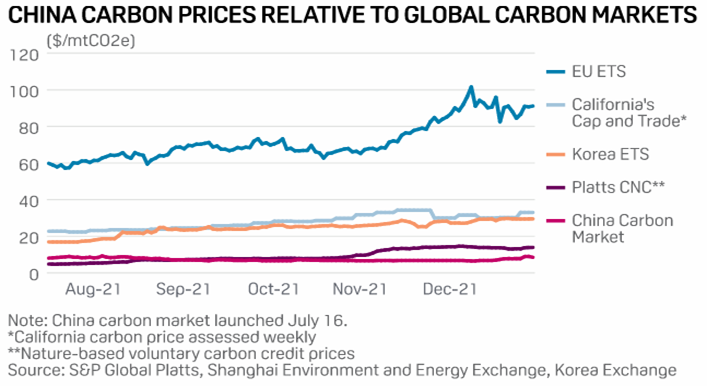

Despite the “soaring” carbon offset market in the FT article linked here, we would remind clients that this is something we have written about extensively and that while “nature-based” offset prices have jumped over the last year they remain very low compared to the physical cost of carbon abatement, whether through reforestation or physical abatement for CO2 emitting fuels and processes. The nature-based credits should at least rise to the physical cost of planting trees and maintaining forests (adjusting for the risk of fires etc). This is well above $50 per ton in our view and maybe as high as $100 per ton depending on how you define the costs. The very low price today, despite the recent rise, reflects an oversupply of credits perhaps, but it may also reflect buyers' unwillingness to pay more because of the uncertainties around accuracy and chain of custody of the credits. If the credit truly reflects the removal of 1 ton of CO2, at $14 per credit, someone is subsidizing the credit – maybe those planting the trees. The chart below shows carbon values at the end of December. See our ESG and Climate report No 57 for more.

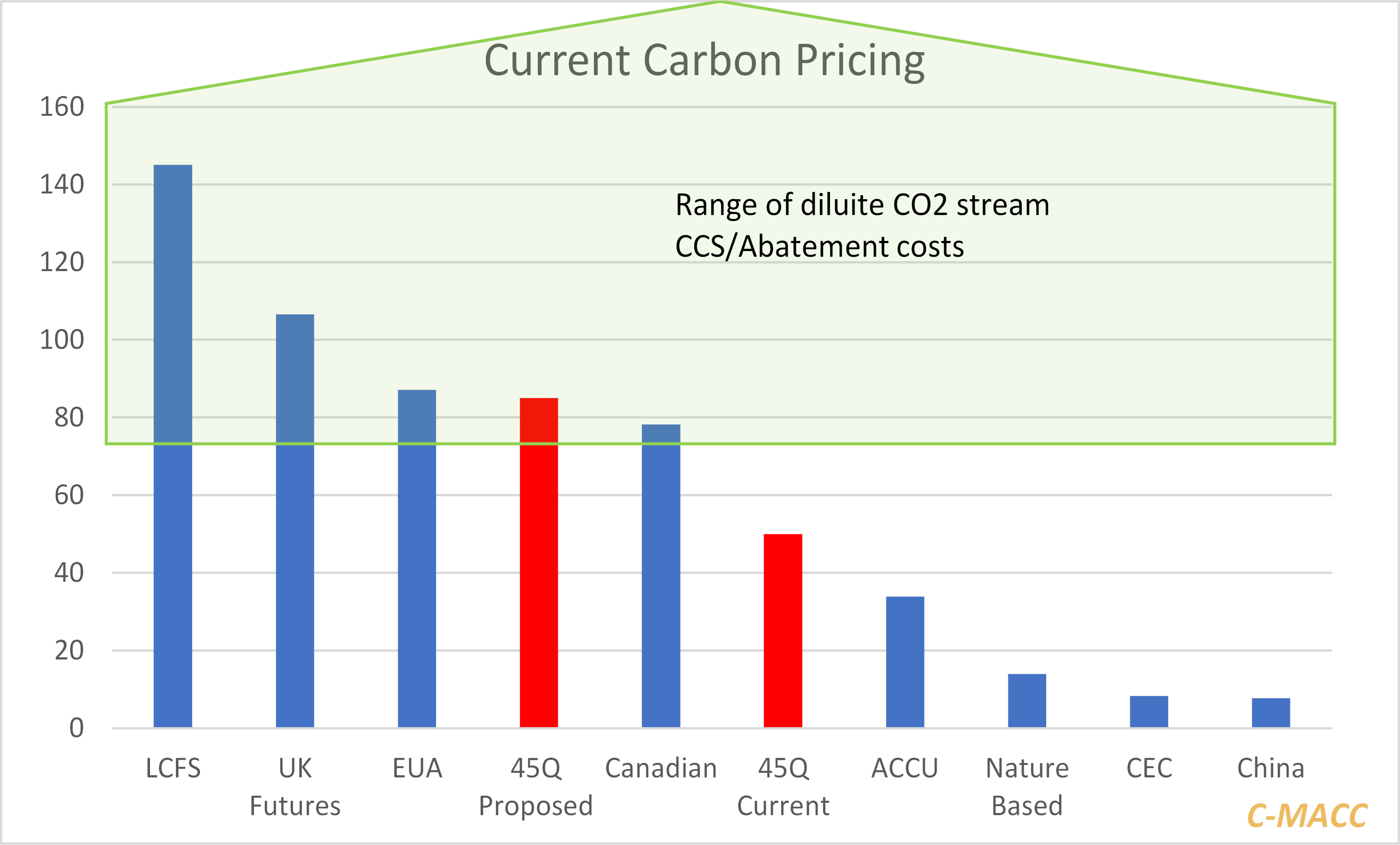

As the chart below shows, there are some very wide ranges in carbon prices today, with only the European price (and only this year) reflecting an approximation to the cost of physically abating carbon dioxide emissions. We cover carbon values in detail in our focused ESG and Climate work and have been suggesting since before we began the dedicated service that it will take an incentive of around $100 per ton of CO2 to get the acceleration of investment needed for CCS to play a major role in emission abatement and perhaps high levels than this for alternative heating technologies than furnaces to makes sense in areas where CCS is not an option.

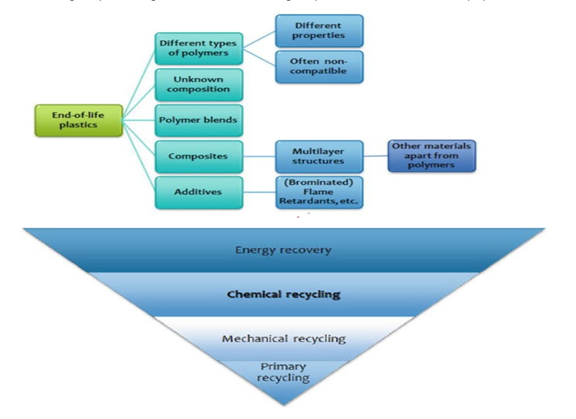

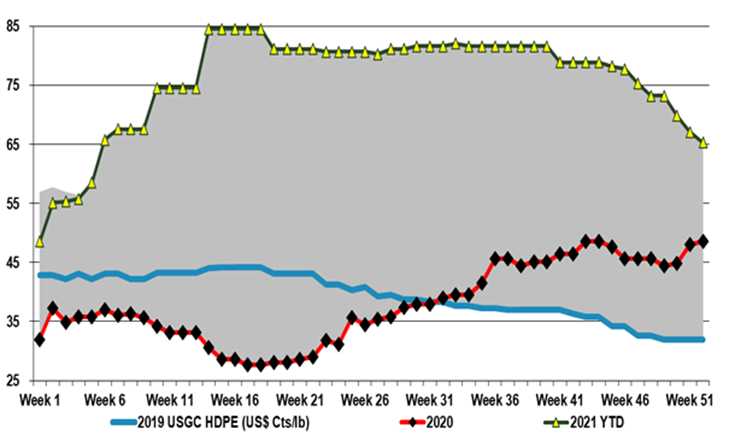

In our ESG and Climate report today we discuss whether plastics recycling and substitution from renewable polymers could take a breath in 2022, in part because of falling virgin polymer prices and in part because of cost inflation around new investments. Packagers, especially those who have been prescriptive around how much recycled/renewable material they plan to use by 2030, cannot afford for the pace of development to slow, but there is not much they can do about it. The polymer industry is pushing chemical recycling and has the balance sheet to keep pushing chemical recycling investment while the independent mechanical recyclers may be forced to pause. The packagers will need to endorse the use of chemically recycled material as the share of plastic waste moving in this direction increased. Complicating things further, there are two headlines today - linked here and here - that talk about plastic waste to hydrogen processes. These add to the Fulcrum Bioenergy facility starting up in Nevada and a second one planned for Indiana. These waste to hydrogen plants will take plastic waste out of the system (which is good) but there will be no ability to prove a chain of custody back into virgin resin as there is with chemical recycling. At some point, we believe that packagers will need to pivot and endorse both chemical recycling and low carbon polymers as an alternative to strict recycling targets. We would add the caveat with the waste to hydrogen processes that there is still a lot of learning curve to travel on large scale waste gasification – Fulcrum is a year late with its facility and not yet operational – the newcomers highlighted in the links are not guaranteed a smoother path.

In our ESG and Climate Piece tomorrow we will look at the impact on plastic waste initiatives of falling virgin polymer prices. If recycling initiatives stall – especially the more expensive mechanical piece – it will likely add to concerns that packagers already have around whether they can get enough material to meet their public goals on recycled content. If it then also looks likely that new materials – renewable based on biodegradable - may be either late to market or more expensive than anticipated the door opens wider for the chemical recycling advocates and also for alternative materials. The chemical recyclers also need collection and sorting to improve, but the more complex/forgiving the facility, the less rigorous the sorting needs to be. Also, this route is somewhat agnostic to the price of virgin polymers as the output is competing with fuels and chemical feedstock values. For chemical recycling to be economic, the price of crude oil must remain high. For chemical recycling to get the lion’s share of recovered plastic waste the price of oil needs to be high and the price of virgin polymers low – discouraging mechanical recycling. While this may spur more chemical recycling, the net effect of low virgin polymer prices would overwhelm the benefit of better recycling economics for the majors – many of whom make up the bulk of the existing and planned chemical recycling capacity today. That said, the more plastic waste that ends up in chemical recycling, the less of an impact there will be on virgin plastic demand

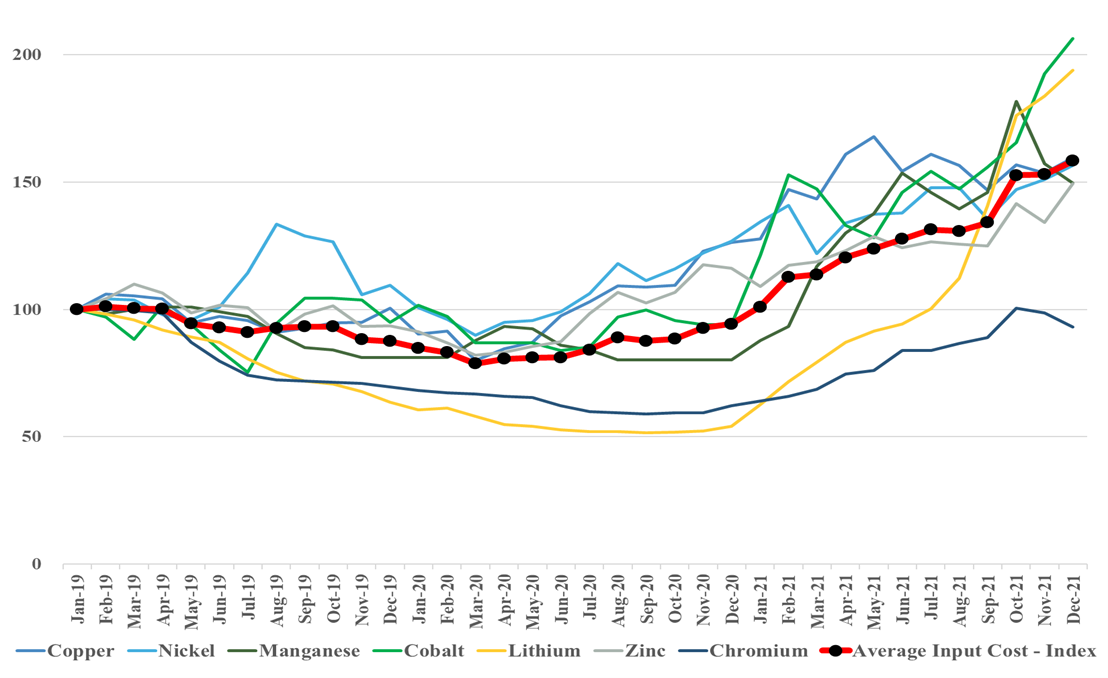

Continuing with our inflation theme this week, we show our renewables metals price index in the Exhibit below, which continues to climb and is now 50% higher than it was 2 years ago, with cobalt and lithium leading the charge at around 100% higher. These are critical components for EV and renewable power manufacture, and with 2022 forecasts for all suggesting much stronger growth, we do not see the materials supply/demand balances improving, suggesting that pricing will go higher. Energy shortages today, will only add more upward pressure to build more renewable capacity quickly and add even greater inflation risk to both components and the materials used to make them. We are concerned that, on the list below, only lithium is seeing significant capital thrown at increasing availability, suggesting that while lithium may peak in pricing, other metals could keep marching up. See our recent Daily, ESG Report, and upcoming Sunday Thematic for more.

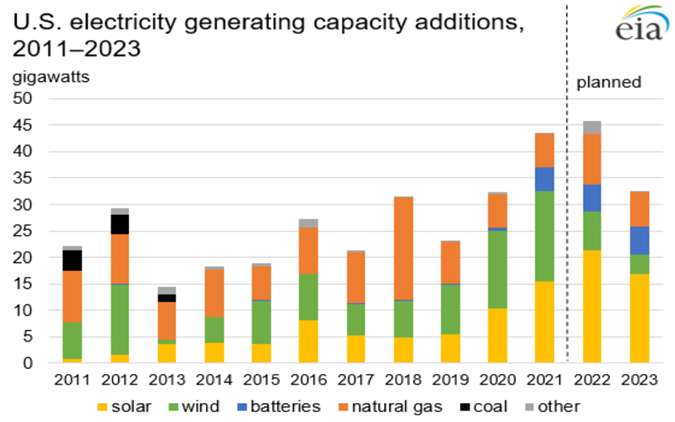

In our ESG and Climate report yesterday we highlighted inflation as one of the most significant risks for 2022 and the estimates in the exhibits below do not leave us any less concerned. The US has struggled to meet solar installation plans for 2021, falling short of early-year estimates because of limited equipment availability and higher equipment prices. While some of this has been the result of the supply chain challenges of 2021, some shortages have also been the result of very strong global demand. The idea that we can increase solar installations in 2022 without creating more supply issues (and more inflation) should be questioned, especially in light of planned additions in China, which will consume an increasing share of Chinese solar modules.

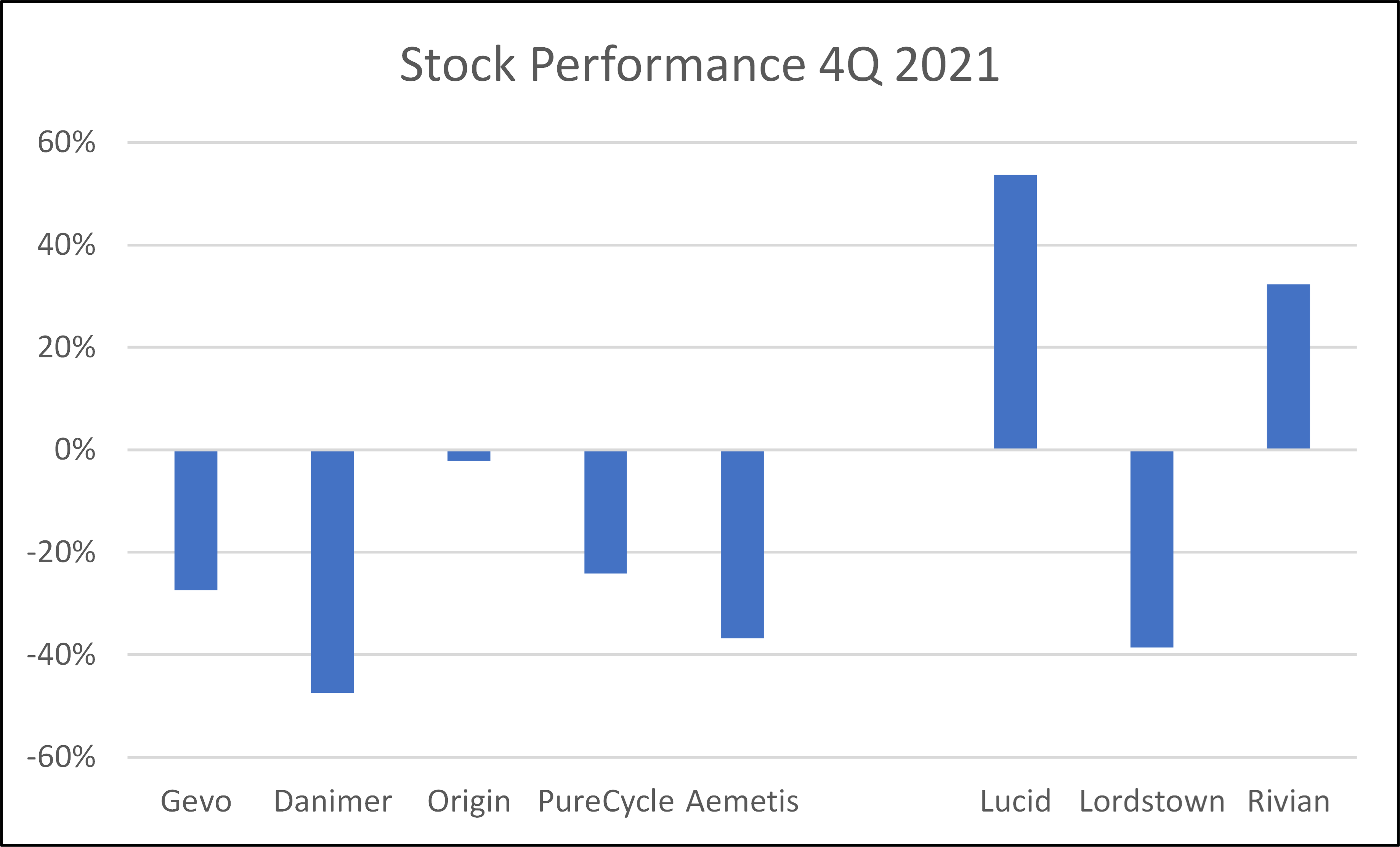

Life in 2022 is likely to be tougher for the new companies in materials and fuels, as all of them need capital to support projects that now look riskier from a cost inflation perspective and the market has moved to reflect that risk – Exhibit below. For every company below, the 2022 story was supposed to be capital spending to create commercial-scale production. The poor stock performance for many has tracked rising raw material prices – especially steel – as well as concerns around supply chain-driven delays and labor shortages. Few have the financial capacity to absorb significant cost overruns and/or construction delays. Danimer Scientific has done a recent capital raise and its impact created roughly half of the downside shown below – Danimer still likely needs more capital, but with more cash on the balance sheet may be able to get the rest through loans. Gevo, which in our view has the more impressive portfolio of potential offtake partners at this point likely plans to borrow at the facility level, and the stock weakness is likely a combination of inflation fears, the declining LCFS value, and the wait for the company to announce that it has a completed FEED study for the first plant and has reached FID. We would struggle to invest in any of these names today given the step-change in company development that each needs to make in 2022, and we would need more offtake agreements and process/construction guarantees than any company can likely get today, and if they could, they might not want to make some agreements public. See more in today's ESG and Climate report

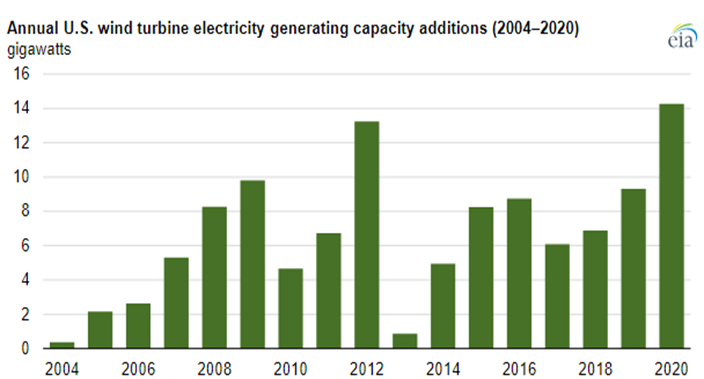

It should not be surprising that 2021 has seen a rebound in emissions as nothing has changed fast enough over the last 24 months in terms of renewable power additions and carbon abatement to offset more than the underlying growth in power demand, and based on what we are seeing in European and Asia LNG markets, we have fallen short of demand growth. The wind capacity chart below has one main conclusion – not enough. One of our main inflationary fears for 2022 is that both wind and solar installation rates need to step up meaningfully from current levels to make a difference – the IEA suggests that installation rates need to double (at a minimum). It has already proven difficult to meet installation targets in 2021, in part because of supply chain issues but also in part because of material shortages, all of which have led to rising installation costs, against the longer-term run of falling costs because of learning curve gains. We believe that costs will rise again in 2022 and 2023 as installers/projects compete for limited solar module and wind turbine components

In yesterday's ESG and Climate report, we looked at an extreme example of how the right support for clean fossil fuel use through a long period of energy transition, could create economic growth, support job growth, and not require subsidies – coal gasification to produce low-cost hydrogen. With the opposition to the “Build Back Better” bill, there is a clear opportunity for the fossil fuel industry to step up and suggest compromises, and we are seeing increasing interest in large scale CCS, despite its cost, in part because it is a path that will allow natural gas and other fossil fuels to meet increasing demand in a way that has a much lower carbon footprint, and in part, because it will still be cheaper than some of the heavily subsidized ideas to try and accelerate investments in renewable power that will inevitably fall foul of equipment and material shortages – something we have written about at length in past research – linked here. The EIA has already noted that coal use in 2021 has risen globally and it is likely that it will rise again, given the increasing demand for electric power and the lack of supply elasticity in the renewable power and natural gas-based systems – coal is a large part of the swing capacity these days. Many of the CCS projects proposed for the US are not much more than proposals today, but we are seeing some initial investment to prove that subsurface storage opportunities are feasible.

While we would generally avoid quoting work from a company that we might consider a peripheral competitor, we are happy to do so when it backs up one of our central themes – in this case, inflation in renewable power costs. The quote is taken from the Wood Mackenzie report flagged article linked here and discusses a view on how challenges that renewable power installers have faced in 2021 will extend into 2022. The quote talks about shortages of renewable power equipment, and the obvious consequence will be higher prices for that equipment, especially as raw material prices for components remain high and possibly move higher. In our ESG and Climate report today, we talk about the need for some commonsense oversight such that impractical ESG investing targets do not limit the ability of producers of critical fuels and materials to operate.