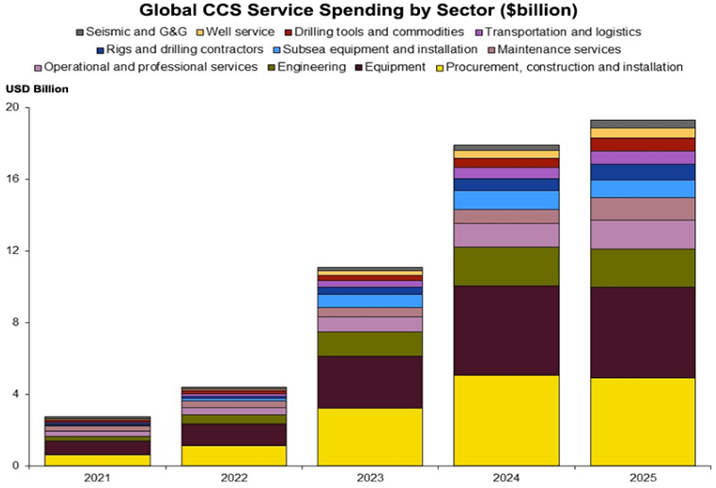

The CCS spending chart below is quite detailed, but shows the limited amount of spending in 2021 and 2022 and may underestimate the amount of seismic spending needed, especially in the US, as companies prepare permit applications. We do not expect to see much spending in the US before mid-decade beyond permit applications. However, as we discuss in today’s ESG and Climate report, should the API proposed carbon tax, or something similar, be additive to the 45Q tax credit, we could see a step-change in CCS when/if the tax is approved. The tax on its own is likely not enough to drive decarbonizing investment, but when added to 45Q it could be a specific trigger for CCS investment, and we could see a step-change in the second half of the decade. This might involve large-scale blue hydrogen production, especially on the Gulf Coast to decarbonize the refining and chemical industries.

The decarbonization of the airline industry remains a hot topic. The energy density issue shown in the exhibit below is a correct assessment of why commercial aviation faces a challenge to transition to electric power. Not only is the energy density too low - which restricts weight/range - but electric power can only turn things, and propellor-based flying has speed limitations relative to jets. The announcements from the airlines to date on electric power have focused on low capacity short-haul opportunities. With this in mind and as noted in the article headlining of the exhibit below, electric power is not the only decarbonizing option for airlines. Hydrogen is the very long-term future - Airbus is saying not before 2050, but in the meantime, the push should be for low carbon or carbon-neutral biofuels. These are essentially plug-in fuels that are identical to current aviation fuel but made either from waste oils or from carbohydrates. Many of the oil majors are working on waste oil or vegetable oil-based processes, especially in California where the LCFS credit helps pay for the conversion, and companies like Gevo and Aemetis are working on carbohydrate-based routes through fermentation. If the carbohydrate, corn in the case of Gevo, is sourced from sustainable agriculture the carbon values of the fuel can be very low and potentially zero or negative through the life cycle. The airlines are going to have to pay up for the low carbon fuel if they want to bid the fuel away from the high credit markets like California diesel and gasoline, but this route could decarbonize the airlines significantly and relatively quickly with the right pricing structure and enough capital.

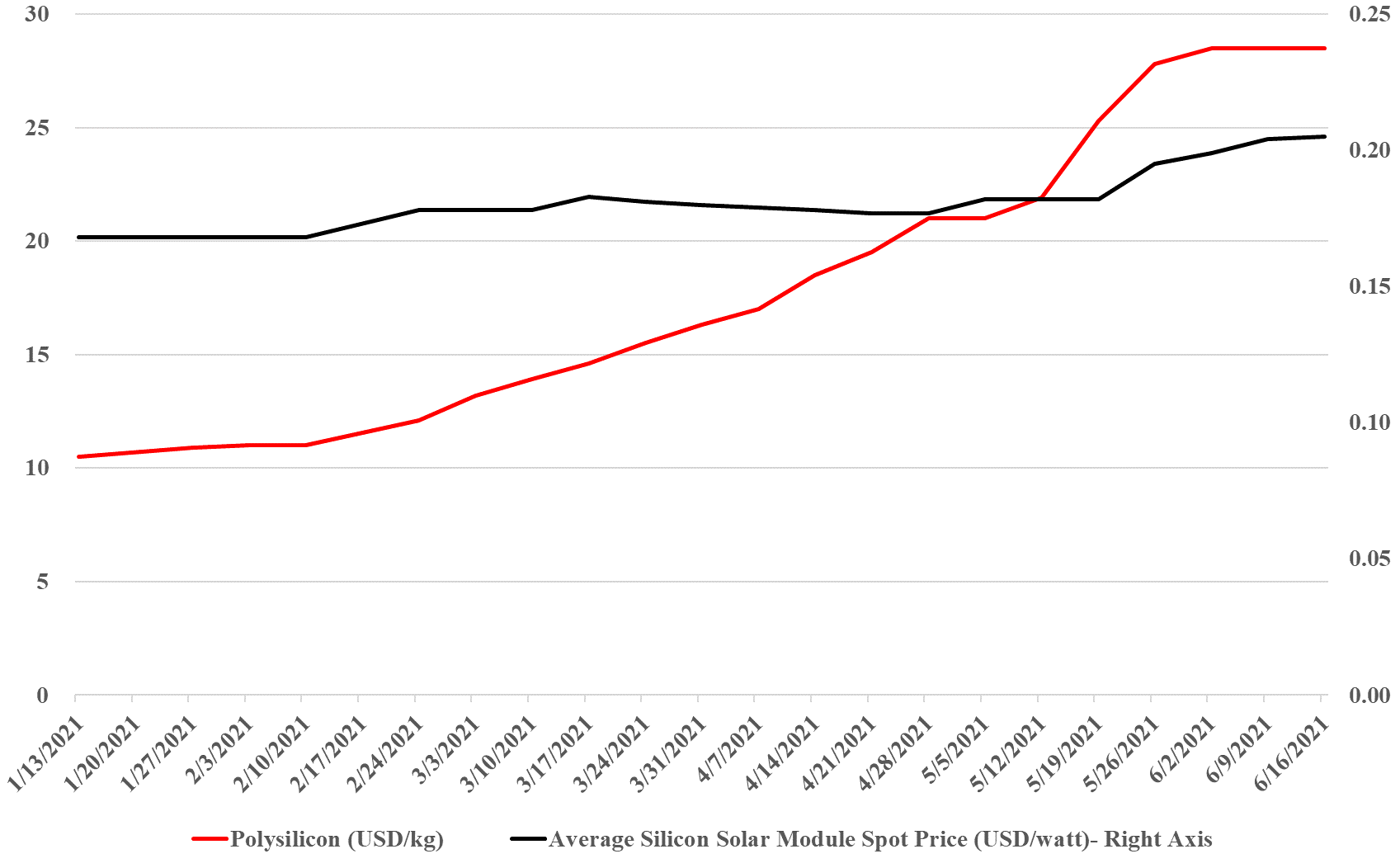

The exhibit below summarizes well one of the primary concerns that we have with some of the very ambitious goals for decarbonizing power grids, EV introduction, the further electrification of industry, and hydrogen. While the solar module price increase does not look that significant (yet), to put it in context, solar module prices have collapsed from over $1.80 per watt in 2010 to below $0.20 in 2020, and many of the expectations around cheap hydrogen require the cost to keep falling. The bigger concern is the polysilicon price, which is up 160% this year, good for the polysilicon producers like Wacker (see the headline here), but bad for the solar module producers, who are seeing major margin squeezes, especially given the rise in copper and silver as well this year. The raw material pressure should drive further increases in solar module pricing and while the higher margins for polysilicon will likely drive expansion investment, the metals are harder to call, given the ESG views on mining. We remain firmly of the view that raw material availability and price inflation, as well as module and wind turbine manufacturing capacity, will be the rate-determining constraint in terms of the growth in renewable power and this is why we question all of the near-term cheap power and cheap hydrogen goals that are being suggested by potential producers and government agencies.