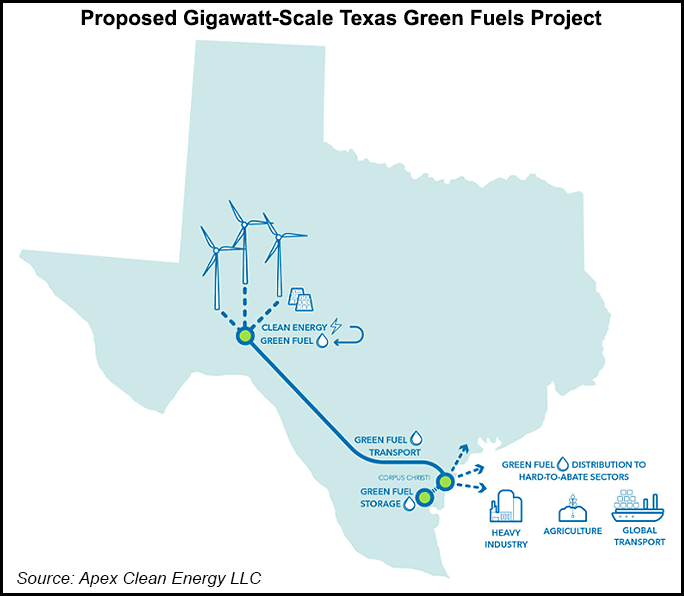

The Texas hydrogen hub is getting a lot of press and we also cover the idea in our ESG and Climate report today. We see this as not a lot more than intent today and would be surprised if any part of the project would be up and running, assuming it gets built at all, before the end of the decade. Green hydrogen economics do not (yet) make sense and some considerable efficiency learning curves need to emerge before any project could expect to make economic sense without significant subsidy. We have talked at length about the inflationary effects of material shortages and this is the core topic of our ESG report again today, where we suggest that a global recession may be the best thing for the renewable industry as it would slow other sectors' demand for critical materials. But the other wild card is renewable power demand, and how many industrial and materials companies along the Gulf Coast have their eyes on the same renewable power capacity to meet 2030 emission reduction goals. No one must buy renewable power today, because no one has 2022 emission goals. So, renewable power demand is likely understated and it is why the premium to buy renewable power in Texas today is quite low. Fast forward to 2030 – when promises have been made – and we will likely see demand spike and prices rise relative to conventionally generated power. This would materially impact the economics of the green hydrogen hub in Texas even if the electrolyzer costs could be reduced. Given the abundant pore space both onshore and offshore, blue hydrogen makes much more economic sense for Houston.

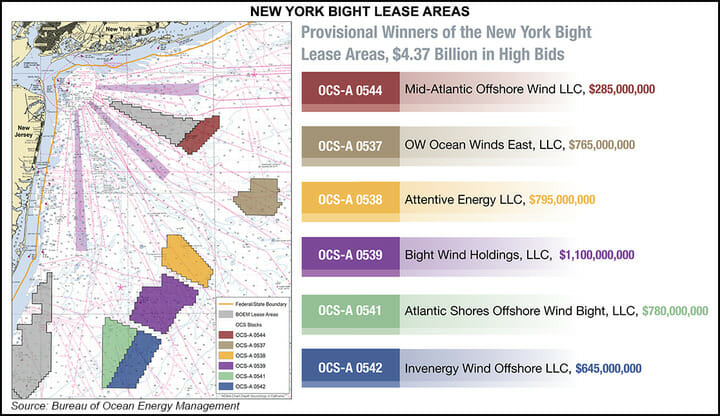

We include a couple of headlines and charts in today's daily report that step into the central theme of this week’s ESG and climate report, which will be published tomorrow (see here). The offshore wind ambitions and the EIA solar and battery projections both assume that the materials are available to build the capacity. In the case of the offshore wind leases, the winning bidders do not need to be in the market for all of the projects today and while the opportunities will lead to a step-change in demand for turbines in the US, the timing is less clear today that it will be in a few months and that timing may be adjusted to reflects equipment timing and costs, etc.

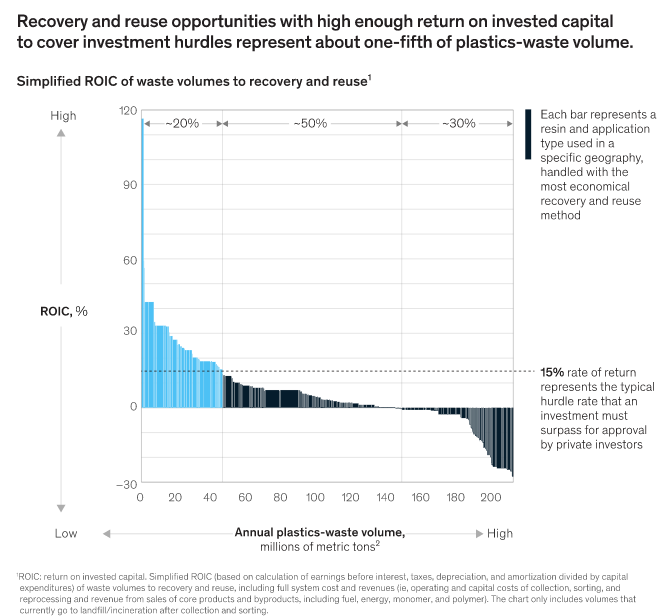

The McKinsey analysis is likely spot-on, as it is very difficult to get enough recycled polymer to produce a mechanically recycled stream that can be used in the highest value same use market. Solving for this is complicated by many factors, with too many stakeholders in many of the chains to make it work:

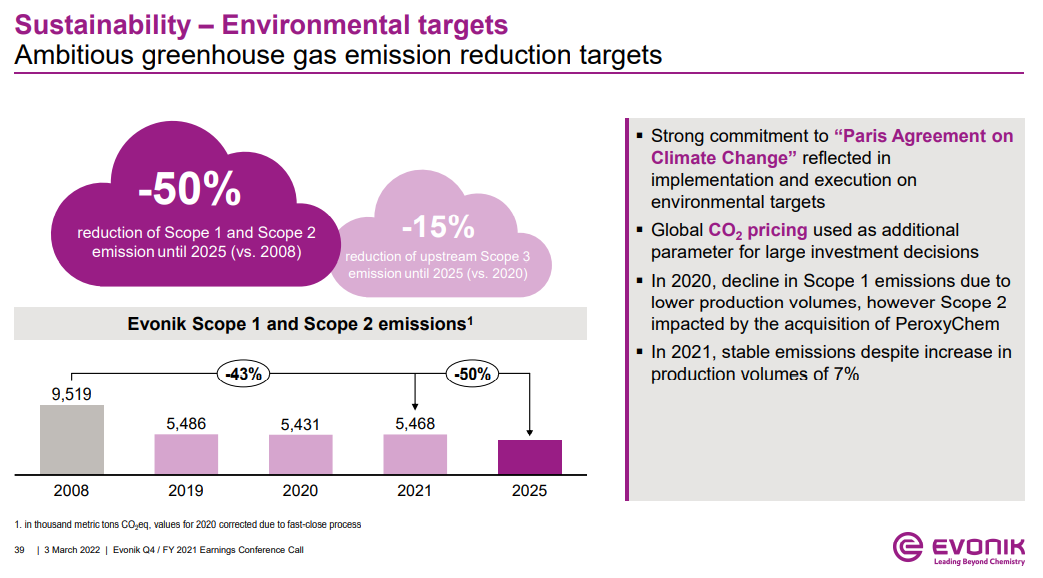

The Evonik discussion around CO2 prices is both relevant and important as CO2 values will be a critical component of investment decisions for many industries going forward. Those waiting for explicit guidance on CO2 prices are likely to be disappointed as we are not seeing much global coordination today and as we discussed yesterday, the European market, which had been the better indicator in our view over the last 18 months, has collapsed in the wake of the Russia/Ukraine conflict as some countries ask for it be suspended, while speculators are assuming that lower gas supplies into Europe will lead to lower emissions and less demand for credits. One of the options here is to take the bp approach and assume a carbon price in investment decisions. Early last year, bp indicated that it would fix on a carbon price of $100 per ton in its longer-term planning. We believe that this is a ballpark steady-state for CO2 pricing but that traded prices could be quite volatile around that level, depending on the mechanisms used. But even if we have a consistent carbon price, we will see significant changes in industry costs and competitive cost curves based on the various costs of carbon abatement. We have written in the past that we could see huge benefits to the US manufacturing base because of the combination of relatively low-cost hydrocarbons and relatively low-cost CCS opportunities. By contrast, we see costs rising steeply in places like central West Europe, where the local CCS opportunity is off the table. Even if Europe can produce cost-effective blue hydrogen on the coast, getting it to central Europe will be an issue. The landscape is less clear in Asia, but we expect to see some competitive edge for countries with low-cost CCS options – Malaysia, Indonesia, Thailand, and parts of China. See more in today's daily.

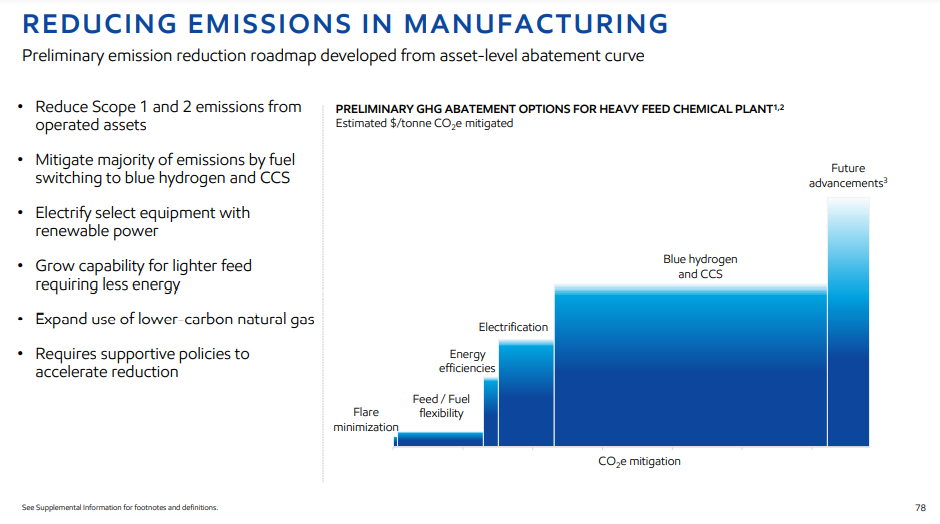

Playing right into the central argument of our ESG and Climate report is today’s ExxonMobil investor day, and we include a couple of key slides around the company's proposed path to net-zero below. The first slide shows just how much blue hydrogen (with CCS) the company plans to add to offset its emission-generating fuels – the volumes implied in the chart are high.

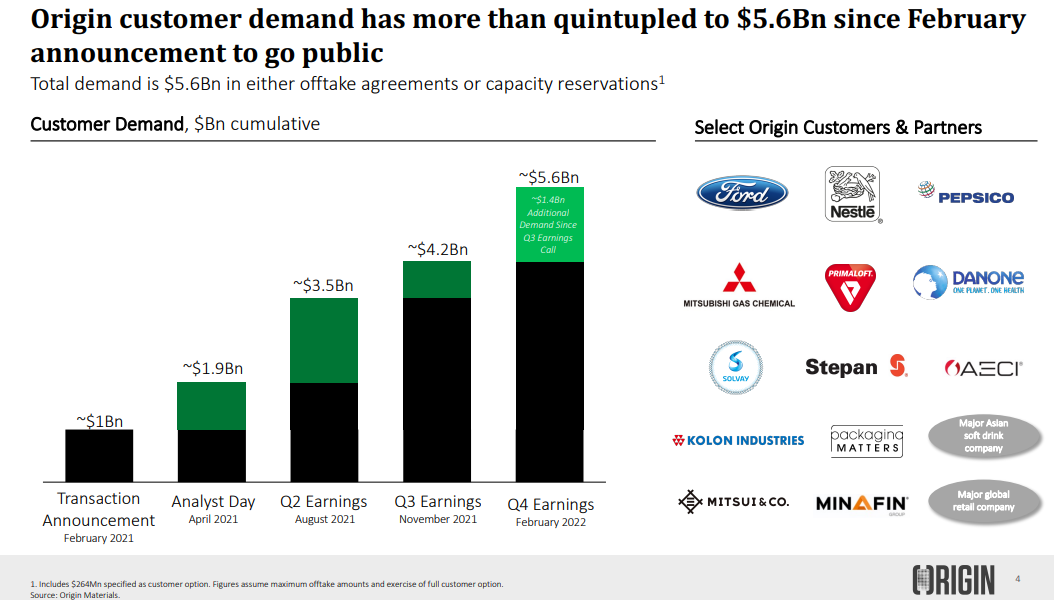

Origin Materials reported earnings yesterday and the highlight was the further increase in possible customer demand for the products the company plans to make, as well as the recent announcement of a second US plant. In our ESG and Climate piece on Wednesday, we talked about how important it is going to be for these new technology companies to have bankable offtake agreements, as these will be needed to support funding, given the more cautious outlook that the market has towards project finance today and the concerns over rising rates. The products that Origin expects to make should have robust demand, and they should attract a whole bunch of interested customers, all of whom are struggling with their own ESG dialogue. The question around Origin is whether the technology can deliver the products at costs that make sense and in reliable volumes. The story looks good if the process does what is promised.

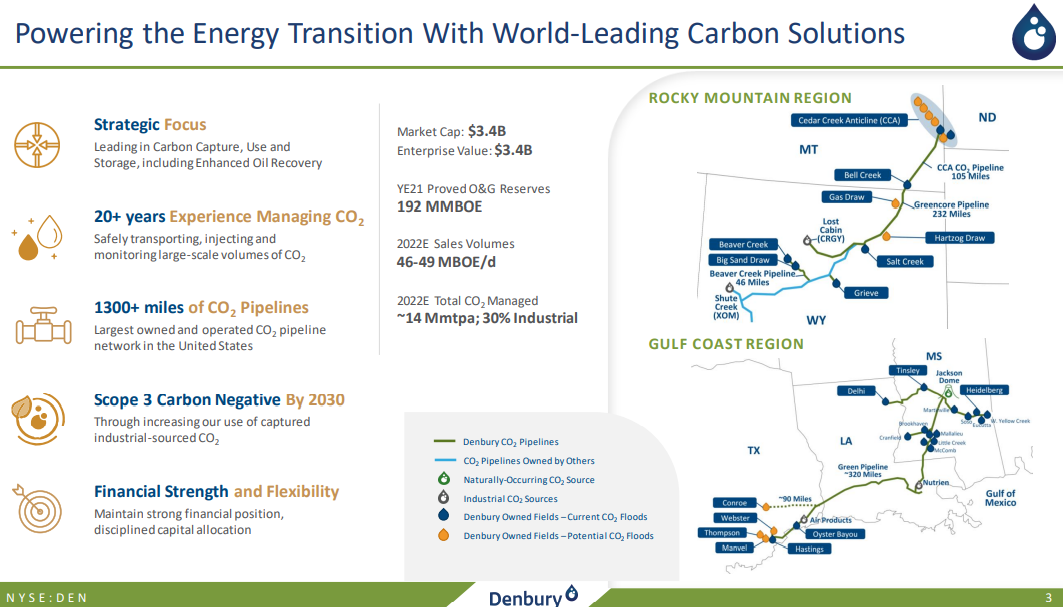

The Denbury release is a great example of something that we discussed in our ESG and Climate piece yesterday. The company is putting stakes in the ground concerning carbon capture and storage but is only really spending on its EOR opportunities, which of course look really interesting today. While the 45Q credit for EOR helps, the main driver is the incremental crude oil volumes that you can pull out of the ground because of the CO2 injection – the higher the price of crude oil the greater the value of EOR. Regardless of the tax credit, the economics of EOR should look very good today and it is not surprising to see several initiatives from Denbury given that it has a lot of existing infrastructure for CO2. The CCS plans are no different than some of the projects we discussed yesterday – they are stakes in the ground – marking territory – but unlikely to move forward without higher incentives. One of the core topics of our report yesterday is whether the conflict in central Europe will turn attention away from energy transition and energy security for tomorrow, because of the acute distraction of both energy and national security today.

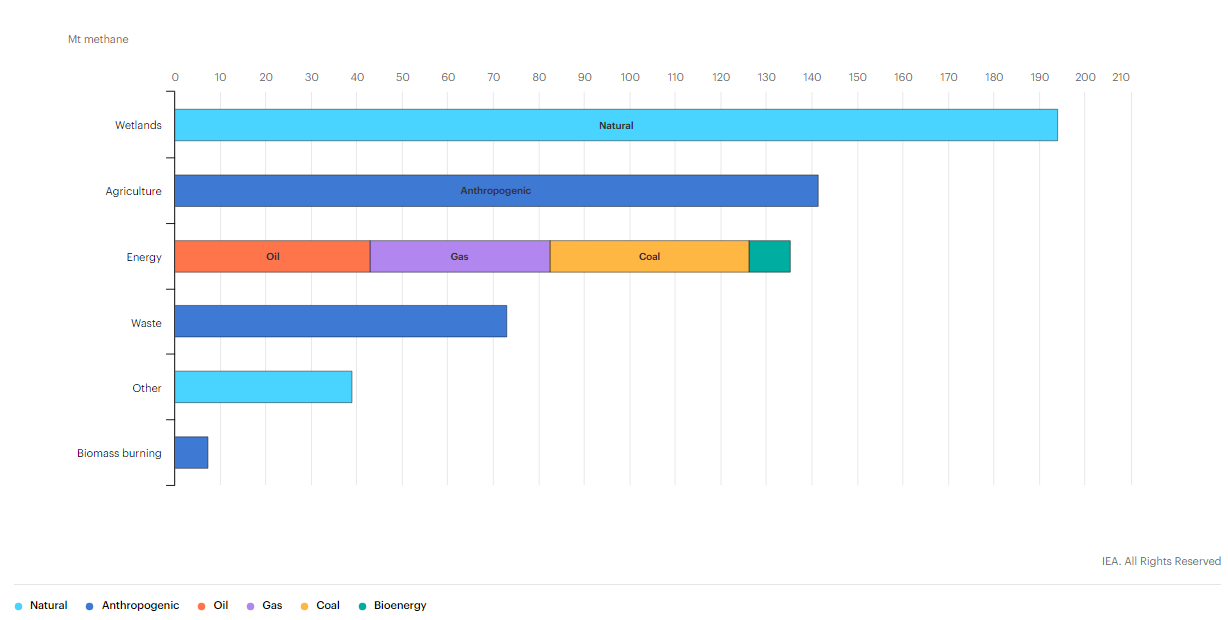

We have noted several renewable natural gas initiatives in the US and the data in the chart below shows how much methane is emitted by agriculture – the largest source after natural leakage. The agriculture-based RNG projects only make economic sense today where you have access to very large farms, where customers are willing to pay a premium, or where you qualify for incentives. That said we expect more projects, with growth stories at companies like Archaea Energy dependent on building new projects. The chart also shows how much emissions flow from the energy industry and this has been a more acute focus for remediation since COP26. See more in today's ESG and Climate report.

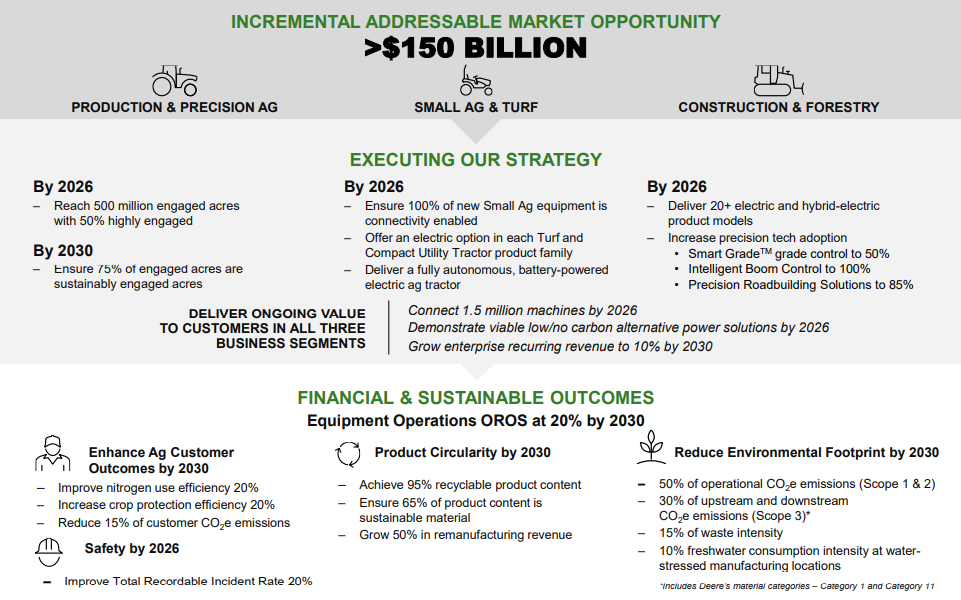

When we highlighted the Ag equipment names as interesting in our daily report earlier in the week, we had not realized that a Deere earnings announcement was imminent. The high farm profitability in the US is giving farmers some freedom with spending at a time when the equipment makers are hitting the market with some exciting new products – especially autonomous machinery – which can save on labor costs. The ESG angle here is further advances in precision agriculture, which can allow for more output for fewer inputs. There is also a very strong push towards low-till and no-till farming (to lower net CO2 emissions or increase CO2 capture) and this is an opportunity for the equipment makers to sell new equipment.

There should be little doubt that the US has a significant opportunity to decarbonize through CCS and if the US has a carbon value close to the level in Europe today we would be seeing investments announced almost weekly. While permitting would cause some significant lead time between announcement and construction/operation, the other uncertainty might be how best to capture the CO2. In its earnings release yesterday, CF talked about purifying CO2 streams at its two large Urea plants on the Gulf Coast, such that the CO2 would be ready to sequester, but the Urea process creates a relatively concentrated stream of CO2 and that makes separation much easier. For others, the better route might be hydrogen investments – driven by the relative ease of capturing the CO2, especially if it is part of the process design. If this route is more economic, the net new investment would be substantial, not just for the SMR, ATR, or fuel cell hydrogen generators, but also for the infrastructure and oxygen capacity for any ATR investment. This seems like a no-brainer bi-partisan opportunity for the US as there is broad support for CCS but incentives need to be higher. For more on this topic see our ESG and Climate research.