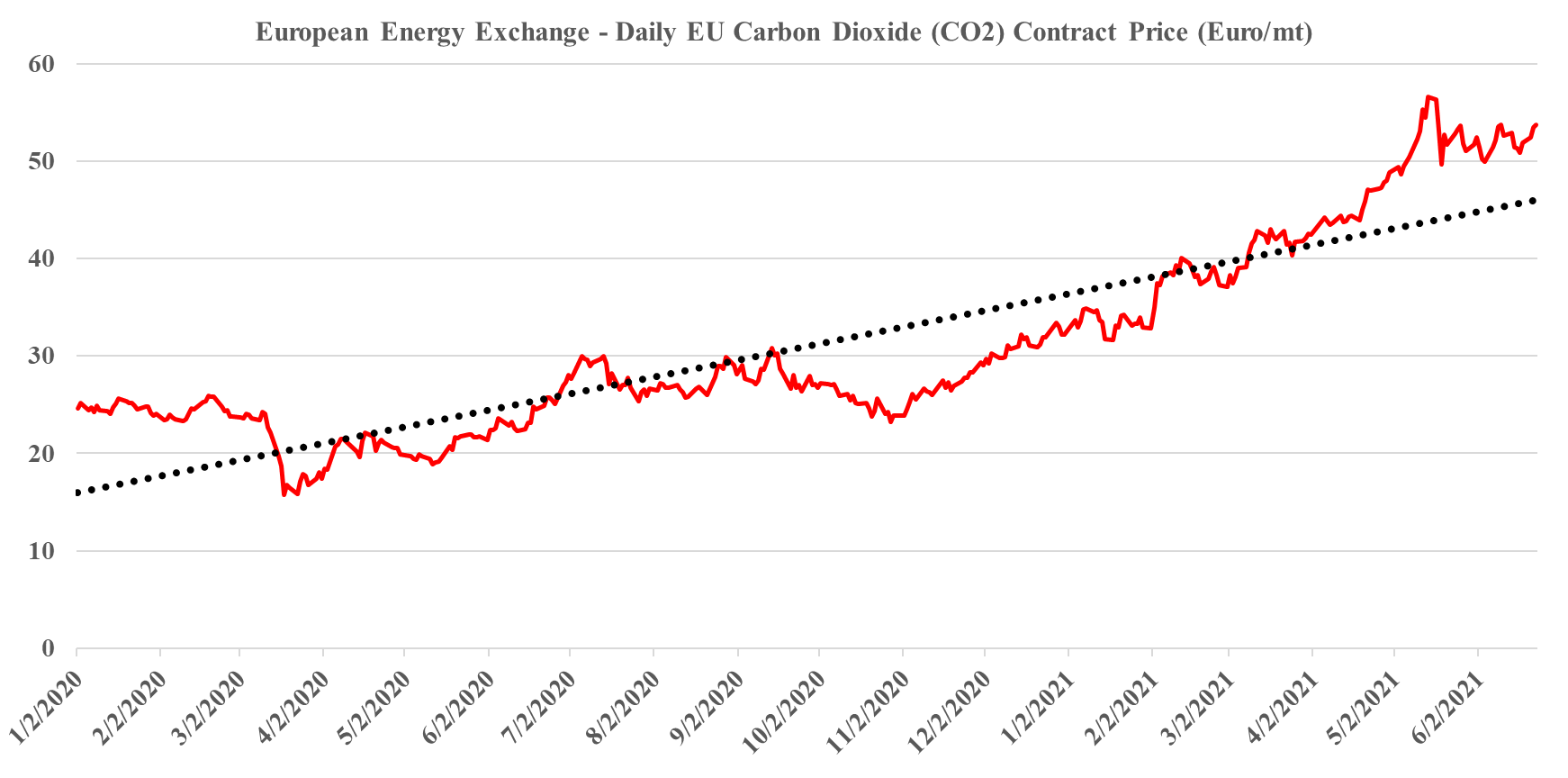

Source: Bloomberg, C-MACC Analysis, May 2021

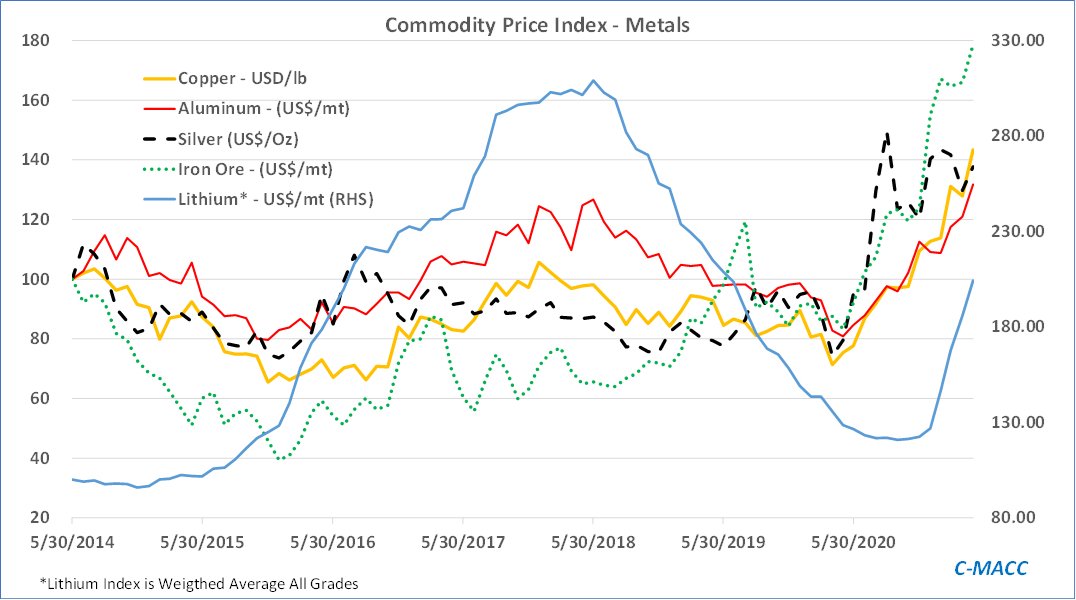

We have talked at length in several pieces of work published this year and last year about the risk that the ESG investor leadership in the climate debate could have unintended consequences, especially if they paint their “bad” ESG group with too broad a brush and include industries that are essential to the energy transition process. We have focused on the US mid-stream industry, which has a central role in providing logistics for more natural gas, more LNG, CO2, and hydrogen, but which will struggle to provide the infrastructure if they are thrown in the fossil fuel bucket and cannot get access to reasonably priced funding. Now we are seeing the same with the miners, many of whom are looking to expand to increase production of materials needed to aid in energy transition also – such as silver, copper, and aluminum.

We don’t want to throw cold water on a very HOT idea, but the BASF, SABIC, Linde announcement of collaboration on electric furnaces for ethylene production is not the first that we have seen, as both Dow and Shell have stated that they are looking at similar ideas. As an “endgame” objective this is interesting, as it would remove the need for natural gas fuel and greatly reduce emissions, but despite the claims in the release, this is an interesting pilot project at best today. It is a credible process, and the companies have likely achieved ethylene production this way on a lab scale. It is possible to get significantly higher temperatures today through electric power than the 800c (1500f) suggested in the article. Some plasma jet technology can achieve temperatures in the 1000s of degrees centigrade, but the power consumption is extremely high, and it is worth noting that the press release does not mention the possible power requirements to get to a metric ton of ethylene. Modern ethylene units produce a million tons a year (or more) – which is around 2 metric tons per minute. The better technologies involve raising the feedstocks to very high temperatures very quickly (measured in fractions of a second). The partners talk about achieving electric power-based ethylene at scale. This is a lofty goal. Should they succeed, not only would ethylene plants require significant retrofitting at the front end at very high capital cost, but the power requirements would be enormous, putting even greater strain on global and regional renewable power ambitions, that already looks hard to achieve, given all of the competing needs. We would want to ask two questions:

- Are you better off making hydrogen and using hydrogen as a furnace fuel in a traditional and well-practiced ethylene process – this would likely mean much lower capital refit costs?

- Are you better off still just capturing and sequestering the CO2 from existing facilities?

Photo by Linde Engineering. The ethylene furnaces are in the background to the right of the picture

With many of these “cleaner” objectives and theoretical technologies, there may be other more practical workarounds, and if not they still probably do not make sense until there is such an abundance of renewable power that the incremental cost of power is very low for 95% of the time.