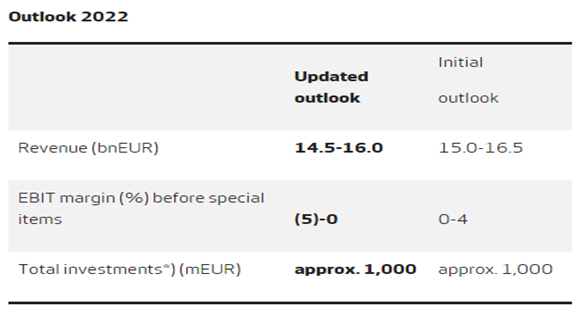

We discussed the woes of the wind power industry at length in a dedicated ESG and Climate piece last week, and the Vestas results below play into the same theme. The company is cutting guidance again for 2022, which is already much lower than estimates would have suggested 6 months ago. While Siemens Gamesa has the added headache of a mismanaged platform change, all of the issues raised by Vestas are shared industry wide, delayed installations because of supply chain issues and material shortages, as well as significant cost inflation. In tomorrow’s ESG and Climate report we discuss some of the increases in European PPAs in 1Q 2022, reversing a multi-year trend of lower installed costs of power. This reversal will likely impact plans for 2022 and 2023, especially for those banking on lower power costs to justify many of the announced hydrogen ventures – particularly in Europe. Those who press ahead despite higher power costs and higher construction costs in general, may stretch both balance sheets and borrowing capacity.

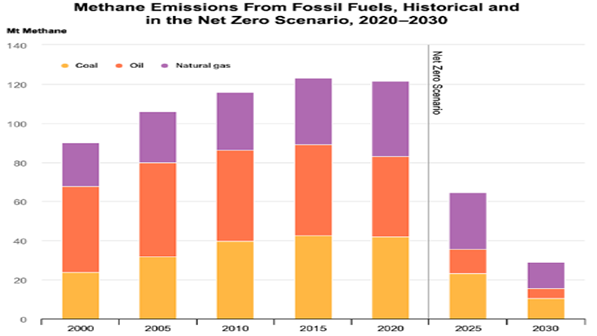

Methane emissions are one of the more challenging carbon equivalent problems in part because it is lots of small emitters, associated with many thousands of wells and many thousands of miles of pipelines, rather than a large source of CO2 that can be eliminated with a specific investment. The API carbon tax, proposed last week, has a condition in the proposal that would prevent any other emission-based legislation for many years to evaluate the effect of the tax. This will not drive lower methane emissions unless it is a broad carbon “equivalent tax”, which could potentially drive a very punitive tax on methane and would get an almost instant response from those that own the wells and the pipes. Some of the abatement solutions are easier than they first appear and all pipeline operators should look at the technology offered by Pipeotech, for example. Wellhead emissions are more problematic but not beyond the engineering skills that exist within the major E&P companies. The harder problem is what to do with emissions from abandoned wells – here the tax idea would not work as there is no one to pay the tax and a fairly complex financial structure would be needed to encourage someone to take on the role of cleaning up these properties. That said, all these pathways will need to be explored to get to the targets outlined below.

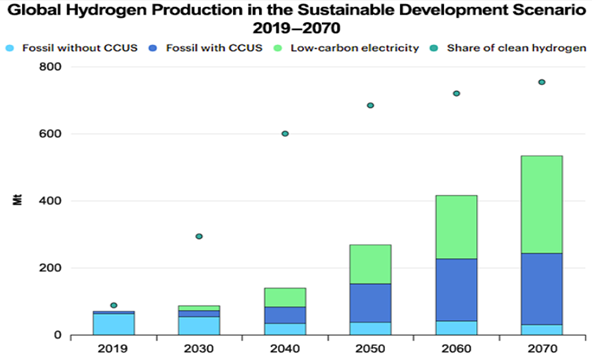

Anyone who read our ESG and Climate reports of the last two weeks will know that we do not believe in the hydrogen projections below as we see renewable power as a potentially scarce resource. Furthermore and also covered yesterday, should the API be successful with its carbon tax proposal in the US and should this be additive to the 45Q incentive for CCS, we could see an explosion of blue hydrogen investments in the US, especially on the Gulf Coast.

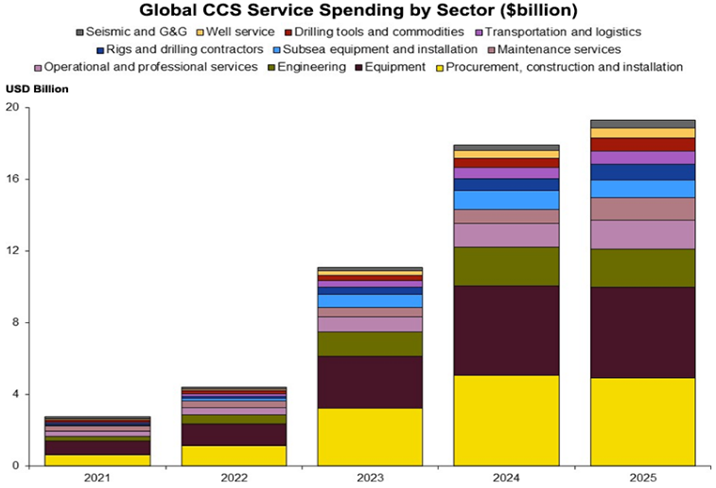

The CCS spending chart below is quite detailed, but shows the limited amount of spending in 2021 and 2022 and may underestimate the amount of seismic spending needed, especially in the US, as companies prepare permit applications. We do not expect to see much spending in the US before mid-decade beyond permit applications. However, as we discuss in today’s ESG and Climate report, should the API proposed carbon tax, or something similar, be additive to the 45Q tax credit, we could see a step-change in CCS when/if the tax is approved. The tax on its own is likely not enough to drive decarbonizing investment, but when added to 45Q it could be a specific trigger for CCS investment, and we could see a step-change in the second half of the decade. This might involve large-scale blue hydrogen production, especially on the Gulf Coast to decarbonize the refining and chemical industries.

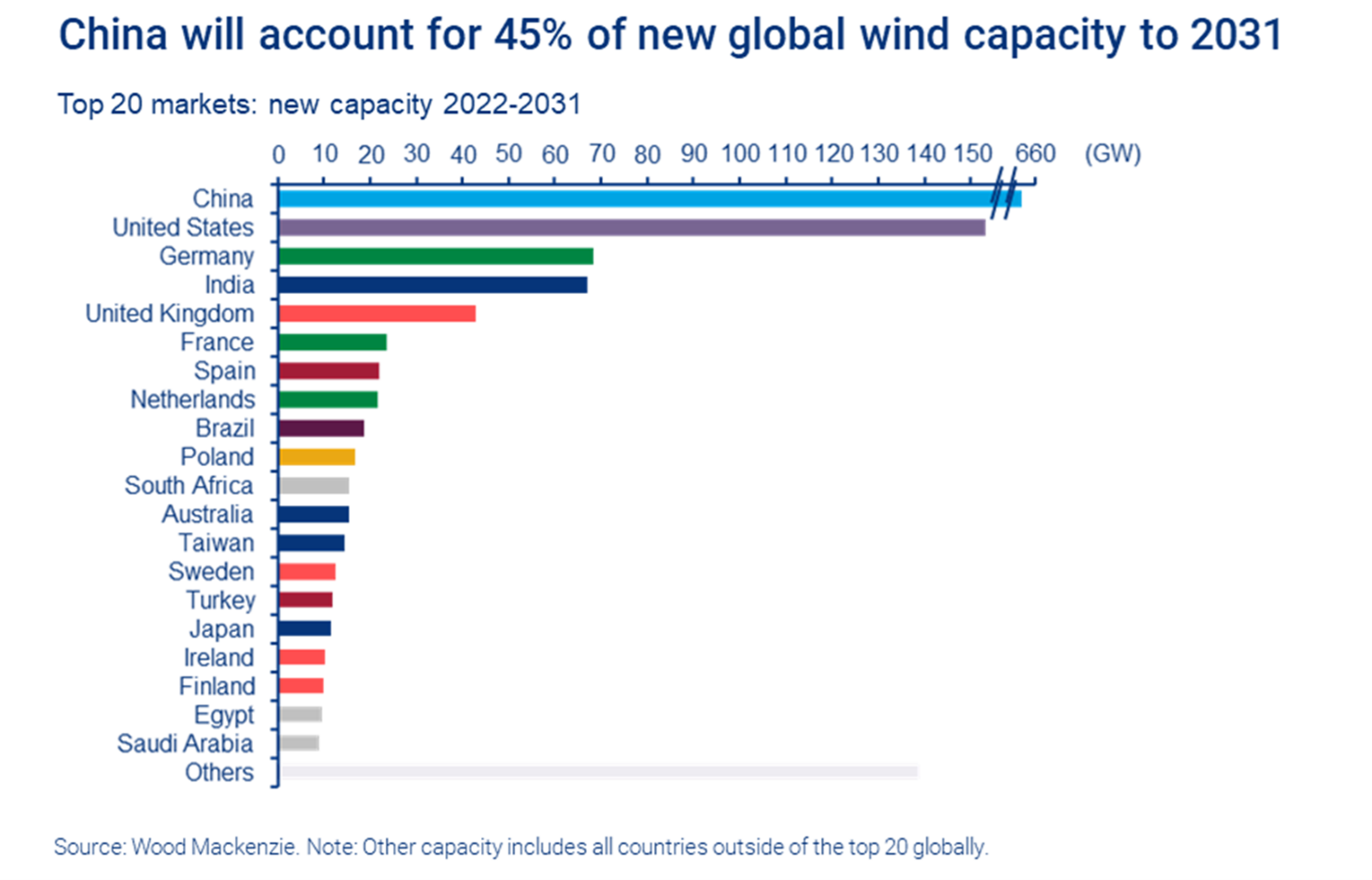

In our ESG and Climate report tomorrow we are focusing on the wind industry and specifically the problems that Siemens Gamesa is facing with execution, costs, and logistics. The estimates for China and the rest of the world in the chart below assume a significant step-up in the rate of installation, and in 2022 we are seeing an industry that is struggling with that. Siemens Gamesa is having problems with its new platform, which had been intended to deliver projects more cheaply from an installed cost basis and an operating costs basis and is perhaps an illustration of what can happen when you are trying to move too quickly – partly because your customers are demanding it. Operational problems at Siemens Gamesa have been compounded by logistic challenges and raw material price and availability, such that current expectations are for the company to break even at an EBITDA level in 2022. This is another great example of the policy and investor disconnects that we see in several aspects of energy transition – we are encouraging investment in front line capacity, but not in the materials and feedstocks needed to feed the front line – metals, natural gas, crops. See our recent body of ESG and Climate work for more on this. These subjects are at the heart of many of the private engagements that we have with several clients in this space.

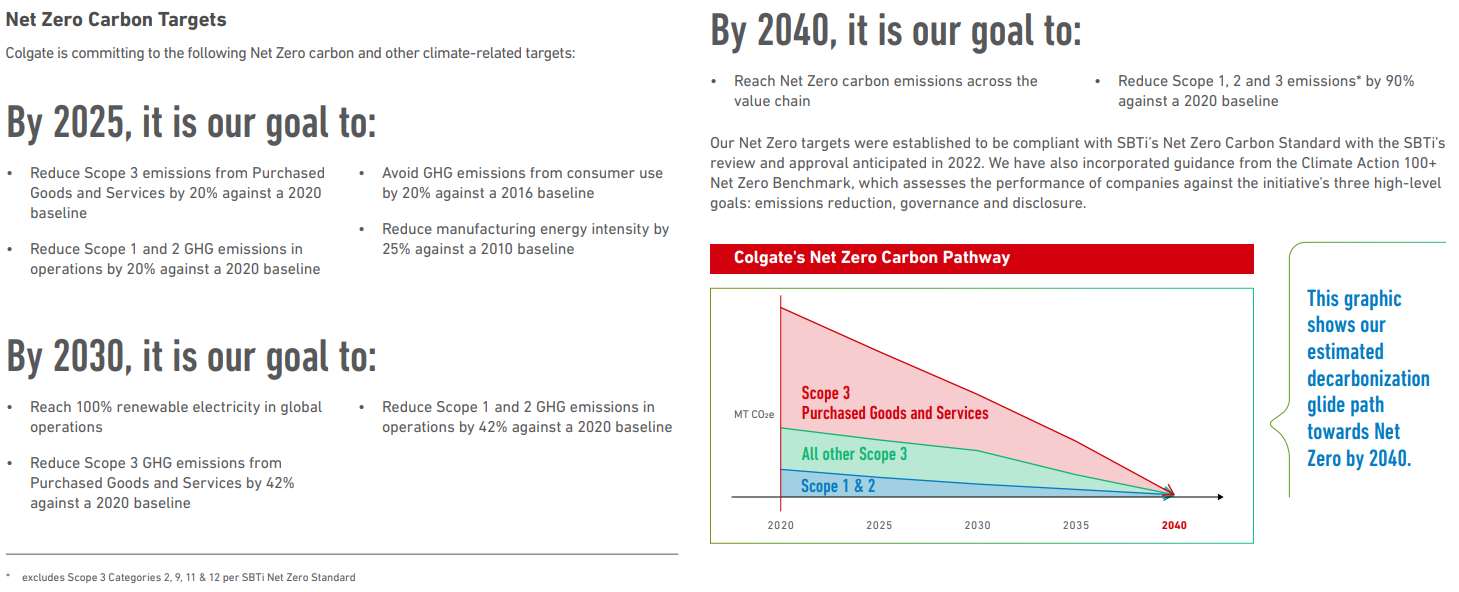

The Colgate Palmolive sustainability and social impact report is very comprehensive, and we like the comprehensive inclusion of water security towards the end. The challenge for all corporates that set goals like those outlined below will be the elements that they cannot control – something we discussed at length in this week’s ESG and Climate report with a focus on sustainable fuels. We cannot pursue renewable power as fast as we would like without supportive policy around materials investment – Colgate Palmolive will not be able to get to 100% renewable power by 2030 if it is either not available or prohibitively expensive because of competition. The company will also not be able to meet its sustainable materials goals of the sustainable goals that need to come from crops. We do not have a radically different farm policy. The goal to achieve 100% recyclable reusable or compostable plastic packaging by 2025, is very ambitious and has some negative ramifications for the compounders, who will likely lose volume, and positive ramifications for compostable polymers.

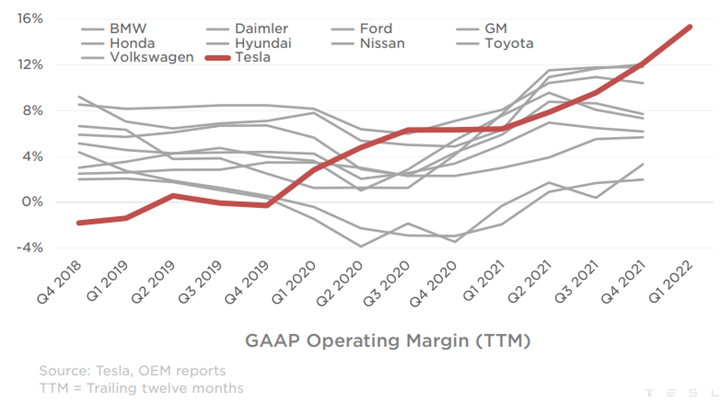

Tesla is on a roll, and showing other EV makers what is possible. The company priced its vehicles to be profitable at lower volumes and is currently seeing the benefit of scale, likely to be enhanced further as the manufacturing footprint grows. While the operating margin below looks very good, we would note that Tesla is not done scaling yet so there is considerable upside to the margin, most likely. One obvious conclusion from this analysis is that Tesla has plenty of wiggle room on pricing should macro conditions impact new car sales or should other EV makers try to steal share with pricing. Tesla has built a huge first-mover advantage in EVs and this will likely benefit the company for many years to come as long as they keep making vehicles that people want.

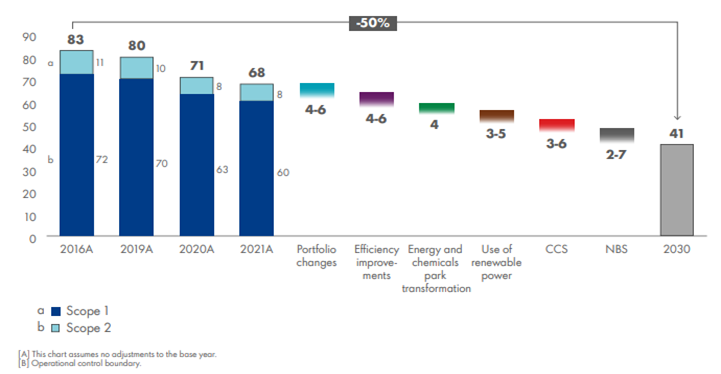

Shell issued its 2021 energy transition progress this morning and the report contains a lot of detail about what Shell has done so far and what the company intends to do. The report is a record of progress and intent and is targeting both general stakeholders as well as the Shell board and annual meeting, where approval of the plan will be sought. When compared with other reports we have seen from other companies, this summary is comprehensive. It provides some concrete steps to achieving emission goals in 2030 – exhibit below - while remaining appropriately vague about getting to 2040 and 2050 targets. However, we would note how much portfolio changes likely added to the 2016 to 2021 progress – likely proportionately much more than they are expected to contribute from 2022 to 2030. Both renewable power and CCS figure in the 2030 projections below and Shell will need to get moving on the CCS front of it is to sequester 3-6 million tons of CO2 per annum by 2030. The expectations are likely based on the European offshore projects, as it may take longer than 8 years to get permits and investments in place in the US. The US could move faster but the EPA would likely need to grant primacy to at least Louisiana and Texas for things to speed up and we are not convinced that this will happen soon. Like many of the other company 2030 plans that we have seen, it is likely that much of Shell’s progress will come in the last couple of years of the decade – especially on CCS.

In our ESG and Climate report tomorrow, we will focus on SAF from a carbon intensity perspective. The Colonial pipeline initiative was inevitable given the demand for jet fuel at the East Coast airports. Still, we would not expect much volume to move in the near term for several reasons. First, there is not that much to move, and second, California can still pay more because of the LCFS credit. The Biden administration is planning to introduce a broad SAF credit which would help encourage use outside California, but this would also need to stimulate production as the volumes are still small and much smaller than the airlines would want – even the projection of volumes by bodies like the IEA fall well short of potential airline demand by 2030 and 2040. This is an investable theme, in our view, and we will discuss it in more detail tomorrow.

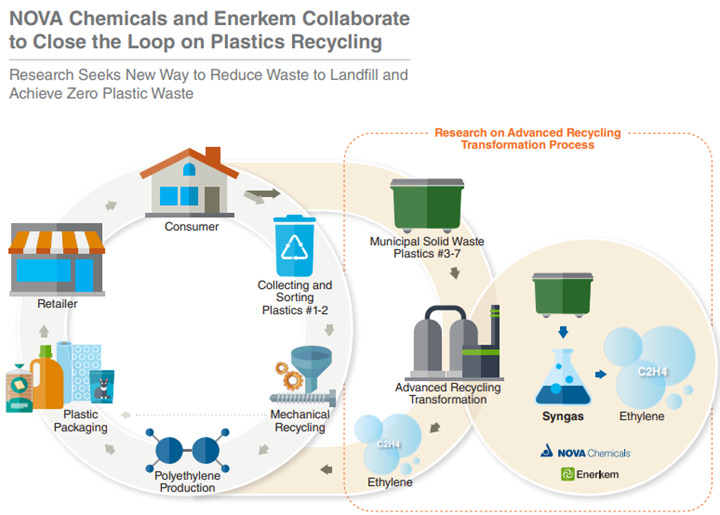

As we look at the news flow on recycling, we see many initiatives to collect, sort, and reuse polymers, whether for like-for-like applications, pyrolysis, or energy. What we do not see enough of, in our view, are initiatives to increase the pool of recycled plastics through packaging standardization or the elimination of compounds or colors that make recycling more challenging. Recycling can be improved by better collection and sorting methodologies and technologies. Still, the rate-limiting step will eventually be the pool of materials fit for recycling, and this is particularly important for like-for-like mechanical recycling. The ironic piece here is that the consumer staples and beverage companies call for higher recycled content and are primarily responsible for the amount of recyclable material in the market. If the packagers were to focus on sustainability rather than the unique look and feel of their packaging, we would see a material change in the volumes of recyclable polymers. This might come at the expense of some of the compounders, especially those with an extensive packaging component to their customer base, but it might also impact specific polymers and we would highlight polystyrene as a particularly vulnerable material as almost any application for which polystyrene is used today could be replaced with PET, polyethylene and/or polyethylene – all of which are larger volume polymers that are easier to recycle. The polystyrene industry is doing a good job of promoting recycling initiatives, but this may not be enough.