We have talked at length in our dedicated ESG pieces about the inevitable role that investors and financial regulators will play in addressing climate change, and we see more evidence that some of this pressure to conform is going to be pushed down to banks and lenders as standards are set for disclosing financial exposure to high emission industries. The banks will have little choice but to add their weight to the calls for better disclosure and eventually mitigation plans, as it will impact their ability to lend and their ability to defend lending portfolios to their stakeholders. Green bond markets are developing around the world, but still need some definitional oversight and it will be interesting to watch corporate behavior if a significant borrowing cost delta emerges between “green lending” and other lending – it might be a lot cheaper to get debt focused on net-zero related projects than expansion projects and it was interesting to note that Repsol’s announcement (linked here) talks about carbon abatement (in general terms) as part of the investment in Portugal.

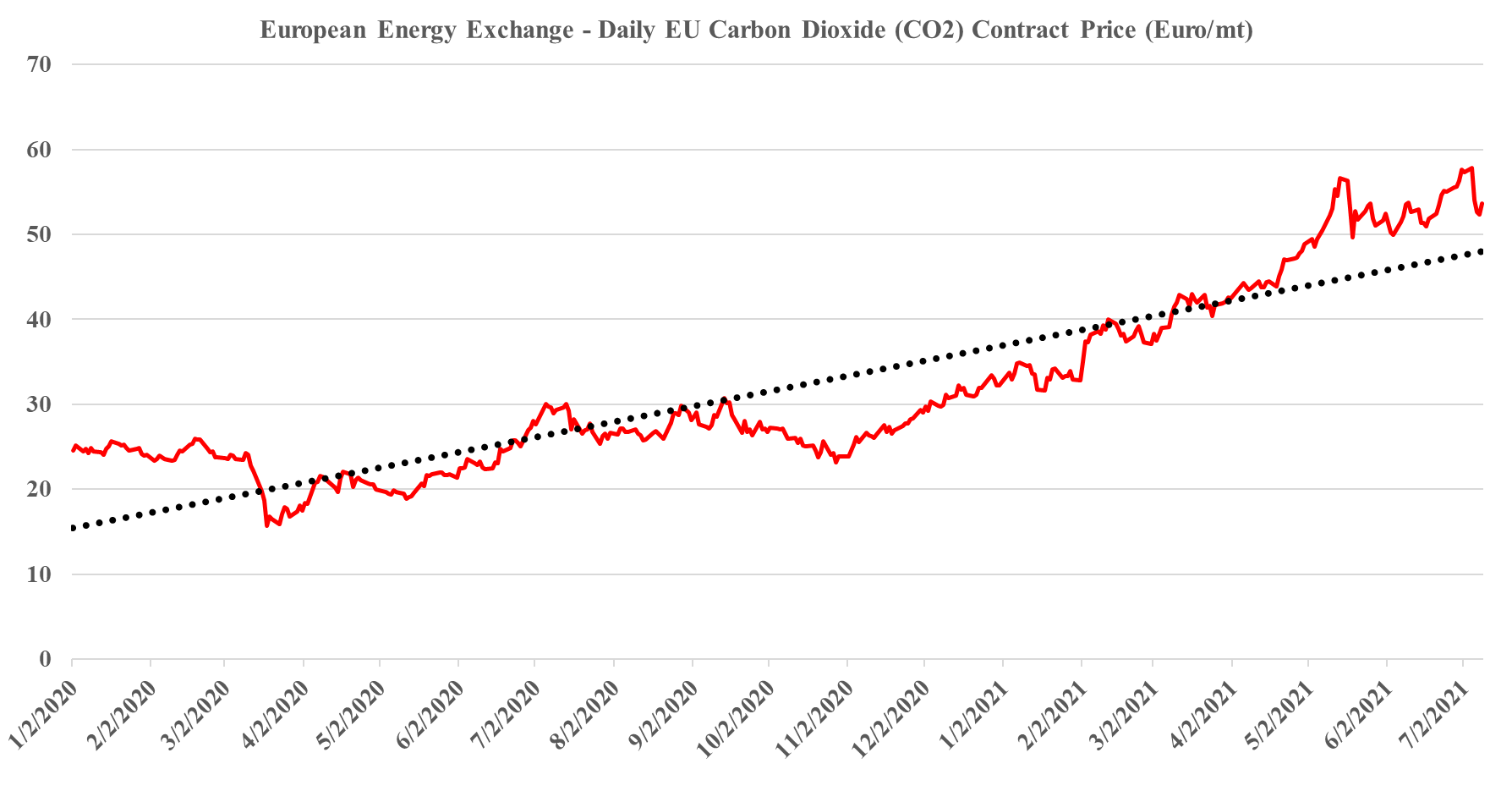

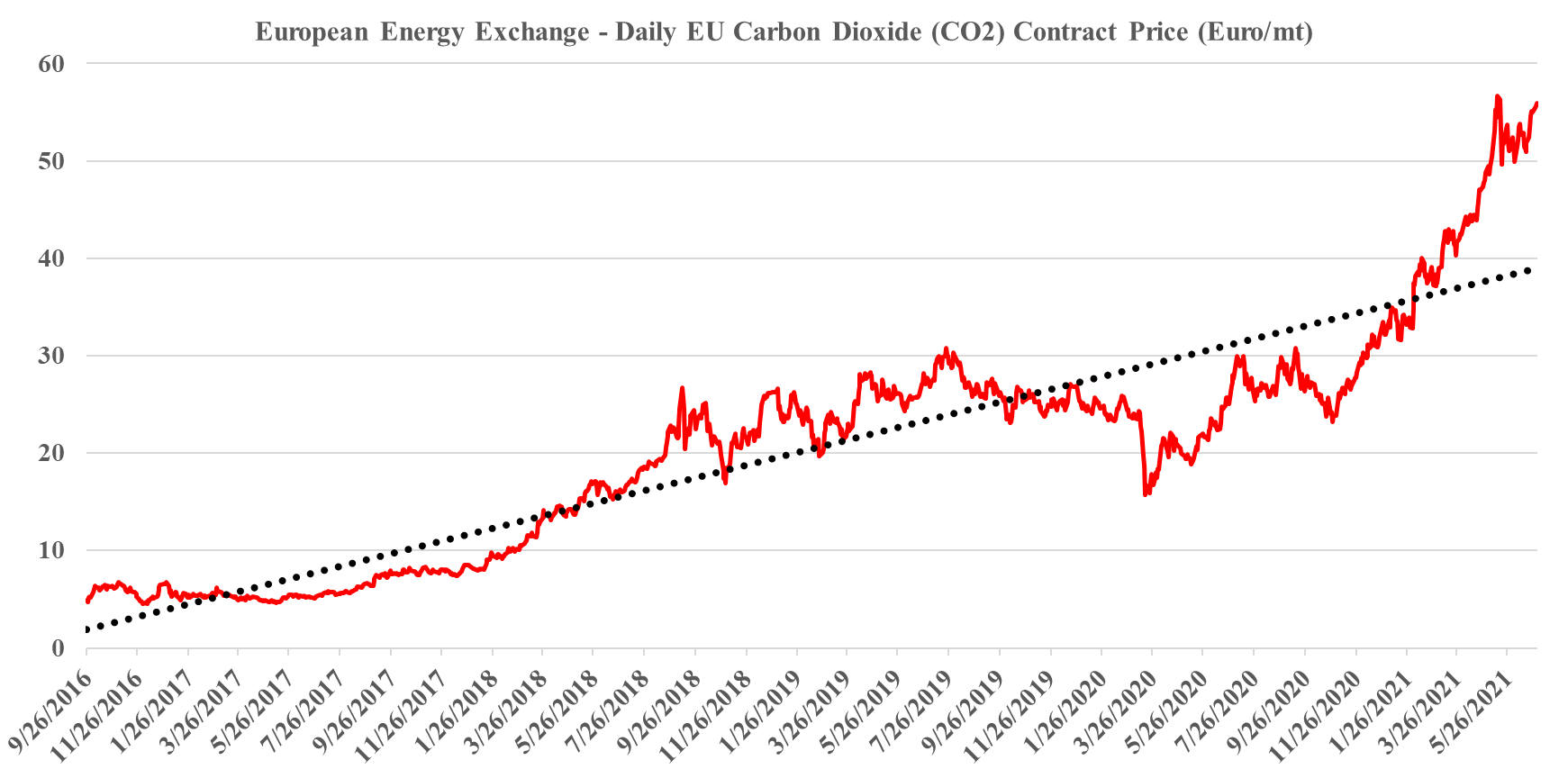

We are skeptical about carbon offsets and we are more skeptical about announcements around carbon-neutral fuel and chemical cargoes. The ESG and climate activists have their radars finely tuned for “greenwashing” and other exaggerated claims, and when we get into offsets, whether as a traded market or as a one-off green cargo we rightly see the skeptics. The cargoes – ethylene below and an LNG cargo earlier this week - are PR stunts in our view and while the accounting may be accurate, the one-off costs are likely high, and the ability to repeat the process for significant volumes is limited. It may be proof that you can create carbon neutrality through offsets, but the supply of offsets will likely never be large enough to create affordable permanent pathways, and offsets should be looked at by all as a way to go the last mile, having exhausted all other options, including carbon avoidance and carbon use or sequestration. We have noted in prior work that we see a risk of too many people banking on a share of the offset market than the likely size of the market – creating price inflation and ultimately lower revenues than could have been achieved through alternate means. Current offset markets are cheap – at least relative to other costs of carbon abatement, but higher levels of oversight, which are both needed and planned, will likely limit availability going forward – also suggesting higher pricing.

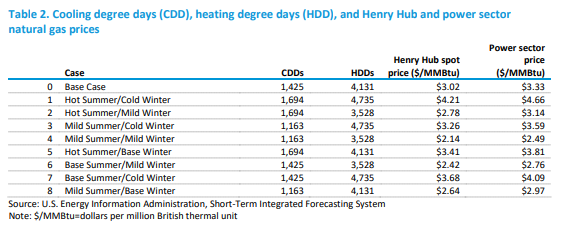

The table below is from an interesting analysis published by the EIA this week that focuses on possible power demand scenarios for the US – all weather-related – and then backs into the power sources that would be needed to meet the demand, concluding with the US carbon emissions that would correspond to each scenario. The conclusions should not be surprising, which are that carbon emissions rise disproportionately faster as power demand rises – as more coal is required to balance generation needs, and fall disproportionately more quickly as power demand falls (as less coal is needed). The analysis is effectively a study of how much less CO2 emissions are using natural gas to generate power versus coal. As renewable generation increases as a share of the total, however, the math will change, and the EIA study does not take into account the weather factor on renewable power, it looks at cooling degree days and heating degree days at a national level only. This is reasonable as there is likely not enough data to be able to put good reliability estimates yet around renewable power annual volatility and more importantly, the impact of weather on renewable power is likely to be short-term in nature. Perhaps this analysis could be improved by adding a “daily risk band” around each scenario, showing how much renewable power volatility could cause peaks in the high scenario and lows in the low, etc.

One of our concerns with the Lithium hype has been what we perceive to be very low barriers to entry – coupled with significant momentum from lithium ultimate end-users to encourage more production. If we look at the linked GM announcement, the company is making exactly the right strategic move. Providing some funding, but more importantly, high-level credibility for a new US-based project that could dwarf other US initiatives. While GM may have contracted all of the lithium volumes from this project, it is unlikely. GM’s interest, which should be aligned with all the other automakers is to ensure an ample to surplus availability of lithium long-term to keep pricing low. Investing a few million to give legitimacy to a new large project may have huge potential longer-term benefits if the capacity helps maintain a longer-term surplus market. While there may be some special sauce in the technology required to make the lithium grades for higher-end and higher density batteries, the bulk of the auto market is likely to trade range for cost in its battery decisions – and at the less expensive end, the lithium barriers are very low, with other brine-based projects under consideration and likely to find funding.

One of the themes that we have focused on in our ESG and Climate work is the lack of realism in the Biden climate plan as it relates to power generation and the same with the plan in California. The more limited reliability factor in renewable power (because of its dependence on cooperation from the weather), means that you have to build a lot more new power capacity than you are replacing and you need to build a storage system for the power – batteries, hydrogen or hydraulic. This gets very expensive and will be more so if the push drives inflation in raw materials – which is already a factor YTD in 2021. Natural gas turbines are a cleaner and reliable source of power and cleaner still if combined with CCS. Politicians in the US are taking a considerable risk by promoting plans that could leave the power grid more vulnerable to some of the issues that we have already seen over the last 12 months (California and Texas). Of course, as the plans call for natural gas phase-outs in 10-12 years, none of those making the decisions today will be in the office to face the consequences!

The ESG investment shakeup could be one of the major events of this year, and as many of the headlines in our daily report suggest, there is a lot of work to be done, whether it is agreeing on a common set of measurement metrics – note the US and European differences discussed in one story – or the introduction of more empirical methods to judge whether what is labeled as an ESG investment fund is labeled correctly. There is also the issue of comparable disclosures, especially for companies in complex industries. It is interesting to note that in many analyses we see around carbon footprint or greenhouse gas emissions, and the potential routes to and cost of abatement, the chemical industry is omitted, except for ethanol and hydrogen. This is despite the industry accounting for 15% of the non-power emissions in the US industrial sector (similar in size to refineries). We believe that this is because the complexity of the industry makes it hard to model, and analysts choose to exclude it because they are not sure what they are doing.

There is an unusual number of interesting topics in today's report, versus the normal mix of small pet projects or broad and unsubstantiated announcements. The EU 2030 targets are worth highlighting and they are in part connected to the central theme of the ESG and climate report that we will publish tomorrow. The European targets are not coordinated with what is happening in the rest of the World and while we admire the ambition, we suspect that the goal is not achievable, simply because the challenges of replacing the power and fossil fuel associated with the emissions to be avoided are too great, given the timeline. The level of additional renewable power generation, EV adoption, and hydrogen production needed to offset so much CO2 are extremely high, and it will be hard to get substantially more CCS offset than already announced because of land rights issues in Europe and logistics. To get the power, EV, and hydrogen, the EU will be competing with other regions that have their own targets and we see scare resources bidding up the price of power, impacting all of the elements, power itself, the cost of running EVs (see the chart below – the EV story does not work of you are using coal as a marginal source of power), and the cost of hydrogen.

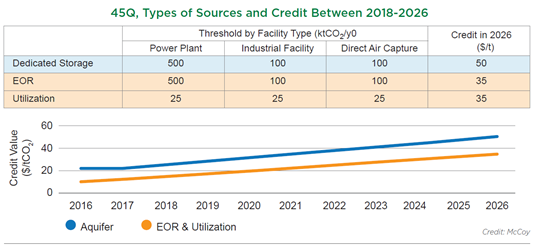

Senator Cramer’s proposed Bill to increase the value of the 45Q carbon credits for sequestration and use as well as remove the annual cap could be a game-changer in many ways. The threshold removal is necessary regardless of the credit value. In our view, the cap creates a potential competitive disadvantage for smaller companies competing with larger ones, especially in the chemical space. Should the Bill increase the tax credit enough to drive real investment in abatement but not remove the threshold we would expect to see litigation from smaller disadvantaged companies. The chart below shows the current expectations for 45Q. To date, the only real investment activity we are seeing is around sequestering CO2 from ethanol production in the US. This is because the CO2 stream is easy to separate in a fermentation process and because some of the ethanol can benefit from the much higher LCFS credit if the fuel is sold into California.

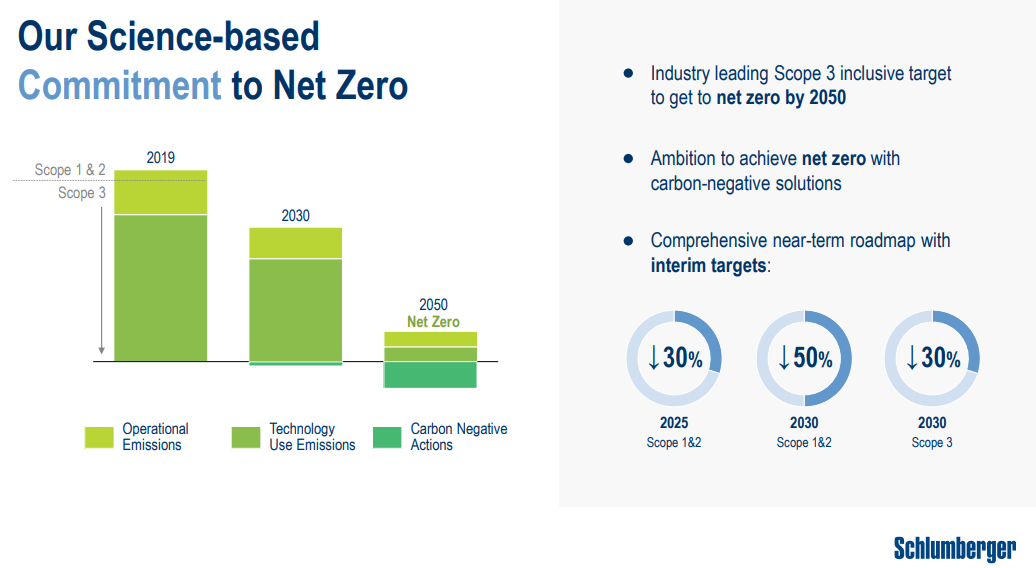

The Schlumberger net-zero goals, as discussed in a couple of articles in today's daily and the presentation linked, set some aggressive but bold ambitions, especially as they are looking to solve problems that they share with their customers, methane leakage from oil and gas wells, and minimizing flaring. Schlumberger is a little dependent on collaboration from its customers here as the technology solutions are likely to be more expensive than current options and the oil and gas producers will need to pay up.