In our ESG piece yesterday we talked about the competitive edge that Canada now has with respect to both natural gas (because of lower prices versus the US) and CCS, both because of relatively low costs but also because of the clear value on carbon. Yet today we see an announcement in the US!

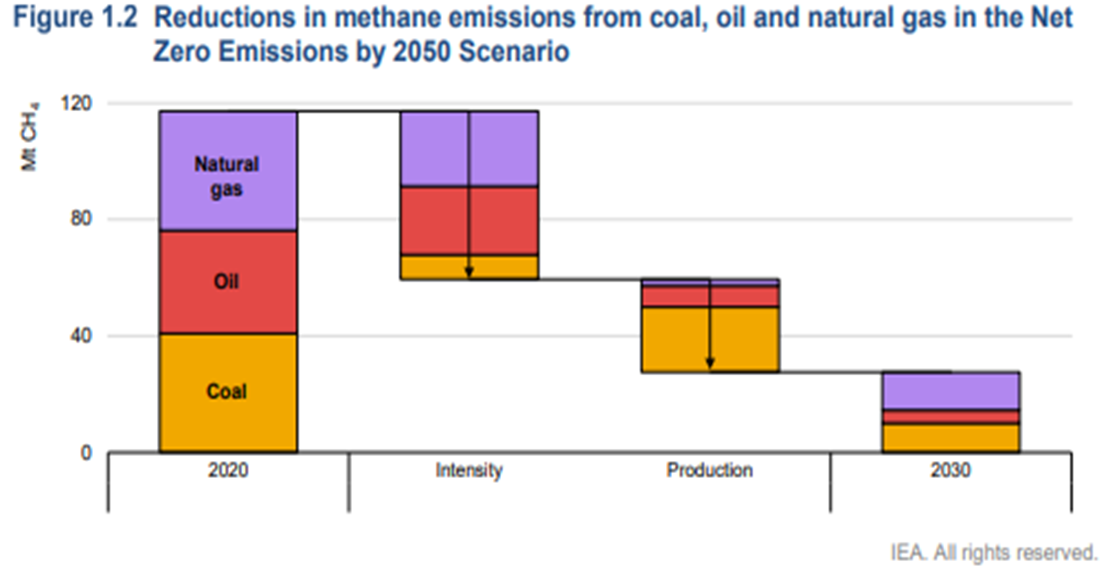

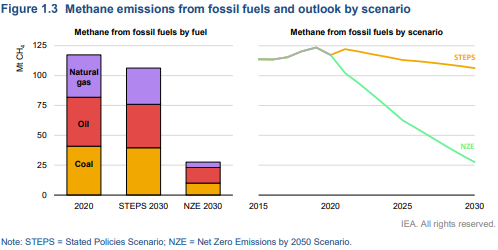

A couple of things worth highlighting in today's daily report – the first being Chevron’s move to join the net-zero club – focusing all eyes now on ExxonMobil in particular but also the rest of the US E&P crowd. Chevron will have some major challenges getting to net-zero and will likely face much of the same skepticism that bp, Shell, and TotalEnergies attracted in Europe initially and still face today. The Europeans have placed a lot of their bets on moving into renewable power – for the moment, Chevron is focused on moving to net zero in its own operations, which we read as biofuels and a lot of CCS. Given the acute shortage of international natural gas, it would make the most sense for the independent natural gas E&P companies and the LNG sellers to jump on the same boat. By promising low carbon natural gas and LNG, the industry is much more likely to gain support for the expansion that the world needs to counter some of the EIA assumptions around coal and petroleum product use from 2030 to 2050. Of course, it would be a whole lot easier for the US industry to do this if they had a value on carbon to work with! The chart below looks at one of the core clean-up issues, which is methane leakage. This is a subject we cover extensively in our ESG and Climate service linked here.

The methane chart below is another reminder of how important it is for governments to increase their demands on methane emitters to find solutions to cut leakage. The current stated policies are grossly inadequate, and while we are seeing some of the majors taking proactive steps to reduce emissions, the problems are more acute among the independents in the West as well as abandoned wells that might have no current ownership and operators outside the US and Europe. We keep talking about the need for COP26 to focus on natural gas, and this would be one of the key issues on which a global agreement would help. See several of our ESG reports for more on this subject.

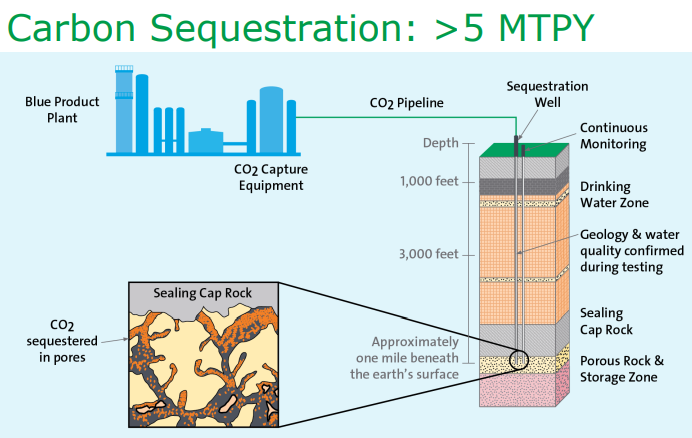

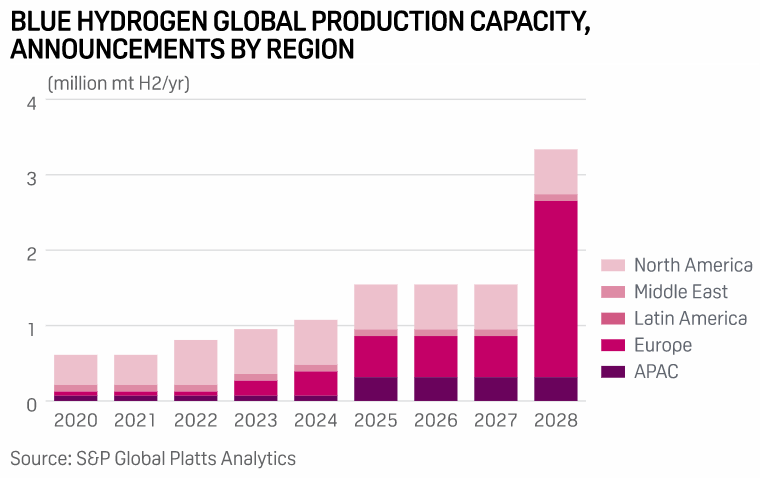

The carbon capture plans lacking a place to put the CO2, suggested in the two connected stories linked here (link 1, link 2), echo something that we have been highlighting for a while. There have been several press releases with respect to CCS – partnerships – plans to accompany new investments – gathering schemes for the ethanol industry, etc. but none have any specificity around where they will put the CO2. The Houston team, discussed in a recent report is talking about offshore Texas, and given both ExxonMobil and Chevron in the partnership, we do not doubt that there is a plan, but in general, the permit activity at the EPA is, we understand, quite limited today. To apply for a class 6 permit, applicants need to have a detailed analysis of the sub-surface that they plan to target, and once you have identified a location, there are likely at least 18 months of work to get into shape to submit the permit. Some of the oil majors may be able to move faster on acreage that they already have seismic models for, but it is a long process – we wrote about the need for 45Q to change in both value and duration in our recent ESG and Climate Piece.

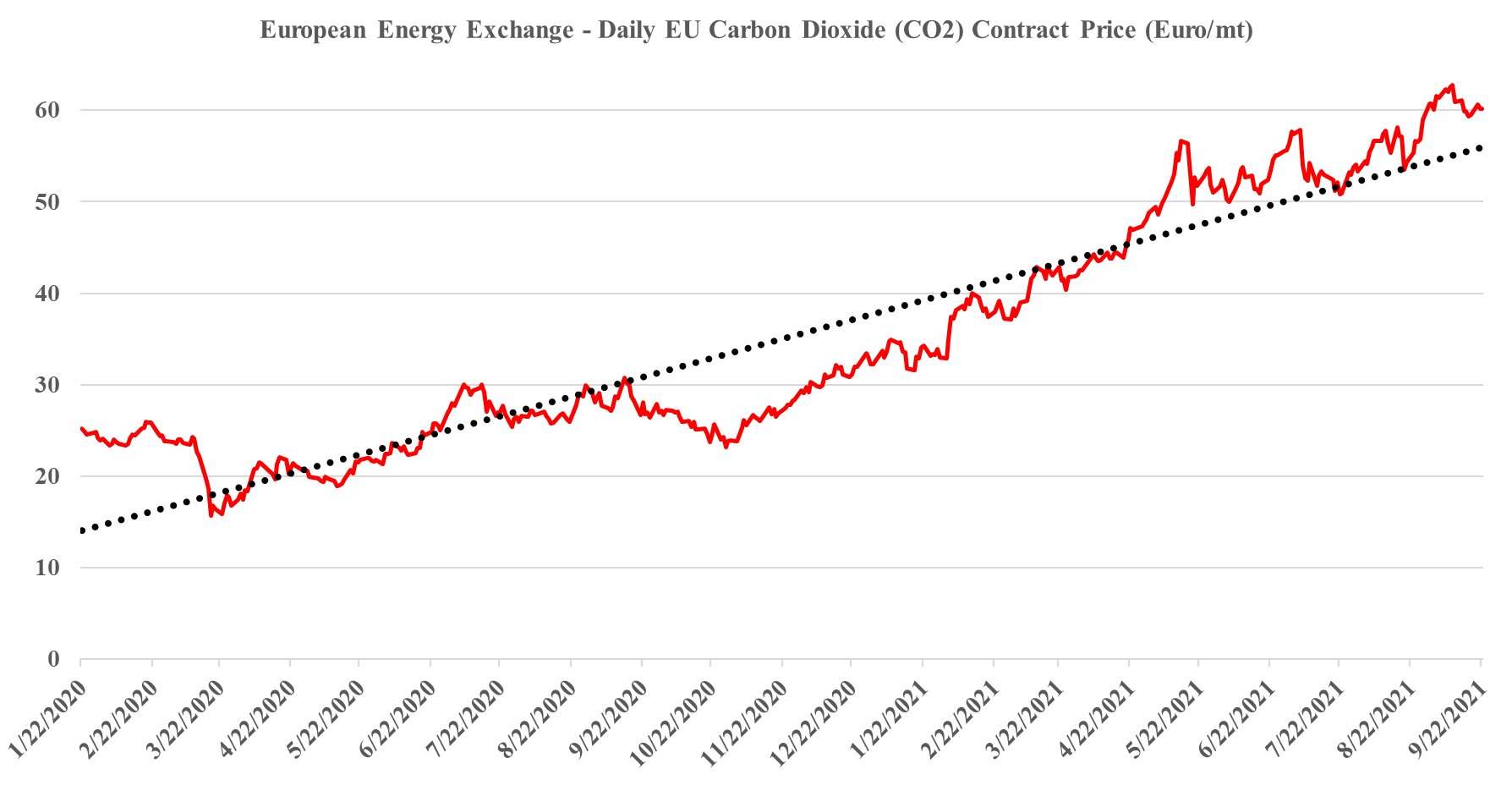

It is worth a short explanation of what is going on with European CO2, given the mixed signals of shortages in headlines today and then the slight weakness in pricing shown in the image below. These are two very different markets, with the food, beverage, medical and nuclear industries looking for pure streams of CO2 rather than the contaminated streams that make up the bulk of emissions. Historically, the food and beverage industry looked to fermentation – so alcohol production – as its source of a pure CO2 stream, but as demand grew, the next best place became ammonia production, which also has a pure CO2 stream as a by-product. Most ammonia is further converted into urea, which is a consumer of CO2 and there is not enough CO2 produced in a natural gas-based ammonia plant to convert all of the ammonia to urea. You sometimes see urea facilities also selling ammonia, but more frequently they take the carbon monoxide by-product of the syngas reaction and convert that to CO2. The result is enough CO2 to convert all of the ammonia to Urea and surplus CO2 to sell. Because of this more dominant supply of food and beverage grade CO2, and shutdowns caused in this case by runaway natural gas prices, have an immediate impact on the industries that rely on the CO2.

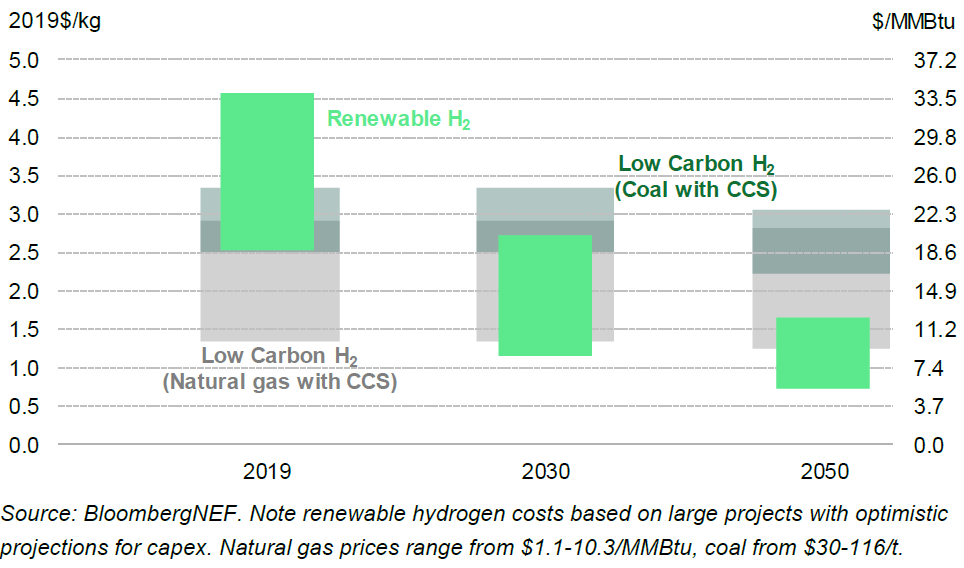

It is hard to ignore the number of headlines on hydrogen initiatives, today, highlighted in our ESG and climate report, as well as the acceleration in project announcements over the last several months. In the 80s in the UK, it was trendy to drive a VW Golf GTI – everyone had to have one – hydrogen has the same feel today – everyone has to have a project. The projects vary and fall into a handful of categories:

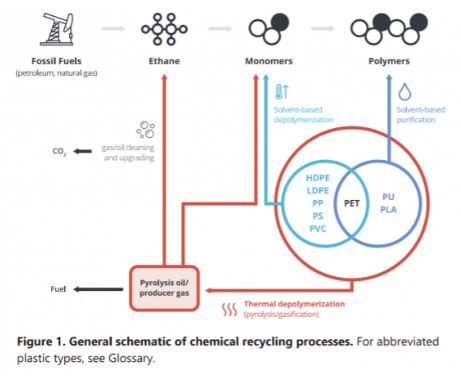

We believe that the plastics industry is right to get as much state backing for chemical recycling as it can – see Louisiana headline and diagram below. While chemical recycling is not as neat as mechanical recycling, it has far more chance of dealing with the core issue, which is the disposal of plastic waste – see report linked here. Our support for chemical recycling stems from the view that it will be very hard to get the behavioral change needed to ramp up mechanical recycling quickly and to a level that will impact waste.

The primary reason for the flurry of carbon capture related headlines in the US over the last few weeks – and our analysis shows a significant step up – is because it looks like this will be the one technology/route to lower carbon emissions that will get a real boost from the infrastructure bill. There is bipartisan support for CCS because the fossil fuel industry sees it as a way to stay in the game and the unions believe that it will create jobs. This combination should garner enough votes to push it into the bill and get it passed, although the details around how CCS would be supported remain unclear. The infrastructure bill has very few real sources of income in it to offset the very high costs – something we will discuss on Sunday – and consequently giving a bigger tax break, through the 45Q program would create an even larger funding gap than we have today. The value/cost dynamic has to rise to get the activity that everyone is looking for and maybe that could be achieved by overlaying a carbon credit onto the program. Anyone exporting to Europe and concerned about the CBAM extending to natural gas, NGLs, chemicals, and polymers would likely consider CCS if they were eligible for 45Q and could also claim an offset on their exported products to neutralize the CBAM tax/fee.

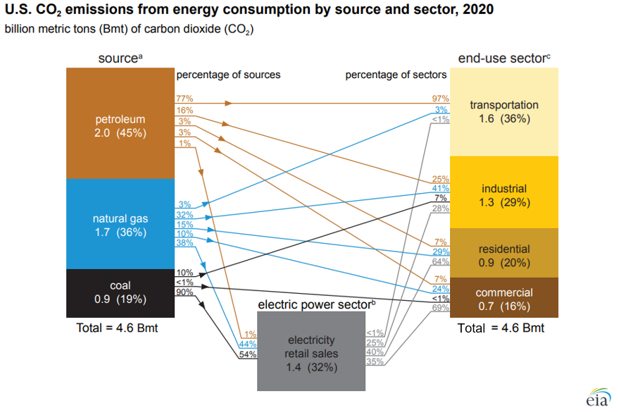

We are increasingly concerned that the US will remain a laggard concerning climate change initiatives given the major challenges of moving to the next steps and the bifurcated congressional views. The emissions reductions that the US has seen over the last 10 years have been more happenstance than planning, with the abundance of natural gas following the shale boom of the last decade creating economic reasons to replace coal-fired power with natural gas rather than environmental reasons. Lower costs for wind and solar power and focused industrial demand for that clean power have been the bigger driver of clean power investments. In the chart below, the decline in emission from the power sector is evident and it should continue. The diagram below shows sources and uses for US emissions in 2020, but the accompanying write-up talks about the step down in emissions overall in 2020. Except for the continuing electric power transition, most of the other 2020 declines are COVID-related and are expected to rebound in the near term, especially transport. The market share gains of EVs are not significant enough yet to make a difference. See more in today's daily report.

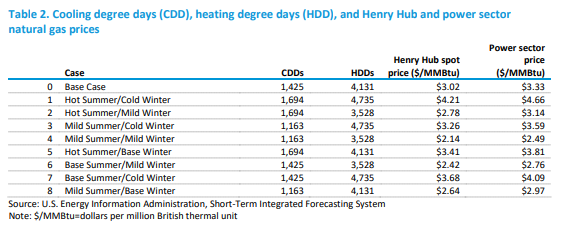

The table below is from an interesting analysis published by the EIA this week that focuses on possible power demand scenarios for the US – all weather-related – and then backs into the power sources that would be needed to meet the demand, concluding with the US carbon emissions that would correspond to each scenario. The conclusions should not be surprising, which are that carbon emissions rise disproportionately faster as power demand rises – as more coal is required to balance generation needs, and fall disproportionately more quickly as power demand falls (as less coal is needed). The analysis is effectively a study of how much less CO2 emissions are using natural gas to generate power versus coal. As renewable generation increases as a share of the total, however, the math will change, and the EIA study does not take into account the weather factor on renewable power, it looks at cooling degree days and heating degree days at a national level only. This is reasonable as there is likely not enough data to be able to put good reliability estimates yet around renewable power annual volatility and more importantly, the impact of weather on renewable power is likely to be short-term in nature. Perhaps this analysis could be improved by adding a “daily risk band” around each scenario, showing how much renewable power volatility could cause peaks in the high scenario and lows in the low, etc.