There are two elements/risks to ESG investing and both are highlighted in articles in today's daily report. The first is a reminder that returns matter and this is a reference to the very high multiples that are being applied to some of the more speculative clean energy stocks where there is credit being given today for technology and scale tomorrow. As with the tech bubble, there will inevitably be companies that fail, either because they have an offering that either will not work or will not be economic or because the market moves away from what they are doing. The fuel cell stocks would be at risk if hydrogen remains too expensive to consider as a transport fuel and if batteries or bio-based fuels become the dominant solution. Equally, bio-fuels could fall out of favor if hydrogen is abundant. On the polymer side, better collection and more chemical recycling could make switching to biodegradable polymers unnecessary or uneconomic. There will be winners and losers on this basis and the better strategy is to buy baskets of new technologies rather than bet on just one.

Our meetings over the last couple of weeks confirm several developments within the ESG investing world, all of which have been the focuses of our prior work. The first is a very significant step up in ESG oversight among most fund managers, with dedicated ESG teams at many companies scrutinizing sustainability reports and other releases, looking for red flags either from inconsistencies in reporting or from departures from the fund managers standards. Second, there remains a lack of real empirical analysis that allows for accurate comparisons between companies and this stems from the fuzzy reporting frameworks that we have today and the lack of clear and actionable guidance from regulators. As we have discussed several times, the huge inflows into ESG funds and the proportion of overall funds market that now has a “social impact” overlay could lead to real disruptions and some rapid valuation changes if and when the regulators provide tighter guidance on both corporate reporting and fund labeling.

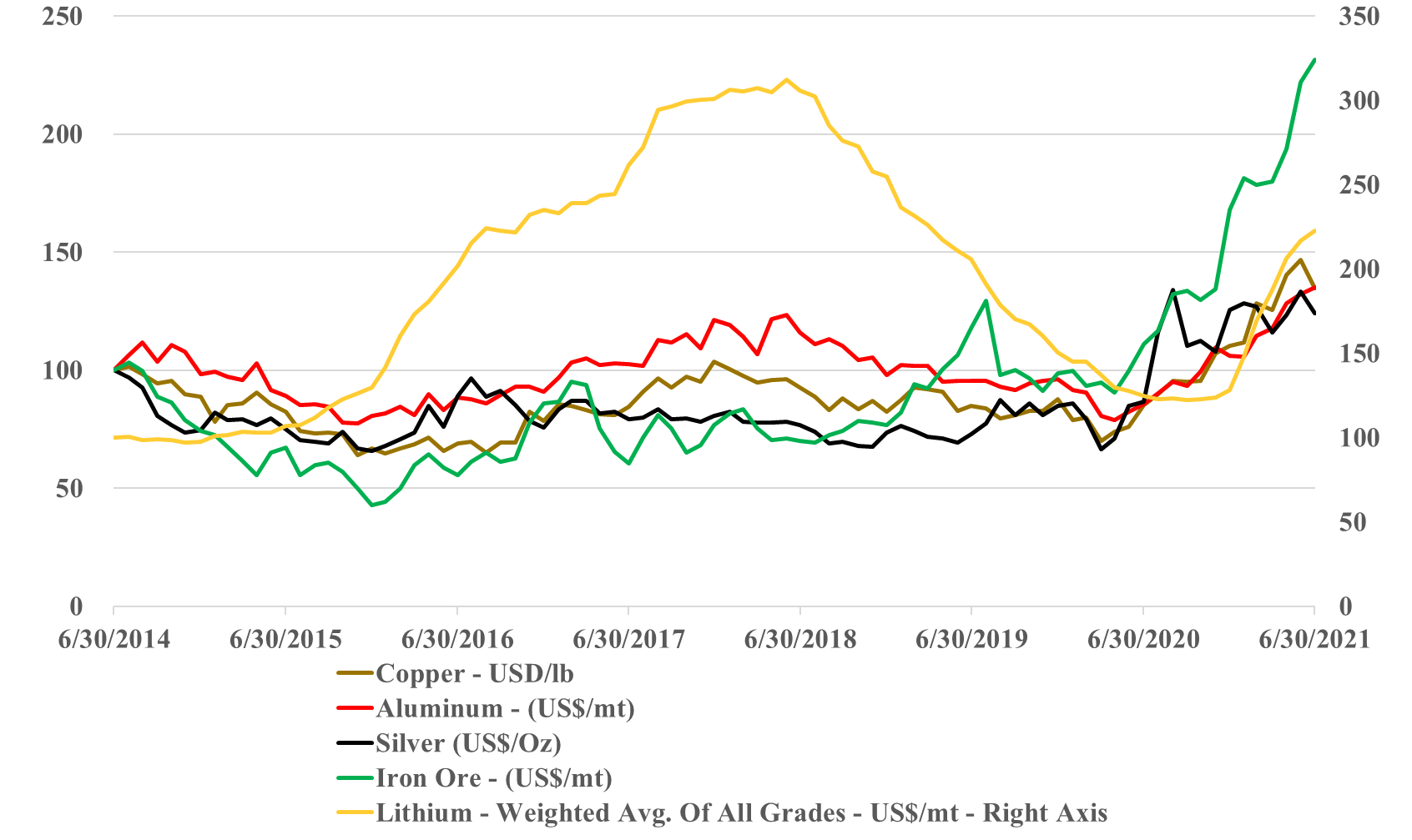

One of our concerns with the Lithium hype has been what we perceive to be very low barriers to entry – coupled with significant momentum from lithium ultimate end-users to encourage more production. If we look at the linked GM announcement, the company is making exactly the right strategic move. Providing some funding, but more importantly, high-level credibility for a new US-based project that could dwarf other US initiatives. While GM may have contracted all of the lithium volumes from this project, it is unlikely. GM’s interest, which should be aligned with all the other automakers is to ensure an ample to surplus availability of lithium long-term to keep pricing low. Investing a few million to give legitimacy to a new large project may have huge potential longer-term benefits if the capacity helps maintain a longer-term surplus market. While there may be some special sauce in the technology required to make the lithium grades for higher-end and higher density batteries, the bulk of the auto market is likely to trade range for cost in its battery decisions – and at the less expensive end, the lithium barriers are very low, with other brine-based projects under consideration and likely to find funding.

There have been some disappointing headlines out of the UN climate meeting this week, which is intended to pave the way for some of the COP26 discussions and come up with proposals that are likely to be agreed upon at the meeting. Most of the issues are around who is paying for what and whether developed nations are investing enough to help developing nations, using the guidelines put forward when the Paris Agreement was signed. In the US, the climate agenda and the Biden plan are bogged down in Congress and the plan is unlikely to pass in its current form.

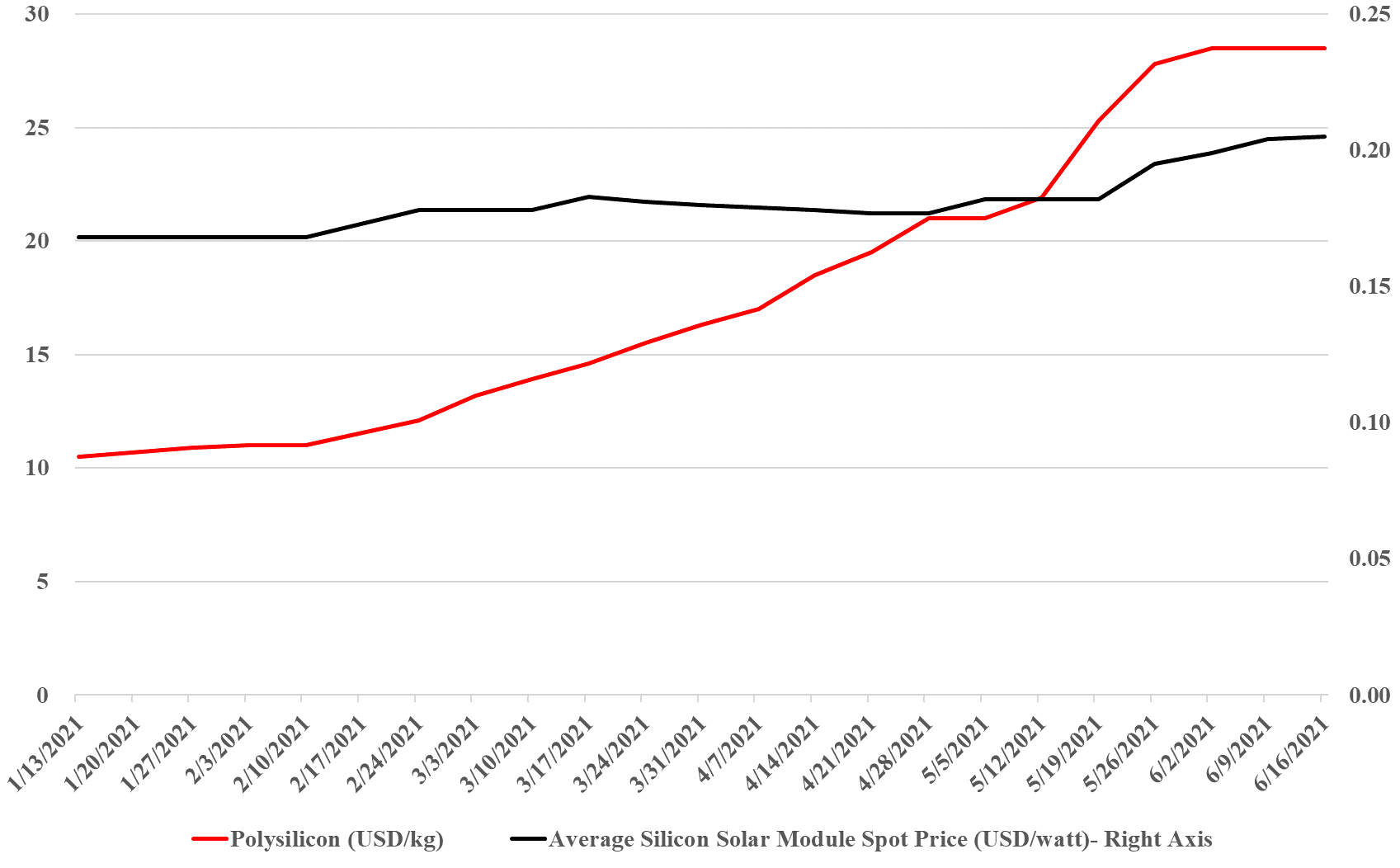

The exhibit below summarizes well one of the primary concerns that we have with some of the very ambitious goals for decarbonizing power grids, EV introduction, the further electrification of industry, and hydrogen. While the solar module price increase does not look that significant (yet), to put it in context, solar module prices have collapsed from over $1.80 per watt in 2010 to below $0.20 in 2020, and many of the expectations around cheap hydrogen require the cost to keep falling. The bigger concern is the polysilicon price, which is up 160% this year, good for the polysilicon producers like Wacker (see the headline here), but bad for the solar module producers, who are seeing major margin squeezes, especially given the rise in copper and silver as well this year. The raw material pressure should drive further increases in solar module pricing and while the higher margins for polysilicon will likely drive expansion investment, the metals are harder to call, given the ESG views on mining. We remain firmly of the view that raw material availability and price inflation, as well as module and wind turbine manufacturing capacity, will be the rate-determining constraint in terms of the growth in renewable power and this is why we question all of the near-term cheap power and cheap hydrogen goals that are being suggested by potential producers and government agencies.

The WSJ article linked talking about rising ESG spending and the risks associated with it is in no way inconsistent with our view that lack of US Government guidelines is constraining ESG spending. The article focuses on the power and auto industries, which, while they face regulatory and incentive uncertainty, have a much clearer path than many others. The power industry is dealing with a customer which is increasingly asking for more renewable power, an investor base that is pushing for less reliance on fossil fuels, and a Government that is pushing for a 50% emissions reduction from the sector. The auto suppliers have clear directives from some US states and some countries about the phasing out of fossil fuel-based vehicle sales, and in some geographies, they have incentive systems that they can tap into. For both industries, there is a significant risk, in that the billions of dollars that they are investing in new plants and new equipment do not come with any guarantees that those investments will pay off well or quickly, but at least the direction of travel is unlikely to change. In other words, there will be demand for their products and investors will likely be happy with the progress – while they might not get the EBITDA they would like, they may get a better multiple of that EBITDA.

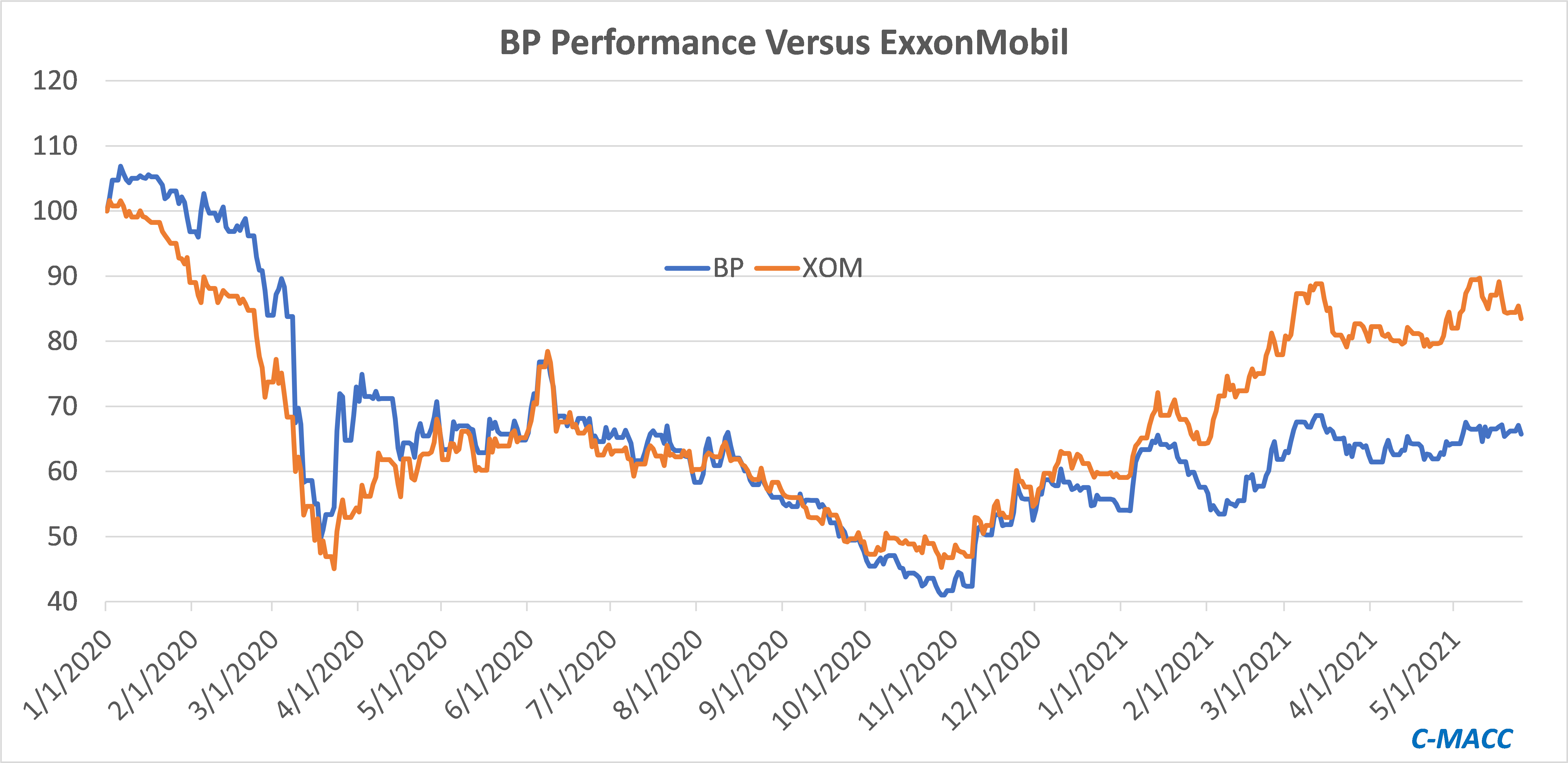

With little chemical corporate news of note, we will focus on ExxonMobil today. The shareholder activism may be high but it is unclear to us what the activists hope to achieve, even if they are successful at the annual meeting. The ESG investment group has largely given up on energy and even if ExxonMobil changes strategy and agrees to spend more on carbon abatement it is unlikely that new investors will show up, especially if the new strategy is more costly. Despite all of its directional change and rhetoric, bp has underperformed ExxonMobil since Mr. Looney took the helm in early 2020. If ExxonMobil were to follow the bp playbook, it is not clear that shareholders would benefit.

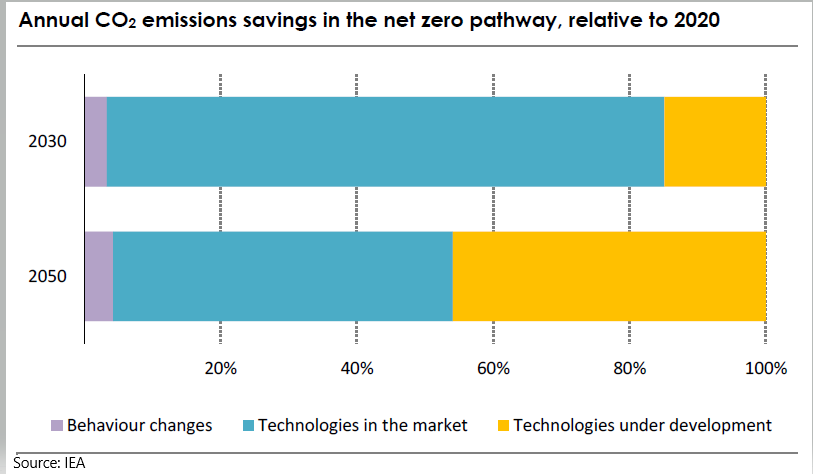

There are too many important topics to choose from today and we will cover many of these in our ESG and Climate report tomorrow. Here we focus on the IEA report published this week, which shows a path to net-zero on a global scale and looks at both the fossil fuel consuming sectors and the rate at which each must change (they are different by sector) and what fuel alternatives will be needed to replace them. Our review of the work would suggest the following:

We have decided to change up our blogs, at least once a week and each Friday, to pose a question rather than throw out opinions.

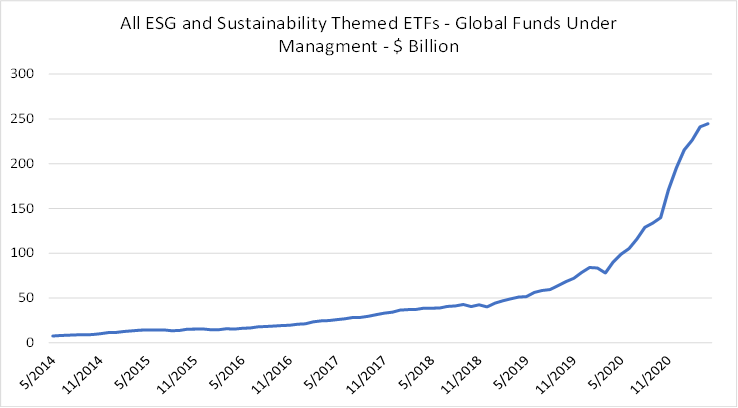

Today we should focus on the very good FT article linked here, which discusses in detail many of the issues facing both ESG investors and corporates concerning the lack of standards in ESG metric providers and the data provided by companies. It is a subject that we have been writing on for a couple of years – before C-MACC – because it is a potential dark stain on ESG investing and has turned (in some cases) a progressive move by the investment community into something that lacks a clear standard empirical base and is currently open to manipulation. The article highlights the ability of corporates to change the ESG metric providers that they use for internal measures and external reporting based on which provider sheds them in a more positive light. It also allows ESG funds to hold stocks that other ESG funds would not because they are not working off the same definitions. The flow of funds into this segment makes oversight critical (see chart below).

We would like thoughts, in the hope of starting an interesting dialogue on what you think the primary role of an ESG fund manager should be – to maximize returns, to promote change, to attract funds, etc.

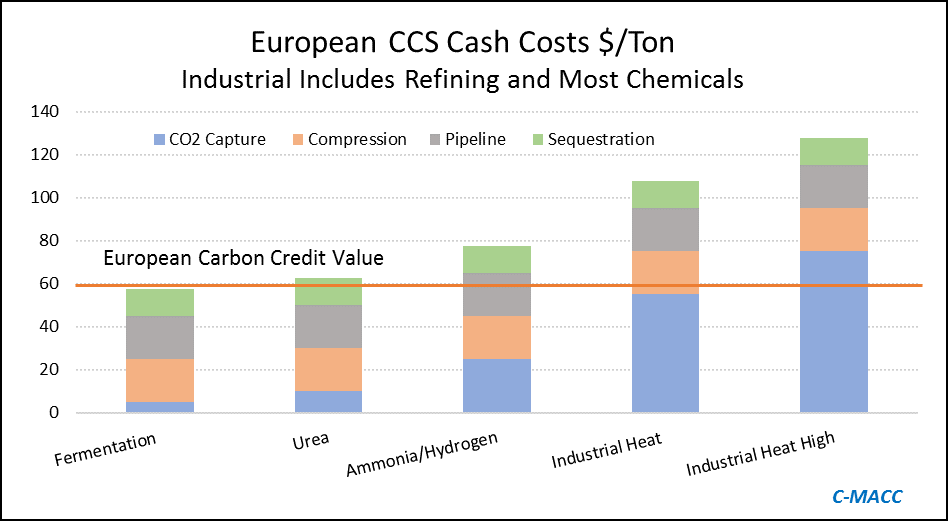

The big news of the week is the massive grant that the Dutch government approved for an offshore carbon capture project that will be focused on the operations of Shell, ExxonMobil, Air Products, and Air Liquide. This looks to be localized within the Port of Rotterdam, where both oil majors operate large refineries, Shell also operates a large chemical site and the industrial gas companies have significant hydrogen capacity. The Dutch government believes that the country cannot achieve its emission goals without carbon capture as it has one of the largest refining and chemical footprints in Europe and the $2.4 billion grant (likely achieved through a series of subsidies) is an indication that the country is willing to invest to make its emission goals a reality. The grant is likely aimed to help close the gap between the current European carbon price – which is just over $65 per ton today and what is estimated to be the full cost of capture and storage under the North Sea, which the linked article suggests is closer to $100 per ton, but this likely underestimates the capture costs – see chart below - even if the CO2 streams are pooled and treated as one stream. Interestingly, despite the high level of subsidy, this project is estimated to store only 2.5 million tons a year and will only last 15 years (likely because of the capacity of the offshore reservoir). For more see today's ESG report.

Source: Global CCS Institute and C-MACC Analysis and Estimates