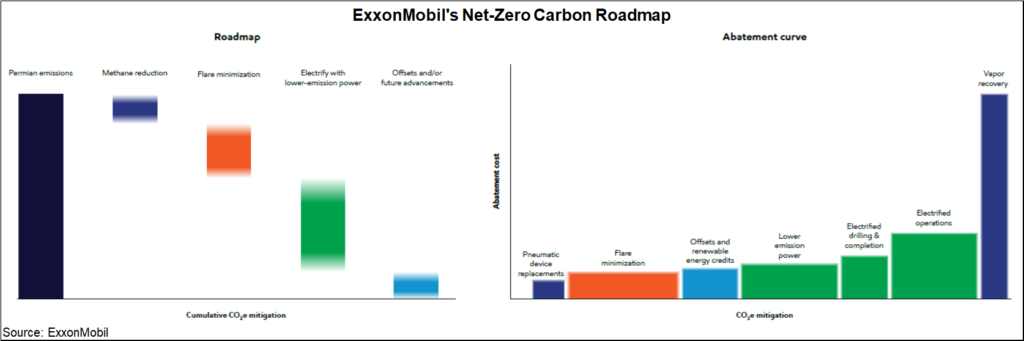

One piece of big news early this week was ExxonMobil’s announcement that it is developing plans that will drive net-zero emissions by 2050 and the company shared a detailed overview. We have picked some charts from the report, some of which can help us draw conclusions for ExxonMobil, but others are more general. The company is banking on a lot of emission reduction and CCS to get to the 2030 target and a large part of the goal is likely to come from the plans for the Permian and the previously stated net-zero target that the company has for 2030 – detail on how this will be achieved is shown in the Exhibit below, see more in today's ESG report.

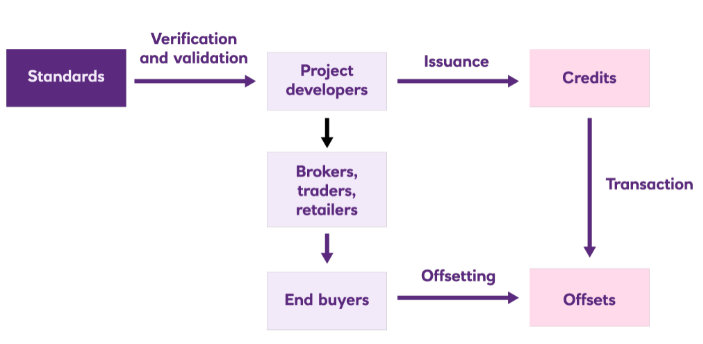

The carbon credit schematic below helps understand the mechanics, but the diagram does not sufficiently emphasize the critical importance of the “Verification and Validation” step. This is a great example of a mechanism that should work logically, but if the input is wrong the output will be also. Potential buyers and sellers of carbon credits understand the process well, but they are more concerned about what goes in the front end as the value of the credit will be very dependent on the quality. Today the only “sure thing” carbon offset is direct air capture, as all of the agriculture-based offsets need much tighter definitions. See research - Carbon Prices – Inequitable and Uncertain – Not What We Need

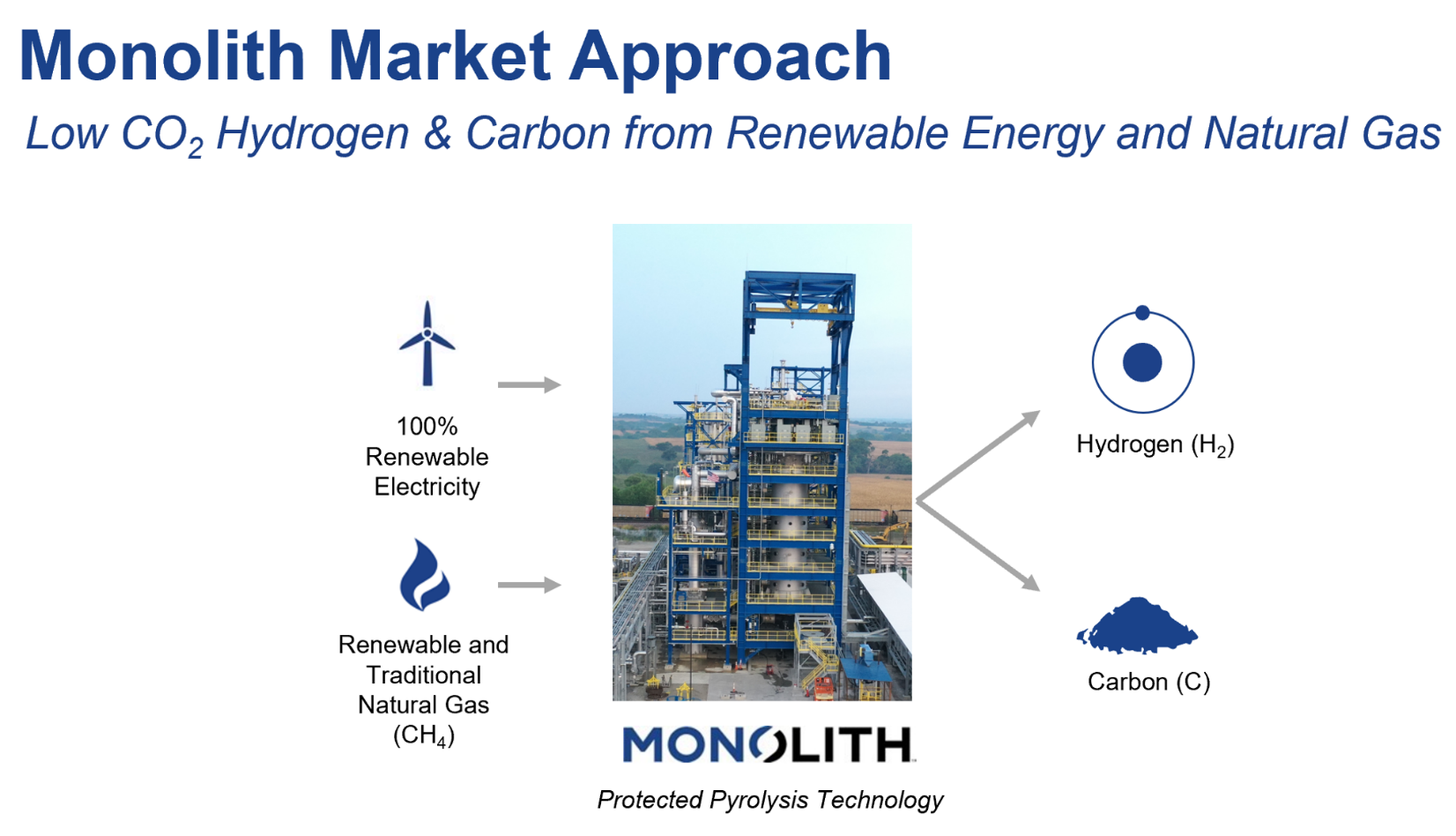

The Monolith announcement is not that surprising, as the auto industry is very focused on its carbon footprint and its suppliers, like Goodyear, are under pressure to look for more sustainable solutions. While Monolith uses natural gas as a feed, it’s carbon black is produced with very limited Scope 1 emissions, unlike the traditional route, used by the incumbents. It is not clear what the production economics are for Monolith because the co-product value of hydrogen could vary greatly depending on local needs, but the emergence of a competitor who sees carbon black potentially as a by-product is not likely to be good news for the traditional makers. A by-product that is more environmentally friendly is even more of a threat. Complicating the picture further could be the arrival of larger volume production from Origin Materials, which has a renewable based carbon black like material, which may also be seen as a by-product.

When China announced its 2060 net-zero goals we dedicated one of our ESG and Climate pieces to the topic - China: A Challenge With 2060 Goal But Also A Possible Edge - concluding that this would likely drive considerable competitive advantage for China assuming that others would bear the costs of new technology learning curves and China would get the solutions more cheaply. In interim China would have lower costs of manufacturing because of the delayed net-zero implementation. With the Biden administration now pushing for a coordinated 2050 commitment for the US, some of the burdens of early costs that China could benefit from also fall on the US. In one of the headlines (from today's report), there is criticism of the European CBAM and questions around whether it could work. The reality is that it, or something like it, has to work, otherwise asymmetric climate policies will create pockets of competitive advantage - potentially very damaging to those spending more.

In our ESG and Climate piece yesterday we briefly discussed the mid-west carbon capture projects, questioning their economic viability. Two of the most expensive components of any CCS project are pipelines and compression costs and we cannot see how a long network of pipe in the mid-west to pick up what are essentially small volumes can work economically. These projects are reliant on very high LCFS-like credits, and as we showed in last week’s report, LCFS credits have fallen this year and could fall further. The pipeline right of way issue is another major hurdle and we have seen growing resistance to pipelines of any sort over the last few years. Those who oppose CCS in principle could cripple these mid-west plans simply by co-opting enough land-owners on the path of the proposed pipelines and refusing access. We are supporters of CCS, but have done substantial work on economics and show that the process only begins to make economic sense if the sequestration is close to the emissions. Relying on possible artificially high carbon prices to justify the projects will only lead to pain, assuming the pipeline right of ways can be obtained.

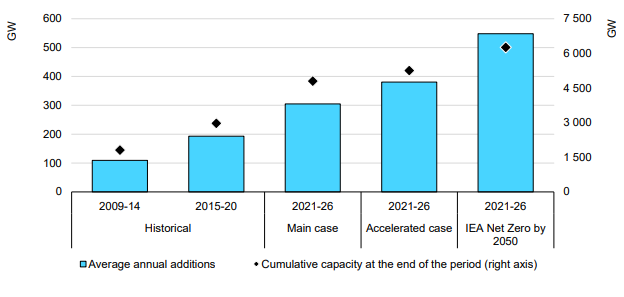

The core message of the IEA analysis published today is around how renewable power rates of investment remain far too low and need to more than double immediately to meet net-zero goals – see below. This analysis is very supportive of our renewable power inflation thesis, as none of the renewable power component manufacturers can double production either cheaply or quickly, and none of their suppliers has that much spare materials capacity. On the solar front, we may have the additional problem of regional production concentration. China has the largest share of capacity for solar module capacity and now has much more aggressive plans for solar power domestically. We could see China-based components stay in China, exaggerating shortages outside China. The IEA has an accompanying report today on the possible impact of commodity pricing on solar and wind pricing and it is also linked here – these reports were published this morning and we will cover them in more detail in next week's ESG and Climate report. More on this in today’s ESG and Climate report.

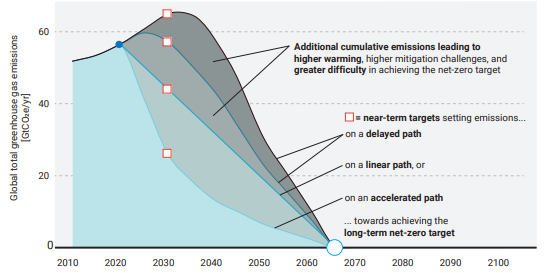

In a media interview earlier this week (more details to follow) we were involved in a discussion about inflation and specifically energy. The discussion covered much more than this, but the chart below is perhaps one of the easier ways of showing where our concern lies, and it ties directly to the behavioral patterns that are emerging concerning climate change and ESG focused investing. As noted in the title of the chart, the likelihood that the linear path from here to net-zero will work is very low, given that we would need global government coordination now, and we are far from it. The other scenarios are much more likely, at least in the early years, and they call for an increase in emissions, which implies growing demand for fossil fuels and other materials that have a high emissions footprint. If you are an oil or gas producer and you look at the chart you could quickly conclude that while your products are in demand today and likely to be in growing demand for several years, the longer-term outlook is very unclear. This might slow down your investment plans, or at least make you think twice about the shorter lead-time projects – such as on-shore and shale-based. However, it could kill any longer-term offshore/deepwater projects that take many years to bring on stream. Today we see energy investment hesitancy everywhere (see our Chemical Blog), but at the same time, we do not see the global coordination to drive a faster energy transition, assuming we had the materials and the investment dollars to move any faster. The risk that we run out of produced fossil fuels from time to time over the next 3-5 years is very high.

In our ESG and Climate report tomorrow we are focusing on the very wide range of carbon prices and the structures of the various emission reduction incentive schemes, with a focus on what it does to the competitive landscape within the impacted markets. For example, with the government subsidy being offered to BASF and Air Liquide for the CCS project in Antwerp, some level of competitive edge will be granted to the companies, because similar subsidies might not be available to others. Last week we discussed the very wide range of potential carbon abatement costs for companies in the same business, driven by technology and geography. If we add to that the potential for some projects to attract subsidies, while others do not, we change the landscape of the competitive playing field. Could we, for example, see BASF shutter production in Germany, where abatement costs are high, and move more manufacturing to Antwerp – something likely to be very unpopular with the German government and trade unions. This is more problematic in Europe because of the open trade policy. For Germany to give the same benefit that BASF has at Antwerp to chemical manufacturers in Germany could be prohibitively expensive given the much higher inland costs of CCS in Europe, assuming any permits would be issued. Alternatives to CCS, such as the electrification of industrial heating processes or the use of hydrogen as fuel might be equally expensive. We see some of the select European subsidies possibly causing discord between the member states.

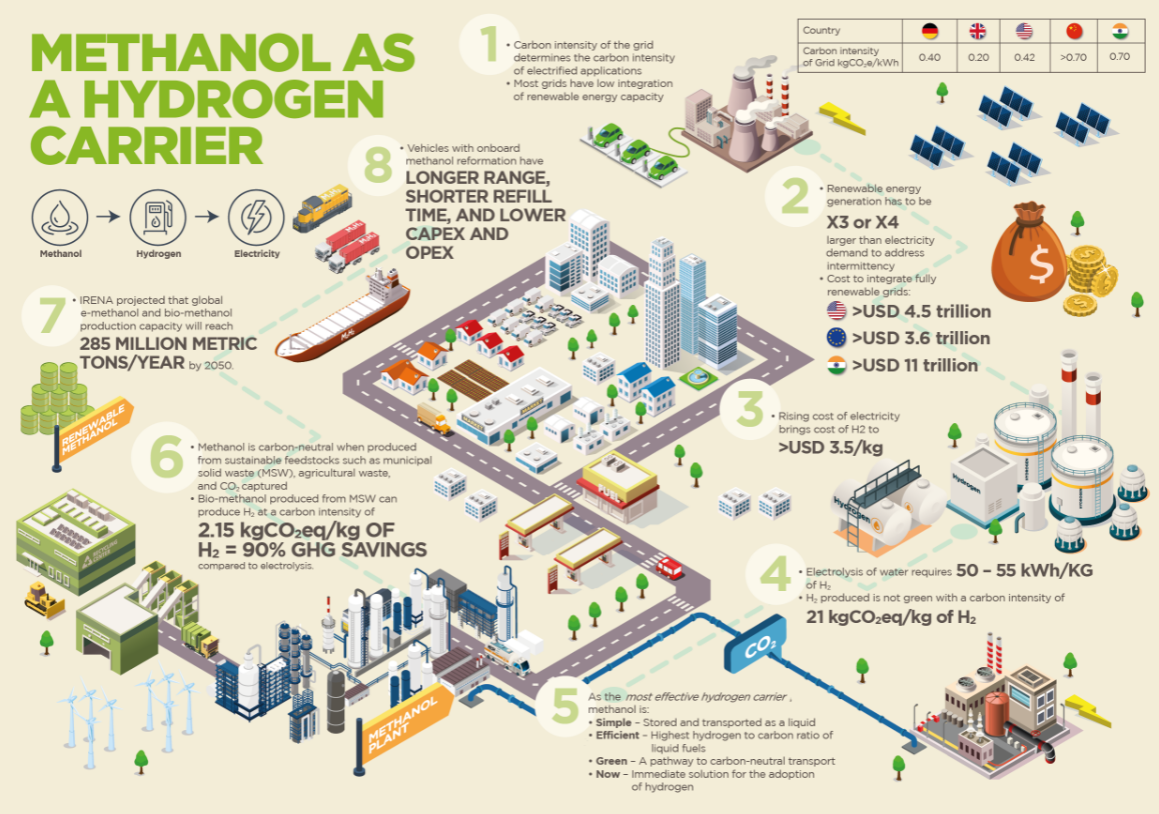

We are going to focus our Sunday Thematic this week (will be found here) on a couple of related topics: alternative technologies that only make sense when prices are high, and whether this has changed with ESG and climate pressure, and ESG solution fixation – “methanol is the only solution” – see infographic below – or it’s hydrogen or ammonia or batteries. Sticking with the theme that seems to have hit a chord with COP26 attendees and something that we discussed in a report around carbon capture several months ago – we cannot let a foolhardy quest for “perfect” get in the way of more economic “good enough” solutions. The emission issues are generally site and process specific and different solutions will be more practical and affordable for different processes and in different geographies – there is no “one size fits all” solution.

ExxonMobil is seriously upping its lower-carbon game with the CCS announcements over the last few weeks and the release this week that states the company will spend $15 billion over the next 6 years on lower carbon initiatives. In this linked headline ExxonMobil states that it will meet its 2025 emission goals this year – we are assuming that this must be correct as the company would not want to risk the accusation of greenwashing. Either way, the critics will weigh in, either claiming “greenwashing” or suggesting that the targets were not high enough, to begin with. The ExxonMobil focus is very much on CCS, which makes sense for an oil and gas-centric company whose only real play right now is to lower the carbon footprint of its fuel portfolio. In the release linked above, ExxonMobil also talks about biofuel and hydrogen initiatives, but again calls for supportive policies from governments and we suspect that the underlying push here is towards the US government. ExxonMobil and others have indicated that $100 per ton is the right incentive to drive CCS and other carbon abatement strategies and we would agree with this estimate as it backs up much of the work that we have done over the last year. See - Carbon: Trading, Offsets, and CCS as a Service – It’s All Coming! and - Carbon Games – Appetite, But Not Enough Hunger Yet. The other reason why ExxonMobil and others would like to see the US act is because other jurisdictions in which they operate will likely take a lead from the US.