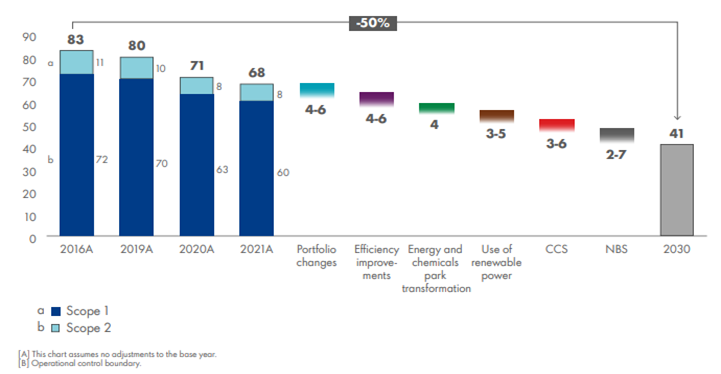

Shell issued its 2021 energy transition progress this morning and the report contains a lot of detail about what Shell has done so far and what the company intends to do. The report is a record of progress and intent and is targeting both general stakeholders as well as the Shell board and annual meeting, where approval of the plan will be sought. When compared with other reports we have seen from other companies, this summary is comprehensive. It provides some concrete steps to achieving emission goals in 2030 – exhibit below - while remaining appropriately vague about getting to 2040 and 2050 targets. However, we would note how much portfolio changes likely added to the 2016 to 2021 progress – likely proportionately much more than they are expected to contribute from 2022 to 2030. Both renewable power and CCS figure in the 2030 projections below and Shell will need to get moving on the CCS front of it is to sequester 3-6 million tons of CO2 per annum by 2030. The expectations are likely based on the European offshore projects, as it may take longer than 8 years to get permits and investments in place in the US. The US could move faster but the EPA would likely need to grant primacy to at least Louisiana and Texas for things to speed up and we are not convinced that this will happen soon. Like many of the other company 2030 plans that we have seen, it is likely that much of Shell’s progress will come in the last couple of years of the decade – especially on CCS.

In our ESG and Climate report tomorrow, we will focus on SAF from a carbon intensity perspective. The Colonial pipeline initiative was inevitable given the demand for jet fuel at the East Coast airports. Still, we would not expect much volume to move in the near term for several reasons. First, there is not that much to move, and second, California can still pay more because of the LCFS credit. The Biden administration is planning to introduce a broad SAF credit which would help encourage use outside California, but this would also need to stimulate production as the volumes are still small and much smaller than the airlines would want – even the projection of volumes by bodies like the IEA fall well short of potential airline demand by 2030 and 2040. This is an investable theme, in our view, and we will discuss it in more detail tomorrow.

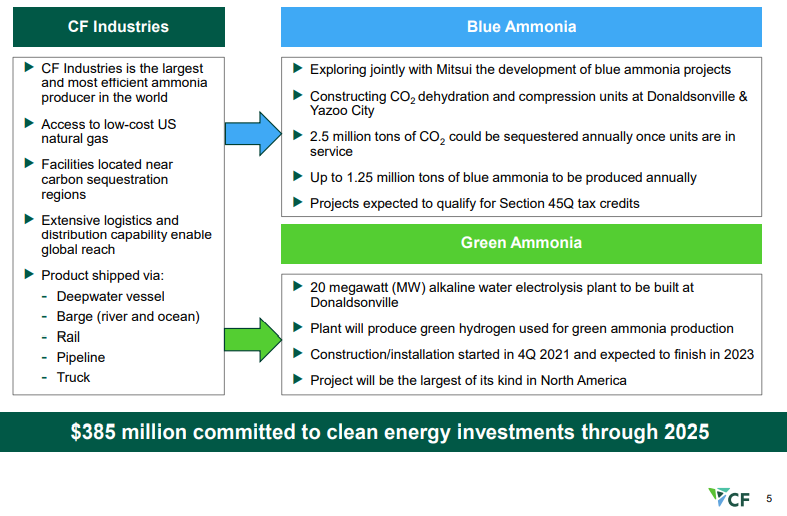

We continue to believe that the US has a cost advantage in CCS versus many of the other regions of the world and that when coupled with low natural gas prices the US should be able to take a lead in developing low carbon chemicals. CF is pushing the idea of both blue ammonia in the US as well as green ammonia, and while the company has yet to announce sequestration plans for the CO2 it is working to purify – see Exhibit - once dehydrated and compressed the incremental cost of storage should be low.