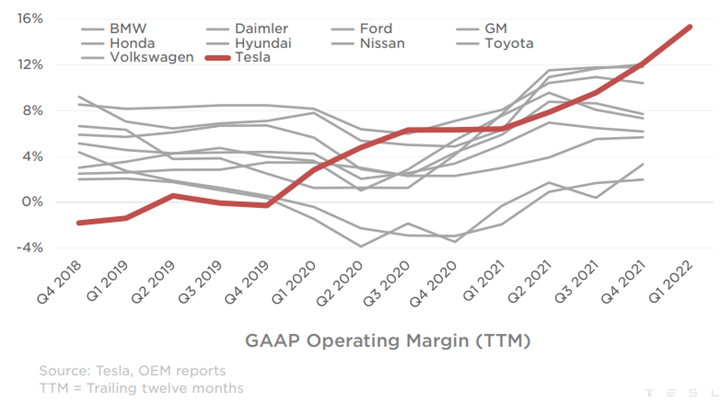

Tesla is on a roll, and showing other EV makers what is possible. The company priced its vehicles to be profitable at lower volumes and is currently seeing the benefit of scale, likely to be enhanced further as the manufacturing footprint grows. While the operating margin below looks very good, we would note that Tesla is not done scaling yet so there is considerable upside to the margin, most likely. One obvious conclusion from this analysis is that Tesla has plenty of wiggle room on pricing should macro conditions impact new car sales or should other EV makers try to steal share with pricing. Tesla has built a huge first-mover advantage in EVs and this will likely benefit the company for many years to come as long as they keep making vehicles that people want.

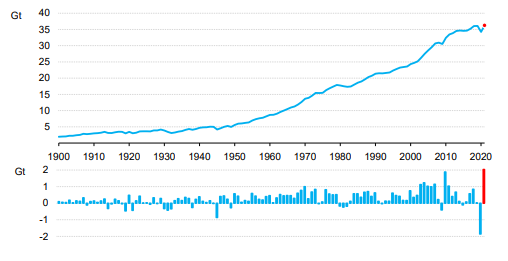

The IEA CO2 emissions data is not a surprise as it has been telegraphed for a while by several commentators that the world went backward in 2021. There were several causes, not least of which was an economy which, with the benefit of hindsight, was overstimulated, pushing up demand for resources in general, including energy. There has also been an overestimation of the rate of investment in renewable power, something which is finally gaining attention more generally, triggered by the energy supply fears that have emerged from the Russia/Ukraine conflict. It will take time to make the very large investments needed to abate the CO2 associated with industrial and consumer activity and there is no overnight fix. Accommodative policies are needed today for investments that will start a decline in emissions several years from now.

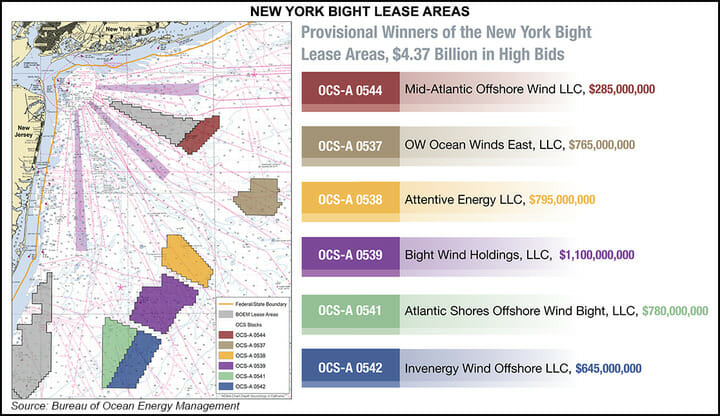

We include a couple of headlines and charts in today's daily report that step into the central theme of this week’s ESG and climate report, which will be published tomorrow (see here). The offshore wind ambitions and the EIA solar and battery projections both assume that the materials are available to build the capacity. In the case of the offshore wind leases, the winning bidders do not need to be in the market for all of the projects today and while the opportunities will lead to a step-change in demand for turbines in the US, the timing is less clear today that it will be in a few months and that timing may be adjusted to reflects equipment timing and costs, etc.

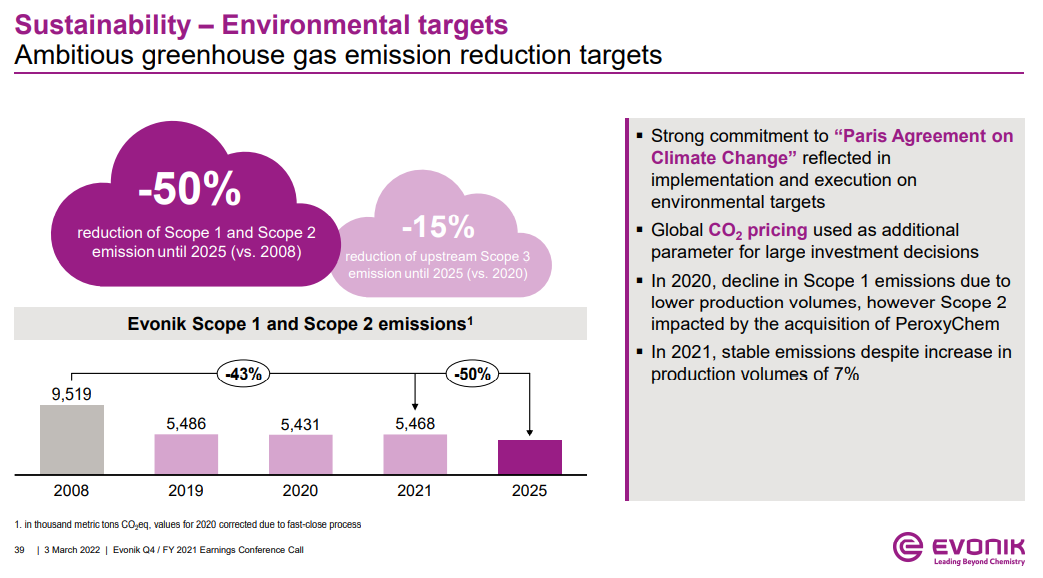

The Evonik discussion around CO2 prices is both relevant and important as CO2 values will be a critical component of investment decisions for many industries going forward. Those waiting for explicit guidance on CO2 prices are likely to be disappointed as we are not seeing much global coordination today and as we discussed yesterday, the European market, which had been the better indicator in our view over the last 18 months, has collapsed in the wake of the Russia/Ukraine conflict as some countries ask for it be suspended, while speculators are assuming that lower gas supplies into Europe will lead to lower emissions and less demand for credits. One of the options here is to take the bp approach and assume a carbon price in investment decisions. Early last year, bp indicated that it would fix on a carbon price of $100 per ton in its longer-term planning. We believe that this is a ballpark steady-state for CO2 pricing but that traded prices could be quite volatile around that level, depending on the mechanisms used. But even if we have a consistent carbon price, we will see significant changes in industry costs and competitive cost curves based on the various costs of carbon abatement. We have written in the past that we could see huge benefits to the US manufacturing base because of the combination of relatively low-cost hydrocarbons and relatively low-cost CCS opportunities. By contrast, we see costs rising steeply in places like central West Europe, where the local CCS opportunity is off the table. Even if Europe can produce cost-effective blue hydrogen on the coast, getting it to central Europe will be an issue. The landscape is less clear in Asia, but we expect to see some competitive edge for countries with low-cost CCS options – Malaysia, Indonesia, Thailand, and parts of China. See more in today's daily.

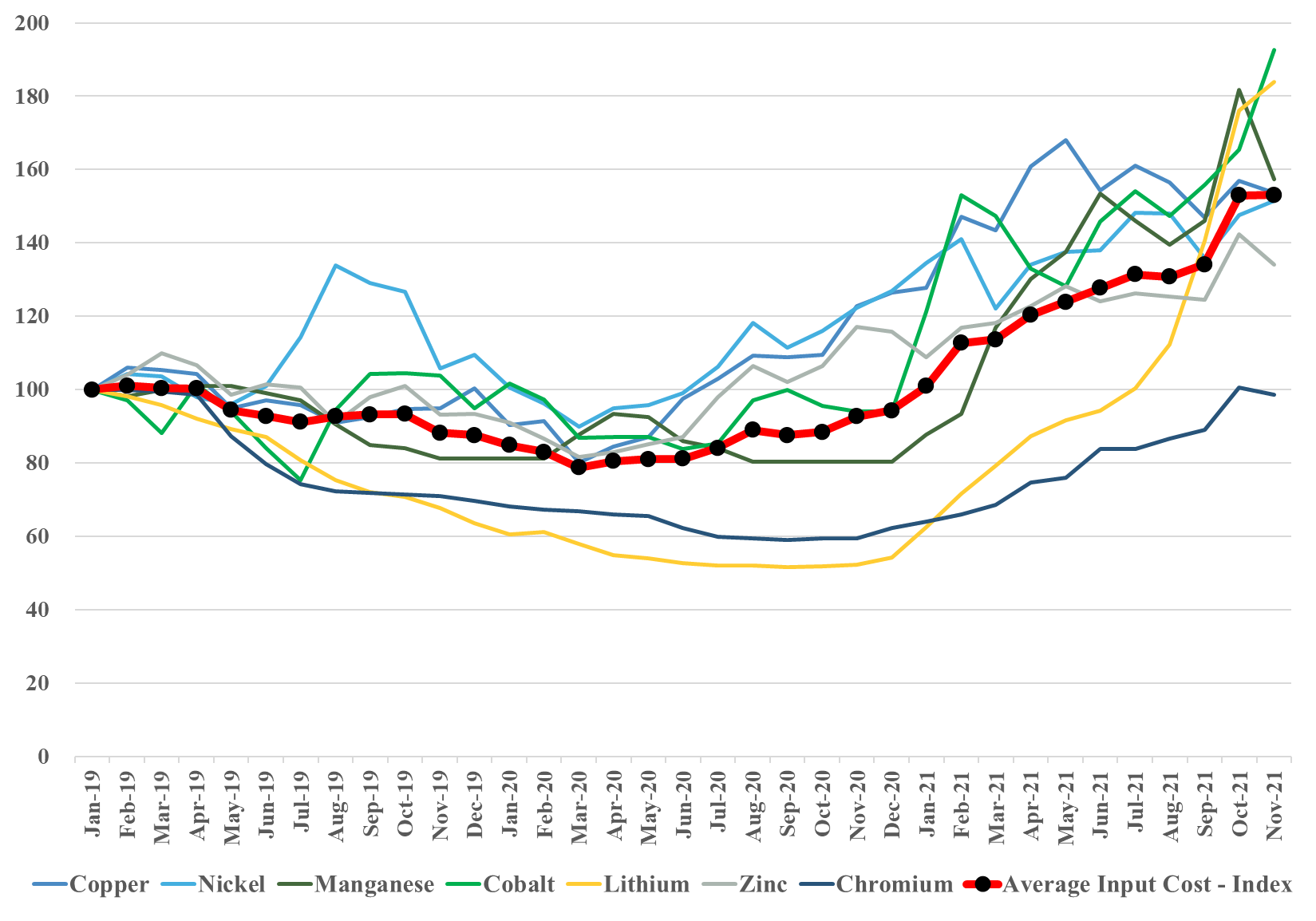

We focus today on raw material inflation and use the IEA analysis of materials demand (excluding steel and aluminum) in EVs and renewable power, creating a price index for the materials in question. This index is a straight average, but we will develop indices for specific sub-industries and include these in our next ESG and climate report. What is important is that the index below is up over 50% since the beginning of 2019 and this is before many of the EV plans and power plans move from planning to construction. We have highlighted inflation risk for more than a year now and remain very concerned that when many of the new auto plants start and many of the incremental renewable power facilities move from planning to equipment purchasing, we will see bottlenecks and faster price increases. See more in today's daily report.