We share views from Christopher Sheeron - The first-ever guest author for C-MACC's most recent ESG and Climate report titled "Does DC Understand Economics – Energy Proposals Suggest No".

Main Points from this report include:

Main Points from this report include:

We discussed the woes of the wind power industry at length in a dedicated ESG and Climate piece last week, and the Vestas results below play into the same theme. The company is cutting guidance again for 2022, which is already much lower than estimates would have suggested 6 months ago. While Siemens Gamesa has the added headache of a mismanaged platform change, all of the issues raised by Vestas are shared industry wide, delayed installations because of supply chain issues and material shortages, as well as significant cost inflation. In tomorrow’s ESG and Climate report we discuss some of the increases in European PPAs in 1Q 2022, reversing a multi-year trend of lower installed costs of power. This reversal will likely impact plans for 2022 and 2023, especially for those banking on lower power costs to justify many of the announced hydrogen ventures – particularly in Europe. Those who press ahead despite higher power costs and higher construction costs in general, may stretch both balance sheets and borrowing capacity.

In our ESG and Climate report tomorrow we are focusing on the wind industry and specifically the problems that Siemens Gamesa is facing with execution, costs, and logistics. The estimates for China and the rest of the world in the chart below assume a significant step-up in the rate of installation, and in 2022 we are seeing an industry that is struggling with that. Siemens Gamesa is having problems with its new platform, which had been intended to deliver projects more cheaply from an installed cost basis and an operating costs basis and is perhaps an illustration of what can happen when you are trying to move too quickly – partly because your customers are demanding it. Operational problems at Siemens Gamesa have been compounded by logistic challenges and raw material price and availability, such that current expectations are for the company to break even at an EBITDA level in 2022. This is another great example of the policy and investor disconnects that we see in several aspects of energy transition – we are encouraging investment in front line capacity, but not in the materials and feedstocks needed to feed the front line – metals, natural gas, crops. See our recent body of ESG and Climate work for more on this. These subjects are at the heart of many of the private engagements that we have with several clients in this space.

One of the concerns that the IPCC has in its report issued this week is that things are not happening fast enough and the Ammonia analysis in the chart below would support this view. Most of the capacity addition comes post-2030 in large part because project planners cannot see a way to enough cheap power to generate the green hydrogen needed until that time. In our view, since COP26 the transition part of the energy transition has been overwhelmed by advocates of green technology and renewable pathways without much thought about how practical they might be today. Those suggesting transition options are being given very little airtime and as a consequence, we see broad hostility towards anything that is not truly green, regardless of whether the costs or time frames make any real sense. If we do not embrace bold transitionary steps including the use of hydrocarbons with aggressive abatement targets we will not meet any of the shorter-term goals that the IPCC highlights and we are putting hope in renewable and technology development which may come up short. Related to this we see the LNG dilemma in Europe, with the current and medium-term needs very apparent, but a reluctance to sign up for longer-term supply because of an expectation that if all things renewable come to pass, the LNG might not be needed. The Europeans will need to make the longer-term commitment if they are to persuade the US and other potential exporters to build new export terminals.

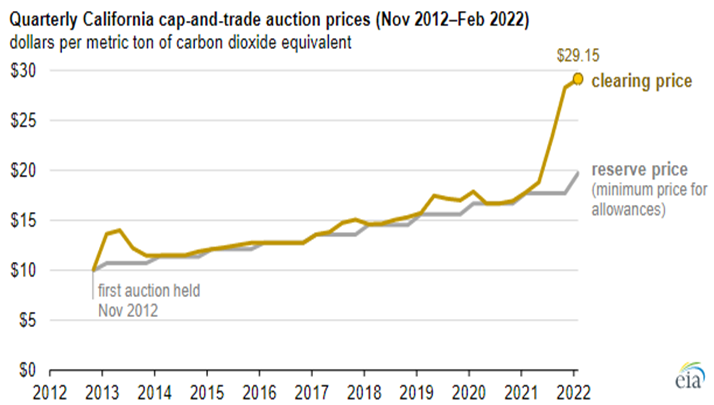

We have written extensively about carbon prices over the last two years and followers of our dedicated ESG and Climate service will know that our expectation is for all CO2 markets to see prices rise to levels that justify large investments to avoid CO2 production or sequester it. We see that price closer to $100 per ton than the $50 per ton that 45Q will rise to by 2026. The California price shown below has much more upside as credits demand rises. Many of the net-zero pledges made by manufacturers and energy producers today cannot be achieved without buying some sort of credit and we expect demand to rise relative to supply through the balance of the decade and possibly quite quickly.

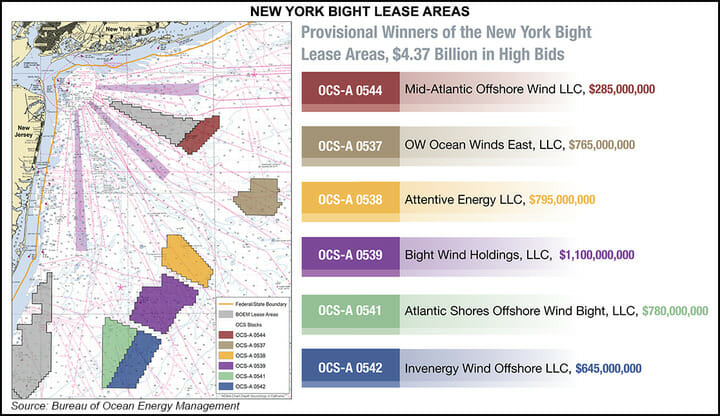

We include a couple of headlines and charts in today's daily report that step into the central theme of this week’s ESG and climate report, which will be published tomorrow (see here). The offshore wind ambitions and the EIA solar and battery projections both assume that the materials are available to build the capacity. In the case of the offshore wind leases, the winning bidders do not need to be in the market for all of the projects today and while the opportunities will lead to a step-change in demand for turbines in the US, the timing is less clear today that it will be in a few months and that timing may be adjusted to reflects equipment timing and costs, etc.

The linked Siemens Gamesa news could not have been a more clear example of one of our key research themes of the last year – backlog up, suggesting strong demand for new wind power capacity – deliveries and profits down because of material shortages – price inflation and logistic issues. While the company is getting squeezed because of higher costs on contracts that have limited opportunity to pass through the cost, at the same time slide 8 of the earnings release deck shows that selling prices rose in fiscal 1Q 2022. This breaks a declining trend in pricing and one of the core assumptions behind many energy transition plans – that renewable power prices can keep falling. Onshore wind orders are falling, but offshore orders are rising – and these come with higher costs and the need for more materials as we showed in a chart in yesterday’s daily. The added costs burden of more offshore wind projects may only serve to tighten markets for materials further, leading to further increases in installed costs.

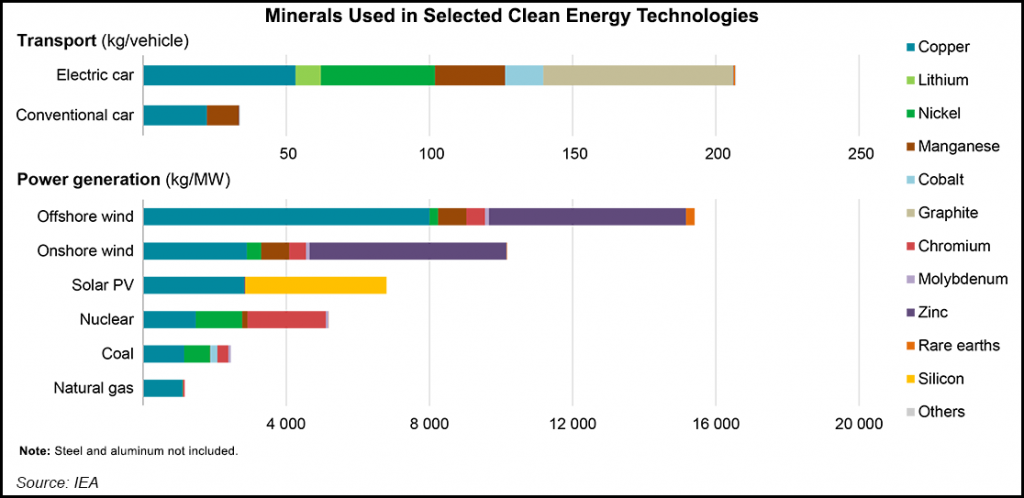

The materials chart in the exhibit below from today's daily report, is worth noting as it highlights all of the materials that are needed to advance the production of equipment required to drive renewable power production and demand. We would make one change to the chart in that lithium should also be added to the wind and solar categories to account for storage that needs to be built, although this could be done through hydrogen production or hydraulically, depending on location. One of our primary concerns concerning renewable power projections is the availability of some of these materials and we have written about the topic at length – most comprehensively in - 2022 – Policy Key, But Inflation Will Distract – Maybe Beneficially.

While we would generally avoid quoting work from a company that we might consider a peripheral competitor, we are happy to do so when it backs up one of our central themes – in this case, inflation in renewable power costs. The quote is taken from the Wood Mackenzie report flagged article linked here and discusses a view on how challenges that renewable power installers have faced in 2021 will extend into 2022. The quote talks about shortages of renewable power equipment, and the obvious consequence will be higher prices for that equipment, especially as raw material prices for components remain high and possibly move higher. In our ESG and Climate report today, we talk about the need for some commonsense oversight such that impractical ESG investing targets do not limit the ability of producers of critical fuels and materials to operate.

The core message of the IEA analysis published today is around how renewable power rates of investment remain far too low and need to more than double immediately to meet net-zero goals – see below. This analysis is very supportive of our renewable power inflation thesis, as none of the renewable power component manufacturers can double production either cheaply or quickly, and none of their suppliers has that much spare materials capacity. On the solar front, we may have the additional problem of regional production concentration. China has the largest share of capacity for solar module capacity and now has much more aggressive plans for solar power domestically. We could see China-based components stay in China, exaggerating shortages outside China. The IEA has an accompanying report today on the possible impact of commodity pricing on solar and wind pricing and it is also linked here – these reports were published this morning and we will cover them in more detail in next week's ESG and Climate report. More on this in today’s ESG and Climate report.