We have decided to change up our blogs, at least once a week and each Friday, to pose a question rather than throw out opinions.

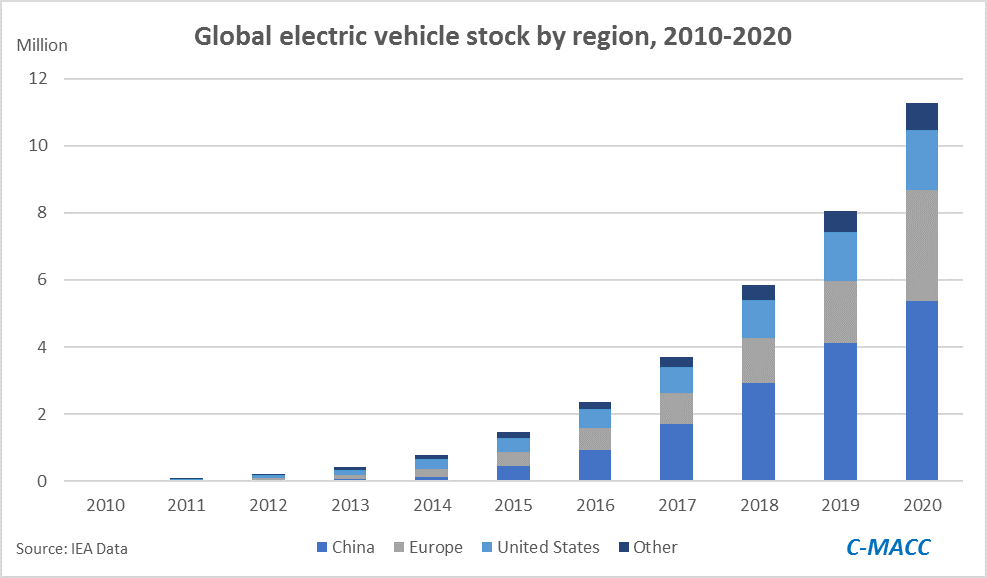

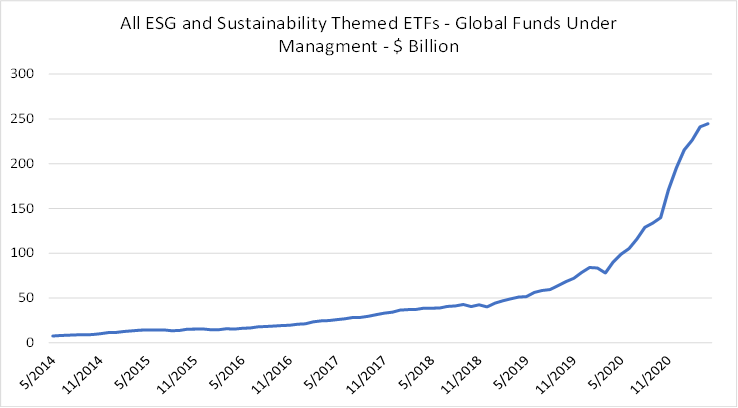

Today we should focus on the very good FT article linked here, which discusses in detail many of the issues facing both ESG investors and corporates concerning the lack of standards in ESG metric providers and the data provided by companies. It is a subject that we have been writing on for a couple of years – before C-MACC – because it is a potential dark stain on ESG investing and has turned (in some cases) a progressive move by the investment community into something that lacks a clear standard empirical base and is currently open to manipulation. The article highlights the ability of corporates to change the ESG metric providers that they use for internal measures and external reporting based on which provider sheds them in a more positive light. It also allows ESG funds to hold stocks that other ESG funds would not because they are not working off the same definitions. The flow of funds into this segment makes oversight critical (see chart below).

We would like thoughts, in the hope of starting an interesting dialogue on what you think the primary role of an ESG fund manager should be – to maximize returns, to promote change, to attract funds, etc.